Europe Pediatric Neurology Devices Market Size, Share, Trends & Growth Forecast Report by Product (Neurosurgery Devices, Neurostimulator), by Service and Treatment (Electroencephalogram, Intrathecal Baclofen Therapy), by Neurological Specialty (Neuro-Oncology, Neuromuscular), by Age Group, by End User, by Application, and Country (Germany, UK, France, Italy, Rest of Europe) – Industry Analysis From 2025 to 2033.

Europe Pediatric Neurology Devices Market Size

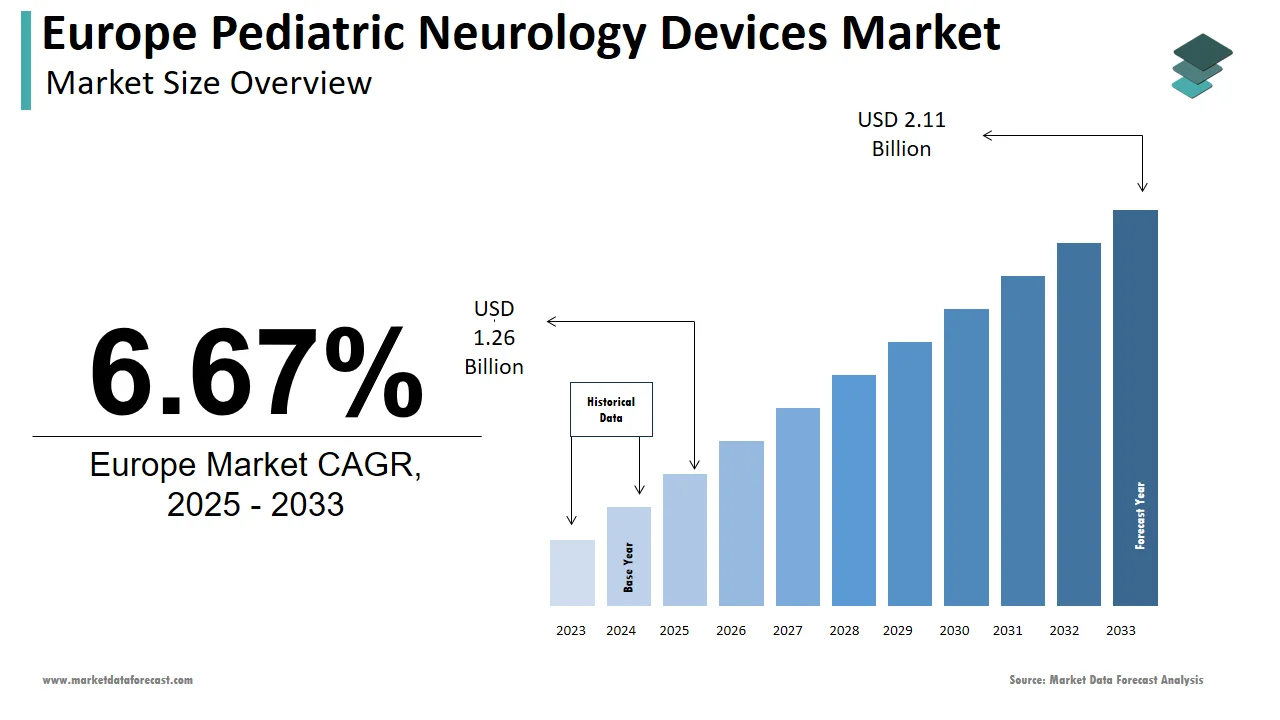

The pediatric neurology devices market size in Europe was valued at USD 1.18 billion in 2024. The European market is estimated to be worth USD 2.11 billion by 2033 from USD 1.26 billion in 2025, growing at a CAGR of 6.67% from 2025 to 2033.

The Europe pediatric neurology devices market is witnessing steady growth driven by advancements in medical technology and an increasing prevalence of neurological disorders among children. A report by the European Federation of Neurological Associations states that nearly 12 million individuals in Europe suffer from rare neurological conditions is pushing innovation in device development. Additionally, government initiatives promoting early diagnosis have further bolstered market expansion. For instance, as per the UK National Health Service (NHS), the adoption of pediatric neurostimulators has risen by 15% since 2020.

MARKET DRIVERS

Rising Prevalence of Neurological Disorders

The escalating incidence of pediatric neurological disorders is a primary driver propelling the Europe pediatric neurology devices market forward. As per the European Brain Council, around 179 million people in Europe live with brain-related illnesses, including epilepsy and cerebral palsy, which account for nearly one-third of all disease burdens. Among these cases, pediatric patients represent a substantial portion, necessitating advanced diagnostic and therapeutic solutions. The growing awareness about timely intervention has fueled the demand for devices such as neurostimulators and intrathecal baclofen pumps. Furthermore, ongoing clinical trials exploring novel treatments have amplified investments in this sector by ensuring continuous innovation and accessibility.

Technological Advancements in Medical Devices

Technological breakthroughs in pediatric neurology devices are revolutionizing patient outcomes across Europe. Innovations such as minimally invasive neurosurgical tools and wearable EEG monitors have transformed diagnostics and treatment protocols. According to the European Medical Device Technology Association, funding for R&D in neurology devices grew by 22% in 2022 alone by reflecting the industry's commitment to cutting-edge solutions. These advancements not only enhance precision but also reduce recovery times is making them highly sought after.

MARKET RESTRAINTS

High Costs Associated with Devices

One of the key barriers hindering the growth of the Europe pediatric neurology devices market is the exorbitant cost of advanced equipment. For example, neurostimulator implants can cost upwards of €30,000 per unit by limiting accessibility for many families and smaller healthcare facilities. According to a study published by the European Health Economics Association, many European households cannot afford out-of-pocket expenses for specialized pediatric devices without financial assistance. This economic disparity creates inequitable access to life-saving technologies. Moreover, hospitals face budget constraints when procuring state-of-the-art devices, especially in rural areas. While subsidies exist, they often fall short of covering the full expense by leaving both providers and patients grappling with affordability issues.

Stringent Regulatory Frameworks

Another significant restraint is the complex regulatory landscape governing pediatric neurology devices in Europe. As per the European Medicines Agency (EMA), obtaining approval for new devices involves rigorous testing phases spanning several years is delaying product launches. For instance, the average time required for CE marking a mandatory certification ranges from 18 to 36 months, depending on the complexity of the device. This prolonged process stifles innovation and discourages smaller firms from entering the market. Additionally, post-market surveillance mandates add further layers of compliance is increasing operational costs. According to a survey conducted by the German Association of Medical Device Manufacturers, nearly 50% of startups cited regulatory hurdles as the primary reason for abandoning projects.

MARKET OPPORTUNITIES

Expansion of Telemedicine Integration

The integration of telemedicine into pediatric neurology care offers immense potential for market growth. With remote consultations becoming increasingly common, Europe is witnessing a surge in demand for connected neurology devices. Wearable EEG devices and portable neurostimulators equipped with IoT capabilities enable real-time monitoring and data transmission is enhancing patient management. The manufacturers can expand their reach to underserved regions, where access to specialized care remains limited.

Growing Focus on Rare Disease Treatments

Europe’s emphasis on addressing rare neurological disorders presents a lucrative opportunity for pediatric neurology device manufacturers. According to Orphanet, a database for rare diseases, there are over 6,000 identified rare conditions affecting children, with neurological manifestations being predominant. Governments and private organizations are investing heavily in research and development to tackle these ailments. Innovative devices such as intrathecal baclofen therapy systems are gaining traction due to their ability to manage symptoms effectively. Data from the French Muscular Dystrophy Association indicates a 25% annual growth in the adoption of neuromuscular devices since 2020.

MARKET CHALLENGES

Limited Awareness Among Stakeholders

A significant challenge facing the Europe pediatric neurology devices market is the lack of awareness among stakeholders, including parents, caregivers, and even healthcare professionals. Many pediatric neurological conditions remain undiagnosed or mismanaged due to insufficient knowledge about available treatment options. This knowledge gap often leads to delayed interventions is worsening patient outcomes.

Supply Chain Disruptions

Supply chain disruptions pose another major obstacle for the Europe pediatric neurology devices market. The COVID-19 pandemic exposed vulnerabilities in global supply chains, leading to shortages of critical components required for manufacturing neurosurgical devices. According to the European Commission’s Directorate-General for Industry, semiconductor shortages impacted the production of electronic neurostimulation devices by up to 30% in 2022. Geopolitical tensions and trade restrictions have intensified these challenges, leading to higher costs and longer lead times. For instance, Italy experienced a 15% decline in the availability of pediatric EEG machines during the first half of 2023, as confirmed by the Italian Ministry of Health. To mitigate these risks, companies must adopt resilient strategies, such as localizing production or diversifying suppliers, though this transition comes at a considerable expense.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Product, Service and Treatment, Neurological Specialty, Age Group, End User, Application, and Region. |

|

Various Analyses Covered |

Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

|

Market Leaders Profiled |

Medtronic plc, Abbott Laboratories, Boston Scientific, Johnson & Johnson, LivaNova PLC, Integra LifeSciences, Natus Medical, Nihon Kohden, B. Braun, Stryker, Siemens Healthineers, Philips Healthcare, Computational Diagnostics, Elekta AB, NeuroPace, Terumo, Smith+Nephew, Mizuho OSI, Orpyx Medical, and Magstim |

SEGMENTAL ANALYSIS

By Product Insights

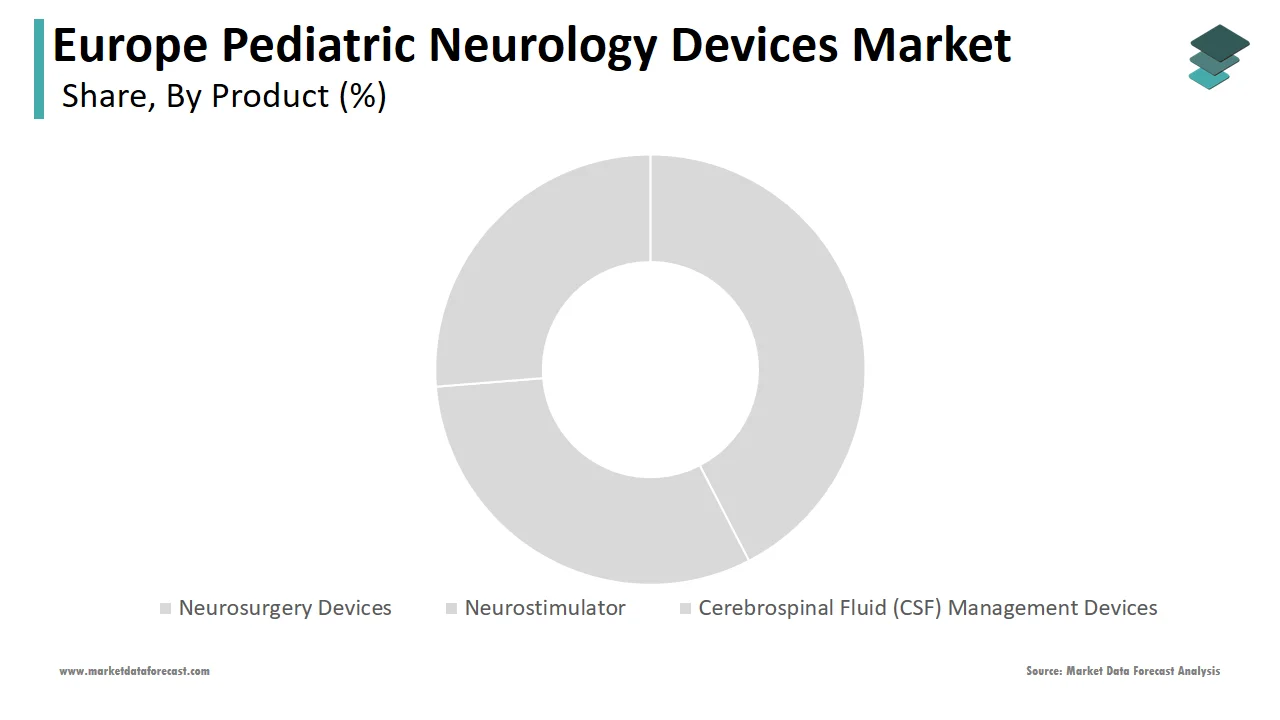

The neurosurgery devices segment was the largest by capturing 40.3% of the Europe pediatric neurology devices market share in 2024 owing to their versatility in treating a wide range of conditions, from congenital anomalies to traumatic injuries. Key factors contributing to this dominance include improved surgical precision, reduced recovery times, and enhanced patient safety. For example, Germany saw a 25% rise in robotic-assisted neurosurgery procedures among children, as per the German Federal Statistical Office. These innovations attract significant investments by enabling manufacturers to maintain a competitive edge. Additionally, collaborations between academia and industry foster continuous improvements by ensuring sustained demand.

The neurostimulator devices segment is anticipated to grow at a CAGR of 12.6% during the forecast period. This rapid expansion is fueled by increasing applications in managing chronic conditions like epilepsy and spasticity. According to the European Federation of Neurological Societies, the adoption of vagus nerve stimulators rose by 35% in 2023 alone. Improved battery life and wireless connectivity have made these devices more user-friendly is appealing to both clinicians and patients. Furthermore, favorable reimbursement policies in countries like France and Spain incentivize usage is accelerating market penetration.

By Service and Treatment Insights

The Electroencephalogram (EEG) services segment was accounted in holding 39.1% of the Europe pediatric neurology devices market share in 2024. The growth of the segment can attributed with their non-invasive nature and utility in diagnosing various neurological disorders, particularly epilepsy. Portable and wearable EEG devices have gained popularity due to their convenience and accuracy. For example, Italy witnessed a 30% increase in outpatient EEG tests for children, as reported by the Italian Pediatric Neurology Society. These trends reflect growing confidence in EEG technology, bolstered by supportive government policies. Additionally, training programs for technicians ensure standardized practices by enhancing reliability and trustworthiness.

Th intrathecal baclofen therapy segment is anticipated to register a CAGR of 14.2% during the forecast period. Its rapid ascent is attributed to its effectiveness in managing severe spasticity caused by conditions like cerebral palsy. According to the European Paediatric Neurology Society, the number of children receiving intrathecal baclofen therapy doubled in Spain between 2020 and 2023. Technological enhancements, such as programmable pumps, have improved dosing precision, minimizing side effects. For instance, France implemented a national initiative to equip pediatric hospitals with advanced infusion systems is resulting in a 50% increase in procedure volumes. Furthermore, partnerships between manufacturers and healthcare providers facilitate wider adoption by ensuring consistent growth.

By Neurological Specialty Insights

The neuro-oncology segment was the largest by occupying 45.6% of the Europe pediatric neurology devices market share in 2024. The segment’s market growth is fueled by the rising incidence of pediatric brain tumors, which are the second most common cancer type in children. Advanced imaging tools and minimally invasive surgical instruments are crucial in enhancing survival rates. For example, Germany introduced cutting-edge intraoperative MRI systems in pediatric oncology centers, boosting treatment success by 20%, as per the German Cancer Research Center. Collaborative efforts between oncologists and engineers drive innovation, sustaining demand for neuro-oncology devices.

The neuromuscular disorders segment is projected in witnessing a fastest CAGR of 13.8% in the next coming years. This growth is propelled by advancements in genetic testing and personalized medicine by enabling targeted therapies. Intrathecal baclofen therapy and wearable neurostimulators are gaining traction due to their ability to alleviate symptoms. For instance, the UK launched a nationwide program to provide neuromuscular devices to affected children by resulting in increasing in adoption rates. Public-private partnerships further accelerate progress, positioning neuromuscular disorder management as a key growth area.

COUNTRY LEVEL ANALYSIS

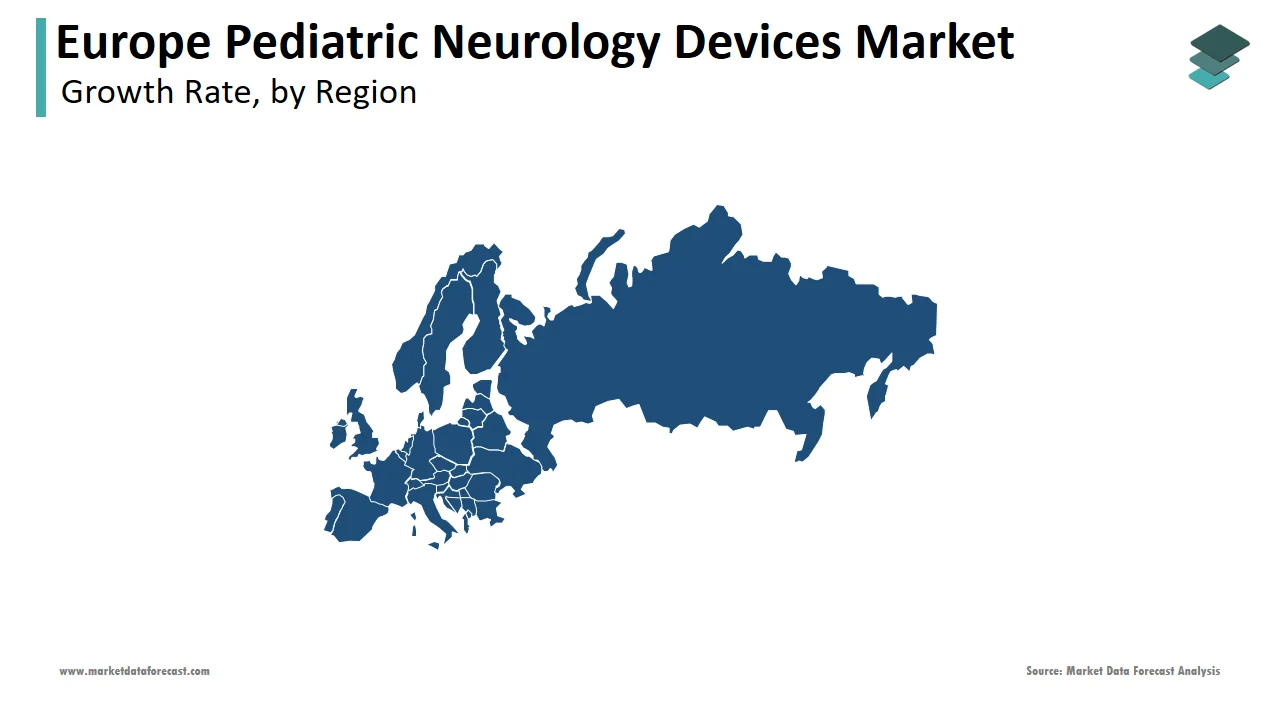

Germany was accounted in holding 28.4% of the Europe pediatric neurology devices market share in 2024 owing to its advanced healthcare infrastructure and high investment in pediatric care. The country’s prominence is further reinforced by its robust R&D ecosystem, with collaborations between universities, hospitals, and private firms fostering innovation. For instance, Germany has established specialized pediatric neurology centers equipped with state-of-the-art devices such as neurostimulators and robotic-assisted neurosurgery systems.

Spain is projected to grow with a CAGR of 13.5% during the forecast period. This growth is fueled by proactive government initiatives aimed at enhancing pediatric neurology care. Furthermore, Spain’s focus on digitizing healthcare via telemedicine platforms has broadened access to remote monitoring tools in rural regions. Investments in training programs for healthcare professionals have also contributed to the rapid adoption of advanced devices by positioning Spain as a key growth hub.

France, Italy, and the UK are projected to experience steady growth, driven by their strong focus on technological advancements and supportive regulatory frameworks.

KEY MARKET PLAYERS

Some notable companies that dominate the Europe pediatric neurology devices market profiled in this report are Medtronic plc, Abbott Laboratories, Boston Scientific, Johnson & Johnson, LivaNova PLC, Integra LifeSciences, Natus Medical, Nihon Kohden, B. Braun, Stryker, Siemens Healthineers, Philips Healthcare, Computational Diagnostics, Elekta AB, NeuroPace, Terumo, Smith+Nephew, Mizuho OSI, Orpyx Medical, Magstim, and others.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe pediatric neurology devices market employ diverse strategies to maintain their competitive edge and expand their footprint. A key strategy is forming strategic partnerships and collaborations with academic institutions and research organizations to speed up R&D efforts. For example, companies collaborate with universities to develop next-generation EEG devices and neurostimulators tailored for pediatric use. Another important strategy is geographic expansion, where companies focus on underserved regions by setting up local manufacturing units or distribution networks. Additionally, product diversification plays a vital role, as manufacturers introduce novel devices catering to niche markets, such as rare neurological disorders. Mergers and acquisitions are also common, enabling companies to consolidate their market presence and integrate complementary technologies into their portfolios.

COMPETITION OVERVIEW

The Europe pediatric neurology devices market is highly competitive, with both global leaders and regional players competing for market dominance. Leading companies like Medtronic, Abbott Laboratories, and Boston Scientific hold significant market shares due to their extensive product portfolios and robust R&D capabilities. However, smaller firms are increasingly challenging incumbents by focusing on niche segments, such as wearable neurostimulators and AI-driven diagnostic tools. Pricing strategies and technological differentiation are pivotal in shaping market dynamics, with firms striving to offer cost-effective yet innovative solutions. Regulatory compliance remains a critical factor, as stringent approval processes create barriers to entry for new entrants.

TOP 5 MAJOR ACTIONS BY KEY COMPANIES

- In March 2024, Medtronic acquired NeuroVation Labs , a startup specializing in pediatric neurostimulation technologies, to bolster its product portfolio and expand its reach in Europe.

- In May 2024, Abbott partnered with the University of Paris to co-develop advanced EEG devices equipped with AI capabilities for real-time monitoring of pediatric patients.

- In June 2024, Boston Scientific launched a pediatric-focused neurosurgical device in Germany, designed to enhance precision during minimally invasive procedures for young patients.

- In July 2024, Philips Healthcare introduced AI-enabled diagnostic tools in France, aiming to improve the accuracy of neurological assessments in children across underserved regions.

- In August 2024, Siemens Healthineers collaborated with UK hospitals to integrate telemedicine platforms with connected neurology devices by enabling remote consultations and treatment management for pediatric patients.

MARKET SEGMENTATION

This Europe pediatric neurology devices market research report is segmented and sub-segmented into the following categories.

By Product

- Neurosurgery Devices

- Neurostimulator

- Cerebrospinal Fluid (CSF) Management Devices

- Other

By Service and Treatment

- Electroencephalogram

- Intrathecal Baclofen Therapy

- Neurological Evaluations

- Vagal Nerve Stimulation

By Neurological Specialty

- Neuro-Oncology

- Neuromuscular

- Neonatal Neurology

- Neuro-Immunology

- Stroke

By Age Group

- Neonates

- Infants

- Children

- Adolescents

By End User

- Hospital

- Healthcare Center

- Specialty Clinics

- Neurological Research Centres

By Application

- Brain Tumour

- Epilepsy

- Autism Spectrum Disorder

- Parkinson’s Disease

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What was the Europe Pediatric Neurology Devices market size in 2024?

The Europe Pediatric Neurology Devices market was valued at USD 1.18 billion in 2024.

2. What is the projected CAGR for the Europe Pediatric Neurology Devices market?

The Europe Pediatric Neurology Devices market is projected to grow at a CAGR of 6.67% from 2025 to 2033.

3. Which segment held the largest Europe Pediatric Neurology Devices market share in 2024?

The neurosurgery devices segment held the largest share (40.3%) of the Europe Pediatric Neurology Devices market in 2024.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]