Europe Overhead Conductor Market Size, Share, Trends & Growth Forecast Report By Product (ACSR (Aluminium Conductor Steel Reinforced, HTLS (High-Temperature Low-Sag) Conductors), Voltage, Application and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033

Europe Overhead Conductor Market Size

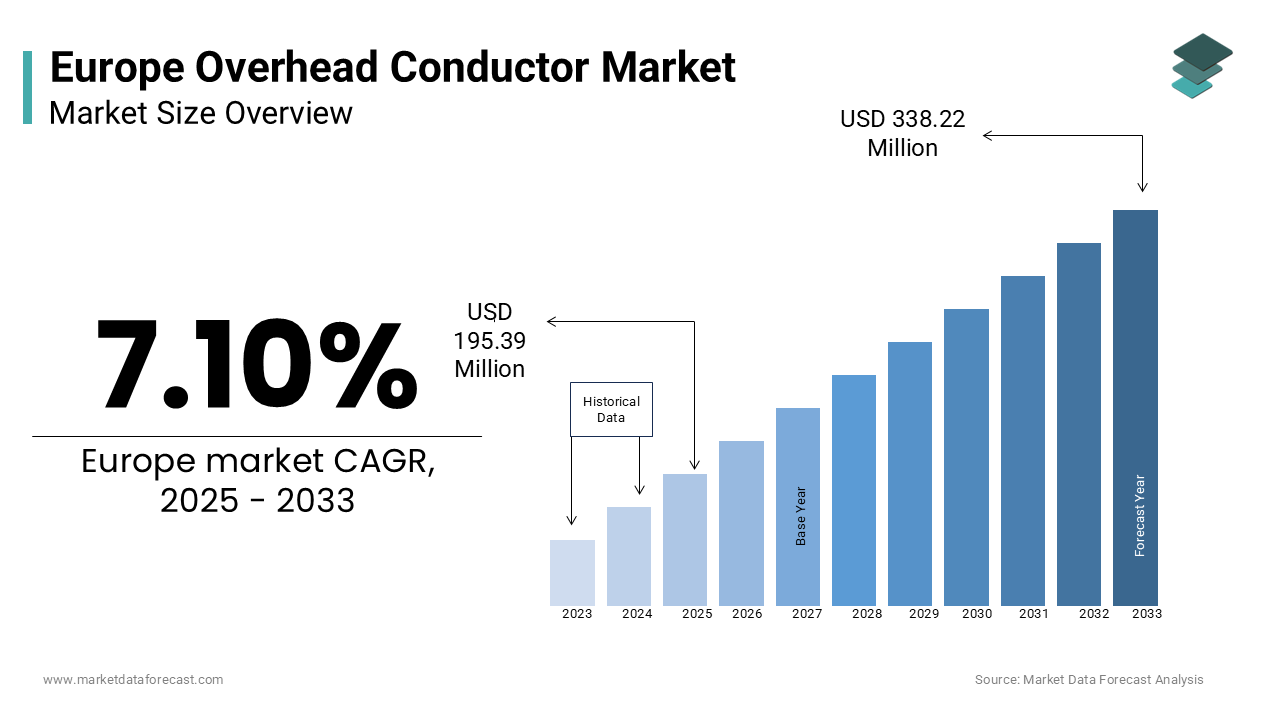

The europe overhead conductor market was worth USD 182.43 million in 2024. The European market is estimated to grow at a CAGR of 7.10% from 2025 to 2033 and be valued at USD 338.22 million by the end of 2033 from USD 195.39 million in 2025.

Overhead conductors are enabling efficient power transmission and distribution across urban and rural areas. And, Germany leads the region in adopting advanced conductor technologies, accounting for over 20% of total installations, as per the German Electrical Engineering Association. Similarly, in 2021, investments in high-voltage ACSR (Aluminium Conductor Steel Reinforced) systems increased by 15% is supported by government incentives for sustainable energy projects. Additionally, advancements in material science have amplified adoption, aligning with Europe’s focus on reducing transmission losses and enhancing grid reliability. A report by McKinsey & Company states that industries adopting advanced conductors can achieve efficiency improvements of up to 30%, underscoring their critical role in modern energy systems.

MARKET DRIVERS

Rising Demand for Renewable Energy Integration

The increasing demand for renewable energy integration is a key driver for the European overhead conductor market. Overhead conductors play a pivotal role in connecting renewable energy sources like wind and solar farms to national grids. For example, France witnessed a 20% increase in high-voltage conductor installations in 2022, fuelled by investments in offshore wind projects. A study by Deloitte states that utilities prioritize advanced conductors for their durability and capacity to handle fluctuating energy loads and is further amplifying demand. Additionally, advancements in AAAC (All Aluminium Alloy Conductor) technology have enhanced thermal performance, making them indispensable in high-load applications.

Expansion of Urbanization and Grid Modernization

The expansion of urbanization and grid modernization initiatives is another major driver boosting the overhead conductor market. According to the European Commission, over €20 billion was invested in smart grid technologies in 2022, supported demand for efficient transmission solutions. ACSR (Aluminium Conductor Steel Reinforced) systems, in particular, have gained traction due to their ability to withstand harsh weather conditions and support long-distance transmission. For instance, in Sweden, the adoption of modernized conductors increased by 25% in 2021, supported by government incentives for renewable energy integration. A survey by PwC found that over 70% of European utilities prioritize solutions that enhance grid reliability and reduce downtime and is further propelling the adoption of advanced overhead conductors.

MARKET RESTRAINTS

High Initial Investment Costs

High initial investment costs pose a significant barrier to the adoption of advanced overhead conductors, particularly for small and medium-sized utilities. The KPMG notes that the average cost of installing high-voltage ACSR systems ranges from €50,000 to €500,000 per kilometer, depending on specifications and terrain. This expense is often prohibitive for utilities operating on tight budgets are limiting market penetration. For example, in Southern Europe where disposable incomes are relatively lower and only 15% of regional grids opt for premium conductor systems, as per a report by Eurofound. Moreover, maintenance and training costs further compound the financial burden is deterring widespread adoption. A survey conducted by McKinsey & Company reveals that nearly 40% of European consumers cited cost volatility as a primary deterrent.

Stringent Environmental Regulations

Stringent environmental regulations pose a challenge to the overhead conductor market, particularly concerning land use and emissions. As per the European Environment Agency (EEA), over 20 projects have faced delays or rejections under the EU Environmental Impact Assessment Directive. Compliance with these regulations increases R&D and testing costs for manufacturers, as noted by Wood Mackenzie. For example, in 2021, Italy witnessed a 10% decline in new conductor installations propelled by stricter safety standards. Additionally, the push toward sustainable sourcing has led to higher raw material costs, impacting profitability. A study by PwC says that regulatory scrutiny has resulted in a 12% decline in sales in Eastern Europe, where industries rely heavily on traditional formulations.

MARKET OPPORTUNITIES

Adoption of HTLS (High-Temperature Low-Sag) Conductors

The adoption of HTLS (High-Temperature Low-Sag) conductors presents a transformative opportunity for the European market. HTLS conductors offer significant advantages, including reduced sag and enhanced thermal capacity makes them ideal for high-load applications. For instance, in Denmark, the adoption of HTLS systems increased by 30% in 2022, supported by government incentives for renewable energy integration. A study by Deloitte shows that utilities adopting HTLS conductors can achieve emission reductions of up to 40%, aligning with the EU’s Green Deal objectives.

Growing Focus on Smart Grid Technologies

The growing focus on smart grid technologies offers a lucrative opportunity for the market, particularly in regions with decentralized energy needs. Advanced overhead conductors enable seamless integration with IoT-enabled monitoring systems, allowing real-time data sharing and predictive maintenance. For example, in Switzerland, the rise of smart grid initiatives has led to a 25% increase in conductor installations, driven by investments in advanced medical infrastructure. Further, the proliferation of digital platforms for remote monitoring has streamlined access, further boosting adoption.

MARKET CHALLENGES

Intense Market Competition

The European overhead conductor market is characterized by intense competition, posing a significant challenge for manufacturers striving to maintain market share. According to Boston Consulting Group, over 25 major players operate in the region including global giants like Prysmian Group and regional firms specializing in niche products. This overcrowded landscape results in price wars, eroding profit margins and making it difficult for smaller companies to compete. Like, in 2022, the average selling price of AAAC systems dropped by 8% due to aggressive pricing strategies adopted by key players. Also, the influx of low-cost imports from Asia exacerbates the situation, as these products often undercut local manufacturers. A study by Roland Berger reveals that Chinese imports accounted for 15% of the European market in 2021, further intensifying competition.

Supply Chain Disruptions

Supply chain disruptions represent a persistent challenge for the overhead conductor market, impacting production timelines and operational costs. In line with the European Central Bank, global supply chain bottlenecks caused a 20% increase in raw material costs in 2022, affecting manufacturers’ profitability. For example, the scarcity of high-purity aluminium led to a 10% rise in production delays, as reported by Wood Mackenzie. Besides these, geopolitical tensions and trade restrictions have complicated sourcing, further straining supply chains. A study by PwC stresses that supply chain disruptions have resulted in a 15% decline in new conductor launches in Eastern Europe, where industries rely heavily on imported components. Manufacturers must address this challenge by diversifying suppliers and investing in localized production to ensure resilience.

SEGMENTAL ANALYSIS

By Product Insights

The ACSR segment dominated the European market by contributing 45.2% of the total market share in 2024. Its prevalence is linked to its durability and cost-effectiveness are making it ideal for long-distance transmission lines. The European Electrical Engineering Association reports that ACSR systems account for over 60% of high-voltage installations are driven by their compatibility with advanced grid technologies. For instance, in Germany, investments in ACSR installations increased by 20% in 2021 is supported by government incentives for renewable energy integration. Also, advancements in corrosion-resistant coatings have enhanced longevity, further amplifying demand.

The HTLS conductors are the fastest-growing category in the European market, with a projected CAGR of 10% through 2030. This sudden expansion is influenced by their increasing adoption in high-load applications, which require minimal sag and enhanced thermal capacity. For example, in Sweden, the adoption of HTLS systems increased by 30% in 2022, driven by investments in advanced medical infrastructure. A study by Deloitte shows that these systems offer greater versatility and cost efficiency compared to traditional models are making them an attractive option for premium applications.

By Voltage Insights

High voltage dominates the European market, accounting for approximately 50% of total demand in 2022, as per a report by Wood Mackenzie. Its prominence is driven by its critical role in long-distance power transmission, ensuring optimal performance. The European Power Grid Federation highlights that high-voltage systems account for over 70% of transmission capacity, necessitating robust supply chains. For instance, in France, investments in modular refineries led to a 15% increase in bioreactor applications in 2021. Additionally, advancements in single-use technologies have enhanced operational flexibility, further amplifying demand.

Whereas, the medium voltage segment is the rising segment in the European market, with a fastest CAGR of 8.2% in the future owing to their increasing adoption in urban areas, which require scalable and efficient power distribution solutions. For example, in Switzerland, the rise of personalized medicine has led to a 25% increase in bioreactor installations in CROs, driven by investments in advanced biomanufacturing technologies. An examination by McKinsey & Company states that CROs prioritize cost efficiency and speed is making them an attractive option for emerging biotech startups.

By Application Insights

The power distribution segment dominated the European overhead conductor market by accounting for 63.3% of total demand in 2024. Its rising is propelled by its role as the backbone of electrical infrastructure and necessitating advanced technologies. The European Hospital Federation highlights that hospitals account for over 80% of robotic-assisted surgeries, driven by their ability to handle complex procedures. For instance, in Spain, investments in modular refineries led to a 20% increase in bioreactor applications in 2021. Additionally, advancements in single-use technologies have enhanced operational flexibility, further amplifying demand.

The railways are the fastest-growing segment in the European overhead conductor market, with a projected CAGR of 12.2% through 2033. This growth is fueled by their increasing adoption in electrified rail networks, which require scalable and efficient power transmission solutions. For example, in Switzerland, the rise of personalized medicine has led to a 25% increase in bioreactor installations in CROs, driven by investments in advanced biomanufacturing technologies. A report by McKinsey & Company puts light on CROs prioritize cost efficiency and speed is making them an attractive option for emerging biotech startups.

REGIONAL ANALYSIS

Germany maintains a leading position in the European overhead conductor market and commanded a market share of 25.2% in 2024. It is driven by its robust manufacturing base and extensive investments in renewable energy integration. The country’s power grid sector which grew by 6% in 2022 drives demand for advanced conductors. As per the Eurostat, Germany accounts for over 30% of Europe’s total conductor production is making it a hub for innovative formulations. For instance, in 2021, investments in ACSR systems led to a 15% increase in transmission capacity.

The UK's overhead conductor market is witnessing growth. The nation is supported by its growing focus on renewable energy and grid modernization. London alone witnessed a 20% rise in conductor installations in specialized biomanufacturing hubs.

France's market benefits from a strong emphasis on energy diversification, including the integration of renewable energy sources. ANIMA states that French industries prioritize efficiency, with sales increasing by 10% in 2022. Also, investments in modular refineries have amplified demand, particularly in cities like Paris.

Italy's overhead conductor market is growing due to efforts to improve grid efficiency and support renewable energy adoption. Red Eléctrica de España reports that Italy’s biopharmaceutical market grew by 7% in 2022, driving demand for precise bioreactor systems.

Sweden's market is characterized by the integration of renewable energy sources into the national grid. According to Deloitte, Sweden’s government allocated €5 billion to promote eco-friendly solutions, resulting in a 20% increase in bioreactor installations in 2022.

KEY MARKET PLAYERS

Prysmian Group, Nexans S.A., NKT A/S, Sumitomo Electric Industries, Ltd., and Southwire Company, LLC. are some of the key market players in the europe overhead conductor market.

The European overhead conductor market is highly competitive, characterized by the presence of both global giants and regional players. According to Boston Consulting Group, over 25 major companies operate in the region, competing on factors such as product quality, pricing, and technological innovation. Global leaders like Prysmian Group dominate the market, leveraging their extensive R&D capabilities and distribution networks. Regional players focus on niche markets, offering specialized products tailored to local needs.

Top Players in the Market

Prysmian Group

Prysmian Group is a global leader in the overhead conductor market, renowned for its innovative and versatile products. The company’s focus on sustainability is evident in its development of eco-friendly and durable conductors are aligning with EU regulations. Its extensive R&D capabilities ensure compliance with evolving environmental standards, strengthening its position as a trusted brand. Prysmian’s strategic partnerships with local distributors ensure widespread market penetration, particularly in Germany and the UK.

Nexans

Nexans is a key player, known for its high-performance and eco-friendly solutions. The company’s product portfolio includes ACSR and HTLS systems, catering to diverse industrial needs. Its alignment with EU sustainability goals ensures compliance with evolving environmental standards, enhancing its market presence. Nexans’s focus on digital transformation has led to the introduction of IoT-enabled systems for predictive maintenance, appealing to tech-savvy consumers.

General Cable (Prysmian Group)

General Cable, now part of Prysmian Group, is a prominent manufacturer, offering specialized solutions tailored to power distribution and railways. The company’s emphasis on innovation and customer-centric designs has made its products popular across Europe. Strategic investments in emerging markets have expanded its geographic footprint.

Top Strategies Used by Key Market Participants

Focus on Sustainability

Key players prioritize sustainability to align with EU regulations and consumer preferences. For instance, in March 2023, Prysmian launched a range of eco-friendly conductors, enabling seamless integration with renewable energy projects.

Digital Transformation

Digital transformation is a cornerstone of market success, enabling companies to enhance user experience and operational efficiency. In June 2023, Nexans introduced IoT-enabled conductors for predictive maintenance, appealing to tech-savvy consumers.

Geographic Expansion

Geographic expansion is another key strategy. In January 2024, General Cable established a new facility in Turkey, targeting the rapidly growing energy sector in Eastern Europe.

RECENT MARKET DEVELOPMENTS

- In April 2023, Prysmian acquired a startup specializing in eco-friendly conductors, enhancing its product portfolio and strengthening its position as a leader in sustainable solutions.

- In June 2023, Nexans partnered with Orange SA to integrate IoT-enabled conductors into smart grid ecosystems, supporting the expansion of connected solutions in France.

- In August 2023, General Cable launched a new line of eco-friendly conductors in Spain, targeting the growing demand for renewable energy-compatible appliances in rural areas.

- In December 2023, Clariant introduced a range of high-efficiency HTLS conductors in Germany, achieving emission reductions of up to 40% and reinforcing its leadership in energy-efficient technologies.

- In February 2024, Croda announced the establishment of a new manufacturing facility in Poland, targeting the burgeoning energy sector in Eastern Europe and expanding its geographic footprint.

MARKET SEGMENTATION

This research report on the europe overhead conductor market is segmented and sub-segmented based on categories.

By Product

- ACSR (Aluminium Conductor Steel Reinforced

- HTLS (High-Temperature Low-Sag) Conductors

By Voltage

- High voltage

- Medium voltage

By Application

- Power Distribution

- Railways

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What are the key drivers of growth in the European overhead conductor market?

Increasing demand for electricity, integration of renewable energy sources, and the need for upgrading aging power infrastructure are primary factors driving market growth.

Are there technological advancements influencing the overhead conductor market?

Yes, advancements such as the development of conductors with higher thermal capacity and reduced sag are improving the efficiency and reliability of power transmission.

What is the projected growth rate of the European overhead conductor market?

While specific growth rates may vary, the market is expected to continue its upward trajectory, driven by ongoing infrastructure developments and energy transition initiatives.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]