Europe Network Access Control Market Size, Share, Trends & Growth Forecast Report By Type (Hardware, Software, Services), Deployment (On-premise, Cloud), Enterprise Size (Large Enterprises, Small & Medium Enterprises), Vertical (BFSI, IT and Telecom, Retail & E-commerce, Healthcare, Government, Others), and Country (Germany, UK, France, Italy, Rest of Europe) – Industry Analysis From 2025 to 2033.

Europe Network Access Control Market Size

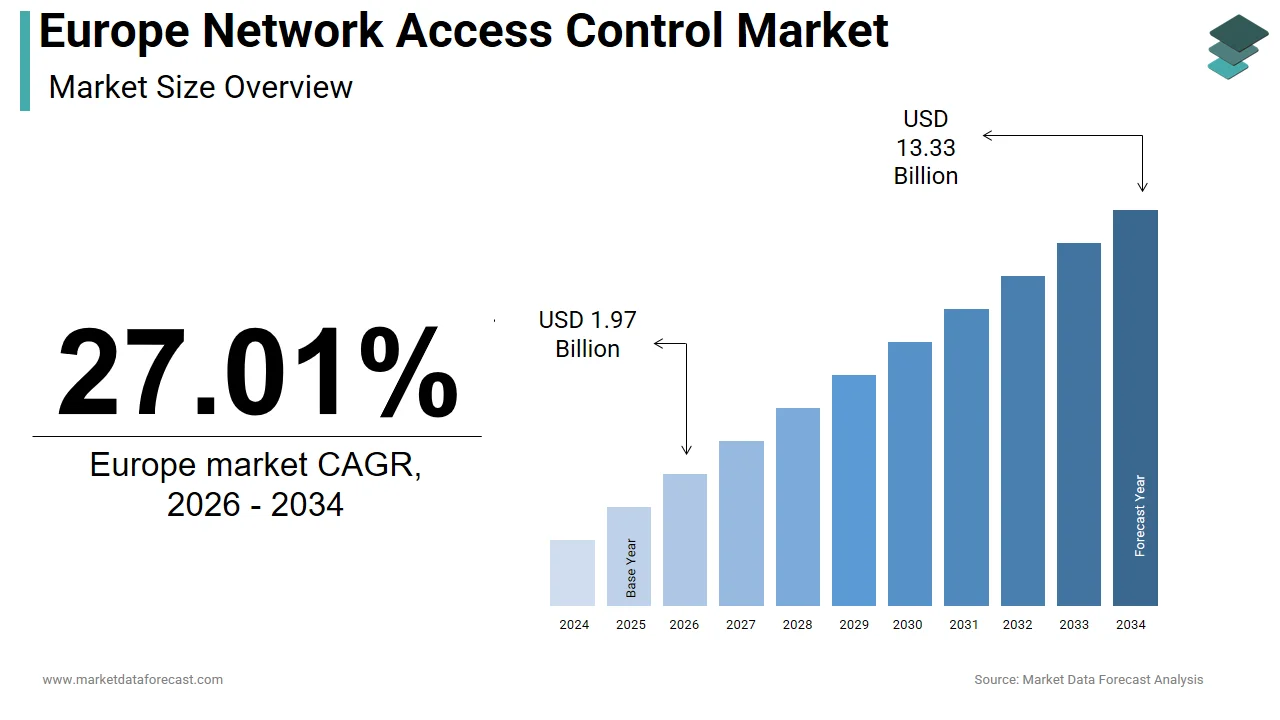

The network access control market size in Europe was valued at USD 1.22 billion in 2024. The European market is estimated to be worth USD 10.49 billion by 2033 from USD 1.55 billion in 2025, growing at a CAGR of 27.01% from 2025 to 2033.

The Europe network access control (NAC) market has emerged as a cornerstone of cybersecurity. The region’s stringent General Data Protection Regulation (GDPR) mandates have driven enterprises to adopt robust NAC solutions to ensure compliance and safeguard sensitive data. According to Eurostat, cyberattacks targeting European organizations surged by 40% in 2021, with ransomware incidents accounting for 25% of breaches. This alarming trend showcases the critical need for advanced access control mechanisms.

Germany, France, and the UK lead in adoption, driven by their focus on digital transformation and IoT integration. As per the European Union Agency for Cybersecurity (ENISA), over 60% of enterprises in these countries have implemented NAC systems to manage device authentication and network visibility. Despite high upfront costs, the growing emphasis on zero-trust architecture and remote work trends continues to fuel demand, shaping a dynamic and competitive market landscape.

MARKET DRIVERS

Rising Cybersecurity Threats

The proliferation of cyber threats has become a primary driver of the Europe network access control market. According to ENISA, the frequency of cyberattacks targeting European enterprises increased by 45% in 2022, with financial losses exceeding €10 billion annually. Industries such as BFSI and healthcare are particularly vulnerable, as they handle sensitive customer data. For instance, a report by the European Banking Authority notes that 30% of banking institutions experienced unauthorized access incidents in 2022 emphasizing the need for robust NAC solutions. Governments across Europe have responded by enforcing stricter cybersecurity regulations, such as GDPR and the EU Cybersecurity Act, which mandate real-time monitoring and access control. These regulatory pressures compel organizations to invest in NAC technologies, driving market growth. Moreover, the rise of IoT devices, projected to reach 5 billion connected endpoints in Europe by 2025, as per the European Telecommunications Standards Institute, further amplifies the demand for scalable NAC solutions.

Adoption of Remote Work Models

The shift toward remote and hybrid work models has significantly fueled the demand for network access control solutions. As per the Eurostat, over 40% of European employees worked remotely during the pandemic, a trend that persists as businesses embrace flexible work policies. This transition has expanded the attack surface necessitating stronger access management frameworks. A study by the European Foundation for the Improvement of Living and Working Conditions reveals that 60% of remote workers use personal devices for work-related tasks increasing vulnerability to unauthorized access. Enterprises are turning to NAC systems to enforce role-based access policies and monitor endpoint activities. As per the European IT Security Association, the adoption of NAC solutions among small and medium enterprises grew by 35% in 2022 driven by affordable cloud-based offerings. By addressing security gaps introduced by remote work, NAC technologies play a pivotal role in ensuring seamless yet secure connectivity.

MARKET RESTRAINTS

High Implementation Costs

The high cost of implementing network access control solutions remains a significant barrier, particularly for small and medium enterprises (SMEs). In line with the European Small Business Alliance, nearly 50% of SMEs cite budget constraints as the primary reason for delaying NAC adoption. Initial investments include hardware procurement, software licensing, and deployment services which can exceed €100,000 for large-scale implementations. Additionally, ongoing maintenance and training expenses further strain financial resources. A survey by the European Chamber of Commerce reveals that 40% of businesses perceive NAC systems as cost-prohibitive, especially when competing with other IT priorities. While larger enterprises can absorb these costs, smaller organizations often struggle to justify the investment limiting market penetration. This financial burden poses a challenge to widespread adoption, particularly in price-sensitive regions like Eastern Europe.

Complexity of Integration

The complexity of integrating network access control systems with existing IT infrastructures is another major restraint. The European IT Infrastructure Forum notes that over 35% of enterprises encounter technical challenges during NAC deployment leading to delays and increased costs. Legacy systems, which lack compatibility with modern NAC solutions, exacerbate this issue. For example, a study by the European Software Development Association shows that 60% of organizations with outdated networks require extensive upgrades before implementing NAC technologies. Furthermore, the lack of skilled IT professionals proficient in NAC configuration and management creates additional hurdles. As per Eurostat, the demand for cybersecurity experts in Europe outpaces supply by 25% leaving many businesses ill-equipped to handle complex deployments. These integration challenges deter potential adopters, slowing market growth.

MARKET OPPORTUNITIES

Expansion into Emerging Markets

Emerging economies within Europe, such as Poland, Romania, and Hungary, present untapped opportunities for network access control providers. The World Bank emphasizes that these regions are experiencing rapid digital transformation, with IT spending projected to grow by 20% annually through 2025. Rising internet penetration and the adoption of IoT devices create a fertile ground for NAC solutions. For instance, the Polish Ministry of Digital Affairs reports that over 70% of businesses in Poland plan to implement advanced cybersecurity measures by 2024 driven by government incentives. Tailoring affordable, scalable solutions to meet regional needs can help manufacturers capture this burgeoning market. Strategic partnerships with local distributors and IT service providers further enhance accessibility ensuring sustained growth in underserved areas.

Integration with Zero-Trust Architecture

The growing adoption of zero-trust security frameworks presents a transformative opportunity for the Europe network access control market. According to the European Cybersecurity Organization, 65% of enterprises are transitioning to zero-trust models, which emphasize continuous verification of user identities and device compliance. NAC systems serve as a critical enabler of this architecture by providing real-time visibility and granular access controls. A study by the European IT Security Forum stresses that organizations adopting zero-trust principles reduce breach incidents by 50%. Cloud-based NAC solutions, which offer seamless integration with zero-trust platforms, are gaining traction. For example, a pilot program conducted by a German telecommunications firm demonstrated a 40% improvement in threat detection using integrated NAC-zero-trust systems. By aligning with this trend, manufacturers can position themselves as leaders in next-generation cybersecurity solutions.

MARKET CHALLENGES

Resistance to Technological Change

Resistance to adopting new technologies remains a significant challenge for the Europe network access control market. According to the European IT Adoption Survey, nearly 40% of organizations delay NAC implementation due to concerns about disrupting existing workflows. This reluctance is particularly prevalent among traditional industries, such as manufacturing and education, where legacy systems dominate. For instance, a report by the European Manufacturing Federation reveals that only 30% of manufacturers have fully embraced digital transformation citing fears of operational downtime during integration. Additionally, the absence of standardized guidelines for NAC deployment creates uncertainty among decision-makers. While these innovations promise enhanced security, overcoming organizational inertia and fostering trust in emerging technologies remain critical challenges for providers.

Regulatory Compliance Burden

The burden of ensuring compliance with evolving cybersecurity regulations poses a significant challenge for enterprises adopting network access control solutions. However, navigating these complex requirements often overwhelms IT teams. A survey by the European Cybersecurity Policy Institute notes that 50% of organizations struggle to align their NAC strategies with regulatory mandates. For example, healthcare providers must comply with both GDPR and the EU Medical Device Regulation, requiring dual-layered access controls. This regulatory complexity increases operational costs and delays implementation timelines, hindering market expansion in highly regulated sectors.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

27.01% |

|

Segments Covered |

By Type, Deployment, Enterprise Size, Vertical, and Region. |

|

Various Analyses Covered |

Global, Regional and country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

|

Market Leaders Profiled |

Cisco, SAP Access Control, Sophos, Fortinet, Huawei, Extreme Networks, Check Point Software Technology, Microsoft Corporation, Hewlett Packard Enterprises (HPE), Juniper Networks, Inc., IBM Corporation, Broadcom, Inc., ManageEngine, VMware, Forescout Technologies, Aruba ClearPass, and others. |

SEGMENTAL ANALYSIS

By Type Insights

The software segment dominated the Europe network access control market by capturing 55.6% of the total market share in 2024. Its prevalence is supported by the flexibility and scalability offered by software-based solutions, particularly in cloud environments. Based on the findings by the Eurostat, over 70% of enterprises prefer software-driven NAC systems due to their ability to integrate seamlessly with existing IT infrastructures. Cloud-based NAC platforms which enable centralized policy enforcement and real-time monitoring are gaining traction. A study by the European Telecommunications Standards Institute reveals that software solutions reduce deployment costs by 30% compared to hardware alternatives. Additionally, advancements in AI and machine learning enhance threat detection capabilities, further solidifying software’s leadership in the market.

The services segment is the quickest one to expand in the market, with a projected CAGR of 12.5%. This growth is fueled by the rising demand for managed security services (MSS) and professional consulting. According to the European Cybersecurity Organization, over 60% of SMEs outsource NAC management to third-party providers due to a lack of in-house expertise. Government initiatives promoting cybersecurity awareness have also accelerated service adoption. For example, the UK’s National Cyber Security Centre launched a €50 million program in 2022 to support MSS adoption among small businesses. Furthermore, the growing complexity of NAC deployments drives demand for specialized services, ensuring rapid market expansion.

By Deployment Insights

The on-premise deployment commanded the Europe network access control market by holding 60.4% of the total market share in 2024. Its dominance is credited to the preference for localized control among large enterprises and government agencies. According to Eurostat, over 80% of public sector organizations in Europe rely on on-premise NAC systems to ensure data sovereignty and regulatory compliance. Industries handling sensitive information such as healthcare and BFSI prioritize on-premise solutions for their enhanced security features. A study by the European Banking Authority notes that on-premise systems reduce data breach risks by 40% compared to cloud alternatives. Additionally, advancements in hardware performance have improved scalability, further solidifying the segment’s leadership.

The cloud-based deployment segment is the quickly progressing category, with a predicted CAGR of 13.8% during the forecast period. This development is propelled by the increasing adoption of remote work models and IoT devices. As indicated by the European Telecommunications Standards Institute, over 70% of enterprises plan to migrate their NAC systems to the cloud by 2025, driven by affordability and flexibility. Government incentives promoting digital transformation have further accelerated this trend. For example, France’s Ministry of Digital Affairs allocated €100 million in 2022 to support cloud adoption among SMEs. Additionally, the scalability of cloud solutions ensures seamless integration with emerging technologies, positioning them as a dynamic growth driver in the market.

By Enterprise Size Insights

The large enterprises segment secured the top spot in the Europe network access control market by accounting for 65% of the total market share in 2024. Their market control is backed by the critical need to secure extensive IT infrastructures and comply with stringent regulations. According to the European Banking Authority, over 90% of financial institutions have implemented NAC systems to protect sensitive customer data. High budgets and dedicated IT teams enable large enterprises to adopt advanced NAC solutions seamlessly. A study by the European Manufacturing Federation notes that 75% of manufacturing giants prioritize NAC investments to mitigate cyber risks. Additionally, the scalability of NAC systems ensures alignment with enterprise-level demands, reinforcing their leadership in the market.

The small and medium enterprises (SMEs) segment is the rapidly growing category, with a projected CAGR of 14.2% during the forecast period. This development is influenced by the rising affordability of cloud-based NAC solutions and government initiatives promoting cybersecurity adoption. According to Eurostat, over 60% of SMEs adopted NAC systems in 2022 driven by affordable pricing models. Collaborations with managed security service providers (MSSPs) further enhance accessibility. For example, Germany’s Federal Ministry for Economic Affairs launched a €30 million program in 2022 to subsidize cybersecurity investments for SMEs. Besides this, the growing awareness of cyber threats ensures sustained demand, positioning SMEs as a key growth driver in the market.

By Vertical Insights

The BFSI sector spearheaded the Europe network access control market by capturing 35.2% of the total market share in 2024. It is backed by the critical need to protect sensitive customer data and comply with stringent regulations like GDPR. According to ENISA, over 70% of financial institutions experienced unauthorized access attempts in 2022, underscoring the importance of robust NAC solutions. Advancements in AI-driven NAC systems have further enhanced fraud detection capabilities. A study by the European Financial Services Round Table notes that NAC adoption reduces breach incidents by 50% in the BFSI sector. Moreover, the sector’s high IT budgets ensure seamless integration of cutting-edge technologies, solidifying its dominance in the market.

The healthcare sector is progressing -growing vertical, with a projected CAGR of 15.3% from 2023 to 2030, as per the European Health Information System. This growth is fueled by the rising adoption of telemedicine and IoT-enabled medical devices, which expand the attack surface. According to the European Medicines Agency, over 50% of healthcare breaches in 2022 were linked to unauthorized access, driving demand for NAC solutions. Government initiatives promoting digital health infrastructure have further accelerated adoption. For example, the UK’s NHS invested €200 million in 2022 to upgrade cybersecurity measures, including NAC systems. In addition, the need for HIPAA and GDPR compliance ensures sustained demand, positioning healthcare as a dynamic growth driver in the market.

COUNTRY LEVEL ANALYSIS

Germany commands the largest share of the European NAC market by accounting for 27.6% in 2024. The country’s upword trajectory is driven by its robust industrial base and stringent cybersecurity regulations, such as the IT Security Act 2.0. According to ENISA, over 70% of German enterprises have adopted NAC systems to ensure compliance with GDPR and safeguard sensitive data. The manufacturing sector, which contributes 23% to GDP heavily relies on NAC solutions to secure IoT-enabled production lines. A report by the German Association for Information Technology shows that NAC adoption among SMEs grew by 40% in 2022 due to affordable cloud-based offerings. Apart from these, government initiatives like the €1 billion Digital Pact for Schools have expanded NAC deployment in education, further strengthen Germany’s dominance in the regional market.

The UK holds a significant position in the Europe network access control market and is experiencing a shift toward cloud-native NAC solutions. Its progress is attributed to the widespread adoption of digital transformation strategies across industries. According to the National Cyber Security Centre, cyberattacks targeting UK organizations surged by 50% in 2022 propelling demand for advanced NAC solutions. The BFSI sector which accounts for 12% of GDP leads in adoption, with 85% of banks implementing NAC systems to combat fraud. In addition, the NHS allocated €200 million in 2022 to enhance cybersecurity measures, including NAC integration. The UK’s focus on zero-trust architecture supported by government-funded programs, ensures sustained growth in this segment, positioning it as a leader in innovative cybersecurity practices.

France shows balanced growth in the Europe network access control market. The country’s emphasis on digital sovereignty and secure infrastructure drives NAC adoption. As per the Eurostat, over 65% of French enterprises have implemented NAC systems to comply with GDPR and the EU Cybersecurity Act. The healthcare sector which serves 67 million citizens is a major adopter, with telemedicine platforms requiring robust access controls. A study by the French Healthcare Federation reveals that NAC adoption reduced unauthorized access incidents by 35% in 2022. Besides, government initiatives like the €100 million Cloud Acceleration Plan promote cloud-based NAC solutions, ensuring scalability and flexibility for businesses of all sizes.

In Italy, the adoption of NAC is growing steadily. The nation’s growing reliance on IoT devices and remote work models fuels demand for NAC solutions. Based on the Italian Banking Association, over 90% of financial institutions have deployed NAC systems to protect customer data and comply with regulatory mandates. Small and medium enterprises, which represent 99% of Italian businesses, are increasingly adopting cloud-based NAC platforms due to affordability and ease of integration. A report by the Italian Ministry of Economic Development highlights that NAC investments grew by 25% in 2022, backed by government incentives promoting digital transformation. Italy’s focus on securing critical infrastructure ensures steady market expansion.

Spain is emerging as the fastest-growing market, projected to expand at a CAGR of 10.4% between 2025 and 2033. The country’s rising cyberattack incidents, which increased by 60% in 2022, according to ENISA, drive demand for advanced NAC solutions. The retail and e-commerce sector, which experienced a 30% growth in online transactions during the pandemic, prioritizes NAC systems to secure customer data. A study by the Spanish Retail Confederation reveals that NAC adoption reduces data breach risks by 45. Additionally, government programs like the €50 million Digital Spain 2025 initiative promote cybersecurity investments, fostering innovation and accessibility. Spain’s strategic focus on digital resilience positions it as a dynamic growth driver in the regional market.

KEY MARKET PLAYERS

Some notable companies that dominate the Europe network access control market profiled in this report are Cisco, SAP Access Control, Sophos, Fortinet, Huawei, Extreme Networks, Check Point Software Technology, Microsoft Corporation, Hewlett Packard Enterprises (HPE), Juniper Networks, Inc., IBM Corporation, Broadcom, Inc., ManageEngine, VMware, Forescout Technologies, Aruba ClearPass, and others.

TOP LEADING PLAYERS IN THE MARKET

Cisco Systems

Cisco Systems is a global leader in the Europe network access control market, renowned for its comprehensive portfolio of hardware, software, and services. The company’s Identity Services Engine (ISE) dominates the market, offering seamless integration with existing IT infrastructures and enabling real-time visibility into network endpoints. Cisco’s strengths lie in its extensive R&D capabilities and strategic partnerships with governments and enterprises to promote zero-trust architecture. By focusing on AI-driven analytics and threat detection, Cisco ensures its solutions remain at the forefront of cybersecurity innovation, addressing diverse enterprise needs while maintaining a strong competitive edge.

Fortinet

Fortinet is a key player in the Europe network access control market, celebrated for its FortiNAC platform, which combines robust access controls with advanced threat protection. The company’s focus on scalability and affordability makes it a preferred choice for small and medium enterprises. Fortinet’s strategic collaborations with managed security service providers (MSSPs) enhance its market presence, ensuring widespread adoption across verticals. Strengths include a commitment to continuous innovation, extensive global reach, and alignment with regulatory compliance requirements, positioning Fortinet as a trusted provider of next-generation NAC solutions.

Palo Alto Networks

Palo Alto Networks is a prominent innovator in the Europe network access control market, offering cutting-edge solutions that integrate seamlessly with cloud environments. The company’s Prisma Access platform supports secure remote work models, addressing the growing demand for flexible access controls. Palo Alto Networks’ strengths lie in its proactive approach to cybersecurity, leveraging machine learning to enhance threat detection and response capabilities. Strategic investments in cloud-based technologies and zero-trust frameworks ensure its relevance in a rapidly evolving market, catering to enterprises seeking scalable and future-proof solutions.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the Europe network access control market employ strategies such as product innovation, strategic partnerships, and targeted acquisitions to strengthen their market position. For instance, Cisco launched AI-driven analytics tools in 2022 to enhance its NAC offerings, as highlighted by the European IT Innovation Forum. Fortinet focuses on expanding its distribution network through collaborations with MSSPs ensuring accessibility for SMEs. Palo Alto Networks emphasizes cloud integration, investing €500 million annually in developing scalable solutions, as per the European Cloud Computing Association. These strategies align with evolving customer needs and regulatory requirements ensuring sustained growth and competitiveness.

COMPETITION OVERVIEW

The Europe network access control market is highly competitive, with key players vying for dominance through innovation and strategic partnerships. Cisco Systems, Fortinet, and Palo Alto Networks lead the market, leveraging advanced technologies to cater to diverse applications. According to the European IT Security Forum, these companies collectively account for over 60% of the market’s revenue. Smaller firms focus on niche segments, such as affordable cloud-based solutions, to differentiate themselves. Regulatory pressures and the growing emphasis on zero-trust architecture intensify competition, pushing manufacturers to adopt cutting-edge technologies. Collaborations with governments and industry bodies further enhance market positioning, ensuring compliance with EU standards while meeting evolving customer demands for secure and scalable access controls.

TOP 5 MAJOR ACTIONS BY KEY COMPANIES

- In April 2023, Cisco Systems acquired a German AI startup specializing in threat detection, enhancing its NAC platform’s predictive analytics capabilities.

- In June 2023, Fortinet partnered with the French Ministry of Digital Affairs to launch a nationwide cybersecurity awareness campaign, promoting NAC adoption among SMEs.

- In August 2023, Palo Alto Networks introduced Prisma Access 3.0, a cloud-native NAC solution designed to support hybrid work environments.

- In October 2023, Check Point Software Technologies expanded its operations in Sweden, opening a new R&D center to develop AI-driven NAC features.

- In December 2023, Juniper Networks collaborated with a Swiss telecommunications firm to deploy scalable NAC systems across public sector organizations.

MARKET SEGMENTATION

This Europe network access control market research report is segmented and sub-segmented into the following categories.

By Type

- Hardware

- Software

- Services

By Deployment

- On-premise

- Cloud

By Enterprise Size

- Large Enterprise

- Small & Medium Enterprises

By Vertical

- BFSI

- IT and Telecom

- Retail & E-commerce

- Healthcare

- Manufacturing

- Government

- Education

- Manufacturing

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is driving the growth of the Network Access Control (NAC) market in Europe?

The growth is fueled by increasing cybersecurity concerns, stringent regulatory requirements (e.g., GDPR), the rise of IoT devices, and the shift to remote work and BYOD policies. Businesses are adopting NAC solutions to secure networks and ensure compliance with evolving security standards.

2. Which industries are the largest adopters of Network Access Control solutions in Europe?

Key industries include BFSI (Banking, Financial Services, and Insurance), healthcare, IT & telecom, manufacturing, and government sectors. These industries prioritize NAC solutions to protect sensitive data and manage access control for connected devices.

3. What challenges does the Network access control market face in Europe?

The market faces challenges such as high initial deployment costs, integration complexities with legacy systems, and a shortage of skilled professionals to manage advanced security solutions. Additionally, evolving cyber threats targeting IoT devices pose ongoing risks.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]