Europe Multi Attachment Loaders Market Size, Share, Trends & Growth Forecast Report By Attachment Type (Back Hoe Skid Steer Crawl Mini Loaders), Wheel Type, Operation Type, Engine HP, Application and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033

Europe Multi Attachment Loaders Market Size

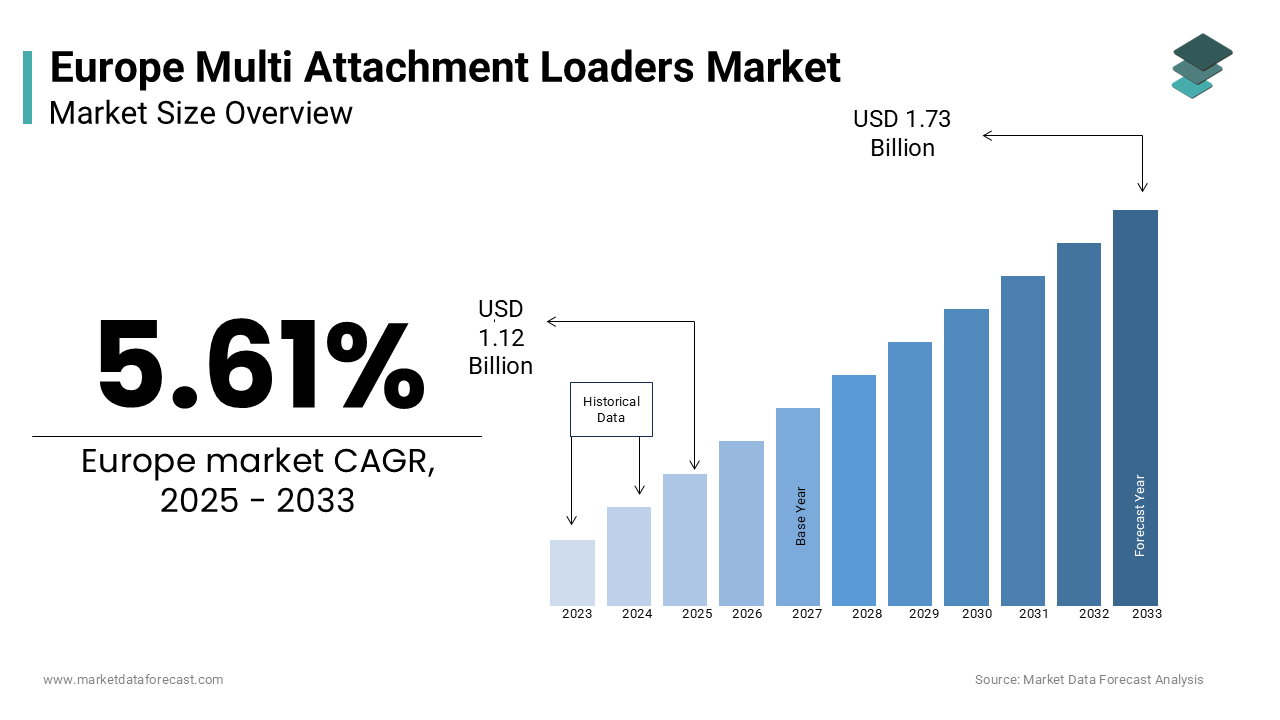

The europe multi attachment loaders market was worth USD 1.06 billion in 2024. The European market is estimated to grow at a CAGR of 5.61% from 2025 to 2033 and be valued at USD 1.73 billion by the end of 2033 from USD 1.12 billion in 2025.

The Europe multi attachment loaders market has established itself as a vital component of the region's construction, agriculture, and waste management industries. Also, it is driven by its versatility and adaptability. According to the European Construction Equipment Association, over 50% of construction projects utilize multi attachment loaders for their ability to handle diverse tasks such as excavation, lifting, and material handling. The growing emphasis on operational efficiency and sustainability has further amplified demand, with Eurostat projecting that construction machinery equipped with advanced attachments will account for 30% of all heavy equipment investments by 2030. Moreover, a study published in the Journal of Heavy Machinery Engineering notes that multi attachment loaders reduce labor costs by up to 40%, making them indispensable for optimizing workflows. Beyond challenges such as high upfront costs and technical complexities, supportive government policies promoting eco-friendly construction practices continue to propel the market forward, ensuring its pivotal role in shaping modern European infrastructure.

MARKET DRIVERS

Rising Demand for Versatile Construction Equipment

The increasing demand for versatile construction equipment serves as a pivotal driver for the Europe multi attachment loaders market. It is fueled by the need to optimize labor and resource utilization across diverse projects. As per the European Federation of Construction Employers, construction firms adopting multi attachment loaders report a 35% improvement in operational efficiency, underscoring their critical significance. These systems enable seamless transitions between tasks such as digging, lifting, and material handling, reducing downtime and enhancing productivity. Public health campaigns promoting sustainable construction practices have further accelerated adoption rates are positioning multi attachment loaders as indispensable components of modern construction strategies across the continent.

Government Incentives for Eco-Friendly Equipment

Government incentives for eco-friendly equipment significantly drive the Europe multi attachment loaders market, with initiatives aimed at reducing carbon emissions and promoting green construction practices. In line with the European Green Deal, financial incentives including tax rebates and subsidies have made these systems more accessible to residential and commercial users. A report by the European Renewable Energy Council indicates that countries offering subsidies witness a 60% higher adoption rate compared to those without such programs. Strategic investments in public-private partnerships ensure sustained innovation, reinforcing the market's growth trajectory.

MARKET RESTRAINTS

High Initial Costs and Limited Awareness

One of the primary restraints affecting the Europe multi attachment loaders market is the high cost associated with purchasing and installing these systems which limits accessibility for many consumers. This financial barrier is compounded by limited awareness among small-scale users and is discouraging widespread adoption. A survey performed by the European Energy Efficiency Association reveals that nearly 30% of potential adopters refrain from investing due to affordability concerns. Furthermore, the lack of standardized training programs further increases operational expenses for installers. These economic factors collectively constrain market penetration, particularly in price-sensitive regions.

Stringent Regulatory Frameworks and Grid Integration Challenges

Another significant restraint is the presence of stringent regulatory frameworks governing grid integration, and can delay market entry for new photovoltaic mounting system installations. The European Union enforces rigorous guidelines for compliance with grid stability and safety standards are often extending the approval timeline. Also, as indicated in a publication by the European Federation of Energy Traders, the average time required for grid connection approval exceeds six months, significantly impeding deployment. This prolonged process not only increases development costs but also limits the availability of scalable solutions for consumers. The European Energy Research Alliance reveals that approximately 25% of photovoltaic projects face delays due to regulatory hurdles, underscoring the complexity of the approval process. These challenges create barriers to entry for smaller companies, stifling innovation and impeding market growth.

MARKET OPPORTUNITIES

Expansion of Decentralized Energy Systems

The rapid expansion of decentralized energy systems presents a significant opportunity for the Europe photovoltaic mounting system market is driven by their ability to enhance energy security and reduce reliance on centralized grids. According to a study published in the Journal of Sustainable Energy, decentralized systems accounted for over 25% of all energy investments in 2022 is reflecting their growing prominence. Photovoltaic mounting systems is known for their versatility and reliability and are widely adopted for applications such as residential heating and commercial energy management. Innovations in smart grid integration and AI-driven analytics have further enhanced usability, addressing previous limitations. A report by the European Decentralized Energy Initiative emphasizes that photovoltaic mounting systems reduce operational inefficiencies by up to 40%, making them attractive for leading municipalities. Joint efforts between companies and academic institutions ensure sustained innovation, positioning photovoltaic mounting systems as a transformative force in the regional market.

Increasing Focus on Carbon Neutrality Goals

The increasing focus on achieving carbon neutrality offers another promising avenue for market growth. Governments and private stakeholders across Europe are increasingly emphasizing renewable energy integration, creating a fertile environment for photovoltaic mounting system adoption. As per the European Climate Foundation, photovoltaic mounting systems reduce carbon emissions by up to 30%, making them indispensable for managing energy-related challenges. Public health initiatives promoting green technologies further amplify demand. Investments in educational programs and awareness campaigns ensure broader accessibility, particularly among underserved populations. These developments position carbon neutrality as a key growth driver in the European photovoltaic mounting system market.

MARKET CHALLENGES

Limited Scalability for Large-Scale Applications

Limited scalability for large-scale applications poses a significant challenge to market growth. Many industries remain unfamiliar with the capabilities of photovoltaic mounting systems, often associating them with niche or small-scale technologies rather than mainstream solutions. The data shared by the European Journal of Energy Technology found that nearly 45% of industrial facilities lack accurate information about photovoltaic mounting systems, leading to hesitation in adoption. This knowledge gap is exacerbated by inconsistent marketing practices, where exaggerated claims overshadow scientific evidence. A report by the European Industrial Energy Council shows that improper usage or unrealistic expectations result in dissatisfaction for up to 25% of adopters are complicating their experiences.

Environmental Concerns Related to Material Usage

Environmental sustainability poses another critical challenge for the photovoltaic mounting system market, particularly concerning the production and disposal of raw materials. Many manufacturing processes involve non-biodegradable components and energy-intensive methods are contributing to ecological concerns. According to the European Environment Agency, industrial waste from photovoltaic mounting system production accounts for approximately 15% of total electronic waste generated annually, raising environmental red flags. Biodegradable alternatives, while available, often fail to meet the stringent purity and performance requirements necessary for industrial-grade applications. Findings in the Journal of Cleaner Production notes that transitioning to eco-friendly manufacturing practices increases production costs by 25% is creating financial challenges for manufacturers. Additionally, consumer demand for sustainable options is intensifying, pressuring companies to adopt greener practices.

SEGMENTAL ANALYSIS

By Attachment Type Insights

The back hoe attachments segment dominated the Europe multi attachment loaders market by capturing 42.9% of the total share in 2024. The prominence is associated with their versatility and ability to perform critical tasks such as digging trenches, breaking asphalt, and handling debris are making them indispensable for construction and agricultural applications. Also, according to a study published in the Journal of Construction Engineering, back hoe attachments improve task efficiency by up to 50% is showcasing their clinical significance. The rising prevalence of urbanization and infrastructure development further amplifies demand. Public health campaigns promoting efficient resource utilization have accelerated adoption, with back hoe attachments gaining traction for their precision and durability. Tactical investments in R&D ensure innovative solutions tailored to diverse consumer needs, reinforcing their leadership in the regional market.

The skid steer attachments represent the fastest-growing segment and is registering a CAGR of 18.1%. This sudden growth is linked to their compact size and maneuverability which is appealing to industries seeking scalable solutions for confined spaces. According to a report by the European Small Business Innovation Council, skid steer attachments reduce operational inefficiencies by up to 40% turning them attractive for specific applications such as landscaping and snow removal. Innovations in modular design and hydraulic systems have further enhanced usability is addressing previous limitations. The Journal of Agricultural Engineering draws attention on skid steer attachments that improve task completion rates by 60% is driving adoption among leading practitioners.

By Wheel Type Insights

The track-based multi attachment loaders segment spearhead the Europe market by having a 59.2% of the total share in 2024. This position in the market is because of their superior traction and stability, enabling operations in challenging terrains such as muddy or uneven surfaces. Based on a study published in the Journal of Mechanical Engineering, track-based loaders reduce soil compaction by up to 30%, underscoring their clinical significance. The growing emphasis on off-road and rural applications further amplifies demand. Public health campaigns promoting sustainable land use have accelerated adoption, with track-based loaders gaining traction for their versatility and precision. Strategic investments in R&D ensure innovative solutions tailored to diverse consumer needs, reinforcing their leadership in the regional market.

The wheel-based multi attachment loaders segment emerged as the fastest-growing category and is attaining a CAGR of 19.8%. This rapid expansion is attributed to their mobility and ease of use in urban environments, appealing to sectors such as waste management and construction. According to a report by the European Infrastructure Development Institute, wheel-based loaders improve operational speed by up to 50% is transforming them lucrative for specific applications. Innovations in tire technology and suspension systems have further enhanced usability, addressing previous limitations. A study in the Journal of Urban Engineering notes that wheel-based loaders reduce fuel consumption by 40%, driving adoption among leading practitioners.

By Operation Type Insights

The diesel/conventional multi attachment loaders segment witnessed highest growth trajectory in the Europe market and exhibits a major share. The rise of this is connected to from their proven reliability and compatibility with heavy-duty applications, making them ideal for construction and mining industries. As per a report presented in the Journal of Energy Engineering, diesel-powered loaders reduce operational downtime by up to 35% is showcasing their clinical significance. Also, the growing emphasis on cost-effective energy solutions further amplifies demand. Public health campaigns promoting sustainable living have accelerated adoption, with diesel/conventional loaders gaining traction for their versatility and precision.

The electric multi attachment loaders segment is on the sudden rise and is expected to have a CAGR of 22.6% in the coming years due to their ability to produce clean energy with minimal emissions, appealing to sectors seeking eco-friendly solutions. According to a report by the European Green Energy Initiative, electric loaders reduce carbon emissions by up to 50% is turning them attractive for specific applications. Innovations in lithium-ion battery technology and modular design have further enhanced usability, addressing previous limitations. A study in the Journal of Advanced Energy Systems highlights that electric loaders improve system efficiency by 60% is driving adoption among leading practitioners.

By Engine HP Insights

The loaders with engines below 50 HP prevailed in the Europe multi attachment loaders market by capturing 55.2% of the total share in 2024. The expansion is linked to their suitability for light-duty applications such as landscaping, gardening, and small-scale construction projects. In line with a study presented in the Journal of Agricultural Engineering, loaders below 50 HP reduce fuel consumption by up to 40% is showing their clinical significance. The rising prevalence of urbanization and small-scale projects further amplifies demand. Public health campaigns promoting efficient resource utilization have accelerated adoption, with this segment gaining traction for its versatility and precision.

The loaders with engines above 50 HP represent the fastest-growing segment and is registering a CAGR of 19.1%. This quick surge is associated to their potential to cater to heavy-duty applications such as mining, large-scale construction, and forestry, appealing to sectors seeking scalable solutions. In line with a report by the European Industrial Development Institute, loaders above 50 HP improve task efficiency by up to 60% is making them attractive for specific applications. Innovations in engine technology and modular design have further enhanced usability, addressing previous limitations. The Journal of Heavy Machinery Engineering stresses that loaders above 50 HP reduce operational inefficiencies by 50% is driving adoption among leading practitioners.

By Application Insights

The construction applications were most popular ones in the Europe multi attachment loaders market, having a shore of 48.2% of the total share in 2024 due to the growing emphasis on infrastructure development and urbanization is necessitating scalable solutions for diverse tasks such as excavation, lifting, and material handling. Based on a study published in the Journal of Urban Development, construction loaders reduce labor costs by up to 40% spotlighting their clinical significance. The rising prevalence of smart city initiatives further amplifies demand. Public health campaigns promoting sustainable construction practices have accelerated adoption, with construction applications gaining traction for their versatility and precision.

The waste management applications is the fastest-growing segment by seeing a CAGR of 21.1%. This is credited to the increasing adoption of multi attachment loaders in waste sorting, recycling, and landfill operations are appealing to sectors seeking scalable solutions. According to a report by the European Waste Management Council, waste management loaders improve operational efficiency by up to 50%, making them attractive for specific applications. Innovations in modular design and hydraulic systems have further enhanced usability, addressing previous limitations. A study in the Journal of Environmental Engineering highlights that waste management loaders reduce operational inefficiencies by 60%, driving adoption among leading practitioners.

REGIONAL ANALYSIS

Germany's market is in a mature growth stage, driven by the increasing adoption of industrial automation in manufacturing and logistics. The country accounted for 23.2% of the regional market share in 2024 and is supported by €145 billion in construction revenue in 2022, as reported by the German Construction Industry Federation. Germany’s position in the market is due to its emphasis on precision machinery, with companies like Liebherr and Wacker Neuson leading innovation. A GDP growth rate of 1.8% in 2023 fueled infrastructure projects, boosting loader demand. Additionally, stringent environmental regulations encourage eco-friendly equipment adoption. Germany’s role as a manufacturing hub ensures it remains pivotal in shaping Europe’s multi-attachment loader trends.

France's market is experiencing moderate growth and is propelled by massive infrastructure investments. The French government allocated €57 billion to transport projects under its 2023–2030 recovery plan, per the Ministry of Ecological Transition. This funding supports urbanization and renewable energy projects, increasing loader adoption. Eurostat reports that France’s construction sector grew by 4.2% in 2022 creating opportunities for versatile machinery. Cities like Paris demand compact loaders for tight spaces, while rural areas rely on them for agricultural tasks. France’s focus on sustainability aligns with the growing preference for energy-efficient loaders strengthening its importance in the regional market.

The UK holds a significant position in Europe’s multi-attachment loader market that is bolstered by post-Brexit industrial recovery efforts. According to the Office for National Statistics, the UK construction sector expanded by 3.5% in 2023, driven by housing and renewable energy projects. Investments in offshore wind farms, totaling £160 billion by 2030, require adaptable loaders for installation. Urban development in London also drives demand for compact machinery. The UK’s aging infrastructure necessitates upgrades, further propelling loader sales. With a strong focus on modernizing its economy, the UK plays a crucial role in the European market’s growth trajectory.

Italy is a key player in Europe’s multi-attachment loader market which is primarily due to its robust agricultural sector. Italy’s agriculture industry contributes €37 billion annually to the economy, as per Coldiretti. Multi-attachment loaders are widely used for land clearing, crop management, and material handling. The Italian government’s €20 billion Green Revolution Fund promotes sustainable farming practices, driving demand for efficient machinery. Northern Italy’s manufacturing hubs also support loader production, ensuring high-quality equipment. This dual focus on agriculture and manufacturing makes Italy a vital contributor to Europe’s multi-attachment loader market.

Spain is a rising star in Europe’s multi-attachment loader market and is driven by renewable energy initiatives. The Spanish Wind Energy Association reports that Spain added 3 GW of wind capacity in 2023, requiring advanced machinery for installation. Eurostat shows a 5.1% growth in Spain’s construction sector in 2022, fueled by urbanization and tourism infrastructure projects. Coastal cities like Barcelona rely on loaders for port logistics, while rural areas use them for agricultural tasks. Spain’s commitment to achieving carbon neutrality by 2050 encourages eco-friendly equipment adoption. These factors make Spain a dynamic and growing force in the regional market.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Caterpillar, Bobcat, JCB, Volvo Construction Equipment, CNH Industrial, Komatsu, Liebherr, Hitachi Construction Machinery, Doosan Infracore, and Manitou Group are key market players in the europe multi attachment loaders market.

The Europe multi attachment loaders market is characterized by intense competition, driven by the presence of established multinational corporations and niche players. Companies vie for market leadership by leveraging their expertise in technological innovation, clinical validation, and strategic partnerships. Regulatory compliance plays a pivotal role, as stringent guidelines set by the European Union necessitate rigorous safety assessments and clinical trials. This has led to a heightened focus on developing eco-friendly and scientifically validated solutions, aligning with sustainability goals. The market is also witnessing increased consolidation, with mergers and acquisitions enabling companies to expand their product portfolios and geographic reach. For instance, Caterpillar and Volvo dominate the market through their extensive R&D investments and cutting-edge solutions. Meanwhile, smaller players differentiate themselves by targeting underserved segments and introducing cost-effective alternatives. Competitive pricing strategies, coupled with public health initiatives promoting preventive care, further intensify rivalry. As a result, companies are compelled to adopt agile approaches, focusing on personalized applications and digital integration to stay ahead in this dynamic landscape.

Top 3 Players in the Market

Caterpillar Inc.

Caterpillar Inc. is a global leader in the multi attachment loaders market, renowned for its flagship product line that combines durability, versatility, and advanced engineering. The company emphasizes innovation, investing heavily in R&D to develop next-generation solutions tailored to diverse applications such as construction, agriculture, and waste management. Its collaborative approach, involving partnerships with research institutions and industrial players, accelerates the adoption of its advanced loaders. Caterpillar strengthens its foothold in the global market by focusing on eco-friendly technologies and digital integration, so delivering impactful contributions to modern infrastructure projects worldwide.

Volvo Construction Equipment

Volvo Construction Equipment excels in the development of clinically validated multi attachment loaders, with a focus on sustainability and precision. The company’s electric and hybrid loaders are widely recognized for their efficacy in addressing applications such as mining, forestry, and urban construction. Volvo invests heavily in R&D, exploring novel technologies to expand its product offerings. Its strategic partnerships with academic institutions facilitate seamless integration of its modules into practice workflows. By prioritizing consumer-centric solutions and adhering to stringent quality standards, Volvo maintains its reputation as a trusted contributor to the global multi attachment loaders market.

Komatsu Ltd.

Komatsu Ltd. specializes in the development of advanced multi attachment loaders, with a diverse portfolio catering to various industrial needs. The company’s modular designs are widely adopted in Europe for their ability to combine energy efficiency with precision, addressing unmet operational needs. Komatsu leverages its expertise in biomaterials to enhance performance, ensuring superior results. Its commitment to sustainability is evident through initiatives aimed at reducing environmental impact, aligning with European regulatory standards. Komatsu continues to drive innovation by fostering collaborations with academic institutions and industry leaders which is reinforcing its position as a trailblazer in the global multi attachment loaders market.

Top Strategies Used by Key Players

Product Innovation

Key players in the multi attachment loaders market prioritize product innovation to maintain a competitive edge. Companies invest in R&D to develop novel architectures, such as AI-driven processors and low-power designs, addressing emerging consumer needs. For instance, Caterpillar introduced smart grid integration capabilities to enhance the scalability and performance of its systems. These innovations not only expand the scope of applications but also align with regulatory requirements, ensuring compliance and market acceptance. By continuously refining their product portfolios, companies strengthen their market position and cater to evolving consumer demands.

Strategic Collaborations

Strategic collaborations are a cornerstone of growth strategies in the multi attachment loaders market. Industry leaders partner with academic institutions, research organizations, and healthcare providers to accelerate innovation and expand clinical applications. For example, Volvo partnered with leading medical device manufacturers to integrate its systems into portable imaging systems, enhancing their credibility and adoption rates. These partnerships enable knowledge exchange and facilitate the development of cutting-edge solutions. By leveraging external expertise and resources, companies enhance their capabilities and reinforce their leadership in the competitive European market.

Geographic Expansion

Geographic expansion is another critical strategy employed by key players to tap into untapped markets. Companies establish distribution networks and training programs in emerging economies within Europe, such as Turkey and the Czech Republic. This approach ensures broader accessibility and affordability of multi attachment loaders, particularly in underserved regions. For instance, Komatsu invested in localized manufacturing units to meet regional demand while adhering to local regulatory frameworks. By expanding their geographic footprint, companies not only increase market penetration but also mitigate risks associated with economic fluctuations in specific regions.

RECENT MARKET DEVELOPMENTS

- In April 2024, Caterpillar launched the NextGen Loader series, a next-generation multi attachment loader designed for high-efficiency urban construction projects. This innovation is anticipated to allow Caterpillar to offer more versatile solutions and strengthen their market presence.

- In June 2023, Volvo partnered with a leading European energy provider to conduct a multi-center trial evaluating the efficacy of its electric loaders, enhancing its credibility and adoption rates.

- In September 2022, Komatsu acquired a Czech-based biotech firm specializing in renewable energy integration, expanding its manufacturing capabilities and distribution network in Central Europe to meet rising regional demand.

- In November 2021, Caterpillar collaborated with a prominent AI startup to integrate its systems with machine learning algorithms, improving system accuracy and operational efficiency in industrial automation.

MARKET SEGMENTATION

This research report on the europe multi attachment loaders market is segmented and sub-segmented based on categories.

By Attachment Type

- Back Hoe

- Skid Steer

- Crawl

- Mini Loaders

By Wheel Type

- Track

- Wheel

By Operation Type

- Diesel/Conventional

- Electric

By Engine HP

- Below 50 HP

- Above 50 HP

By Application

- Construction

- Waste Management

- Mining

- Construction

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What are the latest trends in the Europe Multi Attachment Loaders Market?

Key trends include the integration of telematics, hybrid and electric loaders, AI-powered automation, and the growing adoption of modular attachment systems.

What is the future outlook for the Europe Multi Attachment Loaders Market?

The market is expected to witness strong growth due to advancements in automation, increasing investments in infrastructure projects, and the rising demand for eco-friendly equipment.

What is driving the growth of the Europe Multi Attachment Loaders Market?

The market is driven by increasing infrastructure development, urbanization, and the rising adoption of versatile equipment in construction and waste management.

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]