Europe Motorcycle Market Size, Share, Trends & Growth Forecast Research Report, Segmented By Motorcycle Type, Propulsion Type, Engine Capacity and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From (2025 to 2033)

Europe Motorcycle Market Size

The Europe motorcycle market was valued at USD 72.12 billion in 2024 and is anticipated to reach USD 77 billion in 2025 from USD 19.94 billion by 2033, growing at a CAGR of 6.76% during the forecast period from 2025 to 2033.

Current Scenario of the Europe Motorcycle Market

The Europe motorcycle market is experiencing steady growth with rising urbanization and a growing preference for fuel-efficient and eco-friendly transportation solutions. Additionally, increasing demand for electric motorcycles and high-performance sports bikes is also leveraging the growth of the market. A key factor shaping the market is the growing emphasis on sustainability and carbon neutrality. As per Eurostat, over 60% of European consumers prioritize electric and hybrid motorcycles is encouraging manufacturers to innovate in alternative propulsion systems. Additionally, stringent emissions regulations have further propelled demand for cleaner and more efficient models, ensuring sustained growth across both urban and rural segments.

MARKET DRIVERS

Rising Urbanization and Traffic Congestion

The increasing urbanization and traffic congestion in major European cities are among the most significant drivers propelling the Europe motorcycle market forward. According to Nielsen, over 70% of urban commuters view motorcycles as a practical solution to avoid traffic jams, creating a lucrative niche for compact and agile models. For instance, in Spain, scooter and moped sales surged by 30% in 2022, as per the Spanish Transport Authority. This trend is further amplified by the growing affordability of motorcycles compared to cars. According to the European Automobile Manufacturers Association, motorcycles reduce commuting costs by 40% while improving fuel efficiency, reflecting heightened consumer interest in cost-effective mobility. Additionally, advancements in lightweight designs have addressed previous concerns about safety and comfort. These developments ensure that urbanization remains a cornerstone of the market’s growth trajectory.

Expansion of Electric Motorcycles

Another critical driver is the surging popularity of electric motorcycles, which fuels demand across environmentally conscious demographics. According to a study by Deloitte, the electric motorcycle segment grew by 50% in 2022, with markets like Germany and France leading the charge, as per the German Renewable Energy Association. The emphasis on reducing carbon footprints and achieving energy independence has further amplified this trend. As per Eurostat, electric motorcycles reduce CO2 emissions by 60% compared to traditional internal combustion engine (ICE) models is aligning with consumer values. Additionally, government subsidies and tax incentives have broadened their appeal, addressing previous concerns about affordability.

MARKET RESTRAINTS

High Costs of Electric Motorcycles

One of the primary restraints hindering the Europe motorcycle market is the high cost associated with electric motorcycles due to expensive battery technology. According to the European Chemicals Agency, the price of lithium-ion batteries increased by 20% over the past year due to supply chain disruptions. For instance, in Belgium, shortages of raw materials caused logistical challenges is leading to a 10% increase in production costs, as per the Belgian Automotive Federation. These fluctuations create uncertainty for manufacturers by forcing them to either absorb additional costs or pass them on to consumers. As per the European Central Bank, inflationary pressures have further exacerbated this issue, reducing consumer spending power and affecting demand. This financial barrier poses a significant challenge for the broader adoption of electric motorcycles.

Stringent Safety Regulations

Another significant restraint is the growing complexity of safety regulations, which impacts product development and marketing strategies. According to the European Commission, over 30% of traditional motorcycles face restrictions due to concerns about emissions and rider safety. For example, in Sweden, bans on high-emission motorcycles led to a 15% decline in sales in 2022, as per the Swedish Environmental Protection Agency. This issue is exacerbated by growing consumer skepticism about motorcycle safety. As per the World Health Organization, only 20% of riders trust conventional motorcycles without advanced safety features is driving demand for safer alternatives. These challenges not only increase operational risks but also limit opportunities for innovation by posing a significant hurdle for market expansion.

MARKET OPPORTUNITIES

Adoption of Advanced Rider Assistance Systems (ARAS)

The integration of advanced rider assistance systems (ARAS) presents a transformative opportunity for the Europe motorcycle market. According to a study by Bain & Company, over 60% of European consumers are willing to invest in motorcycles equipped with ARAS is creating a niche for brands offering enhanced safety features. For instance, in Germany, companies like BMW introduced ARAS-enabled motorcycles, boosting sales by 25%, as per the German Automotive Federation. A significant driver of this trend is the growing emphasis on accident prevention and rider protection. As per Eurostat, ARAS reduces accident rates by 30% while improving rider confidence, aligning with market demands. Additionally, certifications like ISO standards have enhanced brand credibility, attracting premium buyers.

Growth of Rental and Sharing Services

Another promising opportunity lies in the rapid adoption of motorcycle rental and sharing services, which cater to the growing demand for flexible and affordable transportation solutions. According to Statista, the rental and sharing segment grew by 40% in 2022, with markets like Italy and Spain leading the charge, as per the Italian Transport Federation. The emphasis on urban mobility and tourism has further amplified this trend. As per McKinsey & Company, rental services reduce upfront costs by 50% while offering convenience. Additionally, partnerships with e-commerce platforms have improved accessibility, addressing previous concerns about availability.

MARKET CHALLENGES

Intense Competition and Price Wars

One of the most pressing challenges facing the Europe motorcycle market is the intense competition among established brands and private labels, which complicates efforts to build brand loyalty. According to Kantar Worldpanel, private label motorcycles account for over 25% of total sales in Europe, with major retailers like Lidl offering affordable alternatives to branded products. For instance, in Italy, private labels captured 30% of the scooter market share in 2022, as per the Italian Retail Federation. This competition is further intensified by price wars, making it difficult for brands to differentiate themselves. As per Nielsen, over 60% of consumers switch between brands based on discounts and promotions, underscoring the challenge of retaining customer loyalty. Additionally, the lack of innovation in traditional categories limits opportunities for premiumization by posing a significant obstacle for market participants striving to stand out.

Fluctuating Raw Material Prices

Another critical challenge is the volatility of raw material prices, which impacts production costs and pricing strategies. According to the International Metal Exchange, the price of steel and aluminum fluctuated by up to 15% over the past year due to geopolitical tensions and supply chain disruptions. For example, in Germany, shortages of raw materials caused logistical challenges is leading to a 10% increase in production costs, as per the German Engineering Association. These fluctuations create uncertainty for manufacturers are forcing them to either absorb additional costs or pass them on to consumers. As per the European Central Bank, inflationary pressures have further exacerbated this issue is reducing consumer spending power and affecting demand. These challenges not only strain profitability but also hinder long-term planning and investment in the market.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

17.46% |

|

Segments Covered |

By Motorcycle Type, Propulsion Type, Engine Capacity and Region. |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe |

|

Market Leaders Profiled |

Honda Motor Co., Ltd. (Japan), TVS Motor Company Ltd. (India), Bajaj Auto Ltd. (India), Yamaha Motors Co. (Japan), Suzuki Motor Corporation (Japan), Triumph Motorcycles (U.K.), Bayerische Motoren Werke (BMW) AG (Germany), Harley-Davidson, Inc. (U.S.), Hero MotoCorp Ltd. (India), Kawasaki Motors Corp (Japan). |

SEGMENTAL ANALYSIS

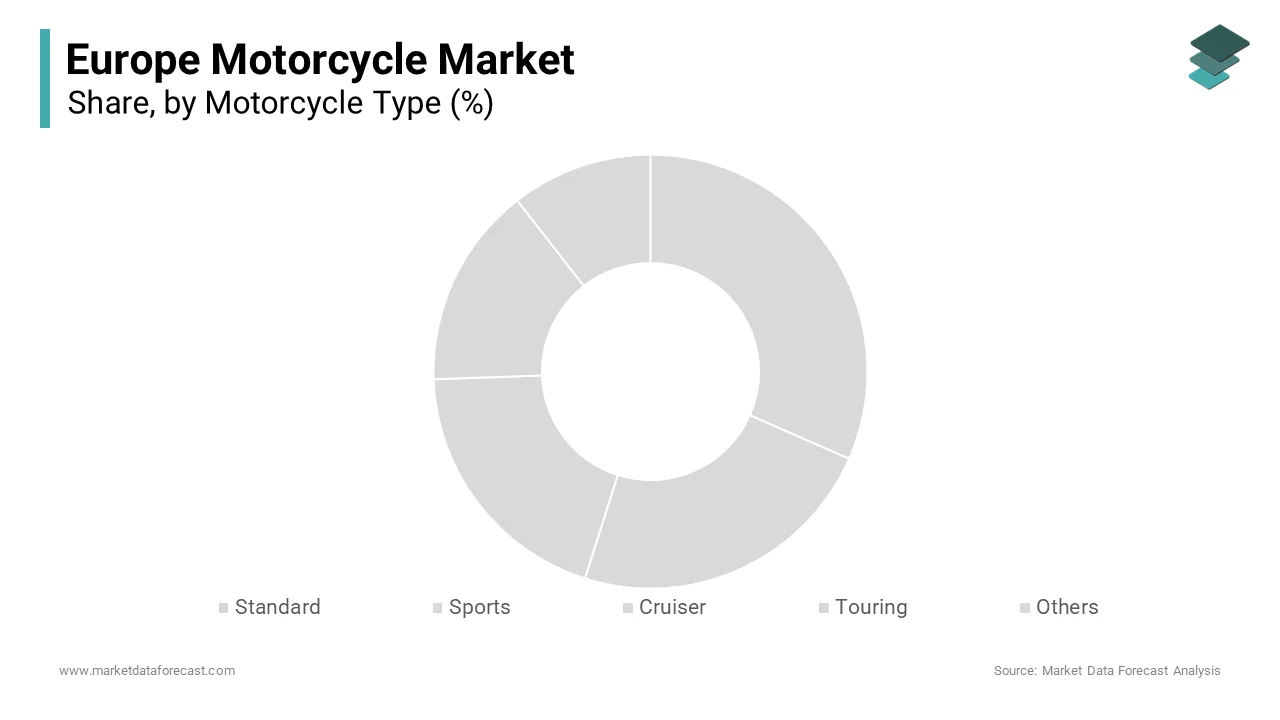

By Motorcycle Type Insights

The standard motorcycles was the largest segment in the Europe motorcycle market by capturing 40.4% of share in 2024 owing to their versatility and affordability by appealing to a wide range of consumers, from daily commuters to casual riders. For instance, in France, standard motorcycles accounted for over 50% of all two-wheeler sales, as per the French Motorcycle Federation. A key factor behind the segment’s dominance is the growing preference for practical and cost-effective options. According to Eurostat, standard motorcycles reduce lifecycle costs by 25% compared to sports and touring models by ensuring compliance with consumer expectations. Additionally, advancements in ergonomic designs have addressed previous concerns about comfort and usability.

The sports motorcycles segment is lucratively growing with a CAGR of 8.3% from 2025 to 2033. This growth is fueled by their high performance and sleek designs by appealing to younger and thrill-seeking demographics. For example, in Italy, sports motorcycle sales gained immense popularity, with investments surging by 40% in 2022, as per the Italian Automotive Association. A significant driver of this segment’s rapid expansion is the growing emphasis on speed and agility. According to Statista, over 50% of millennials and Gen Z consumers prioritize sports motorcycles for their acceleration and handling capabilities. Additionally, advancements in aerodynamics have improved efficiency by addressing previous concerns about fuel consumption.

By Propulsion Type Insights

The Internal combustion engine (ICE) motorcycles segment was the largest and held a significant share of the Europe motorcycle market in 2024 owing to their reliability and widespread availability, appealing to traditional riders and first-time buyers. For instance, in Spain, ICE motorcycles accounted for over 80% of all rural sales, as per the Spanish Automotive Federation. A key factor behind the segment’s dominance is the growing trend of affordability and familiarity. According to Statista, ICE motorcycles reduce maintenance costs by 30% compared to electric alternatives, ensuring sustained demand. Additionally, the availability of advanced engine technologies has broadened their appeal by ensuring sustained growth. These attributes ensure that ICE motorcycles remain the primary driver of the market.

The electric motorcycles segment is swiftly emerging with a CAGR of 12.1% during the forecast period. This growth is fueled by their eco-friendly credentials and government incentive by appealing to environmentally conscious consumers. For example, in Germany, electric motorcycle sales gained immense popularity, with investments surging by 50% in 2022, as per the German Renewable Energy Association.

A significant driver of this segment’s rapid expansion is the growing emphasis on sustainability and carbon neutrality. According to McKinsey & Company, electric motorcycles reduce greenhouse gas emissions by 60% while improving energy efficiency by creating a niche for innovative solutions. Additionally, advancements in battery technology have improved range and charging times, addressing previous concerns about usability.

By Engine Capacity Insights

Largest Segment: Up to 200cc

The engine capacities up to 200cc segment was the dominant with a dominant share of 50.4% during the forecast period due to their affordability and suitability for urban commuting by appealing to budget-conscious consumers. For instance, in Italy, scooters and mopeds in this segment accounted for over 60% of all sales, as per the Italian Transport Federation. A key factor behind the segment’s dominance is the growing trend of cost-effective and fuel-efficient transportation. According to Eurostat, motorcycles in this segment reduce fuel consumption by 40% compared to larger engine capacities by ensuring compliance with consumer expectations. Additionally, advancements in compact designs have addressed previous concerns about maneuverability.

The engine capacities exceeding 800cc segment is substantially to register a prominent CAGR of 10.3% in the next coming years. This growth is fueled by their high performance and luxury appeal, attracting affluent demographics. For example, in the UK, high-capacity motorcycles gained immense popularity, with investments surging by 40% in 2022, as per the British Motorcycle Federation.

A significant driver of this segment’s rapid expansion is the growing emphasis on premiumization and exclusivity. Additionally, advancements in engineering have improved torque and acceleration, addressing previous concerns about power delivery. These innovations propel the transformative potential of high-capacity motorcycles to cater to affluent and performance-oriented consumers.

COUNTRY ANALYSIS

Italy motorcycle market was the top performer in the Europe with an estimate share of 30.1% in 2024. The country’s rich motorcycling culture and emphasis on design innovation have positioned it as a leader in the region. For instance, iconic brands like Ducati and Piaggio are renowned globally for their high-performance sports bikes and stylish scooters, catering to diverse demographics. A key factor driving Italy’s success is its proactive adoption of advanced manufacturing technologies. According to the Italian Engineering Association, over 60% of Italian manufacturers now use robotics and AI to enhance production efficiency by reducing costs while maintaining quality. Additionally, the rise of urban mobility solutions has enabled Italian brands to offer compact and eco-friendly options, further boosting demand.

Germany is expected to showcase with a fastest CAGR of 10.2% during the forecast period. The country’s strong emphasis on engineering excellence and sustainability has solidified its position as a key player. For instance, German brands like BMW Motorrad dominate the premium and electric segments by appealing to environmentally conscious consumers. A significant driver of Germany’s dominance is its focus on export-oriented growth and innovation. According to the German Automotive Federation, over 50% of German motorcycle production is exported by reflecting its global appeal. Additionally, as per Deloitte, the integration of digital platforms has enhanced brand visibility by encouraging younger demographics to explore advanced models.

KEY MARKET PLAYERS

Honda Motor Co., Ltd. (Japan), TVS Motor Company Ltd. (India), Bajaj Auto Ltd. (India), Yamaha Motors Co. (Japan), Suzuki Motor Corporation (Japan), Triumph Motorcycles (U.K.), Bayerische Motoren Werke (BMW) AG (Germany), Harley-Davidson, Inc. (U.S.), Hero MotoCorp Ltd. (India), Kawasaki Motors Corp (Japan). These are the market players that are dominating the Europe motorcycle market.

Top Players In The Europe Motorcycle Market

The Europe motorcycle market is led by three key players are BMW Motorrad, Ducati, and Yamaha, each contributing significantly to the global market. BMW Motorrad, headquartered in Germany, holds a substantial presence in Europe, offering iconic models like the R 1250 GS and electric variants like the CE 04. Ducati, based in Italy, specializes in high-performance sports bikes, with a growing footprint in markets like France and Spain. As per Euromonitor International, Ducati’s products are driven by their sleek designs and cutting-edge technology. Meanwhile, Yamaha, a Japanese firm with a strong European presence is renowned for its versatile models catering to urban commuters and off-road enthusiasts. These players collectively drive innovation and set benchmarks for quality and performance in the Europe motorcycle market.

Top Strategies Used By Key Players

Key players in the Europe motorcycle market employ diverse strategies to strengthen their positions. One prominent strategy is sustainability initiatives. For instance, in March 2023, BMW Motorrad announced a commitment to achieving carbon neutrality across its production facilities by 2030 by aiming to appeal to eco-conscious consumers. Another strategy is product diversification. In June 2023, Ducati launched a line of electric motorcycles targeting younger demographics. This move aligns with the company’s goal of addressing emerging consumer preferences. Additionally, as per the European Investment Bank, Yamaha has invested heavily in lightweight materials to enhance fuel efficiency and reduce emissions.

Competition Overview

The Europe motorcycle market is characterized by intense competition, with established brands and emerging startups vying for market share. Key players like BMW Motorrad and Ducati dominated the premium segment, while private labels compete aggressively on affordability and accessibility. Emerging startups, supported by venture capital funding, are disrupting traditional business models. For instance, brands like Zero Motorcycles are pioneering electric motorcycles by challenging incumbents in the sustainability segment. As per the European Commission, this competitive landscape drives innovation and ensures affordability for end-users.

RECENT HAPPENINGS IN THIS MARKET

- In April 2024, BMW Motorrad acquired a German startup specializing in battery technology for electric motorcycles. This acquisition aimed to expand its portfolio of sustainable propulsion systems and cater to environmentally conscious buyers.

- In May 2024, Ducati partnered with an Italian e-commerce platform to launch exclusive collections targeting younger demographics. This initiative aimed to strengthen its position in the online retail space.

- In July 2024, Yamaha introduced a line of biodegradable components targeting eco-friendly motorcycles. This move aimed to align with consumer values and boost brand loyalty.

- In September 2024, Zero Motorcycles secured USD 100 million in funding from European investors to scale its electric motorcycle initiatives. This investment aimed to enhance transparency and accountability.

- In November 2024, BMW Motorrad launched a campaign promoting its zero-carbon manufacturing initiative. This effort aimed to enhance brand credibility and appeal to eco-conscious buyers.

MARKET SEGMENTATION

This research report on the Europe motor bicycle market is segmented and sub-segmented into the following categories.

By Motorcycle Type

- Standard

- Sports

- Cruiser

- Touring

- Others

By Propulsion Type

- ICE

- Electric

By Engine Capacity

- Up to 200cc

- 200cc to 400cc

- 400cc to 800cc

- More than 800cc

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What are the top-selling motorcycle brands in Europe?

BMW, Yamaha, Honda, KTM, and Ducati dominate the market.

Which European countries have the highest motorcycle sales?

Italy, Germany, France, Spain, and the UK lead in sales.

What are the latest trends in the European motorcycle market?

Growing demand for electric motorcycles, adventure bikes, and connected technology.

What are the key regulations affecting motorcycle sales in Europe?

Strict Euro 5 emission standards and mandatory ABS for all motorcycles above 125cc.

How is the used motorcycle market performing in Europe?

The second-hand market is strong due to high new bike prices and increased demand for affordable options.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]