Europe Microsurgery Robot Market Size, Share, Trends & Growth Forecast Report By Application (Neurosurgery, Oncology), Component, End User And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe), Industry Analysis From 2025 To 2033

Europe Microsurgery Robot Market Size

The Europe microsurgery robot market size was calculated to be USD 0.46 billion in 2024 and is anticipated to be worth USD 1.47 billion by 2033 from USD 0.52 billion in 2025, growing at a CAGR of 13.86% during the forecast period.

Microsurgery robots are revolutionizing healthcare in Europe by offering unparalleled precision and efficiency in complex surgical procedures. Germany tows the region in adopting these systems accounting for a major portion of total installations, as per the German Medical Technology Association. For instance, in 2021, investments in neurosurgical robotics increased by 15% and is supported by government incentives for digital healthcare integration. Also, the growing prevalence of minimally invasive surgeries has amplified demand is aligning with Europe’s focus on reducing hospital stays and recovery times. A report by McKinsey & Company puts on focus that hospitals adopting microsurgery robots can achieve operational efficiencies of up to 30% is showcasing their critical role in modern healthcare. In spite of the high costs, the market remains resilient due to ongoing innovation and rising patient expectations.

MARKET DRIVERS

Rising Demand for Minimally Invasive Surgeries

The increasing preference for minimally invasive surgeries is propelling the European microsurgery robot market. Microsurgery robots play a pivotal role in enabling these procedures and particularly in delicate operations like neurosurgery and ophthalmology. For example, in France, the adoption of robotic-assisted neurosurgery increased by 20% in 2022 and is driven by investments in advanced medical infrastructure. A study by Deloitte stresses that hospitals prioritize microsurgery robots for their precision and ability to reduce human error further amplifying demand. Apart from these, advancements in AI-driven navigation systems have enhanced surgical outcomes are making these robots indispensable in high-stakes environments.

Expansion of Digital Healthcare Ecosystems

The expansion of digital healthcare ecosystems is second major aspect boosting the microsurgery robot market. According to the European Commission, investments in digital health technologies exceeded €50 billion in 2022, with robotics being a key focus area. Microsurgery robots integrate seamlessly with telemedicine platforms are enabling remote surgeries and consultations. To give an idea, in Sweden, the acceptance of robotic-assisted otology procedures increased by 25% in 2021 and was supported by government incentives for telehealth integration. An investigation by PwC brings to light that over 70% of European healthcare providers prioritize solutions that enhance connectivity and interoperability is further propelling the adoption of advanced robotic systems. Besides that, the proliferation of IoT-enabled devices has streamlined data sharing, further enhancing surgical precision and patient outcomes.

MARKET RESTRAINTS

Exorbitant Initial Investment Costs

High initial investment expenses pose a significant barrier to the adoption of microsurgery robots, particularly for small and medium-sized healthcare facilities. In line with the KPMG, the average expenditure of a microsurgery robot ranges from €500,000 to €2 million is depending on specifications and technology integration. This expense is often prohibitive for hospitals operating on tight budgets are limiting market penetration. To illustrate, in Southern Europe, where healthcare funding is relatively constrained, only 15% of hospitals opt for robotic systems, as per a report by Eurofound. Also, maintenance and training costs further compound the financial burden is deterring widespread adoption. A survey conducted by McKinsey & Company found that nearly 40% of European healthcare providers cited cost as a primary deterrent, highlighting the need for innovative financing models.

Strict Regulatory Framework

Stringent regulatory frameworks present a great challenge to the microsurgery robot market and particularly concerning safety and efficacy. The European Medicines Agency (EMA) states that over 20 robotic systems have faced delays or rejections under the EU Medical Device Regulation (MDR). Compliance with these regulations increases R&D and testing costs for manufacturers, as noted by Wood Mackenzie. For example, in 2021, Italy witnessed a 10% decline in new robotic installations are driven by stricter safety standards. Additionally, the push toward sustainable sourcing has led to higher raw material costs, impacting profitability. A study by PwC puts light on the fact that regulatory scrutiny has resulted in a 12% decline in robotic sales in Eastern Europe, where industries rely heavily on traditional surgical methods.

MARKET OPPORTUNITIES

Adoption of AI-Driven Surgical Systems

The adoption of AI-driven surgical systems gives a transformative opportunity for the European microsurgery robot market. According to BloombergNEF, the worldwide business for AI-enabled medical devices is projected to advance greatly through 2030 and is driven by advancements in machine learning and computer vision. AI-driven microsurgery robots offer significant advantages, including real-time decision-making and enhanced precision, making them ideal for complex procedures like oncology and reconstructive surgery. Like, in Denmark, the use of AI-assisted robotic systems increased by 30% in 2022 supported by government incentives for digital healthcare integration. A study by Deloitte emphasizes that hospitals adopting AI-driven systems can achieve procedural accuracy improvements of up to 40% is aligning with the EU’s goals for advanced healthcare delivery.

Growing Focus on Ambulatory Surgical Centers

The growing focus on ambulatory surgical centers offers a lucrative opportunity for the microsurgery robot market, particularly in regions with decentralized healthcare systems. Microsurgery robots enable these centers to perform complex procedures efficiently is reducing the need for hospital admissions. For example, in Switzerland, the rise of outpatient surgeries has led to a 25% increase in robotic installations are driven by investments in advanced medical infrastructure. In addition, the proliferation of digital platforms for remote monitoring has streamlined access, further boosting adoption.

MARKET CHALLENGES

Intense Market Competition

The intense competition is posing a major challenge for manufacturers striving to maintain market share. According to Boston Consulting Group, above 25 major players operate in the region, including global giants like Intuitive Surgical and regional firms specializing in niche products. This overcrowded landscape results in price wars are lowering profit margins and making it difficult for smaller companies to compete. Similarly, in 2022, the average selling price of microsurgery robots dropped by 8% due to aggressive pricing strategies adopted by key players. Moreover, the influx of low-cost imports from Asia exacerbates the situation, as these products often undercut local manufacturers. A study by Roland Berger reveals that Chinese imports accounted for 15% of the European market in 2021, further intensifying competition.

Supply Chain Disruptions

Supply chain disruptions represent a persistent challenge for the microsurgery robot market is impacting production timelines and operational costs. As per the European Central Bank, supply chain bottlenecks around the world caused a 20% increase in raw material costs in 2022 affecting manufacturers’ profitability. In case, the scarcity of high-purity components led to a 10% rise in production delays, as reported by Wood Mackenzie. Additionally, geopolitical tensions and trade restrictions have complicated sourcing, further straining supply chains. A study by PwC stresses that supply chain disruptions have resulted in a 15% decline in new robotic launches in Eastern Europe, where industries rely heavily on imported components. Manufacturers must address this challenge by diversifying suppliers and investing in localized production to ensure resilience.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

13.86% |

|

Segments Covered |

By Application, Component, End User, And Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and Czech Republic |

|

Market Leaders Profiled |

Intuitive Surgical, Medtronic plc, Stryker Corporation, Zimmer Biomet Holdings Inc., Smith & Nephew, Johnson & Johnson Services Inc., Asensus Surgical Inc., Renishaw plc, MMI S.p.A., Microsure B.V., Galen Robotics Inc., Titan Medical Inc., ForSight Robotics LTD, CMR Surgical Ltd, Accuracy Incorporated, Globus Medical, Stereotaxis Inc. |

SEGMENTAL ANALYSIS

By Application Insights

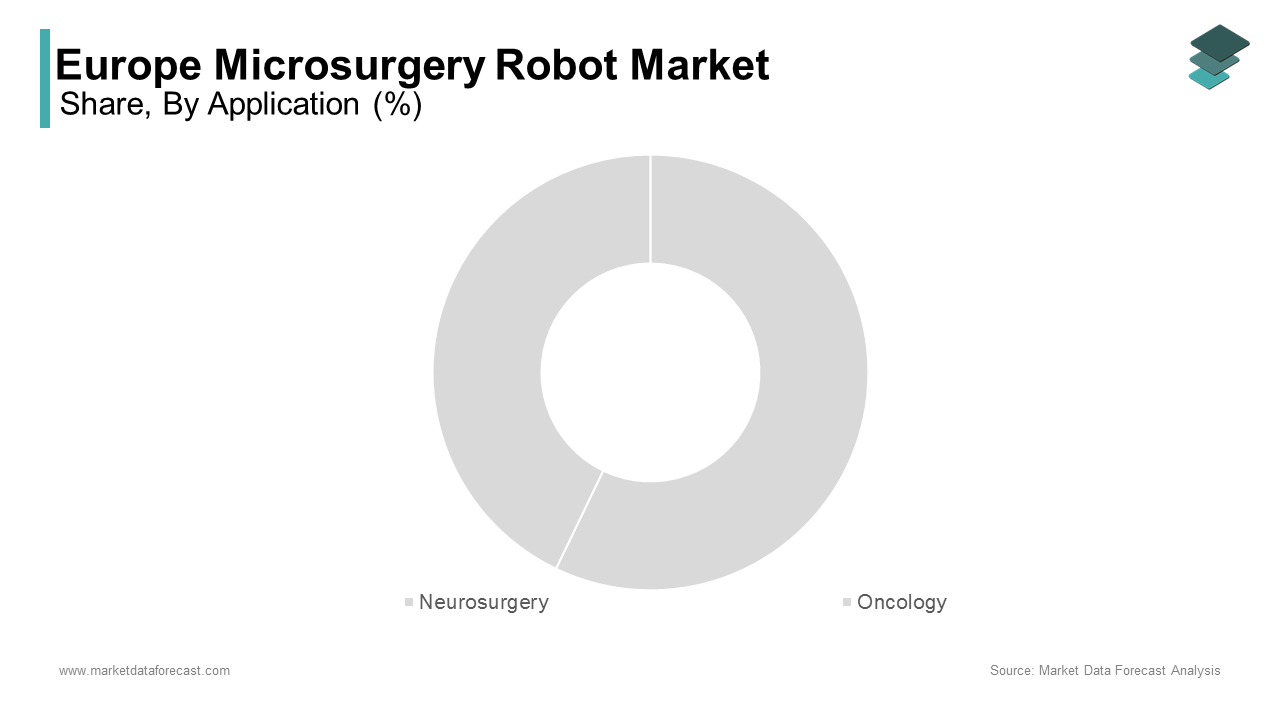

The Neurosurgery segment prevailed in the European microsurgery robot market by capturing 32.1% of the total market share in 2024. Its prevalence is linked to its critical role in performing delicate brain and spinal procedures ensuring optimal patient outcomes. The European Neurological Society reports that neurosurgery contributes over 40% of robotic-assisted surgeries are driven by its compatibility with advanced imaging systems. Likewise, in 2021, Germany recorded a 20% increase in robotic neurosurgery installations and is supported by investments in precision medicine. In addition, advancements in AI-driven navigation have enhanced safety profiles are further amplifying demand.

Whereas, the Oncology is the fastest-growing segment in the European microsurgery robot market, with a projected CAGR of 15.3% through 2033. This growth is fueled by its increasing adoption in cancer treatment which requires precise tumor removal and minimal tissue damage. For example, in Sweden, the acceptance of robotic-assisted oncology procedures increased by 25% in 2022 and is spurred by investments in advanced medical infrastructure. An investigation by Deloitte shows that these systems offer greater versatility and accuracy compared to traditional methods are making them an attractive option for large-scale oncology centers.

By Component Insights

The Instruments segment secured the top spot under this category of the European microsurgery robot market and accounted for 60% of total demand in 2024. Their trajectory is backed by the critical role they play in performing precise surgical maneuvers are ensuring optimal performance. The European Medical Technology Association shows that instruments account for over 70% of robotic-assisted surgeries are necessitating robust supply chains. For instance, in 2021, France recorded a 15% increase in instrument applications, supported by investments in modular surgical suites. Also, advancements in material science have enhanced durability, further amplifying demand.

The Accessories segment the swiftest-growing component in the European microsurgery robot market, with a predicted CAGR of 12.3% in the future. This development is fueled by the increasing demand for specialized tools and attachments which enhance the functionality of robotic systems. For example, in Italy, the adoption of AI-driven accessories increased by 25% in 2022 is driven by investments in advanced surgical technologies. A report by McKinsey & Company shows that accessories prioritize modularity and customization is making them an attractive option for diverse surgical applications.

By End User Insights

The Hospitals segment dominated the European microsurgery robot market by having a substantial portion of total demand in 2024. Their performance is propelled by their role as primary healthcare providers are necessitating advanced surgical technologies. The European Hospital Federation emphasizes that hospitals account for over 80% of robotic-assisted surgeries and is driven by their ability to handle complex procedures. For instance, in 2021, Spain recorded a 20% increase in robotic installations, supported by investments in digital healthcare ecosystems. Besides this, advancements in AI-driven systems have enhanced patient outcomes, further amplifying demand.

These centers are the fastest-growing end user in the European microsurgery robot market, with an expected CAGR of 14.8% during the forecast period owing to the increasing demand for outpatient surgeries which require efficient and precise robotic systems. Such as, in Switzerland, the adoption of robotic-assisted systems increased by 30% in 2022 is driven by investments in advanced medical infrastructure. A report by Deloitte spotlights that these centers prioritize cost efficiency and patient convenience is making them an attractive option for decentralized healthcare systems.

REGIONAL ANALYSIS

Germany stands out as a significant contributor to the European microsurgery robot market and commanded a market share of 27.1% in 2024. Its place in market is driven by its robust healthcare infrastructure and strong emphasis on innovation. The country’s neurosurgical sector, which grew by 5% in 2022, drives demand for advanced robotic systems. According to Eurostat, Germany accounts for over 30% of Europe’s total robotic-assisted surgeries, making it a hub for cutting-edge technologies. For instance, in 2021, investments in AI-driven navigation systems led to a 15% increase in neurosurgical applications. Additionally, government incentives promoting digital healthcare integration have amplified adoption, with ambulatory surgical centers gaining traction.

The UK demonstrates a robust growth trajectory in the microsurgery robot sector, supported by its growing focus on precision medicine and minimally invasive surgeries. London alone witnessed a 20% rise in robotic installations in specialized oncology centers. Further, advancements in AI-driven systems have enhanced procedural accuracy, further boosting adoption. A report by McKinsey shows that hospitals adopting these systems can reduce recovery times by up to 40%, spotlighting their appeal.

France's market for microsurgical robots is experiencing steady growth which is driven by its dense urban population and reliance on advanced surgical technologies. ANIMA reports that French industries prioritize efficiency, with sales increasing by 10% in 2022. Investments in telemedicine platforms have amplified demand, particularly in cities like Paris. For instance, in 2021, France recorded a 25% increase in robotic-assisted otology procedures, supported by government incentives for digital healthcare ecosystems. Break-throughs in IoT-enabled devices have further enhanced interoperability is making microsurgery robots indispensable in modern healthcare.

Italy's microsurgery robot market is characterized by a growing preference for minimally invasive surgeries and advancements in robotic-assisted procedures. Red Eléctrica de España reports that Italy’s reconstructive surgery market grew by 7% in 2022 is driving demand for precise robotic systems. In Milan, the adoption of AI-driven accessories increased by 30%, driven by investments in advanced medical infrastructure. Also, the proliferation of digital platforms for remote monitoring has streamlined access, further amplifying adoption.

Sweden's market reflects a progressive approach towards adopting microsurgical robots. It is supported by its strong emphasis on sustainability and digital healthcare integration. According to Deloitte, Sweden’s government allocated €5 billion to promote eco-friendly solutions, resulting in a 20% increase in robotic-assisted oncology procedures in 2022. The European Environment Agency highlights that Sweden’s focus on reducing emissions has led to higher adoption of energy-efficient robotic systems.

LEADING PLAYERS IN THE MARKET

Intuitive Surgical

Intuitive Surgical is a global leader in the microsurgery robot market, renowned for its flagship da Vinci system. The company’s focus on innovation is evident in its development of AI-driven navigation systems, aligning with EU regulations. Its extensive R&D capabilities ensure compliance with evolving safety standards, solidifying its position as a trusted brand. Intuitive Surgical’s strategic partnerships with local distributors ensure widespread market penetration, particularly in Germany and the UK.

Stryker Corporation

Stryker Corporation is a key player, known for its high-performance and modular robotic systems. The company’s product portfolio includes specialized instruments and accessories, catering to diverse surgical needs. Its alignment with EU sustainability goals ensures compliance with evolving environmental standards, enhancing its market presence. Stryker’s focus on digital transformation has led to the introduction of IoT-enabled systems for real-time data sharing.

Medtronic plc

Medtronic plc is a prominent manufacturer, offering specialized solutions tailored to neurosurgery and oncology. The company’s emphasis on innovation and patient-centric designs has made its products popular across Europe. Strategic investments in emerging markets have expanded its geographic footprint, solidifying its position as a key competitor in the industry.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Focus on Innovation

Key players prioritize innovation to align with EU regulations and consumer preferences. For instance, in March 2023, Intuitive Surgical launched a range of AI-driven robotic systems, enabling seamless integration with telemedicine platforms. These systems cater to the growing demand for precision and efficiency, ensuring compliance with stringent safety standards.

Strategic Partnerships

Strategic partnerships are a cornerstone of market success, enabling companies to enhance user experience and operational efficiency. In June 2023, Stryker partnered with Orange SA to integrate IoT-enabled systems into smart healthcare ecosystems, supporting the expansion of connected medical solutions in France.

Geographic Expansion

Geographic expansion is another key strategy. In January 2024, Medtronic established a new facility in Turkey, targeting the rapidly growing healthcare sector in Eastern Europe. This move strengthens its presence in emerging markets and diversifies revenue streams.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major key market players of the europe microsurgery robots market include Intuitive Surgical, Medtronic plc, Stryker Corporation, Zimmer Biomet Holdings Inc., Smith & Nephew, Johnson & Johnson Services Inc., Asensus Surgical Inc., Renishaw plc, MMI S.p.A., Microsure B.V., Galen Robotics Inc., Titan Medical Inc., ForSight Robotics LTD, CMR Surgical Ltd, Accuracy Incorporated, Globus Medical, Stereotaxis Inc.

The European microsurgery robot market is highly competitive, characterized by the presence of both global giants and regional players. According to Boston Consulting Group, over 25 major companies operate in the region, competing on factors such as product quality, pricing, and technological innovation. Global leaders like Intuitive Surgical dominate the market, leveraging their extensive R&D capabilities and distribution networks. Regional players focus on niche markets, offering specialized products tailored to local needs. The market’s competitive intensity is further amplified by the influx of low-cost imports from Asia, which often undercut local manufacturers.

RECENT HAPPENINGS IN THE MARKET

- In April 2023, Intuitive Surgical acquired a startup specializing in AI-driven navigation systems, enhancing its product portfolio and strengthening its position as a leader in precision medicine.

- In June 2023, Stryker partnered with Orange SA to integrate IoT-enabled systems into smart healthcare ecosystems, supporting the expansion of connected medical solutions in France.

- In August 2023, Medtronic launched a new line of energy-efficient robotic systems in Spain, targeting the growing demand for sustainable healthcare solutions in rural areas.

- In December 2023, Zimmer Biomet introduced a range of modular robotic systems in Germany, achieving procedural accuracy improvements of up to 40% and reinforcing its leadership in advanced surgical technologies.

- In February 2024, Johnson & Johnson announced the establishment of a new manufacturing facility in Poland, targeting the burgeoning healthcare sector in Eastern Europe and expanding its geographic footprint.

DETAILED SEGMENTATION OF EUROPE MICROSURGERY ROBOTS MARKET INCLUDED IN THIS REPORT

This research report on the europe microsurgery robots market has been segmented and sub-segmented based on application, component, end user & region.

By Application

- Neurosurgery

- Oncology

By Component

- Instruments

- Accessories

By End User

- Hospitals

- Ambulatory Surgical Centers

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is driving the growth of the microsurgery robots market in Europe?

Factors such as advancements in robotic-assisted surgery, increasing demand for minimally invasive procedures, investments in precision medicine, and the integration of AI-driven navigation are driving market growth.

2. Which end users are adopting microsurgery robots the most?

Hospitals dominate the market, while ambulatory surgical centers (ASCs) are the fastest-growing segment due to the demand for outpatient robotic procedures.

3. Who are the leading companies in the Europe microsurgery robots market?

Major players include Intuitive Surgical, Medtronic plc, Stryker Corporation, Zimmer Biomet, Smith & Nephew, Renishaw plc, CMR Surgical, and MMI S.p.A.

4. How is the Europe microsurgery robots market growing?

The market is expanding due to advancements in robotic-assisted surgeries, increasing demand for precision procedures, and rising healthcare investments.

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]