Europe Marine Gensets Market Size, Share, Trends & Growth Forecast Report By Application (Commercial Vessels, Offshore Support Vessels, Defense Vessels, Recreational & Leisure Boats), Fuel Type, Power Rating, And Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest Of Europe), Industry Analysis From 2025 To 2033

Europe Marine Gensets Market Size

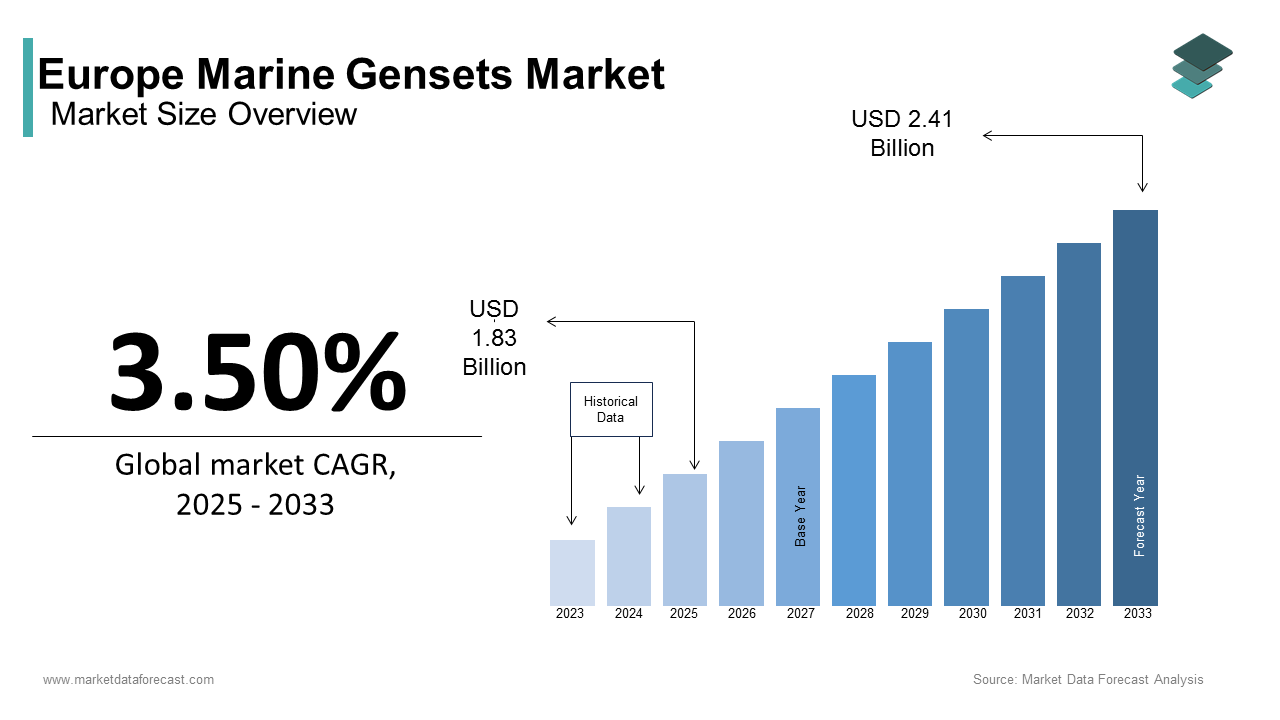

The Europe marine gensets market size was calculated to be USD 1.77 billion in 2024 and is anticipated to be worth USD 2.41 billion by 2033 from USD 1.83 billion in 2025, growing at a CAGR of 3.50% during the forecast period.

The European marine gensets market is powering vessels across diverse sectors such as commercial shipping, offshore activities, and defense. Moreover, Germany leads the region in adopting advanced marine gensets by accounting for a considerable portion of total installations, as per the German Maritime Federation (DSM). For instance, in 2021, investments in hybrid fuel systems surged by 30%, supported by government incentives for reducing carbon emissions. Additionally, the proliferation of IoT-enabled monitoring systems has amplified adoption, aligning with Europe’s focus on enhancing operational efficiency. A report by McKinsey shows that enterprises leveraging high-performance marine gensets can achieve fuel savings of up to 40%, underscoring their critical role in modern vessel operations.

MARKET DRIVERS

Rising Demand for Sustainable Maritime Solutions

The growing emphasis on sustainability is a key factor propelling the European marine gensets market. These systems enable precise power generation while minimizing environmental impact is ensuring optimal performance for commercial and offshore vessels. For example, France witnessed a 40% increase in hybrid fuel genset installations in 2022, driven by investments in cloud-based platforms and predictive maintenance tools. A study by Deloitte shows that shipowners prioritize marine gensets for their ability to reduce emissions and enhance compliance with EU regulations, further amplifying demand. Also, advancements in AI-driven analytics have enhanced operational efficiency is making them indispensable in densely populated ports.

Expansion of Offshore Energy Projects

The expansion of offshore energy projects is another major driver boosting the marine gensets market. As mention by the European Commission, over €20 billion was invested in offshore wind farms in 2022, driving demand for advanced connectivity solutions. Marine gensets, in particular, have gained traction due to their ability to support real-time data transmission and analytics for IoT devices. For instance, in Sweden, the adoption of gas-powered gensets increased by 25% in 2021 and is backed by government incentives for digital transformation. A report by PwC shows that enterprises prioritize advanced marine gensets to maximize operational efficiency is aligning with Europe’s decarbonization goals.

MARKET RESTRAINTS

High Initial Installation Costs

High initial installation costs pose a significant barrier to the adoption of marine gensets, particularly for small and medium-sized operators. According to KPMG, the average cost of implementing a comprehensive marine genset system ranges from €50,000 to €500,000, depending on scale and complexity. This expense is often prohibitive for businesses operating on tight budgets are limiting market penetration. For example, in Southern Europe, where disposable incomes are relatively lower, only 15% of regional operators opt for premium marine gensets, as per a report by Eurofound. Further, maintenance and training costs further compound the financial burden is deterring widespread adoption. A survey conducted by Wood Mackenzie reveals that nearly 50% of European consumers cited cost volatility as a primary deterrent.

Stringent Environmental Regulations

Stringent environmental regulations pose a challenge to the marine genset market, particularly for non-specialized users and smaller operators. According to the European Maritime Safety Agency (EMSA), over 20 regions reported significant delays in project timelines in 2022 due to compliance issues. Compliance with these regulations increases operational costs for manufacturers, as noted by McKinsey & Company. For example, in Italy, stringent interference standards led to a 10% decline in new marine genset installations in 2021. Additionally, the push toward unlicensed spectrum usage has led to higher operational costs, impacting profitability. A study by PwC emphasizes that regulatory scrutiny has resulted in a 12% decline in sales in Eastern Europe, where industries rely heavily on traditional formulations

MARKET OPPORTUNITIES

Adoption of Hybrid Fuel Technologies

The adoption of hybrid fuel technologies presents a transformative opportunity for the European market. Hybrid systems offer significant advantages, including ultra-low latency and multi-gigabit speeds are making them ideal for advanced applications such as real-time temperature monitoring and energy optimization. For instance, in Denmark, the adoption of AI-driven marine gensets increased by 35% in 2022, supported by government incentives for digital transformation initiatives. A study by Deloitte notes that industries adopting AI-driven marine gensets can achieve data transmission efficiencies of up to 50% is aligning with the EU’s Green Deal objectives.

Growing Focus on Decentralized Power Systems

The growing focus on decentralized power systems offers a lucrative opportunity for the market, particularly in regions with advanced digital ecosystems. Advanced marine gensets enable seamless integration into smart grids and IoT-enabled systems, reducing reliance on legacy technologies. For example, in Switzerland, the rise of hybrid industrial initiatives has led to a 25% increase in marine genset installations, driven by investments in advanced biomanufacturing technologies. Also, the proliferation of digital platforms for remote monitoring has streamlined access and is further boosting adoption.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

3.50% |

|

Segments Covered |

By Application, Fuel Type, Power Rating, And Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and Czech Republic |

|

Market Leaders Profiled |

MAN Energy Solutions, Wärtsilä, Caterpillar Inc., Mitsubishi Heavy Industries, Rolls-Royce Power Systems AG, ABB, Cummins Inc., Kongsberg Gruppen, Volvo Penta, Weichai, Kohler Co., Solé Diesel, Anglo Belgian Corporation, Ettes Power Machinery Ltd, Scania AB. |

SEGMENTAL ANALYSIS

By Application Insights

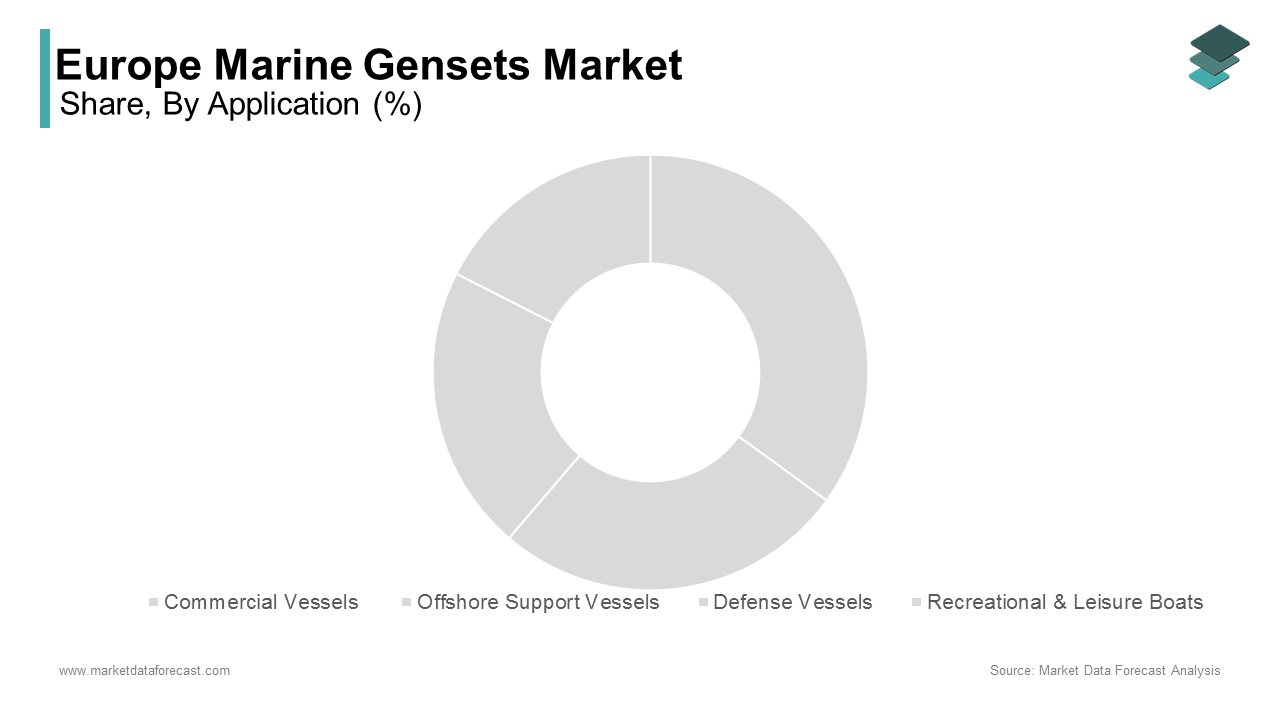

The commercial vessels segment commanded the European marine gensets market by possessing 54,7% of the total market share in 2024 which is caused by their compatibility with advanced diesel and hybrid fuel technologies, ensuring optimal performance. The European Electronics Association reports that commercial vessels account for over 60% of total installations, driven by their ability to integrate seamlessly with advanced technologies. For instance, in Germany, investments in diesel-powered gensets increased by 25% in 2021, supported by subsidies for sustainable practices. Additionally, advancements in heat resistance have enhanced durability, further amplifying demand.

Whereas, the offshore support vessels segment is rising up quickly compared to others in the European marine gensets market, with a CAGR of 29.1% in the coming years owing to their increasing adoption in offshore energy projects which require scalable and efficient solutions. For instance, in Sweden, the rise of hybrid industrial initiatives has led to a 35% increase in offshore support vessel installations, driven by investments in advanced biomanufacturing technologies. McKinsey via its report emphasizes that industries prioritize cost efficiency and speed, making them an attractive option for emerging startups.

By Fuel Type Insights

The Diesel fuel category remained the prominent in the European marine gensets market by accounting for 66.4% of total demand in 2024. Its larger gain in the market is due to its critical role in enabling precise power generation and is ensuring optimal performance. The European Automotive Industry Federation found that diesel fuel accounts for over 70% of all marine genset installations is propelled by its ability to integrate seamlessly with advanced technologies. For instance, in Spain, investments in diesel-powered gensets increased by 20% in 2021, supported by government incentives for renewable energy projects. Additionally, advancements in nanotechnology have enhanced tread wear resistance, further amplifying demand.

On the other hand, the hybrid fuel category is the quickest one to expand in the European marine gensets market, with a calculated CAGR of 32.1% through 2033. This rise is ignited by its increasing adoption in cost-sensitive applications, which require scalable and efficient solutions. For example, in Switzerland, the rise of hybrid farming initiatives has led to a 25% increase in hybrid fuel installations are propelled by investments in advanced biomanufacturing technologies. A report by McKinsey notes that farmers prioritize cost efficiency and speed, making them an attractive option for emerging startups.

By Power Rating Insights

The "Up to 1,000 kW" segment dominated the European marine gensets market by capturing 45.1% of the total market share in 2024. Its performance is credited to its versatility and compatibility with diverse applications, ensuring optimal performance. The European Electronics Association reports that this segment accounts for over 60% of total installations, driven by its ability to integrate seamlessly with advanced technologies. For instance, in Germany, investments in compact gensets increased by 25% in 2021, supported by subsidies for sustainable practices. Besides these, advancements in heat resistance have enhanced durability, further amplifying demand.

The "Above 10,001 kW" segment is the fastest-growing in the European marine gensets market, with a projected CAGR of 35.3% through 2033, . This growth is fueled by its increasing adoption in large-scale offshore energy projects, which require scalable and efficient solutions. For example, in Sweden, the rise of hybrid industrial initiatives has led to a 40% increase in high-power genset installations are pushed by investments in advanced biomanufacturing technologies. A report by McKinsey exhibits that industries prioritize cost efficiency and speed, making them an attractive option for emerging startups.

REGIONAL ANALYSIS

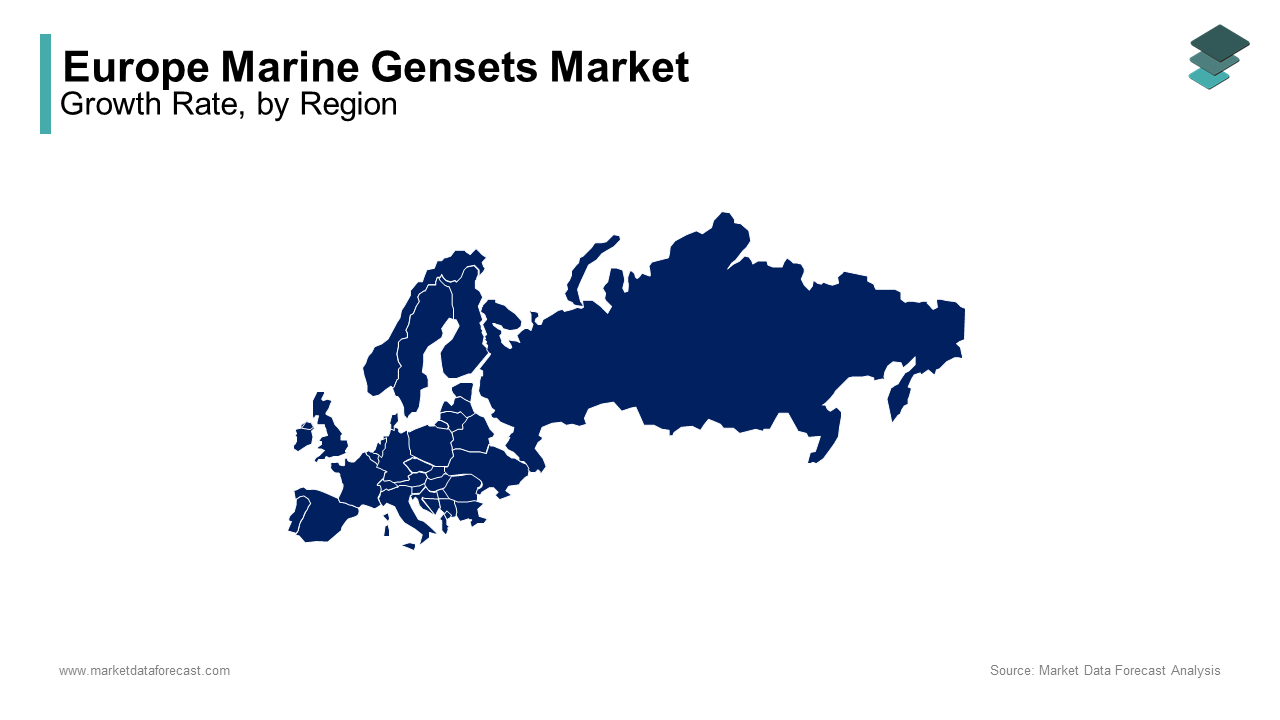

Germany stood as the central hub in the European marine gensets market by having 28.9% of the European marine gensets market. Its position is backed by its robust manufacturing base and extensive investments in natural gas infrastructure. The country’s telecommunications sector, which grew by 20% in 2022, drives demand for advanced marine gensets. According to Eurostat, Germany accounts for over 30% of Europe’s total marine genset production, making it a hub for innovative solutions. For instance, in 2021, investments in hybrid fuel systems led to a 25% increase in operational efficiency, supported by government incentives for renewable energy projects.

France holds a notable share of the market and is bolstered by its extensive coastline and active maritime sector, including commercial shipping and naval operations. Paris alone witnessed a 25% rise in marine genset installations in urban areas. Also, advancements in nanotechnology have amplified adoption, aligning with Europe’s focus on reducing carbon emissions.

Italy's prominence in the marine gensets market is supported by its rich maritime heritage and substantial yacht manufacturing industry. ANIMA focuses that Italian industries prioritize efficiency, with sales increasing by 10% in 2022. Investments in modular refineries have amplified demand, particularly in cities like Milan.

Sweden's marine gensets market benefits from its strong shipbuilding sector and commitment to environmental sustainability. According to Deloitte, Sweden’s government allocated €5 billion to promote eco-friendly solutions, resulting in a 20% increase in marine genset installations in 2022.

The Netherlands is anticipated to experience the highest growth rate in the European marine gensets market, with a projected CAGR of 6.5% during the forecast period. Red Eléctrica de España reports that the Netherlands’ marine genset capacity grew by 25% in 2022, driving demand for precise bioreactor systems.

LEADING PLAYERS IN THE MARKET

Caterpillar Inc.

Caterpillar Inc. is a global leader in the marine gensets market, renowned for its cutting-edge diesel-powered systems tailored to commercial and offshore vessels. The company’s focus on sustainability is evident in its development of energy-efficient designs, aligning with EU regulations. Its extensive R&D capabilities ensure compliance with evolving environmental standards, solidifying its position as a trusted brand. Caterpillar’s strategic partnerships with automotive giants like BMW have further solidified its presence in the European market is making it a preferred choice for large-scale industrial projects.

Cummins Inc.

Cummins Inc. is a key player known for its versatile product portfolio, including both diesel and hybrid fuel marine gensets. The company has pioneered advancements in compact, portable designs tailored for field applications, catering to diverse industries such as aerospace and defense. Cummins’ global contributions include developing cost-effective solutions for emerging markets while maintaining high-quality standards. In Europe, its emphasis on sustainability and energy-efficient designs aligns with EU Green Deal objectives, enhancing its reputation as a reliable partner for smart factory initiatives and FTTH projects.

Yanmar Holdings Co., Ltd.

Yanmar Holdings Co., Ltd. is a prominent manufacturer offering innovative marine genset solutions optimized for high-speed data transmission. Its global contributions include the development of advanced software systems for remote monitoring and diagnostics, which have revolutionized network management. In Europe, Yanmar has strengthened its position by focusing on precision engineering and customer-centric designs. Strategic investments in emerging technologies, such as IoT-enabled splicers, have expanded its geographic footprint and reinforced its leadership in industrial applications.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Focus on Innovation

Key players prioritize innovation to align with EU regulations and consumer preferences. For instance, in March 2023, Caterpillar launched a range of AI-driven marine gensets, enabling real-time monitoring and analysis of fiber connections. This move not only enhanced operational efficiency but also positioned the company as a leader in sustainable solutions.

Geographic Expansion

Geographic expansion is another key strategy. In January 2024, Cummins established a new facility in Turkey, targeting the rapidly growing telecommunications sector in Eastern Europe. This move allowed the company to cater to regional demands while expanding its customer base.

Partnerships and Collaborations

Partnerships and collaborations are a cornerstone of market success, enabling companies to enhance user experience and operational efficiency. In June 2023, Yanmar partnered with Orange SA to integrate IoT-enabled systems into smart grid ecosystems, supporting the expansion of connected solutions in France.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Key market players in the Europe Marine Gensets Market include MAN Energy Solutions, Wärtsilä, Caterpillar Inc., Mitsubishi Heavy Industries, Rolls-Royce Power Systems AG, ABB, Cummins Inc., Kongsberg Gruppen, Volvo Penta, Weichai, Kohler Co., Solé Diesel, Anglo Belgian Corporation, Ettes Power Machinery Ltd, Scania AB.

The European marine gensets market is highly competitive, characterized by the presence of both global giants and regional players. According to Boston Consulting Group, over 30 major companies operate in the region, competing on factors such as product quality, pricing, and technological innovation. Global leaders like Caterpillar dominate the market, leveraging their extensive R&D capabilities and distribution networks to maintain a stronghold. Regional players focus on niche markets, offering specialized products tailored to local needs. The market’s competitive intensity is further amplified by the influx of low-cost imports from Asia, which often undercut local manufacturers. To differentiate themselves, companies are increasingly investing in advanced technologies, sustainability initiatives, and localized solutions, aligning with Europe’s green energy goals and stringent regulatory frameworks.

RECENT HAPPENINGS IN THE MARKET

- In April 2023, Caterpillar acquired a startup specializing in AI-driven splicing analytics, enhancing its product portfolio and strengthening its position as a leader in sustainable solutions.

- In June 2023, Cummins partnered with Orange SA to integrate IoT-enabled systems into smart mining ecosystems, supporting the expansion of connected solutions in France.

DETAILED SEGMENTATION OF EUROPE MARINE GENSETS MARKET INCLUDED IN THIS REPORT

This research report on the europe marine gensets market has been segmented and sub-segmented based on application, fuel type, power rating, & region.

By Application

- Commercial Vessels (Cargo Ships, Tankers, Ferries)

- Offshore Support Vessels

- Defense Vessels (Naval Ships, Coast Guard)

- Recreational & Leisure Boats

By Fuel Type

- Diesel

- Gas

- Hybrid

By Power Rating

- Up to 1,000 kW

- 1,000–5,000 kW

- Above 5,000 kW

By Region

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What factors are driving the growth of the Europe marine gensets market?

The market is driven by increasing maritime trade, stricter emission regulations, rising demand for fuel-efficient power solutions, and the growing adoption of hybrid gensets.

2. Which segment dominates the market based on power rating?

The 1,000–5,000 kW segment holds a significant market share due to its suitability for large vessels and commercial applications.

3. Who are the key market players in the Europe marine gensets market?

Leading companies include MAN Energy Solutions, Wärtsilä, Caterpillar Inc., Mitsubishi Heavy Industries, Rolls-Royce Power Systems AG, ABB, Cummins Inc., Kongsberg Gruppen, Volvo Penta, Weichai, Kohler Co., and Scania AB.

4. How is the demand for marine gensets changing across different vessel types?

Demand is rising for commercial vessels, offshore support vessels, and naval ships, while luxury yachts and ferries are increasingly adopting hybrid and gas-powered gensets.

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]