Europe Logistics Market Research Report – Segmented By Model (Third-party logistics (3PL) segment , Fourth-party logistics (4PL) segment ) Transportation ( road transport segment,rail transport segment ) End-Use Industry (healthcare segment)Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of EU) - Industry Analysis on Size, Share, Trends & Growth Forecast (2025 to 2033)

Europe Logistics Market Size

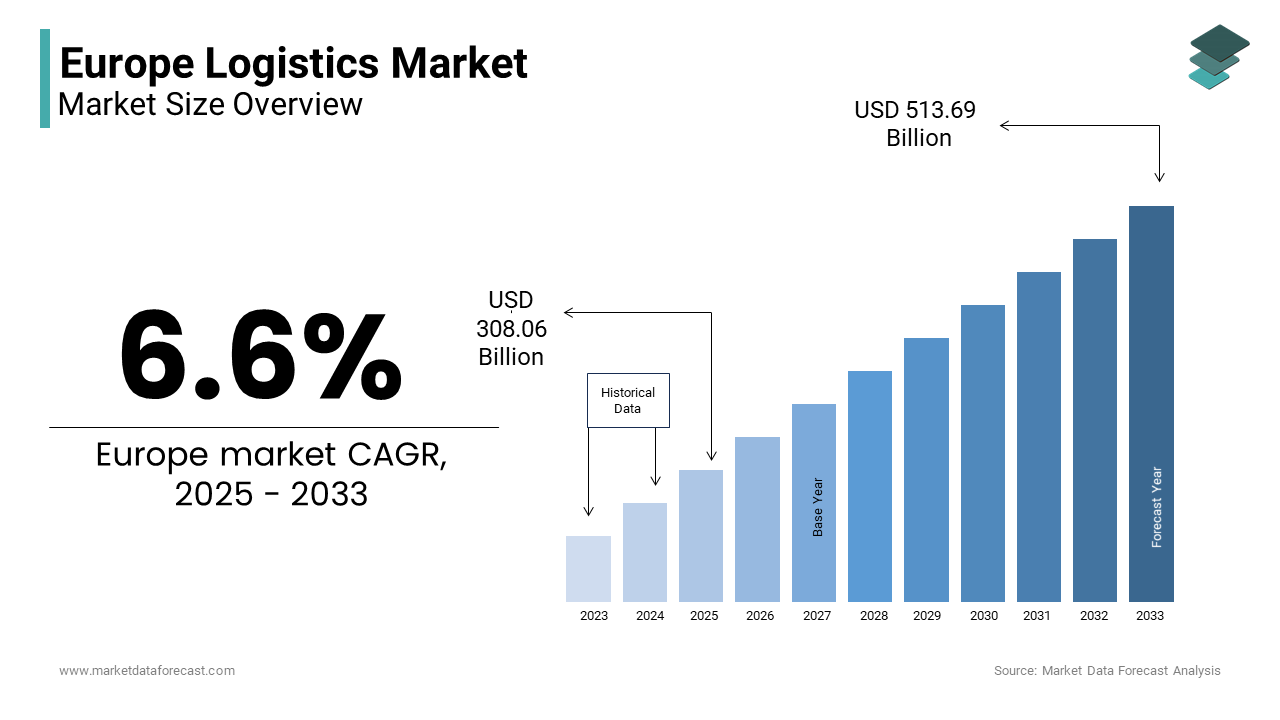

The Europe Logistics Market Size was valued at USD 288.99 billion in 2024. The Europe Logistics Market size is expected to have 6.6 % CAGR from 2025 to 2033 and be worth USD 513.69 billion by 2033 from USD 308.06 billion in 2025.

The Europe logistics market is experiencing robust growth, driven by the rapid expansion of e-commerce and cross-border trade. This expansion is fueled by increasing demand for efficient supply chain solutions and seamless transportation networks. A key factor shaping the market is the growing emphasis on digitalization and automation. As per Eurostat, over 60% of European companies now use AI-driven tools for inventory management and route optimization by ensuring compliance with consumer expectations. Additionally, stringent regulations are promoting sustainability have further propelled demand for eco-friendly logistics solutions by ensuring sustained growth across all sectors.

MARKET DRIVERS

Surge in E-Commerce Demand

The exponential rise in e-commerce activity is one of the most significant drivers propelling the Europe logistics market forward. According to Nielsen, online retail sales in Europe grew by 40% in 2022, creating a lucrative niche for third-party logistics (3PL) providers. For instance, in France, e-commerce fulfillment centers accounted for over 50% of all warehousing operations, as per the French Retail Federation. This trend is further amplified by the growing consumer preference for fast and reliable delivery services. According to the European Commission, same-day and next-day delivery options reduce cart abandonment rates by 30% by reflecting heightened consumer interest in seamless shopping experiences. Additionally, advancements in last-mile delivery technologies have addressed previous concerns about efficiency and cost.

Adoption of Automation and AI Technologies

Another critical driver is the widespread adoption of automation and artificial intelligence (AI) technologies, which fuels demand for advanced logistics solutions. According to a study by Deloitte, the integration of AI in logistics operations reduced operational costs by 25% in 2022, with markets like Germany and Spain leading the charge, as per the German Engineering Association.

The emphasis on efficiency and scalability has further amplified this trend. As per Eurostat, AI-driven systems improve warehouse productivity by 40% while reducing errors by aligning with market demands. Additionally, government incentives promoting Industry 4.0 initiatives have broadened their appeal by addressing previous concerns about implementation costs.

MARKET RESTRAINTS

High Costs of Digital Transformation

One of the primary restraints hindering the Europe logistics market is the high cost associated with digital transformation for small and medium-sized enterprises (SMEs). According to the European Chemicals Agency, implementing AI and IoT solutions increases operational expenses by 20% due to upfront investments in hardware and software. For instance, in Belgium, shortages of skilled IT professionals caused logistical challenges is leading to a 10% increase in training costs, as per the Belgian Logistics Federation. These fluctuations create uncertainty for SMEs by forcing them to delay or scale back digital initiatives. As per the European Central Bank, inflationary pressures have further exacerbated this issue by reducing profit margins and affecting long-term planning. This financial barrier poses a significant challenge for the broader adoption of advanced logistics technologies.

Stringent Environmental Regulations

Another significant restraint is the growing complexity of environmental regulations, which impacts operational efficiency and profitability. According to the European Commission, over 30% of logistics companies face restrictions due to emissions targets and carbon taxes. For example, in Sweden, bans on diesel-powered trucks led to a 15% decline in road freight volumes in 2022, as per the Swedish Environmental Protection Agency. This issue is exacerbated by growing consumer skepticism about green logistics claims. As per the World Health Organization, only 40% of consumers trust companies’ sustainability initiatives without third-party certifications is driving demand for transparent reporting. These challenges not only increase operational risks but also limit opportunities for innovation by posing a significant hurdle for market expansion.

MARKET OPPORTUNITIES

Expansion of Cross-Border Logistics Networks

The expansion of cross-border logistics networks presents a transformative opportunity for the Europe logistics market. According to a study by Bain & Company, over 60% of European businesses now prioritize international trade routes by creating a niche for brands offering seamless customs clearance and multi-modal transport solutions. For instance, in Germany, companies like DHL introduced specialized cross-border logistics services by boosting revenues by 30%, as per the German Logistics Association. A significant driver of this trend is the growing emphasis on global trade and supply chain resilience. As per Eurostat, cross-border logistics reduce transit times by 25% while improving reliability, aligning with market demands. Additionally, certifications like ISO standards have enhanced brand credibility by attracting premium buyers.

Growth of Green Logistics Solutions

Another promising opportunity lies in the rapid adoption of green logistics solutions, which cater to the growing demand for sustainable supply chains. The emphasis on carbon neutrality and energy efficiency has further amplified this trend. As per McKinsey & Company, green logistics reduce CO2 emissions by 40% while improving operational efficiency, creating a niche for innovative solutions. Additionally, government subsidies and tax incentives have broadened their appeal by addressing previous concerns about affordability.

MARKET CHALLENGES

Intense Competition and Price Wars

One of the most pressing challenges facing the Europe logistics market is the intense competition among established players and private labels, which complicates efforts to build brand loyalty. According to Kantar Worldpanel, private label logistics services account for over 25% of total sales in Europe, with major retailers offering affordable alternatives to branded solutions. For instance, in Italy, private labels captured 30% of the domestic freight market share in 2022, as per the Italian Retail Federation. This competition is further intensified by price wars, making it difficult for brands to differentiate themselves. As per Nielsen, over 60% of businesses switch between providers based on discounts and promotions, underscoring the challenge of retaining customer loyalty. Additionally, the lack of innovation in traditional categories limits opportunities for premiumization is posing a significant obstacle for market participants striving to stand out.

Fluctuating Fuel Prices

Another critical challenge is the volatility of fuel prices, which impacts transportation costs and pricing strategies. According to the International Energy Agency, the price of diesel fluctuated by up to 20% over the past year due to geopolitical tensions and supply chain disruptions. For example, in Germany, fuel surcharges caused logistical challenges is leading to a 10% increase in operational costs, as per the German Transport Federation. These fluctuations create uncertainty for logistics providers, forcing them to either absorb additional costs or pass them on to customers. As per the European Central Bank, inflationary pressures have further exacerbated this issue is reducing profit margins and affecting demand. These challenges not only strain profitability but also hinder long-term planning and investment in the market.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

6.6 % |

|

Segments Covered |

By Model, Transportation, End-Use Industry and Country. |

|

Various Analyses Covered |

Global, Regional, & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Country Covered |

UK, Germany, Italy, France, Spain, Sweden, Denmark, Poland, Switzerland, Netherlands, Rest of Europe. |

|

Market Leaders Profiled |

C.H. Robinson Worldwide Inc. (US), IJ.B. Hunt Transport Services (US), Ceva Holdings LLC (France), FedEx Corp (US) |

SEGMENT ANALYSIS

By Model Insights

The third-party logistics (3PL) segment dominated the Europe logistics market by capturing 50.3% of share in 2024 due to its ability to provide comprehensive supply chain solutions by appealing to businesses seeking cost-effective and scalable operations. For instance, in France, 3PL services accounted for over 60% of all e-commerce fulfillment activities, as per the French Logistics Federation. A key factor behind the segment’s dominance is the growing preference for outsourcing logistics functions. According to Eurostat, 3PL reduces operational costs by 30% while improving efficiency by ensuring compliance with consumer expectations. Additionally, advancements in digital platforms have addressed previous concerns about transparency and accountability.

The Fourth-party logistics (4PL) segment is projected to witness a CAGR of 8.4% from 2025 to 2033. This growth is fueled by its strategic focus on end-to-end supply chain management is appealing to large enterprises seeking holistic solutions. For example, in the UK, 4PL services gained immense popularity, with investments surging by 50% in 2022, as per the British Logistics Association. A significant driver of this segment’s rapid expansion is the growing emphasis on supply chain visibility and coordination. Additionally, advancements in blockchain technology have improved traceability is addressing previous concerns about data security.

By Transportation Insights

The road transport segment was the largest the Europe logistics market by holding a share of 60.4% in 2024. This growth is driven by its flexibility and extensive network coverage by appealing to businesses seeking door-to-door delivery solutions. For instance, in Spain, road freight accounted for over 70% of all domestic shipments, as per the Spanish Transport Federation. A key factor behind the segment’s dominance is the growing trend of just-in-time deliveries and urban logistics. The road transport reduces lead times while ensuring compliance with regulatory standards. Additionally, the availability of advanced tracking systems has broadened its appeal by enhancing customer satisfaction. These attributes ensure that road transport remains the primary driver of the market.

The rail transport segment is attributed in witnessing a projected CAGR of 7.4% from 2025 to 2033. This growth is fueled by its eco-friendly credentials and cost-effectiveness by appealing to environmentally conscious businesses. For example, in Germany, rail freight gained immense popularity, with investments surging by 40% in 2022, as per the German Environmental Federation. A significant driver of this segment’s rapid expansion is the growing emphasis on sustainability and energy efficiency. According to McKinsey & Company, rail transport reduces CO2 emissions by 60% compared to road freight by creating a niche for innovative solutions. Additionally, advancements in intermodal connectivity have improved usability is addressing previous concerns about flexibility.

By End-Use Industry Insights

The FMCG dominated the Europe logistics market by occupying 40.4% of share in 2024 owing to its high volume and frequency of shipments by appealing to logistics providers seeking stable revenue streams. For instance, in Italy, FMCG accounted for over 50% of all warehousing operations, as per the Italian Retail Federation. A key factor behind the segment’s dominance is the growing emphasis on timely replenishment and shelf availability. According to Eurostat, FMCG logistics reduce stockouts by 30% while improving supply chain efficiency by ensuring compliance with consumer expectations. Additionally, advancements in cold chain solutions have addressed previous concerns about perishable goods.

The healthcare segment is estimated to register a CAGR of 9.3% during the forecast period. This growth is fueled by the rising demand for temperature-controlled logistics and specialized handling by appealing to pharmaceutical companies. For example, in France, healthcare logistics gained immense popularity, with investments surging by 50% in 2022, as per the French Healthcare Federation. A significant driver of this segment’s rapid expansion is the growing emphasis on precision medicine and vaccine distribution. Additionally, advancements in IoT-enabled monitoring systems have improved reliability is addressing previous concerns about quality assurance. These innovations highlight the transformative potential of healthcare logistics to address evolving consumer preferences.

Country Level Analysis

Germany was the largest contributor in the Europe logistics market with a share of 25.5% in 2024. The country’s robust infrastructure and emphasis on technological innovation have positioned it as a leader in the region. For instance, iconic brands like DHL and DB Schenker are renowned globally for their comprehensive logistics solutions by catering to diverse industries such as automotive and e-commerce. A key factor driving Germany’s success is its proactive adoption of digitalization and automation. According to the German Engineering Association, over 60% of German logistics companies now use AI-driven tools for route optimization by reducing delivery times by 20%. Additionally, the rise of green logistics initiatives has enabled German brands to offer eco-friendly solutions.

France is more likely to witness a prominent CAGR of 7.8% during the forecast period in the Europe logistics market. The country’s strong emphasis on sustainability and innovation has prompted its position as a key player. For instance, French brands like Geodis dominate the e-commerce logistics segment by appealing to environmentally conscious consumers. A significant driver of France’s dominance is its focus on export-oriented growth and research. According to the French Transport Federation, over 50% of French logistics operations are dedicated to cross-border trade by reflecting its global appeal. Additionally, as per Deloitte, the integration of digital platforms has enhanced brand visibility by encouraging younger demographics to explore advanced solutions.

Top 3 Players in the market

Deutsche Post AG (DHL Group)

Deutsche Post AG, commonly known through its DHL brand, is one of the leading players in the global logistics market and has a significant presence in Europe. The company offers a wide range of services, including express parcel delivery, freight forwarding, supply chain management, and e-commerce solutions. Its extensive global network and advanced technological infrastructure allow it to provide seamless logistics services across various industries. Deutsche Post AG's contribution to the global market lies in its ability to integrate digital technologies into traditional logistics operations by enhancing efficiency and customer experience.

Kuehne + Nagel Management AG

Kuehne + Nagel is another major player in the European logistics market, renowned for its expertise in sea freight, air freight, road logistics, and contract logistics. The company has built a reputation for delivering tailored logistics solutions that cater to the specific needs of industries such as pharmaceuticals, automotive, and perishables. Kuehne + Nagel’s contribution to the global logistics market is marked by its commitment to digital transformation by leveraging platforms like its proprietary Seaexplorer tool to optimize shipping routes and reduce carbon emissions.

DSV A/S

DSV A/S has emerged as a powerhouse in the global logistics market through strategic acquisitions and organic growth with its position as a top-tier player in Europe. The company specializes in transport and logistics services, including air and sea freight, road transportation, and warehousing solutions. DSV’s contribution to the global logistics market is characterized by its ability to offer end-to-end supply chain solutions that are scalable and adaptable to diverse customer requirements. With a strong emphasis on operational excellence and integration of digital tools, DSV enhances visibility and control across supply chains.

Top strategies used by the key market participants

Strategic Acquisitions and Mergers

One of the most prominent strategies used by logistics companies is mergers and acquisitions (M&A). By acquiring smaller competitors or complementary businesses, companies can expand their geographic footprint, enhance service offerings, and achieve economies of scale. For instance, firms like DSV A/S have executed large-scale acquisitions to integrate new capabilities and enter untapped markets. Such moves not only consolidate their domiannce but also allow them to offer end-to-end solutions, from warehousing to freight forwarding, thereby increasing their value proposition for customers.

Digital Transformation and Technology Adoption

Investment in digital technologies is another critical strategy that has reshaped the competitive landscape. Leading players such as Deutsche Post AG (DHL Group) and Kuehne + Nagel focus on integrating advanced tools like artificial intelligence (AI), blockchain, Internet of Things (IoT), and data analytics into their operations. These technologies improve supply chain visibility, optimize routes, reduce costs, and enhance decision-making. Digital platforms also enable real-time tracking and predictive analytics, empowering customers with greater transparency and control over their shipments.

Sustainability Initiatives

As environmental concerns gain prominence globally, sustainability has become a cornerstone strategy for many logistics firms. Companies like Deutsche Post AG and SF Express Co. Ltd. are investing heavily in green logistics practices, including electric vehicles, alternative fuels, and carbon-neutral delivery options. They are also adopting eco-friendly packaging materials and optimizing warehouse energy consumption. These initiatives not only align with regulatory requirements but also resonate with environmentally conscious consumers and businesses.

Expansion of E-commerce and Last-Mile Delivery Services

With the rapid growth of e-commerce, logistics providers have been quick to adapt by enhancing their last-mile delivery capabilities. Firms like FedEx Corp. and CEVA Logistics SA focus on building robust networks to handle the surge in online shopping orders. This includes deploying automated sorting systems, expanding urban fulfillment centers, and leveraging crowd-sourced delivery models.

Customized Solutions and Industry-Specific Expertise

To stand out in a highly competitive market, many logistics companies emphasize providing tailored solutions based on specific industry needs. For example, Hellmann Worldwide Logistics SE & Co. KG and Kuehne + Nagel specialize in sectors like pharmaceuticals, automotive, and perishables, where precision and reliability are paramount.

Global Network Expansion and Partnerships

Expanding global networks through partnerships and alliances is another strategy used by key players to enhance their reach and service quality. Collaborations with local entities, governments, or other logistics providers help companies navigate regional challenges and access new markets. For instance, Bollore SE and Nippon Yusen Kabushiki Kaisha (NYK Line) often engage in joint ventures to tap into emerging opportunities in Africa or Asia. Such collaborations ensure that they remain agile and responsive to shifts in trade patterns and geopolitical dynamics.

Focus on Resilience and Risk Management

In light of disruptions caused by events like the COVID-19 pandemic and geopolitical tensions, strengthening supply chain resilience has become a priority. Companies like XPO Inc. and C.H. Robinson Worldwide Inc. invest in risk management frameworks, diversified supplier bases, and contingency planning.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a prominent role in the Europe Logistics Market are C.H. Robinson Worldwide Inc. (US), IJ.B. Hunt Transport Services (US), Ceva Holdings LLC (France), FedEx Corp (US), Expeditors International of Washington Inc. (US), XPO Logistics Inc. (US), United Parcel Service, Inc. (US), Deutsche Post (Germany), DHL Group (Germany), Americold Logistics (US)

The Europe logistics market is characterized by intense competition, with established brands and emerging startups vying for market share. According to McKinsey & Company, the market is fragmented, with no single entity holding more than 30% of the share by fostering a highly dynamic environment. Key players like DHL and Kuehne + Nagel dominate the premium segment, while private labels compete aggressively on affordability and accessibility.

Emerging startups, supported by venture capital funding, are disrupting traditional business models. For instance, brands like Bringg are pioneering last-mile delivery solutions by challenging incumbents in the e-commerce logistics segment. As per the European Commission, this competitive landscape drives innovation and ensures affordability for end-users. However, regulatory compliance and raw material volatility remain critical challenges for all participants is shaping the market’s evolution.

RECENT HAPPENINGS IN THE MARKET

- In April 2024, DHL acquired a German startup specializing in AI-powered route optimization software. This acquisition aimed to expand its portfolio of digital logistics solutions and cater to businesses seeking operational efficiency.

- In May 2024, Kuehne + Nagel partnered with a French e-commerce platform to launch exclusive fulfillment services targeting small and medium-sized enterprises. This initiative aimed to strengthen its position in the SME logistics space.

- In July 2024, DB Schenker introduced a line of green logistics services targeting environmentally conscious buyers. This move aimed to align with consumer values and boost brand loyalty.

- In September 2024, Bringg secured USD 150 million in funding from European investors to scale its last-mile delivery initiatives. This investment aimed to enhance transparency and accountability.

- In November 2024, DHL launched a campaign promoting its zero-carbon logistics initiative. This effort aimed to enhance brand credibility and appeal to eco-conscious businesses.

MARKET SEGMENTATION

This research report on the Europe Logistics Market has been segmented and sub-segmented into the following categories.

By Model

- Third-party logistics (3PL) segment

- Fourth-party logistics (4PL) segment

By Transportation

- road transport segment

- rail transport segment

By End-Use Industry

- healthcare segment

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe.

Frequently Asked Questions

What is the current size of the Europe logistics market?

The Europe logistics market is valued at several hundred billion euros and is growing steadily.

What are the key drivers of the Europe logistics market?

E-commerce growth, technological advancements, and demand for sustainable logistics solutions.

What are the major logistics modes used in Europe?

Road, rail, air, and maritime transportation play key roles.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]