Europe Industrial Boiler Market Size, Share, Trends, & Growth Forecast Report By Capacity (10 MMBTU/hr, 10 - 25 MMBTU/hr, 25 - 50 MMBTU/hr, 50 - 75 MMBTU/hr, 75 - 100 MMBTU/hr, 100 - 175 MMBTU/hr, 175 - 250 MMBTU/hr, and > 250 MMBTU/hr), Application, Technology, Fuel, Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2024 to 2033

Europe Industrial Boiler Market Size

The Europe industrial boiler market was worth USD 2.54 billion in 2024. The European market is expected to reach USD 3.48 billion by 2033 from USD 2.63 billion in 2025, growing at a CAGR of 3.56% from 2025 to 2033.

Industrial boilers are robust systems designed to generate steam or hot water by burning various fuels, including natural gas, coal, biomass, and oil, or utilizing renewable energy sources like solar thermal technology. These systems play an indispensable role in powering industrial processes, heating large facilities, and supporting district heating networks across Europe. The market is witnessing steady growth supported by the increasing demand for energy-efficient solutions, stringent environmental regulations and the transition toward cleaner energy alternatives.

The European industrial boiler market is projected to grow notably from 2025 to 2033. The rising industrialization in Eastern Europe and significant investments in retrofitting existing boiler systems to meet emission standards set by the European Union is fuelling this growth. Furthermore, according to the International Energy Agency, nearly 30% of industrial energy consumption in Europe relies on steam generation which is revealing the fundamental role of boilers in achieving sustainability goals. The European market is poised for transformative changes in the coming years because of the growing adoption of condensing boilers, combined heat and power (CHP) systems, and advancements in digital monitoring technologies.

MARKET DRIVERS

Stringent Regulatory Framework for Emission Reduction

The stringent regulatory framework aimed at curbing carbon emissions and promoting energy efficiency is mainly driving the growth rate of the European industrial boiler market. The European Union’s Green Deal which aspires to achieve climate neutrality by 2050 has compelled industries to adopt cleaner technologies including high-efficiency boilers. According to the European Environment Agency, industrial sectors contribute approximately 20% of the EU’s total greenhouse gas emissions and necessitates a transition to low-carbon solutions. This has spiked the adoption of biomass boilers and natural gas-fired systems that emit fewer pollutants compared to traditional coal-based boilers. The International Energy Agency states that upgrading old industrial boilers with modern as well as energy-efficient models can lower energy usage by up to 30%. Such compelling statistics have incentivized industries to align with EU directives are driving demand for advanced boiler technologies.

Rising Demand for District Heating Systems

The growing demand for district heating systems, particularly in Nordic and Eastern European countries is another key driver of this market. District heating networks rely heavily on industrial boilers to supply heat to residential, commercial, and industrial users. According to the European Commission, district heating accounts for about 12% of the EU’s total heating demand with countries like Denmark and Sweden deriving over 60% of their heating needs from such systems. Eurostat data reveals that investments in district heating infrastructure have increased by 15% annually since 2020 and is fueled by urbanization and the need for sustainable heating solutions. This trend has amplified the demand for large-scale industrial boilers capable of integrating renewable energy sources like solar thermal and geothermal which is ensuring reliable and eco-friendly heat supply across Europe.

MARKET RESTRAINTS

High Initial Investment Costs

The high initial investment required for advanced boiler systems is a key obstacle for the European industrial boiler market. Modern industrial boilers particularly those incorporating energy-efficient and low-emission technologies often come with significant upfront costs. The European Investment Bank notes that the installation of a high-efficiency condensing boiler or a biomass-based system can cost up to 50% more than traditional models. For small and medium-sized enterprises (SMEs) which form a substantial portion of Europe’s industrial base and these costs can be prohibitive. Additionally, as per the International Renewable Energy Agency, retrofitting existing boiler systems to comply with EU emission standards requires an average investment of €200,000 to €500,000 per facility. This financial burden discourages many industries from upgrading their infrastructure and thereby limiting the market's growth potential despite the availability of long-term energy savings.

Limited Availability of Skilled Workforce

The limited availability of skilled professionals capable of operating and maintaining advanced industrial boiler systems is restricting the growth of the European industrial boiler market. The technology is evolving and there is an increasing demand for technicians and engineers trained in digital monitoring, automation, and renewable energy integration. According to Eurostat, approximately 40% of European companies in the energy and manufacturing sectors report difficulties in finding qualified personnel to manage modern boiler systems. The European Centre for the Development of Vocational Training further states that only 30% of workers in the industrial sector have received training in advanced energy technologies. This skill gap not only delays the adoption of innovative boiler solutions but also increases operational risks because of improper maintenance which is ultimately hindering the market’s expansion and efficiency gains.

MARKET OPPORTUNITIES

Growing Adoption of Renewable Energy Integration

The integration of renewable energy sources such as biomass, solar thermal, and geothermal into boiler systems is a potential prospect for the market growth. The European Commission stresses that renewable energy accounted for 22% of the EU’s total energy consumption in 2022 with ambitious targets to increase this share to 42.5% by 2030. This change presents a lucrative opportunity for industrial boiler manufacturers to develop hybrid systems that combine conventional fuels with renewable energy. According to the International Energy Agency, industries implementing renewable-integrated boilers can lower their carbon footprint by up to 60% which is consistent with EU sustainability goals. Furthermore, the European Biomass Association reports that biomass boilers alone could achieve a 15% hike in industrial boiler installations by 2030 and is driven by government incentives and subsidies for green technologies.

Expansion of Retrofitting and Upgradation Projects

The increasing focus on retrofitting and upgrading existing boiler systems to enhance efficiency and comply with stringent emission standards is a further promising opportunity for the European industrial boiler market. The European Environment Agency states that nearly 70% of industrial boilers in Europe are over 20 years old and that makes them prime candidates for modernization. Retrofitting these systems with advanced technologies such as condensing boilers or digital monitoring tools can enhance energy efficiency by up to 40%, as per data from the European Investment Bank. Additionally, according to the Eurostat highlights, governments across Europe are allocating over €1 billion annually in grants and low-interest loans for industrial energy efficiency projects. This financial support coupled with the growing emphasis on sustainability creates a favourable environment for boiler manufacturers and service providers to capitalize on retrofitting initiatives which is driving market growth significantly.

MARKET CHALLENGES

Fluctuating Energy Prices and Fuel Supply Uncertainty

One of the major challenges facing the European industrial boiler market is

The volatility in energy prices and uncertainty in fuel supply is hampering the expansion of the European industrial boiler market. The European Commission revealed that natural gas being a primary fuel for industrial boilers has experienced price spikes of up to 200% in 2022 owing to geopolitical tensions and supply chain disruptions. This instability forces industries to reconsider their reliance on gas-fired boilers and particularly as the International Energy Agency (IEA) reports that over 50% of Europe’s industrial boilers depend on fossil fuels. Additionally, the European Environment Agency notes that coal and oil prices have also seen substantial fluctuations and that is further complicating fuel procurement decisions. Such unpredictability increases operational costs for industries and is making it challenging to plan long-term investments in boiler systems and hindering the adoption of advanced technologies.

Stringent Emission Standards and Compliance Costs

The increasing burden of complying with stringent emission standards set by the European Union is majorly affecting the European industrial boiler market growth. The EU Industrial Emissions Directive mandates industries to lower emissions of pollutants such as nitrogen oxides (NOx) and sulfur dioxide (SOx) which requires costly upgrades to existing boiler systems. According to Eurostat, adherence to these regulations can increase operational expenses by up to 25% for small and medium-sized enterprises (SMEs). Furthermore, the European Investment Bank states that retrofitting older boilers to meet these standards often requires investments exceeding €300,000 per facility and that many industries find financially burdensome. These measures are crucial for environmental sustainability but the high compliance costs and technical complexities pose significant barriers especially for smaller players in the industrial boiler market.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

3.56% |

|

Segments Covered |

By Capacity, Application, Technology, Fuel, and Country |

|

Various Analyses Covered |

Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and Rest of Europe |

|

Market Leaders Profiled |

Babcock & Wilcox, Bosch Industriekessel, Clayton Industries,Cochran, Doosan, FERROLI, Forbes Marshall, Fulton, Hoval, Hurst Boiler & Welding, IHI, John Cockerill, John Wood Group, Miura America, Mitsubishi Heavy Industries, Rentech Boilers, Thermax, and Viessmann. |

SEGMENTAL ANALYSIS

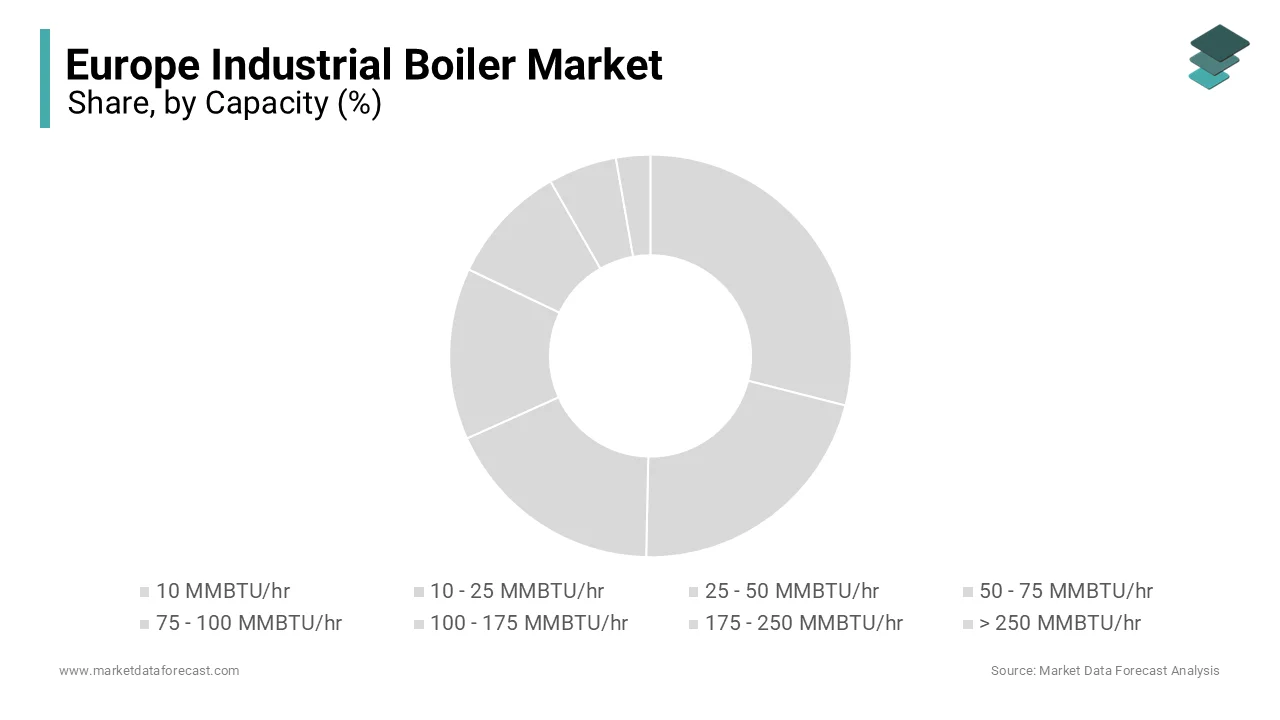

By Capacity Insights

The 10-25 MMBTU/hr capacity segment dominated the market by capturing 30.4% of the total market share in 2024. Its versatility and is catering to medium-sized industries like pharmaceuticals and textiles which form a significant portion of Europe’s industrial base is primarily driving the growth of this segment in the global market. As per the International Energy Agency, these boilers are increasingly being retrofitted with energy-efficient technologies and is increasing their adoption. Their importance lies in balancing cost-effectiveness with compliance to EU emission standards and that is making them indispensable for SMEs.

On the other hand, the >250 MMBTU/hr segment is predicted to witness the highest CAGR of 6.5% from 2025 to 2033. The rising demand for large-scale district heating systems and energy-intensive industries transitioning to renewable-integrated solutions is fuelling the market growth of the segment. The European Environment Agency notes that these boilers are critical for decarbonization, as they can incorporate carbon capture technologies. Their ability to support ultra-large operations like refineries and chemical plants underscores their importance in achieving Europe’s sustainability goals while meeting escalating energy demands.

By Application Insights

The chemical industry segment was the largest application segment in the European industrial boiler market and accounted for 20.4% of the total market share in 2024. The sector's heavy reliance on steam and heat for processes like polymerization and distillation is strengthening the position of this segment in the global market. According to the European Environment Agency, over 40% of the chemical industry’s energy consumption comes from thermal processes which is escalating demand for high-capacity boilers. Additionally, stringent EU emission regulations have pushed chemical manufacturers to adopt energy-efficient and renewable-integrated boilers and is making this segment critical for achieving Europe’s decarbonization goals while maintaining industrial productivity.

However, the district heating segment emerged as the fastest expanding application and is projected to grow at a CAGR of 7.2% during the forecast period. This rapid growth is influenced by urbanization and the expansion of centralized heating networks and particularly in Nordic countries like Denmark where district heating meets over 60% of heating needs, as stated by Eurostat. The International Energy Agency notes that modern boilers in district heating systems reduce energy losses by up to 30%, enhancing efficiency. This segment’s importance lies in its ability to integrate renewable energy sources, supporting Europe’s transition to sustainable energy solutions while addressing rising urban heating demands.

By Technology Insights

Non-condensing boilers dominated the European industrial boiler market and held 55.3% of the total market share in 2024. Their widespread use in energy-intensive industries like refineries and chemicals where high-temperature steam is essential is basically driving the segment forward. The European Investment Bank states that over 60% of existing industrial boilers in Europe are non-condensing systems and is reflecting their historical prevalence. These boilers remain critical for heavy-duty applications despite being less efficient. Their importance lies in their ability to meet high heat demands though retrofitting initiatives to enhance efficiency and comply with EU emission standards are driving gradual transitions to cleaner technologies.

The condensing boilers segment is predicted to witness the highest CAGR of 8.3% from 2025 to 2033. The increasing demand for energy-efficient solutions and stricter environmental regulations is rapidly propelling the growth of this segment in the global market. As per the International Energy Agency, condensing boilers can recover up to 90% of the heat lost in exhaust gases which reduces energy consumption by up to 20%. Their ability to integrate with renewable energy sources such as biomass and solar thermal makes them vital for achieving Europe’s decarbonization goals. Condensing boilers are becoming indispensable for reducing emissions and operational costs because industries prioritize sustainability.

By Fuel Insights

The natural gas segment led the European industrial boiler market by capturing 45.1% of the total market share in 2024. Its progress is due to its clean-burning properties and compliance with EU emission standards, emitting up to 50% less CO₂ compared to coal, according to the European Commission. These gas boilers are widely adopted in industries like food processing and district heating due to their efficiency and reliability. The International Energy Agency stated that natural gas remains a transitional fuel and is bridging the shift from fossil fuels to renewables. Its importance lies in supporting Europe’s decarbonization goals while ensuring stable energy supply for industrial processes.

The "Others" segment including biomass, biogas, and renewables is the quickest growing category and is estimated to exhibit a CAGR of 9.5% over the projection period. This development is spurred by the EU’s renewable energy targets and subsidies promoting sustainable practices. The European Biomass Association states that biomass boilers alone could account for a 15% annual increase in installations through 2030. These fuels reduce greenhouse gas emissions by up to 80% compared to fossil fuels and is making them vital for achieving Europe’s net-zero goals. Their importance lies in enabling industries to adopt eco-friendly solutions while reducing reliance on traditional energy sources.

REGIONAL ANALYSIS

Germany commanded the European industrial boiler market by holding 25.8% of the regional market share in 2024. Its strong industrial base but particularly in chemicals, automotive, and manufacturing sectors which rely heavily on advanced boiler systems is driving the dominance of this region in the global market. According to Eurostat, Germany has invested over €1 billion annually in retrofitting old boilers with energy-efficient technologies and that is in accordance with the EU’s decarbonization goals. The International Energy Agency stated that Germany’s focus on integrating renewable energy sources like biomass and biogas into industrial boilers has positioned it as a pioneer in sustainable practices.

The United Kingdom ranks as a top performer in the European industrial boiler market and is projected to grow at a CAGR of 5.8% during the forecast period. This is attributed to its aggressive push toward renewable energy integration and district heating systems and especially in urban areas. The European Commission notes that the UK has allocated over £500 million in subsidies for industrial energy efficiency projects, driving adoption of condensing and hybrid boilers. Additionally, the UK’s industrial strategy emphasizes achieving net-zero emissions by 2050, boosting investments in low-carbon boiler technologies.

France is another leading player in the European industrial boiler market. The country’s prominence is attributed to its extensive use of natural gas-fired boilers and growing adoption of biomass systems in industries such as food processing and pharmaceuticals. The International Energy Agency reports that France has set ambitious targets to reduce industrial emissions by 40% by 2030, encouraging industries to upgrade their boiler systems. Furthermore, France’s emphasis on nuclear energy complements its industrial boiler sector, ensuring stable energy supply. So, France’s position in the regional market is reinforced by its proactive environmental policies, technological advancements, and strong support for renewable energy integration.

KEY MARKET PLAYERS

The major players in the Europe industrial boiler market include Babcock & Wilcox, Bosch Industriekessel, Clayton Industries,Cochran, Doosan, FERROLI, Forbes Marshall, Fulton, Hoval, Hurst Boiler & Welding, IHI, John Cockerill, John Wood Group, Miura America, Mitsubishi Heavy Industries, Rentech Boilers, Thermax, and Viessmann.

MARKET SEGMENTATION

This research report on the Europe industrial boiler market is segmented and sub-segmented into the following categories.

By Capacity

- 10 MMBTU/hr

- 10 - 25 MMBTU/hr

- 25 - 50 MMBTU/hr

- 50 - 75 MMBTU/hr

- 75 - 100 MMBTU/hr

- 100 - 175 MMBTU/hr

- 175 - 250 MMBTU/hr

- > 250 MMBTU/hr

By Application

- Food Processing

- Pulp & Paper

- Chemical

- Refinery

- Primary Metal

- Others

By Technology

- Condensing

- Non-Condensing

By Fuel

- Natural Gas

- Oil

- Coal

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is driving the growth of the Europe industrial boiler market?

The growth of the Europe industrial boiler market is primarily driven by increasing industrialization, rising demand for energy-efficient heating solutions, and stringent environmental regulations promoting cleaner fuel adoption.

Which industries are the major consumers of industrial boilers in Europe?

Key industries using industrial boilers in Europe include food processing, chemicals, pharmaceuticals, power generation, and metal manufacturing.

What is the trend in industrial boiler technology in Europe?

The market is seeing advancements in energy-efficient designs, digital monitoring systems, and hybrid boiler technologies combining conventional and renewable fuel sources.

How is the demand for industrial boilers expected to evolve in the coming years?

The demand for industrial boilers in Europe is expected to grow steadily, driven by the need for energy efficiency, stricter emissions regulations, and increasing industrial activity.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]