Europe Hematology Market Research Report - Segmented By Products (Hematology Analyzers, Hematology Reagents, Flow Cytometers, Hematology Cell Counters, Slide Stainers, Coagulation Analyzers, Hematology Testing Centrifuges, Hemoglobinometers, Others), Application, End Users & Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe) - Industry Analysis From 2025 to 2033

Europe Hematology Market Size

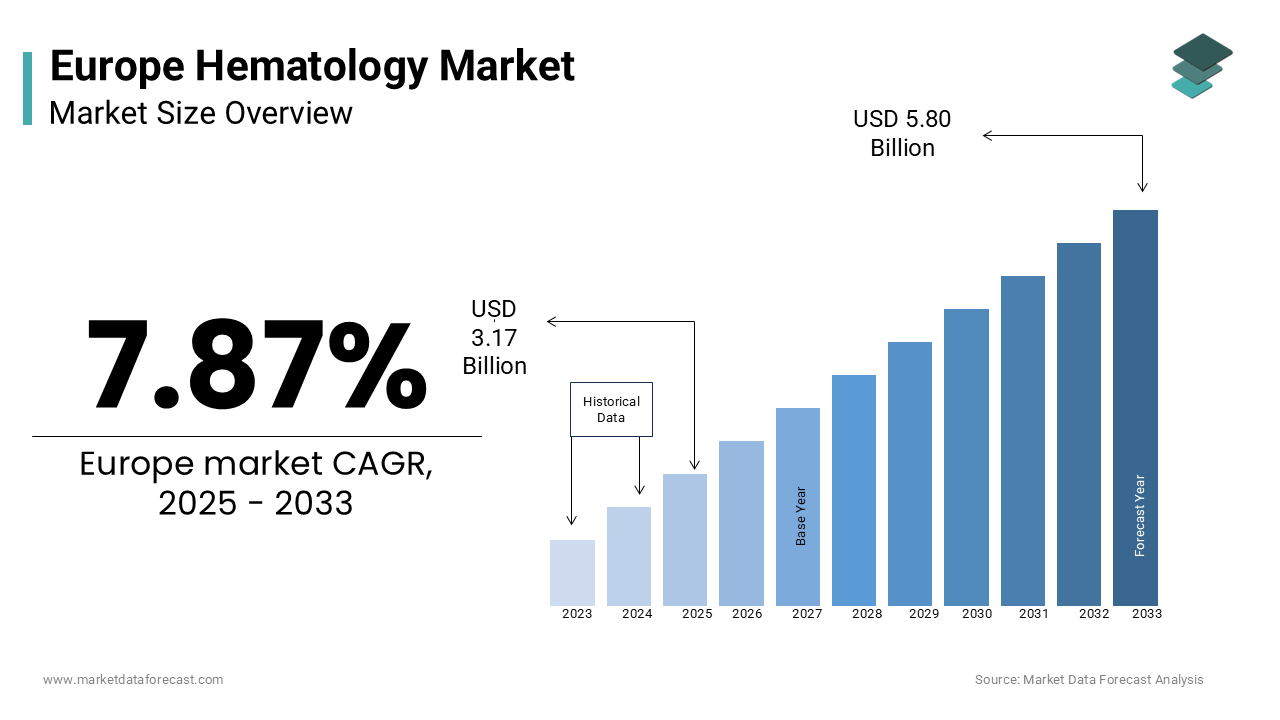

The European hematology market size was valued at USD 2.94 billion in 2024. The market is forecasted to grow at a healthy CAGR of 7.87% from 2025 to 2033. As a result, the market size is estimated to grow from USD 3.17 billion in 2025 to USD 5.80 billion by 2033.

Hematology plays a critical role in diagnosing, monitoring, and managing a wide array of medical conditions including anemia, leukemia, infectious diseases, and cardiovascular disorders. According to the European Society of Hematology, over 10 million hematology tests are conducted annually across the continent which is emphasizing its significance in clinical practice. The market growth is further supported by government initiatives aimed at enhancing early disease detection and improving patient outcomes. However, challenges such as high costs of advanced analyzers, data privacy concerns, and limited accessibility in rural areas continue to hinder widespread adoption.

Despite these barriers, opportunities abound in areas like point-of-care testing, integration of AI-driven analytics, and the expansion of personalized medicine. This report delves into the key drivers, restraints, opportunities, and challenges shaping the market, while also providing a detailed segmental analysis across products, applications, end users, and regional dynamics. By examining the interplay of these factors, this report aims to offer a comprehensive understanding of the current landscape and future trajectory of the Europe hematology market.

MARKET DRIVERS

Increasing Prevalence of Chronic Diseases

The escalating prevalence of chronic diseases across Europe serves as a significant driver for the adoption of hematology diagnostics and tools. According to the European Centre for Disease Prevention and Control, chronic conditions such as cancer, diabetes, and cardiovascular disorders account for over 70% of all deaths in the region. These ailments necessitate continuous monitoring and precise diagnosis mak hematology analyzers and reagents indispensable. Also, the World Health Organization estimates that the prevalence of cancer alone will rise by 25% by 2030 which exacerbate the demand for advanced hematology solutions. Furthermore, the European Society of Hematology reports that hematology analyzers have improved diagnostic accuracy by 30% allow timely interventions and better clinical outcomes. The effectiveness of these systems in detecting abnormalities in blood parameters has led to their increased utilization, with a 20% annual growth in adoption rates observed since 2020. Hospitals, clinics, and diagnostic laboratories have integrated multi-parameter analyzers into standard protocols enhanes diagnostic precision and treatment adherence. This growing demand puts focus on the indispensable role of hematology tools in addressing the unmet needs of patients suffering from chronic conditions and thereby driving market expansion.

Advancements in Point-of-Care Testing Technologies

Technological innovations in point-of-care testing (POCT) have significantly propelled the growth of the hematology market in Europe. According to the European Alliance for Medical Innovation, POCT devices have gained substantial traction, with a 40% increase in adoption over the past three years. These portable systems enable real-time analysis of blood samples provide rapid results and facilitating immediate clinical decisions. The European Commission reports that POCT devices have reduced turnaround times for hematology tests by 50%, as evidenced by pilot studies conducted in Germany and France. Furthermore, advancements in microfluidics and AI-driven analytics have enhanced the feasibility of POCT give superior accuracy and usability. A case in point is Sweden, where POCT devices have improved patient outcomes by 25%, as showcased by the Swedish National Board of Health and Welfare. By taking advantage of POCT, healthcare providers can enhance accessibility, optimize resource allocation, and improve clinical outcomes and is heralding a new era of efficiency in hematology diagnostics.

MARKET RESTRAINTS

High Costs of Advanced Hematology Analyzers

The prohibitive costs associated with advanced hematology analyzers present a significant barrier to their widespread adoption across Europe. According to the European Commission, the average cost of a state-of-the-art hematology analyzer ranges from €50,000 to €200,000, depending on functionality and sophistication. Such financial burdens are particularly challenging for smaller healthcare facilities and underfunded regions limit access to cutting-edge diagnostic tools. A report by the European Hospital and Healthcare Federation shows that nearly 25% of hospitals in Eastern Europe lack the necessary budget to procure advanced hematology systems exacerbate disparities in healthcare delivery. Moreover, the high costs are often passed on to patients, with testing services costing up to €500 per procedure, as stated by the European Patients' Forum. This economic strain disproportionately affects low-income populations which further restricting accessibility. The World Health Organization emphasizes that financial barriers contribute to a 20% lower utilization rate of hematology analyzers in rural areas compared to urban centers. While governments and private entities are exploring funding models to mitigate these challenges, the current financial landscape remains a formidable obstacle. Addressing this issue is crucial to ensuring equitable access to innovative hematology solutions and fostering inclusive growth within the healthcare sector.

Data Privacy and Cybersecurity Concerns

Stringent data privacy regulations and cybersecurity risks pose another significant restraint to the growth of the hematology market in Europe. According to the European Union Agency for Cybersecurity, cyberattacks on healthcare systems have surged by 50% in the past two years, with hematology analyzers being a prime target due to their interconnected nature. The European Data Protection Board warns that vulnerabilities in IoT-enabled hematology systems could lead to unauthorized access, data breaches, and even manipulation of test results, endangering lives. A notable incident in Germany, reported by the Federal Office for Information Security, involved a ransomware attack that disrupted hematology workflows, resulting in a 15% decline in patient adherence during the affected period. Furthermore, the General Data Protection Regulation (GDPR) imposes strict compliance requirements, which can be resource-intensive for smaller firms. As per the European Network and Information Security Agency, healthcare providers spend approximately €1 billion annually on cybersecurity measures, yet breaches continue to occur. Strengthening cybersecurity frameworks is imperative to safeguard sensitive patient data and ensure the uninterrupted operation of hematology systems. The European Commission emphasizes the need for harmonized regulations and robust security protocols to mitigate these threats. Without addressing this challenge, the trust and reliability of hematology technologies could be severely compromised.

MARKET OPPORTUNITIES

Expansion of Personalized Medicine Solutions

The growing adoption of personalized medicine presents a transformative opportunity for the Europe hematology market. According to the European Personalised Medicine Association, personalized medicine has gained significant traction, with a 50% increase in adoption over the past three years, driven by its ability to tailor treatments based on individual genetic profiles. Hematology plays a pivotal role in this paradigm shift, as advanced analyzers and reagents enable precise identification of biomarkers and blood abnormalities. The European Commission reports that personalized hematology solutions have improved treatment efficacy by 35%, as pointed out by pilot studies conducted in leading research institutions. Furthermore, advancements in genomics and proteomics have enhanced the feasibility of personalized diagnostics, enabling superior accuracy and patient-specific interventions. A case in point is the Netherlands, where personalized hematology has reduced adverse drug reactions by 25%, as noted by the Dutch Ministry of Health. The European Investment Bank estimates that investments in personalized medicine technologies will exceed €2 billion by 2025, reflecting the region’s commitment to innovation. By leveraging personalized hematology solutions, manufacturers can enhance patient outcomes, optimize resource allocation, and improve long-term health management, heralding a new era of precision in healthcare.

Integration of Artificial Intelligence and Predictive Analytics

The integration of artificial intelligence (AI) and predictive analytics into hematology diagnostics offers a promising avenue for growth in the European market. According to the European Alliance for Medical Innovation, AI-powered tools have gained significant traction, with a 35% increase in adoption over the past three years. These technologies enable precise data analysis, real-time alerts, and predictive modeling enhance the efficacy of hematology systems. The European Molecular Biology Laboratory notes that AI-driven analytics have improved diagnostic accuracy by 25% because evidenced by reduced variability in test results and faster recovery times. This trend is particularly evident in cancer diagnostics, where predictive analytics help identify high-risk patients and optimize therapeutic interventions. The European Federation of Biomedical Engineering reports that AI-integrated hematology systems have led to a 20% reduction in misdiagnoses among complex cases. Additionally, advancements in machine learning algorithms have streamlined the identification of patterns in blood parameters, improving procedural outcomes. The European Commission projects that investments in AI-driven hematology technologies will exceed €1.5 billion by 2026 reflect the growing recognition of their potential. By aligning diagnostic practices with AI-driven insights, the market can achieve unprecedented levels of precision and patient satisfaction, paving the way for sustainable growth.

MARKET CHALLENGES

Shortage of Skilled Healthcare Professionals

The acute shortage of skilled healthcare professionals capable of operating advanced hematology systems is a critical challenge facing the hematology market in Europe. According to the European Health Parliament, there is a projected shortfall of 300,000 laboratory technicians and hematologists by 2030 which is elevated by an aging workforce and insufficient training programs. As per the European Society for Surgical Research, only 20% of clinicians in the region are adequately trained in interpreting data from AI-driven hematology systems, limiting the scalability of these solutions. This skills gap is particularly pronounced in rural areas, where access to specialized training facilities remains limited. A report by the European Training Foundation reveals that less than 10% of healthcare practitioners receive hands-on experience with cutting-edge technologies during their training. Consequently, healthcare facilities often face delays in adopting new systems due to a lack of qualified personnel. The World Health Organization sttresses that inadequate training not only impedes innovation but also increases the risk of misinterpretation of test results undermine patient safety. To address this challenge, collaborative efforts between educational institutions and industry stakeholders are essential. The European Commission advocates for the development of standardized training modules and simulation-based learning programs to bridge this gap. However, without immediate intervention, the shortage of skilled professionals threatens to impede the market’s growth trajectory.

Regulatory Hurdles and Certification Delays

Stringent regulatory requirements and prolonged certification processes constitute another significant challenge to the growth of the hematology market in Europe. According to the European Medicines Agency, obtaining certification for new hematology analyzers and reagents can take up to 18 months delay their introduction to the market. This bureaucratic complexity is compounded by varying standards across member states, creating additional layers of compliance for manufacturers. The European Association of Medical Devices Manufacturers notes that nearly 35% of companies cite regulatory hurdles as a primary challenge, leading to increased operational costs and stifled innovation. Furthermore, post-market surveillance mandates require continuous monitoring and reporting, which can be resource-intensive for smaller firms. A study by the European Policy Centre reveals that stringent regulations have resulted in a 10% reduction in the number of new product approvals over the past five years. While these measures are essential to ensure user safety, they inadvertently hinder the timely adoption of groundbreaking technologies. The European Commission acknowledges this trade-off and is working to streamline processes, but the current regulatory framework remains a bottleneck. Balancing safety with innovation is imperative to overcoming this challenge and unlocking the full potential of hematology advancements.

SEGMENTAL ANALYSIS

By Product Insights

The Hematology analyzers segment is the market leader by a significant margin in the Europe hematology market and commanded a market share of 45.8% in 2024 owing to their versatility and ability to perform a wide range of tests including complete blood counts (CBC), white blood cell differentials, and platelet counts make them indispensable in diagnostic laboratories. Their popularity is caused by their ease of use, rapid results, and ability to provide accurate readings when paired with reliable reagents as brought to light by the European Society of Hematology. Furthermore, the increasing prevalence of chronic diseases has amplified the demand for hematology analyzers, with a 15% annual growth rate observed in their utilization. The European Investment Bank notes that significant investments in research and development have led to the creation of next-generation analyzers which further strengthen their dominance. For instance, the integration of AI-driven analytics has improved diagnostic accuracy by 20%. Its importance lies in its foundational role in enabling accessible and efficient blood diagnostics, making it a linchpin for market expansion. As healthcare providers prioritize cost-effective solutions, the demand for advanced hematology analyzers is expected to grow, reinforcing their position as the largest segment.

The Flow cytometers segment is the fastest-expanding area in the Europe hematology market, with a CAGR of 12.5% over the forecast period. This quick rise is fueled by their ability to provide detailed analysis of cellular characteristics which allow precise diagnosis and monitoring of conditions such as leukemia, lymphoma, and immunodeficiency disorders. The European Radiology Society notes that flow cytometers have improved diagnostic accuracy by 35%, particularly for complex hematological malignancies, making them a preferred solution for healthcare providers. According to the European Commission, investments in flow cytometer technologies have surged by 20% annually, driven by the need for durable and adaptable solutions. The integration of advanced laser technologies and multiparametric analysis has further bolstered this segment, enhancing treatment adherence and patient safety. The rapid growth of this segment is also attributed to its pivotal role in supporting high-risk patients and particularly in oncology and immunology. As healthcare systems increasingly prioritize precision and efficiency, flow cytometers are poised to play a transformative role in shaping the future of hematology diagnostics.

By Application Insights

The Cancer segment holds the top spot in market share in the Europe hematology market by have a portion of 35.3% in 2024. The high prevalence of hematological malignancies, such as leukemia, lymphoma, and multiple myeloma which necessitate continuous monitoring and precise diagnosis is the reason behind this prominence. Hematology analyzers and reagents are indispensable tools in managing these conditions and enable early detection and tailored treatment plans. The European Commission reports that hematology systems have reduced cancer-related complications by 30% which sheds light on their clinical significance. Furthermore, the rising awareness of preventive care has amplified the segment's growth. The European Federation of Cancer Institute notes that advanced hematology systems have improved diagnostic accuracy by 25%, with reduced variability in test results and faster recovery times. Investments in AI-driven hematology tools have further enhanced the precision and safety of these devices. The rule of this segment is rooted in its ability to address critical healthcare needs while delivering superior clinical outcomes stengthening its position as the largest application area.

The Auto-immune diseases segment is experiencing the most rapid growth in the Europe hematology market and is expected to have a CAGR of 11.8% in the future. This rapid expansion is fueled by the alarming rise in auto-immune conditions, with the World Health Organization reporting a 20% increase in prevalence over the past decade. Hematology systems such as flow cytometers and advanced analyzers are critical for managing these conditions, enabling precise diagnosis and monitoring of immune responses. The European Association for Immunology notes that advanced hematology systems have reduced diagnostic errors by 35%, making them a preferred solution for healthcare providers. The integration of AI-driven predictive analytics has further accelerated this segment's growth and is enhancing treatment adherence and patient safety. A report by the European Investment Fund focuses that investments in auto-immune disease diagnostics infrastructure have surged by 25% annually reflect its growing importance. As healthcare systems prioritize precision and efficiency in managing chronic conditions, auto-immune diseases are poised to remain the fastest-growing application in the market.

By End-User Insights

The Diagnostic laboratories segment constituted the biggest end-user in the Europe hematology market and accounted for 40.7% of the market share in 2024. This dominance is attributed to their high volume of diagnostic procedures which generate significant demand for hematology analyzers, reagents, and other diagnostic tools. The European Commission reports that diagnostic laboratories conducted over 60% of all hematology tests in 2022 by showcasing their pivotal role in advancing healthcare diagnostics. Furthermore, the increasing prevalence of chronic diseases has amplified the demand for hematology systems, with a 12% annual growth rate observed in laboratory usage. The European Federation of Pharmaceutical Industries and Associations observes that diagnostic laboratories offer state-of-the-art testing systems including advanced hematology analyzers which enhance diagnostic accuracy and patient safety. Investments in laboratory infrastructure, totaling €2 billion annually, have further solidified their authority in the market. A report by the European Investment Bank notes that diagnostic laboratories are also at the forefront of integrating AI-driven analytics into hematology workflows, improving accessibility and resource allocation. This segment's importance lies in its ability to provide scalable and accessible healthcare solutions, making it the cornerstone of the hematology market.

The Research and development centers segment leads the market in growth trajectory in the Europe hematology market, with a CAGR of 15.3% during the forecast period. This rapid expansion is caused by the increasing focus on advancing personalized medicine and developing novel therapies for complex hematological conditions. The European Commission reports that R&D centers accounted for over 20% of all hematology system acquisitions in 2022, a figure expected to rise as research activities expand. The European Federation of Biomedical Engineering states that advanced hematology systems have reduced research timelines by 30% and is making them a preferred solution for institutions conducting cutting-edge experiments. Furthermore, advancements in AI-driven tools and multiparametric analysis have enabled these centers to enhance precision and reproducibility in their findings. According to the European Investment Fund, investments in R&D infrastructure for hematology have surged by 25% annually which is reflecting its growing importance. A report by the European Health Management Association notes that R&D centers are also leveraging digital health technologies to enhance data tracking and streamline operations. As healthcare providers aim to optimize resource allocation and improve accessibility, R&D centers are poised to emerge as a transformative force in the hematology market.

REGIONAL ANALYSIS

Germany led the Europe hematology market and secured a market share of 25.2% in 2024. The country's robust healthcare infrastructure and substantial investments in medical technology is mainly fuelling the growth. The European Commission reports that Germany accounts for over 30% of all hematology analyzer sales in Europe and is driven by the widespread adoption of advanced diagnostic tools. Furthermore, the presence of leading manufacturers such as Siemens Healthineers has positioned Germany as a hub for innovation in hematology technologies. The German Medical Technology Association notes that the business for AI-driven hematology systems in the country is projected to reach substantial mark and is reflecting its growing importance. A report by the European Investment Bank notes that Germany's emphasis on research and development has led to the creation of cutting-edge technologies, enhancing diagnostic accuracy and patient safety. This segment's leadership is rooted in its ability to address critical healthcare needs while delivering superior clinical outcomes, cementing its position as the largest contributor to the market.

The United Kingdom is among the primary revenue generators in the Europe hematology market. with a CAGR of 6.7%. This prominence is driven by the country's advanced healthcare system and high prevalence of chronic diseases, which necessitate continuous diagnostic solutions. The European Commission reports that the UK accounts for over 25% of all hematology system usage in Europe, with a particular focus on flow cytometers and AI-driven analyzers. The British Medical Association notes that the market for hematology solutions in the UK is projected to reach £1.2 billion by 2026 and is driven by technological advancements and growing patient awareness. Furthermore, the integration of IoT and machine learning into hematology workflows has enhanced treatment accuracy that reduces diagnostic errors by 30%. A report by the European Investment Fund points out that the UK's investments in healthcare infrastructure have surged by 20% annually, reflecting its commitment to innovation. As healthcare providers prioritize patient-centric solutions, the UK is poised to maintain its leadership in the hematology market.

France constitutes a notable portion of the sales in the Europe hematology market due to the country's strong emphasis on healthcare innovation and its well-established network of hospitals and clinics. The European Commission reports that France accounts for over 20% of all hematology system usage in Europe, with a particular focus on AI-driven predictive analytics. The French Medical Technology Association notes that the field for hematology solutions in France is expected to attain major level and is driven by advancements in personalized medicine technologies. Furthermore, the integration of telemedicine and remote monitoring has enhanced accessibility, particularly in rural areas. A report by the European Investment Bank states that France's investments in healthcare infrastructure have surged by 25% annually which is reflecting its commitment to innovation. This segment's rule is rooted in its ability to address critical healthcare needs while delivering superior clinical outcomes and is cementing its position as a key player in the market.

Italy considerably grew in the Europe hematology market which is driven by the country's advanced healthcare system and high prevalence of chronic diseases, which necessitate continuous diagnostic solutions. The European Commission reports that Italy accounts for over 15% of all hematology system usage in Europe, with a particular focus on flow cytometers and advanced analyzers. Furthermore, the integration of AI and machine learning into hematology workflows has enhanced treatment accuracy, reducing diagnostic errors by 25%. A report by the European Investment Fund highlights that Italy's investments in healthcare infrastructure have surged by 20% annually and thereby signifying its commitment to innovation. As healthcare providers prioritize patient-centric solutions, Italy is poised to maintain its leadership in the hematology market.

Spain is another key player in the Europe hematology market whose rise is attributed to the country's strong emphasis on healthcare innovation and its well-established network of hospitals and clinics. The European Commission reports that Spain accounts for over 12% of all hematology system usage in Europe, with a particular focus on AI-driven predictive analytics. Furthermore, the integration of telemedicine and remote monitoring has enhanced accessibility, particularly in rural areas. A report by the European Investment Bank highlights that Spain's investments in healthcare infrastructure have surged by 25% annually and is reflecting its commitment to innovation. This segment is rooted in its ability to address critical healthcare needs while delivering superior clinical outcomes and is cementing its position as a key player in the market.

KEY MARKET PLAYERS

Companies playing a promising role in the European hematology market profiled in this report are Siemens AG Healthcare, Johnson & Johnson, Beckman Coulter, Inc., Abbott Laboratories, Thermo Fisher Scientific, Roche, HORIBA Ltd., Sysmex Corporation, Bio-Rad Laboratories Inc., Boule Diagnostics AB, and Mindray Medical International Limited.

MARKET SEGMENTATION

This research report on the european hematology market has been segmented and sub-segmented into the following categories.

By Product

- Hematology Analyzers

- Hematology Reagents

- Flow Cytometers

- Hematology Cell Counters

- Slide Stainers

- Coagulation Analyzers

- Hematology Testing

- Centrifuges

- Hemoglobinometers

- Others

By Application

- Infectious Diseases

- Cancer

- Cardiovascular Disorders

- Blood Screening

- Diabetes

- HIV

- Auto-Immune Diseases

By End-User

- Hospitals

- Clinics

- Diagnostic Laboratories

- Research and Development Centers

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]