Europe Helicopter Market Size, Share, Trends, & Growth Forecast Report Segmented By Point of Sale (OEM and Aftermarket), Type, Application, Component & System, Number of Engines, Component & System, Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2024 to 2033

Europe Helicopter Market Size

The European Helicopter market was worth USD 10.08 billion in 2024. The European market is projected to reach USD 16.76 billion by 2033 from USD 10.66 billion in 2025, growing at a CAGR of 5.81% from 2025 to 2033.

As of 2023, Europe remains one of the largest consumers of helicopters globally due to the robust demand for advanced rotorcraft technologies tailored to meet specific operational needs. According to Eurocontrol, which is the air traffic management organization of Europe, helicopter operations in Europe have witnessed steady growth over the past decade, with approximately 15% of all rotary-wing flights dedicated to emergency medical services (EMS), underscoring their critical role in public safety infrastructure.

The rising investments in modernizing aging fleets, particularly among NATO member states seeking to enhance defense capabilities amidst evolving geopolitical tensions are fuelling the demand for helicopters in the European region. France, Germany, and the United Kingdom are leading contributors to this trend and collectively account for nearly 60% of total regional expenditure on military-grade helicopters, as noted by the Stockholm International Peace Research Institute. On the civilian front, urban air mobility initiatives and offshore energy support operations continue to drive demand for light and medium-weight helicopters. Meanwhile, stringent regulatory frameworks imposed by the European Union Aviation Safety Agency ensure high standards of safety and environmental compliance, further shaping the competitive landscape of this thriving market.

MARKET DRIVERS

Increasing Demand for Emergency Medical Services (EMS) and Search-and-Rescue (SAR) Operations

The rising demand for helicopters in emergency medical services (EMS) and search-and-rescue (SAR) operations is driving the growth of the Europe helicopters market. These sectors are critical to public safety, particularly in remote and urban areas where rapid response is essential. According to Eurocontrol, over 80,000 helicopter missions were conducted annually in Europe for medical emergencies as of 2022, with Germany and France being the largest contributors. As per the European Commission, approximately 25% of all SAR operations in the region involve helicopters, which is emphasizing their indispensability. Additionally, according to the reports of the European Maritime Safety Agency, maritime SAR activities account for nearly 15% of total helicopter usage, which is further amplifying demand. With aging fleets requiring replacement and advancements in technology enhancing operational efficiency, governments are prioritizing fleet modernization, thereby propelling market growth.

Rising Adoption of Helicopters in Offshore Energy Operations

The growing adoption of helicopters in offshore energy operations, particularly in regions like the North Sea is further propelling the European helicopters market expansion. The commitment of the European Union to renewable energy has spurred offshore wind farm installations, which is creating a parallel need for reliable transportation and maintenance support via helicopters. A report by the International Energy Agency states that Europe accounts for over 40% of global offshore wind capacity, with projections indicating a compound annual growth rate of 8% through 2030. Helicopters are indispensable for transporting personnel and equipment to these remote locations, with the UK Civil Aviation Authority estimating that over 100,000 flights annually are dedicated to offshore energy logistics. Furthermore, NATO’s increased defense spending has indirectly supported this sector by encouraging dual-use technologies. These factors collectively underscore the pivotal role of offshore energy operations in driving the European helicopter market forward.

MARKET RESTRAINTS

Stringent Regulatory Frameworks and Environmental Compliance

One of the major restraints impacting the European helicopter market is the stringent regulatory frameworks imposed by governing bodies such as the European Union Aviation Safety Agency (EASA). These regulations, while ensuring safety and environmental sustainability, often lead to increased operational costs and delays in fleet modernization. For instance, EASA mandates rigorous noise emission standards, which require operators to invest in costly upgrades or replacements of older models. According to a report by the European Environment Agency, helicopters contribute approximately 0.5% of total aviation emissions in Europe, prompting stricter emission norms that further strain manufacturers and operators. Additionally, the certification process for new helicopter models can take up to five years, as highlighted by the European Commission. These prolonged timelines and compliance costs hinder market growth, particularly for small and medium-sized enterprises operating in the sector.

Economic Uncertainty and Budget Constraints

Economic uncertainty and budget constraints across Europe also pose significant challenges to the helicopter market. Fluctuating economic conditions, coupled with inflationary pressures, have led to reduced defense and civil aviation budgets in several countries. The European Central Bank reports that defense spending growth in the region has slowed to 2.3% in 2023, compared to 4.5% in 2021, affecting procurement plans for military-grade helicopters. Similarly, the European Investment Bank highlights that private operators face liquidity challenges due to rising fuel prices, which account for nearly 30% of operational costs. This financial strain is further exacerbated by geopolitical tensions, which divert funds away from civilian helicopter projects. As a result, many operators are delaying fleet expansions or opting for cost-effective alternatives, thereby restraining overall market growth in the region.

MARKET OPPORTUNITIES

Advancements in Urban Air Mobility (UAM) Initiatives

The European helicopter market is poised to benefit significantly from advancements in urban air mobility (UAM) initiatives, which are gaining traction as cities seek innovative solutions for congestion and pollution. The European Commission has identified UAM as a key pillar of its sustainable urban transport strategy, with projections indicating that the global UAM market could reach USD 9 billion by 2030. According to Eurocontrol, over 300 UAM-related projects are currently underway in Europe, with countries like Germany and France leading pilot programs for electric vertical takeoff and landing (eVTOL) aircraft. These initiatives create opportunities for traditional helicopter manufacturers to diversify into hybrid and electric rotorcraft technologies. Additionally,

Expansion of Helicopter Services in Emerging Markets within Europe

The expansion of helicopter services in emerging markets within Eastern and Southern Europe, where infrastructure development is accelerating, which is another significant opportunity in the European helicopters market. As per the reports of the European Bank for Reconstruction and Development, investments in regional connectivity have grown by 15% annually over the past five years, which is creating demand for helicopters in construction, tourism, and emergency services. For instance, Romania and Poland have seen a 20% increase in helicopter usage for medical evacuations and disaster response, according to the European Emergency Number Association. Furthermore, according to the European Maritime Safety Agency, coastal nations like Greece and Croatia are leveraging helicopters for tourism and maritime logistics, with over 50,000 annual flights supporting these sectors. As these regions continue to develop, the need for versatile and reliable helicopter solutions presents a lucrative growth avenue for manufacturers and operators alike.

MARKET CHALLENGES

High Operational and Maintenance Costs

One of the major challenges facing the European helicopter market is the high operational and maintenance costs associated with rotorcraft, which limit their accessibility for smaller operators. As per the European Aviation Safety Agency, maintenance expenses account for nearly 40% of the total lifecycle cost of a helicopter, which is making it a significant financial burden. Additionally, fuel costs, which constitute approximately 30% of operational expenses, have risen sharply due to geopolitical tensions and supply chain disruptions, as reported by the European Central Bank. These escalating costs are particularly challenging for regional operators in Eastern Europe, where profit margins are already thin. According to the European Investment Bank, small-scale operators often delay fleet upgrades or reduce flight operations to manage expenses, which is stifling the European market growth.

Limited Infrastructure for Helicopter Operations

The limited infrastructure available for helicopter operations across many parts of Europe, particularly in rural and underdeveloped regions is further challenging the growth of the Europe helicopters market. As per the reports of the European Commission, only 20% of heliports in Europe are equipped to handle modern, medium-weight helicopters, creating bottlenecks for expanding services. Furthermore, according to Eurocontrol, airspace congestion in urban areas restricts helicopter usage, with over 60% of European cities lacking dedicated air corridors for rotorcraft. This lack of infrastructure is especially problematic for emergency medical services and search-and-rescue operations, where timely access is critical. The European Union Agency for the Space Programme also notes that inadequate navigation and communication systems in remote areas hinder the efficiency of helicopter operations. Addressing these infrastructure gaps requires substantial investment, which many governments and private entities are reluctant to undertake amidst competing priorities, thereby constraining market potential.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

5.81% |

|

Segments Covered |

By Point of Sale, Type, Application, Component & System, Number of Engines, Component & System, and Country |

|

Various Analyses Covered |

Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and Rest of Europe |

|

Market Leaders Profiled |

Airbus Helicopters SAS (France), Bell Helicopters (US), The Boeing Company (US), Leonardo S.p.A. (Italy), Sirkorsky-Lockheed Martin (US), Russian Helicopters (Russia), and Kawasaki Heavy Industries (Japan). |

SEGMENTAL ANALYSIS

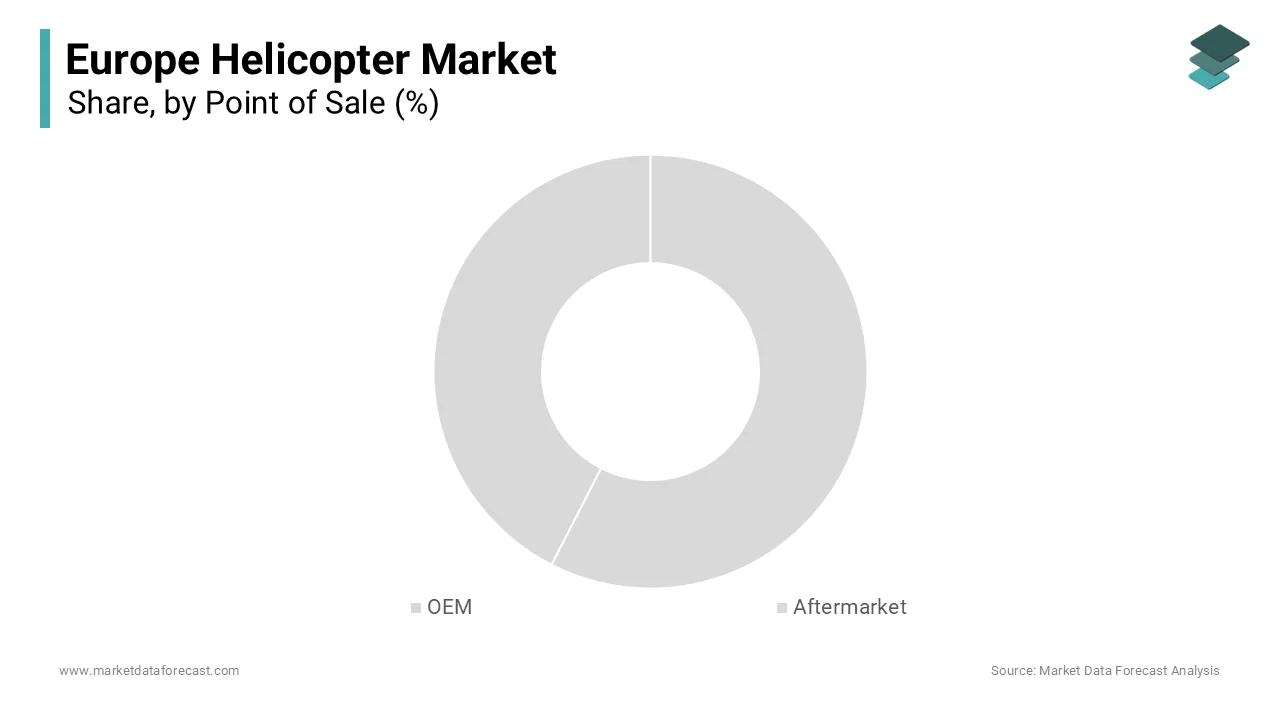

By Point of Sale Insights

The OEM segment led the market by accounting for 60.6% of the European market share in 2024. The high demand for new helicopters equipped with advanced technologies, particularly in defense and urban air mobility sectors are contributing to the domination of the OEM segment in the European market. According to NATO, defense-related OEM sales grew by 5% annually due to the fleet modernization programs. The segment's importance lies in its ability to introduce innovative rotorcraft, such as hybrid and electric models, which align with sustainability goals. With Eurocontrol estimating over 80,000 annual missions relying on new-generation helicopters, the OEM segment remains critical for meeting evolving operational needs.

The aftermarket segment is likely to be the fastest growing segment in the European market and is predicted to witness a CAGR of 4.5% over the forecast period. Factors such as aging fleets requiring frequent maintenance and repairs and stringent safety regulations imposed by the European Union Aviation Safety Agency are propelling the growth of the aftermarket segment in the European market. Annual spending on MRO services exceeds EUR 3 billion, as highlighted by the European Emergency Number Association, with emergency services driving demand. The segment's rapid expansion underscores its importance in ensuring operational safety and efficiency, making it indispensable for sustaining Europe’s helicopter operations amidst rising operational complexities.

By Type Insights

The medium military helicopter segment (4.5–8.5 tons) dominated the market by accounting for 40.8% of the European market share in 2024 due to its versatility in missions like troop transport, combat support, and disaster response. As per the reports of NATO, defense spending on medium helicopters grew by 6% annually, with over 1,200 units operational across Europe. These helicopters strike a balance between payload capacity, range, and cost-efficiency, making them indispensable for modern militaries. According to the European Commission, the role of medium military helicopter is critical in addressing geopolitical challenges, particularly in Eastern Europe. With aging fleets requiring replacement, medium helicopters remain critical for ensuring operational readiness and enhancing defense capabilities.

The light civil and commercial helicopter segment (<3.1 tons) is predicted to showcase a notable CAGR of 5.2% over the forecast period. The rising demand for emergency medical services (EMS), urban air mobility (UAM), and tourism are fuelling the expansion of the light civil and commercial helicopter segment in the European market. According to the European Investment Bank, more than 70% of EMS helicopters in Europe are light models, conducting approximately 20,000 annual missions. Advancements in hybrid and electric technologies have also reduced operational costs, boosting adoption. The European Emergency Number Association emphasizes their importance in remote-area accessibility and rapid response. Their affordability and adaptability make them pivotal for emerging applications, positioning them as a key growth driver in the civil helicopter market.

By Application Insights

The military transport helicopters dominated the European helicopter market by occupying a share of 35.7% of the European market in 2024. These helicopters are essential for troop deployment, logistics support, and humanitarian missions, with NATO reporting a 7% annual increase in procurement due to modernization programs. The European Commission notes that over 800 transport helicopters are operational across Europe, with France and Germany leading investments. Their ability to operate in diverse terrains and carry heavy payloads makes them indispensable for defense operations. Additionally, their role in disaster relief, such as during floods or wildfires, underscores their strategic importance. With geopolitical tensions driving fleet upgrades, military transport helicopters remain a cornerstone of Europe's defense infrastructure.

The emergency rescue and medical support helicopter segment is anticipated to witness a CAGR of 6.1% over the forecast period due to the increasing demand for rapid medical response, particularly in remote areas. According to the reports of the European Emergency Number Association, these helicopters conducted over 80,000 life-saving missions annually in Europe as of 2022. Advances in navigation and communication technologies have enhanced their efficiency, while urbanization has amplified the need for quick access to healthcare. As per the European Investment Bank, governments are investing heavily in EMS infrastructure, with countries like Germany and France expanding fleets. Their critical role in saving lives ensures sustained growth and innovation in this vital sector.

By Component & System Insights

The airframe segment captured the leading share of European market in 2024. The critical role of airframes in defining a helicopter's structural integrity, performance, and payload capacity is majorly driving the segmental expansion in the European market. Aerostructures and main rotor systems, key subcomponents of the airframe, are particularly significant due to their direct impact on flight efficiency and safety. EASA highlights that over 60% of maintenance-related expenditures are linked to airframe components, reflecting their importance in operational reliability. The European Commission notes that advancements in lightweight composite materials have further boosted demand for modern airframes, especially in military and civil applications. With stringent safety regulations and aging fleets requiring upgrades, the airframe segment remains pivotal for the helicopter industry.

The avionics segment is predicted to grow at the fastest CAGR of 7.2% over the forecast period due to factors such as the increasing demand for advanced navigation, communication, and stability augmentation systems that enhance operational safety and efficiency. According to the European Defence Agency, investments in avionics for military helicopters have surged by 8% annually due to the integration of AI-based flight control systems and real-time data analytics. In the civil sector, Eurocontrol notes that emergency systems and environment control systems are becoming standard in new models, particularly for urban air mobility (UAM) and emergency medical services (EMS). According to the European Investment Bank, avionics innovations are critical for meeting regulatory compliance and reducing pilot workload. As helicopters evolve into smarter, more autonomous platforms, avionics will remain a key driver of technological advancement and market growth.

By Number of Engines Insights

The twin-engine segment held the largest share of the European helicopters market in 2024. The domination of twin-engines segment is driven from their superior safety, reliability, and ability to perform long-range missions, which is making them ideal for critical applications such as offshore energy operations, emergency medical services (EMS), and military transport. As per the European Maritime Safety Agency, more than 70% of offshore helicopters in Europe are twin-engine models, given their ability to operate in challenging maritime environments. Additionally, EASA emphasizes that twin-engine configurations are preferred for EMS and search-and-rescue (SAR) missions due to their redundancy and enhanced safety features. With increasing demand for versatile and high-performance rotorcraft, twin-engine helicopters remain a cornerstone of the European market.

The single-engine helicopter segment is anticipated to expand at a CAGR of 4.8% over the forecast period due to their cost-effectiveness, lower maintenance requirements, and suitability for light-duty applications such as training, tourism, and urban air mobility (UAM). According to the European Investment Bank, single-engine helicopters are increasingly being adopted for UAM initiatives, particularly in urban areas where smaller, agile rotorcraft are needed for short-distance travel. Furthermore, advancements in engine efficiency and safety technologies have expanded their operational scope, making them more competitive. As per the European Emergency Number Association, single-engine models are also gaining traction in emergency response roles in less densely populated regions. Their affordability and adaptability position them as a key growth driver in emerging applications across Europe.

By Component & System Insights

The aerostructures segment dominated the market by occupying a share of 25% in the European market in 2024. Aerostructures form the backbone of a design of helicopter and include components like fuselages, rotor blades, and tail assemblies, which directly impact performance and safety. According to the European Commission, advancements in lightweight composite materials, such as carbon fiber and advanced alloys, have significantly increased demand for modern aerostructures, particularly in military and civil applications. As per the reports of the EASA, more than 40% of maintenance-related costs are linked to aerostructure upkeep, which is indicating their critical role in operational reliability. With aging fleets requiring upgrades and increasing emphasis on fuel efficiency, aerostructures remain a pivotal focus for manufacturers and operators alike.

The avionics segment is another key segment in the European market and is likely to showcase the fastest CAGR of 7.5% over the forecast period due to factors such as rising adoption of advanced navigation, communication, and flight control systems that enhance safety, efficiency, and operational capabilities. As per the European Defence Agency, investments in avionics for military helicopters have surged by 9% annually due to the integration of AI-based stability augmentation systems and real-time data analytics. In the civil sector, According to the Eurocontrol, emergency systems and environment control systems are becoming standard in new models, particularly for urban air mobility (UAM) and emergency medical services (EMS). The European Investment Bank emphasizes that avionics innovations are critical for meeting stringent regulatory standards and reducing pilot workload. As helicopters evolve into smarter and more autonomous platforms, avionics will continue to drive technological advancements and market expansion.

KEY MARKET PLAYERS

The major players in the Europe helicopters market include Airbus Helicopters SAS (France), Bell Helicopters (US), The Boeing Company (US), Leonardo S.p.A. (Italy), Sirkorsky-Lockheed Martin (US), Russian Helicopters (Russia), and Kawasaki Heavy Industries (Japan).

REGIONAL ANALYSIS

France was the largest market for helicopters in Europe and held 25.3% of the regional market share in 2024. The domination of France in the European market is majorly driven by the robust aerospace industry of France that is spearheaded by global leaders like Airbus Helicopters, which commands over 50% of the global civil and parapublic helicopter market. As per the European Defence Agency, France's military modernization programs, including investments in heavy and medium helicopters, have bolstered demand. Additionally, France's focus on innovation, particularly in hybrid-electric rotorcraft, aligns with sustainability goals. According to the Eurocontrol, France's strategic position in offshore energy operations in the North Sea further amplifies its helicopter usage. With strong government support and cutting-edge R&D, France remains at the forefront of the European helicopter market.

Germany is another significant player in the European helicopters market and is expected to expand at a CAGR of 5.1% during the forecast period. The advanced manufacturing capabilities of Germany and significant investments in defense and emergency medical services (EMS) are propelling the helicopters market growth in Germany. According to the reports of the NATO, defense spending of Germany on helicopters has grown by 6% annually due to the fleet upgrades for search-and-rescue and troop transport missions. Furthermore, as per the European Emergency Number Association, Germany operates one of Europe's largest EMS fleets, conducting over 50,000 annual missions. The country's emphasis on urban air mobility (UAM) initiatives also positions it as a leader in adopting next-generation rotorcraft technologies, ensuring sustained growth and innovation.

The United Kingdom holds a prominent position in the European helicopter market. The extensive offshore energy sector of the UK, particularly in the North Sea, where helicopters are indispensable for transporting personnel and equipment are driving the UK helicopters market. As per the reports of the European Maritime Safety Agency, more than 30% of Europe's offshore helicopter operations are based in the UK. Additionally, the UK's commitment to defense modernization includes procurement of advanced attack and reconnaissance helicopters. The country is also a hub for avionics innovation, with companies pioneering autonomous flight systems.

MARKET SEGMENTATION

This research report on the European helicopter market is segmented and sub-segmented into the following categories.

By Point of Sale

- OEM

- Aftermarket

By Type

- Military

- Heavy Helicopters ( >8.5 Tons)

- Medium Helicopters (4.5 -8.5 Tons)

- Light Helicopters ( <4.5 Tons)

- Civil & Commercial

- Heavy Helicopters ( >9.0 Tons)

- Medium Helicopters (3.1 –9.0 Tons)

- Light Helicopters ( <3.1 Tons)

By Application

- Military

- Attack & Reconnaissance Helicopters

- Transport Helicopters

- Maritime Helicopters

- Training Helicopters

- Search & Rescue Helicopters

- Civil & Commercial

- Transport Helicopters

- Civil Utility Helicopters

- Emergency Rescue & Medical Support Helicopters

- Offshore Helicopters

By Component & System

- Airframe

- Aerostructures

- Main Rotor Systems

- Cabin Interiors

- Anti-torque Systems

- Transmission Systems

- Electrical Systems

- Hydraulic Systems

- Avionics

- Stability Augmentation Systems

- Flight Control Systems

- Undercarriages

- Environment Control Systems

- Emergency Systems

- Special-purpose Systems

- Engines

By Number of Engines

- Twin Engines

- Single Engines

By Component & System

- Aerostructures

- Main Rotor Systems

- Avionics

- Landing Gear Systems

- Emergency Systems

- Cabin Interiors

- Actuators

- Filters

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What are the key factors driving the growth of the Europe helicopter market?

The Europe helicopter market is driven by increasing demand for emergency medical services (EMS), search and rescue (SAR) operations, and defense modernization programs. Additionally, growing tourism and offshore oil and gas exploration contribute to market expansion.

What are the major applications of helicopters in the European market?

Helicopters in Europe are primarily used for military operations, emergency medical services, law enforcement, tourism, offshore oil and gas transport, and corporate travel.

What are the key technological advancements in the European helicopter industry?

Advancements include hybrid-electric propulsion, autonomous flight systems, improved avionics, and enhanced rotor blade designs for increased efficiency and safety.

What is the future outlook for the Europe helicopter market?

The market is expected to see steady growth, driven by increasing demand for emergency response services, defense procurement, and technological innovations in hybrid and electric helicopters.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]