Europe Glass Packaging Market Size, Share, Trends & Growth Forecast Report By Product (Borosilicate, De-Alkalized Soda Lime, And Soda Lime), By Application, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2025 to 2033

Europe Glass Packaging Market Size

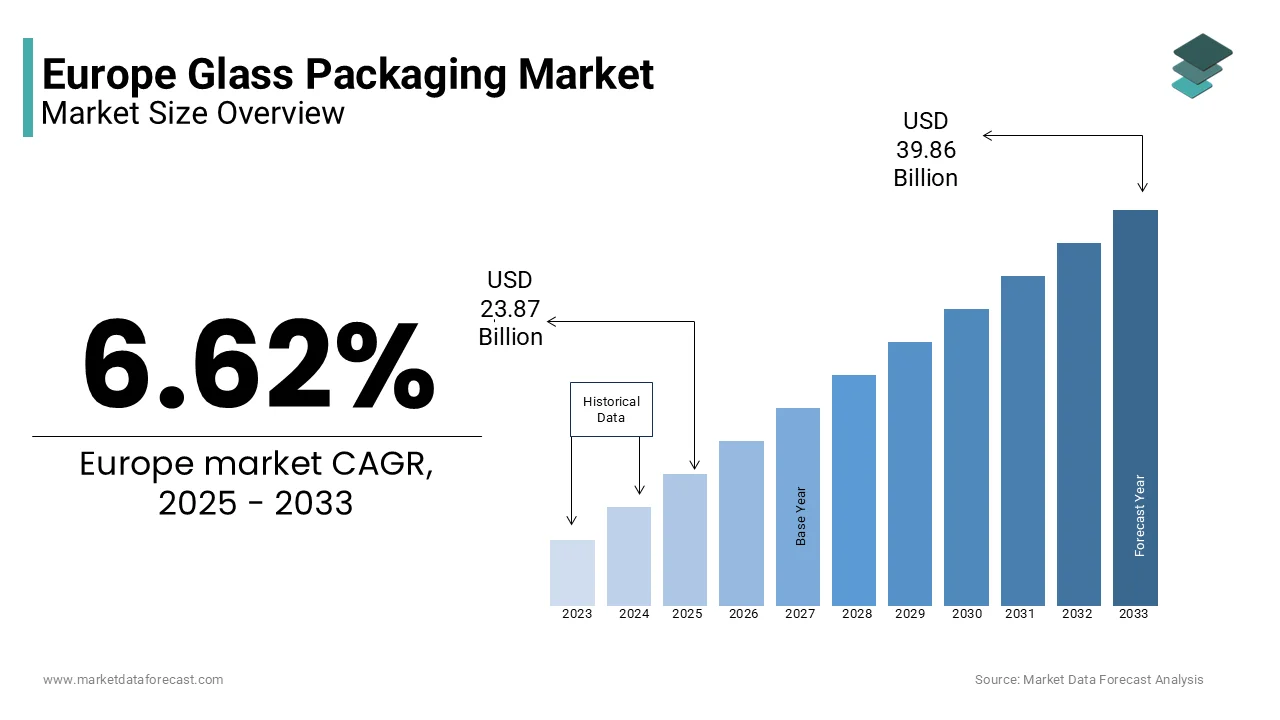

The Europe glass packaging market size was valued at USD 22.39 billion in 2024. The European market is estimated to be worth USD 39.86 billion by 2033 from USD 23.87 billion in 2025, growing at a CAGR of 6.62% from 2025 to 2033.

The Europe glass packaging market’s growth is driven by increasing consumer preference for sustainable packaging solutions in the food and beverage sector. Glass packaging is favored for its recyclability, inertness, and ability to preserve product quality by making it indispensable for premium products. Additionally, stringent environmental regulations, such as the EU’s Circular Economy Action Plan, mandate the use of recyclable materials that is likely to fuel the growth of the market.

MARKET DRIVERS

Rising Demand for Sustainable Packaging Solutions

A key driver of the Europe glass packaging market is the growing emphasis on sustainability. According to the European Environmental Agency, over 60% of consumers in Europe prioritize eco-friendly packaging, with glass being a preferred choice due to its infinite recyclability. The European Commission’s Circular Economy Action Plan mandates that all packaging must be reusable or recyclable by 2030 is creating a favorable environment for glass adoption. Glass packaging also aligns with corporate sustainability goals. For example, as per the European Federation of Food, Agriculture, and Tourism Trade Unions, major beverage companies like Coca-Cola and Heineken have committed to increasing their use of recycled glass by 50% by 2025.

Growing Alcohol and Beverage Industry

The thriving alcohol and beverage industry serves as another major driver. Premiumization trends, particularly in wine and champagne, have further amplified demand for glass bottles, which enhance product aesthetics and shelf appeal. Additionally, government incentives for local wineries and distilleries have boosted production volumes. As per the Italian Ministry of Agriculture, wine exports from Italy increased by 15% in 2022 is directly correlating with higher glass packaging consumption.

MARKET RESTRAINTS

High Production Costs

A significant restraint facing the Europe glass packaging market is the high cost of production. According to the European Manufacturing Association, the energy-intensive nature of glass manufacturing contributes to costs that are 30% higher than those of plastic alternatives. This financial burden is exacerbated by fluctuating energy prices, which have risen by 40% since 2021, as stated by Eurostat. Small- and medium-sized enterprises (SMEs) are particularly affected, as they struggle to absorb these costs while maintaining competitive pricing. A survey by the European Glass Packaging Alliance revealed that nearly 25% of SMEs consider switching to alternative materials due to cost pressures. These affordability issues create barriers to market expansion in price-sensitive regions.

Logistical Challenges

Logistical inefficiencies represent another restraint. According to the European Logistics Association, transporting glass packaging is 25% more expensive than plastic due to its weight and fragility. This challenge is pronounced in geographically dispersed regions like Eastern Europe, where infrastructure limitations increase transportation costs. Additionally, breakage rates during transit remain a concern. These logistical hurdles not only inflate operational costs but also limit accessibility in remote areas.

MARKET OPPORTUNITIES

Expansion into Pharmaceutical Applications

The pharmaceutical industry presents a significant opportunity for the Europe glass packaging market. The inert properties of glass ensure product stability is making it indispensable for sensitive medications like vaccines and injectables. For instance, the rollout of COVID-19 vaccines in Europe required over 1 billion glass vials, as per the European Medicines Agency. This surge in demand escalates the growing importance of glass packaging in pharmaceutical applications. Moreover, government investments in healthcare infrastructure are expected to further boost adoption, positioning this segment as a key growth driver.

Growing Adoption in Organic and Specialty Foods

Another major opportunity lies in the organic and specialty food segment. According to the European Organic Food Federation, the organic food market in Europe grew by 12% in 2022, with glass packaging being a preferred choice for preserving product quality and extending shelf life. Consumers associate glass with premium and natural products, driving its adoption in this niche market. For example, as per the Italian Ministry of Agriculture, organic olive oil exports from Italy increased by 20% in 2022, with glass bottles accounting for over 70% of packaging solutions.

MARKET CHALLENGES

Competition from Alternative Materials

Competition from alternative materials, such as plastics and aluminum, poses a significant challenge. This competition is particularly intense in the food and beverage sector, where manufacturers seek affordable solutions. Additionally, innovations in biodegradable plastics threaten to erode glass’s market share. A study by the European Bioplastics Association reveals that biodegradable packaging is projected to grow by 15% annually through 2030, creating a formidable rival for glass. These dynamics necessitate continuous innovation to maintain competitiveness.

Regulatory Compliance Costs

Regulatory compliance costs represent another challenge. According to the European Commission, manufacturers must adhere to stringent safety and environmental standards, which increase operational expenses. For instance, the REACH regulation mandates rigorous testing for chemical leaching that is by adding 10% to production costs, as per the European Chemicals Agency. Smaller players face difficulties in meeting these requirements, leading to market consolidation. According to a survey by the European Packaging Federation, nearly 30% of small-scale glass manufacturers have exited the market due to compliance-related challenges with the need for supportive policies.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

6.62% |

|

Segments Covered |

By Product, Application, and Region |

|

Various Analyses Covered |

Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled |

The Sherwin-Williams Company, Owen-Illinois, Inc., Amcor Limited, and RPM International Inc., and others. |

SEGMENT ANALYSIS

By Product Insights

The soda lime segment was the largest share holder in the Europe glass packaging market in 2024 owing to its versatility and cost-effectiveness by making it suitable for a wide range of applications, including beverages and food. For instance, soda lime glass accounts for over 80% of wine and spirits packaging in Europe, according to the European Spirits Organization. Key factors driving this segment include its excellent clarity and durability. Additionally, advancements in recycling technologies have enhanced its sustainability profile that will propel the growth of the market.

The borosilicate segment is anticipated to hit a fastest CAGR of 5.8% during the forecast period. The growth off the segment is fueled by its superior thermal resistance and chemical inertness by making it ideal for pharmaceutical and laboratory applications. According to the European Medicines Agency, borosilicate vials accounted for over 60% of vaccine packaging during the pandemic. Partnerships

By Application Insights

The alcoholic beverages segment dominated the Europe glass packaging market with 40.9% of share in 2024 with the high demand for premium glass bottles in wine, spirits, and champagne packaging. For instance, over 80% of spirits in Europe are packaged in glass, as stated by the Italian Ministry of Agriculture, due to its ability to enhance product aesthetics and preserve quality. Key factors driving this segment include the growing trend of premiumization and increasing exports. According to Eurostat, wine exports from France and Italy grew by 15% in 2022 is directly correlating with higher glass packaging consumption. Additionally, government incentives for local wineries have boosted production volumes by ensuring sustained dominance in the market.

The pharmaceutical segment is likely to grow with a CAGR of 6.5% during the forecast period. This growth is fueled by the rising demand for glass vials and ampoules for vaccines and injectables. According to the European Medicines Agency, over 1 billion glass vials were required during the COVID-19 pandemic. Advancements in borosilicate glass technologies have enhanced chemical resistance, driving adoption. Additionally, investments in healthcare infrastructure and the expansion of biologics have increased the need for sterile, inert packaging solutions by positioning this segment as a key growth driver.

REGIONAL ANALYSIS

Germany was the top performer in the Europe glass packaging market with 25.4% of share in 2024 with the country’s robust manufacturing base and high demand for glass in the beverage and pharmaceutical sectors. Germany’s emphasis on sustainability aligns with the EU’s Circular Economy Action Plan, driving glass adoption. For instance, as per the German Glass Packaging Association, over 70% of beer and wine produced in Germany is packaged in glass.

Turkey is expected to grow with a CAGR of 7.2% during the forecast period. This growth is fueled by rapid urbanization, increasing consumer spending, and rising exports of beverages and food products. Additionally, government-led initiatives promoting sustainable packaging have accelerated adoption, positioning Turkey as a key growth driver in the region.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Key players in the Europe glass packaging market are The Sherwin-Williams Company, Owen-Illinois, Inc., Amcor Limited, and RPM International Inc.

The Europe glass packaging market is highly competitive, characterized by the presence of global leaders and regional players vying for market share. Major companies like Saint-Gobain, Vetropack, and Ardagh dominate the landscape through continuous innovation and strategic collaborations.

Intense competition drives technological advancements, with firms focusing on developing cost-effective and scalable solutions. Regional players differentiate themselves by catering to niche segments, such as organic foods or specialty beverages. Regulatory compliance and adherence to sustainability standards further intensify competition by ensuring that only the most reliable products gain traction. As demand grows, players increasingly invest in expanding their geographic footprint and forming alliances with end-users is fostering a dynamic and evolving competitive environment.

TOP PLAYERS IN THIS MARKET

Saint-Gobain

Saint-Gobain is a leading player in the Europe glass packaging market, contributing significantly to innovations in sustainable packaging solutions. The company specializes in producing high-quality soda lime and borosilicate glass, catering to diverse applications such as beverages and pharmaceuticals. Its focus on integrating recycled materials aligns with Europe’s sustainability goals, enabling it to maintain a competitive edge.

Vetropack Holding AG

Vetropack Holding AG is another key contributor, renowned for its expertise in producing glass containers for the food and beverage industry. Vetropack’s strategic emphasis on expanding its production capacity in emerging markets has driven growth. Its presence in Europe is strengthened by partnerships with local beverage manufacturers, ensuring widespread adoption of its products.

Ardagh Group

Ardagh Group plays a pivotal role in advancing glass packaging technologies, particularly in the alcoholic beverages and pharmaceutical sectors. Ardagh has transformed the industry through its state-of-the-art facilities. Its commitment to innovation and collaboration positions it as a major player in the market, particularly in high-growth regions like the UK and Germany.

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players in the Europe glass packaging market employ strategies such as sustainability initiatives, geographic expansion, and technological advancements to strengthen their positions. Sustainability initiatives are central, with companies investing in recycling technologies to meet EU regulations. Geographic expansion is another focus, with firms targeting emerging markets like Turkey and Eastern Europe to tap into untapped potential. Technological advancements also play a crucial role. Ardagh Group has introduced lightweight glass solutions, reduced production costs and improving logistical efficiency. These strategies collectively drive market growth and ensure sustained competitiveness.

RECENT HAPPENINGS IN THE MARKET

- In April 2023, Saint-Gobain launched a new line of lightweight glass bottles in Germany by reducing material usage by 20% while maintaining durability and recyclability.

- In June 2023, Vetropack Holding AG partnered with Italian wineries to develop custom glass packaging solutions by enhancing brand differentiation and market penetration.

- In September 2023, Ardagh Group acquired a leading glass manufacturer in Turkey by strengthening its position in the fast-growing Middle Eastern market.

- In November 2023, Owens-Illinois introduced a cloud-based recycling platform in Switzerland is streamlining the collection and reuse of glass packaging materials.

- In February 2024, Gerresheimer collaborated with pharmaceutical companies in France to develop borosilicate vials for biologics is positioning itself as a leader in the pharmaceutical segment.

MARKET SEGMENTATION

This research report on the Europe glass packaging market is segmented and sub-segmented into the following categories.

By Product

- Borosilicate

- De-Alkalized Soda Lime

- Soda Lime

By Application

- Alcoholic Beverages

- Food & Beverages

- Pharmaceutical

- Beer

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What was the size of the Europe Glass Packaging Market in 2024?

The Europe Glass Packaging market was valued at USD 22.39 billion in 2024

2. What factors are driving the growth of the Europe Glass Packaging Market?

Growth drivers include advancements in glass technology, increasing demand for sustainable packaging, and rising wine consumption in Europe

3. Which regions dominate the Europe Glass Packaging Market?

Western European countries like Germany, France, and the United Kingdom lead due to strong manufacturing infrastructures and consumer demand for premium packaging.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]