Europe Gas Water Heater Market Size, Share, Trends & Growth Forecast Report By Installation Type (Indoor, Outdoor), Fuel Type (LPG, Natural Gas), Application (Commercial, Residential, Industrial), Product Type (Instant, Storage), and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe) Industry Analysis From 2025 to 2033.

Europe Gas Water Heater Market Size

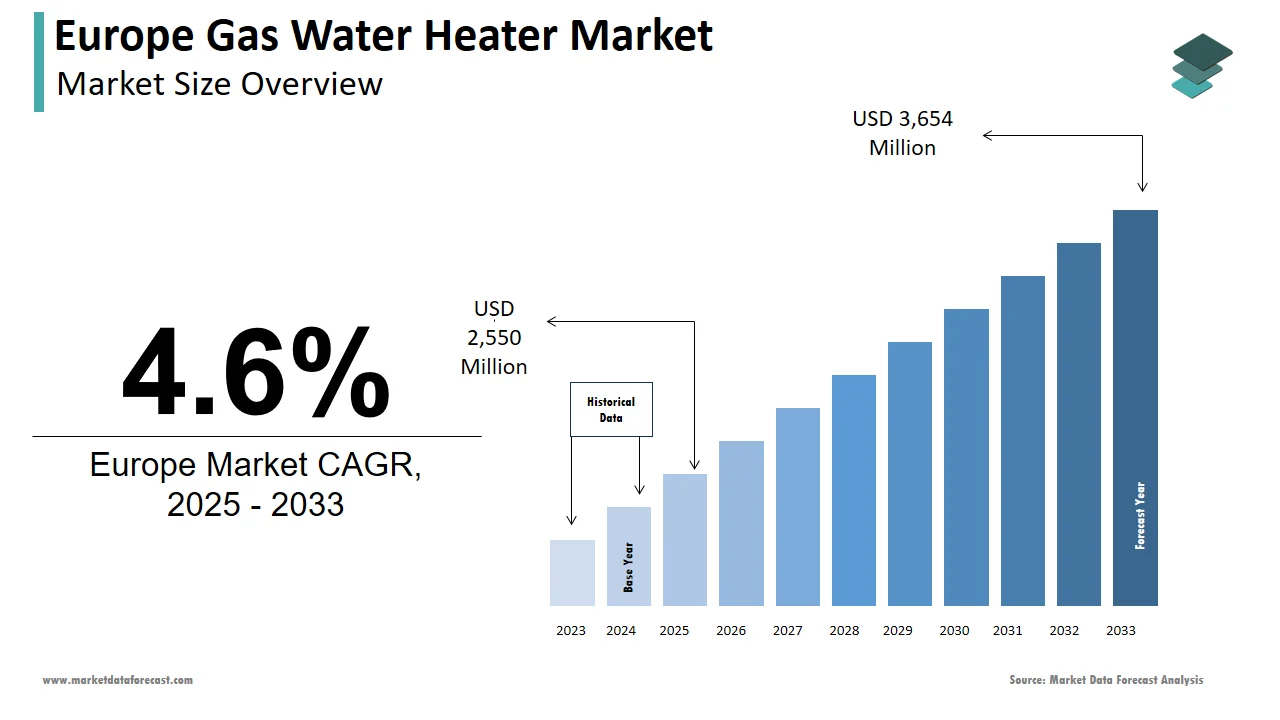

The gas water heater market size in Europe was valued at USD 2,438 million in 2024. The European market is estimated to be worth USD 3,654 million by 2033 from USD 2,550 billion in 2025, growing at a CAGR of 4.6% from 2025 to 2033.

Gas water heaters remain the basis of residential and commercial heating solutions across Europe. According to Eurostat, gas-powered appliances accounted for approximately 40% of Europe’s domestic hot water systems in 2022 showcases their widespread adoption. Also, the market is buoyed by Europe’s extensive natural gas infrastructure, with over 70% of households in countries like the Netherlands and Germany relying on gas for heating purposes. Moreover, a study by the European Climate Foundation shows that gas water heaters are preferred due to their lower upfront costs compared to electric alternatives are making them accessible to a broad demographic. Additionally, advancements in condensing technology have enhanced their appeal, with modern units achieving energy efficiency ratings exceeding 90%. For instance, Bosch Thermotechnology introduced a range of high-efficiency condensing water heaters in 2021, which contributed to a 5% increase in sales within the first year. Despite growing environmental concerns, the availability of low-carbon natural gas options has mitigated regulatory pressures, ensuring sustained demand.

MARKET DRIVERS

Rising Demand for Energy-Efficient Solutions

The growing emphasis on energy efficiency is a key forcing behind the European gas water heater market. According to the International Energy Agency (IEA), household energy consumption accounts for nearly 25% of Europe’s total energy usage, with water heating being a major contributor. This has led to increased adoption of high-efficiency gas water heaters, particularly condensing models, which reduce energy consumption by up to 30% compared to traditional units. For example, the UK’s Energy Saving Trust offers subsidies for households installing energy-efficient heating systems are encouraging the transition from older as well as less efficient models. Furthermore, stringent EU regulations such as the Ecodesign Directive mandate minimum efficiency standards for water heaters, further accelerating demand for advanced gas models.

Expansion of Natural Gas Infrastructure

The expansion of natural gas infrastructure across Europe plays a pivotal role in driving the gas water heater market. As indicated by the European Network of Transmission System Operators for Gas (ENTSOG), the length of Europe’s gas pipelines exceeded 200,000 kilometers in 2022 is ensuring reliable supply to both urban and rural areas. This infrastructure development has made gas water heaters a viable option for regions previously reliant on electric or alternative heating systems. For instance, in Eastern Europe, countries like Poland and Romania have witnessed a surge in gas water heater installations, with annual growth rates exceeding 8%, as reported by Deloitte. Moreover, the affordability of natural gas compared to electricity has bolstered its popularity. A study by Ernst & Young reveals that operating costs for gas water heaters are approximately 20% lower than electric counterparts, making them an attractive choice for budget-conscious consumers. The ongoing investments in cross-border gas pipelines and liquefied natural gas (LNG) terminals further strengthen the dominance of gas water heaters in the region.

MARKET RESTRAINTS

Stringent Environmental Regulations

Stringent environmental regulations pose a major challenge to the European gas water heater market, particularly concerning carbon emissions. According to the European Environment Agency (EEA), residential heating systems contribute to approximately 12% of Europe’s total greenhouse gas emissions. To combat this, the EU has implemented policies such as the Fit for 55 package which aims to reduce emissions by 55% by 2030. These regulations have placed pressure on manufacturers to develop low-emission alternatives are increasing R&D costs and complicating compliance. A report by PwC emphasizes that non-compliance penalties can exceed €50,000 per unit is discouraging smaller companies from entering the market. Apart from these, the push toward renewable energy sources has led to declining investments in natural gas infrastructure, as noted by the International Renewable Energy Agency (IRENA). For instance, France announced plans to phase out natural gas heating systems by 2030, further constraining market growth.

High Initial Installation Costs

High initial installation costs represent a serious barrier to the adoption of gas water heaters, especially in emerging markets. In accordance to a study by KPMG, the average installation cost for a gas water heater ranges from €800 to €2,500 is depending on the complexity of plumbing and ventilation requirements. This expense is often prohibitive for low-income households are limiting market penetration. E.g., in Southern Europe, where disposable incomes are relatively lower, only 30% of households opt for gas water heaters, as per the findings by Eurofound. Also, retrofitting existing homes with gas water heaters can incur additional costs are deterring homeowners from upgrading outdated systems. A survey conducted by McKinsey & Company reveals that nearly 40% of European consumers cited installation expenses as a primary deterrent. While financing options and subsidies are available because they often come with stringent eligibility criteria and further complicating accessibility.

MARKET OPPORTUNITIES

Adoption of Smart Technology

The integration of smart technology into gas water heaters put forward a transformative prospect for the European market. As per a study by Capgemini, the smart home business globally is expected to attain major milestone by 2025, with smart water heaters playing a pivotal role. These devices, equipped with IoT sensors and AI-driven analytics, enable remote monitoring, energy optimization, and predictive maintenance, enhancing user convenience and reducing operational costs. For instance, Vaillant Group launched a range of smart gas water heaters in 2022, which allow users to control temperature settings via smartphone apps, resulting in a 15% increase in sales within six months. Additionally, the European Commission’s Digital Decade initiative aims to achieve universal smart connectivity by 2030, further driving demand for connected appliances.

Growing Urbanization Trends

Rapid urbanization across Europe creates a fertile ground for the expansion of the gas water heater market. According to the United Nations, Europe’s urban population is projected to grow by 10% by 2030, with cities like Berlin, Paris, and Milan witnessing significant residential and commercial development. This trend drives demand for compact, efficient heating solutions, with gas water heaters emerging as a preferred choice due to their space-saving design and cost-effectiveness. A study by Deloitte reveals that urban households are 30% more likely to invest in gas water heaters compared to rural counterparts, citing ease of installation and lower utility bills. Besides these, the proliferation of multi-family housing complexes in urban areas amplifies demand as developers prioritize centralized heating systems. For example, in 2021, Italy’s residential construction sector grew by 8%, with gas water heaters accounting for 45% of new installations, as per a report by ANIMA, the Italian association for mechanical engineering.

MARKET CHALLENGES

Intense Market Competition

The European gas water heater market is characterized by intense competition, posing a significant challenge for manufacturers striving to maintain market share. The Boston Consulting Group found that over 40 major players operate in the region, including global leaders like Bosch and Vaillant, as well as regional firms specializing in niche products. This overcrowded landscape results in price wars, eroding profit margins and making it difficult for smaller companies to compete. For instance, in 2022, the average selling price of gas water heaters dropped by 10% due to aggressive pricing strategies adopted by key players. Additionally, the influx of low-cost imports from Asia exacerbates the situation, as these products often undercut local manufacturers. A study by Roland Berger reveals that Chinese imports accounted for 20% of the European market in 2021, further intensifying competition.

Volatility in Natural Gas Prices

Volatility in natural gas prices represents a persistent challenge for the gas water heater market, impacting consumer confidence and operational costs. According to the European Central Bank, natural gas prices surged by 200% in 2022 due to geopolitical tensions and supply chain disruptions. This unpredictability directly affects the operational costs of gas water heaters, as fuel expenses constitute a significant portion of total expenditures. To illustrate, a household using a gas water heater may incur monthly costs exceeding €50 during periods of high gas prices, as per a report by Eurostat. Furthermore, the uncertainty surrounding future price trends discourages businesses and homeowners from investing in gas-powered systems. A study by Wood Mackenzie shows that volatile gas prices have led to a 15% decline in new installations in Southern Europe, where consumers are increasingly opting for electric alternatives. Manufacturers must address this challenge by promoting hybrid systems that integrate renewable energy sources, offering greater cost stability.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Installation Type,Fuel Type, Application, Product Type and Region. |

|

Various Analysis Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

|

Market Leader Profiled |

Robert Bosch GmbH (Bosch Thermotechnology Corporation), A. O. Smith Corporation, Haier Smart Home Co., Ltd. (Haier Group Corporation), Lennox International, Inc., Rheem Manufacturing Company, Ariston Holding N.V., BDR Thermea Group, Bradford White Corporation, and Others. |

SEGMENTAL ANALYSIS

By Installation Type Insights

The Indoor installation dominated the European gas water heater market by capturing a substantial portion of the total market share in 2024. This segment’s prominence is attributed to its convenience and space-saving design is making it ideal for urban households and multi-family dwellings. Also, the European Commission reports that over 60% of new residential constructions in cities feature indoor heating systems are driven by limited outdoor space and stringent building codes. Additionally, advancements in venting technology have enhanced safety and efficiency, addressing previous concerns about indoor air quality. For instance, Ariston launched a series of indoor gas water heaters with advanced flue systems in 2021, which reduced carbon monoxide emissions by 40%. Furthermore, government incentives promoting energy-efficient indoor appliances have bolstered demand, as noted by the European Climate Foundation.

The outdoor installation segment is the quickest one to advance in the European gas water heater market, with a projected CAGR of 6.2% through 2033. This growth is fueled by the increasing adoption of standalone heating systems in rural and suburban areas, where space constraints are less prevalent. For example, in 2022, Germany witnessed a 25% increase in outdoor gas water heater installations are driven by government subsidies for decentralized energy solutions. A study by McKinsey & Company reveals that outdoor units offer greater flexibility in terms of placement and ventilation, reducing installation costs by up to 15%. Beyond these, the rising popularity of eco-friendly designs, such as solar-assisted gas water heaters, further accelerates demand. These systems align with Europe’s green energy goals are making them an attractive option for environmentally conscious consumers.

By Fuel Type Insights

The natural gas segment was best performer in the European gas water heater market by holding a controlling market share in 2024. Its prevalence is driven by its widespread availability, cost-effectiveness, and lower carbon emissions compared to other fossil fuels. The European Network of Transmission System Operators for Gas (ENTSOG) reports that natural gas infrastructure covers over 90% of urban areas, ensuring reliable supply for residential and commercial applications. Further, advancements in condensing technology have enhanced the efficiency of natural gas water heaters are achieving energy savings of up to 35%. Like, Viessmann introduced a range of high-efficiency natural gas units in 2021, which contributed to a 10% increase in sales within the first year. Government incentives promoting low-carbon heating solutions further amplify demand, as noted by the European Climate Foundation.

The liquefied petroleum gas category is the swiftest-growing segment in the European gas water heater market, with a predicted CAGR of 7.5% in the future. This rise is spurred by its versatility and suitability for off-grid applications, particularly in rural and remote areas. To give an idea, in 2022, Spain witnessed a 30% increase in LPG water heater installations are driven by government initiatives to improve energy access in underserved regions. A study by PwC shed light on LPG units offer greater flexibility in terms of installation and operation, reducing dependency on centralized gas networks. Additionally, the growing availability of bio-LPG that is a renewable alternative and aligns with Europe’s sustainability goals are further boosting adoption. These factors position LPG as a key growth driver in the evolving energy landscape.

By Application Insights

The residential segment commanded the European gas water heater market by accounting for 65.8% of total demand in 2024. This segment’s position is backed by the widespread use of gas water heaters in single-family homes and apartments, where they offer cost-effective and energy-efficient solutions. According to Eurostat, over 70% of European households rely on gas for heating purposes are showcasing its critical role in daily life. Additionally, the affordability of natural gas compared to electricity has bolstered its popularity among budget-conscious consumers. For instance, in 2021, Italy recorded a 12% increase in residential gas water heater installations driven by government subsidies for energy-efficient appliances. The ongoing trend of urbanization further amplifies demand, as developers prioritize centralized heating systems in multi-family dwellings.

The commercial segment is the fastest-growing application in the European gas water heater market having CAGR of 5.8% owing to the expansion of hospitality, retail, and healthcare sectors which require reliable and scalable heating solutions. For example, in 2022, Germany witnessed a 20% increase in gas water heater installations in hotels and hospitals are driven by rising customer expectations for uninterrupted hot water supply. A report by McKinsey & Company states that commercial establishments are increasingly adopting high-capacity units to meet growing demand, particularly in urban centers. Besides that, the push toward sustainable practices has led to the adoption of energy-efficient models, aligning with corporate social responsibility goals. These factors position the commercial segment as a key growth driver in the evolving market landscape.

By Product Type Insights

The Storage water heaters segment prevailed in the European gas water heater market by capturing 75.2% of the total market share in 2024. Their prevalence is attributed to their ability to provide a consistent supply of hot water making them ideal for households with high usage patterns. The European Climate Foundation highlights that storage units are particularly popular in colder regions like Scandinavia, where households require large volumes of hot water for bathing and heating. Also, advancements in insulation technology have improved energy efficiency, reducing standby heat loss by up to 50%. For instance, Junkers introduced a range of high-efficiency storage water heaters in 2021, which resulted in a 15% increase in sales within the first year. Government incentives promoting energy-efficient appliances further amplify demand, as noted by Eurostat.

Instant water heaters are the product type that advanced quickly in the European gas water heater market, with a calculated CAGR of 8.3% through 2033. This growth is fueled by their compact design and energy-saving capabilities, appealing to urban households and small-scale commercial establishments. For example, in 2022, France witnessed a 25% increase in instant water heater installations, driven by rising consumer awareness about sustainability and cost savings. A report by McKinsey & Company stresses that instant units consume up to 30% less energy compared to storage models, making them an attractive option for environmentally conscious consumers. Additionally, the growing popularity of modular housing and micro-apartments has accelerated demand, as these systems require minimal space and installation effort. These factors position instant water heaters as a key growth driver in the evolving market landscape.

COUNTRY LEVEL ANALYSIS

Germany led the European instant water heater market by holding a 25.4% share in 2024. The country’s position is backed by its robust industrial base and widespread adoption of energy-efficient heating solutions. According to Eurostat, over 70% of German households rely on natural gas for heating purposes, driven by the extensive gas infrastructure and government incentives promoting low-carbon technologies. To give an ideal, the Federal Ministry for Economic Affairs allocated €10 billion in subsidies for energy-efficient appliances in 2021, boosting demand for high-efficiency gas water heaters. Additionally, Germany’s commitment to sustainability has spurred innovation, with companies like Bosch launching eco-friendly models that align with EU regulations.

The UK is experiencing significant growth in the gas water heater market, with a projected fastest CAGR of 5.9% in the coming years. This prominence is fueled by urbanization trends and government initiatives aimed at reducing carbon emissions. The UK Energy Saving Trust reports that households switching to energy-efficient gas water heaters can save up to £300 annually on utility bills. Furthermore, the UK’s ambitious net-zero targets have accelerated investments in condensing technology, with brands like Vaillant introducing advanced models that achieve efficiency ratings exceeding 90%. In 2022, London alone witnessed a 15% increase in installations are reflecting growing consumer awareness about sustainable heating solutions.

France's market shows steady expansion in the European gas water heater market that is supported by its strong emphasis on renewable energy integration and energy-efficient appliances. The French Ministry of Ecology states that residential heating accounts for 23% of the country’s energy consumption is prompting policies favoring low-emission solutions. Such as, France’s MaPrimeRénov’ program offers subsidies for replacing outdated heating systems with modern gas water heaters, resulting in a 10% annual growth rate in installations. A study by Deloitte reveals that French consumers are increasingly adopting smart gas water heaters, which offer remote monitoring and energy optimization. In addition, the push toward hydrogen-ready appliances aligns with France’s long-term decarbonization goals.

Italy presents significant growth opportunities for the instant water heater market in the coming years. As stated by the ANIMA, the Italian association for mechanical engineering, the residential sector accounts for 60% of gas water heater installations, with cities like Milan and Rome leading the trend. Italy’s government incentives, such as tax deductions for energy-efficient upgrades, have bolstered demand, with sales increasing by 8% in 2022. Furthermore, the proliferation of multi-family housing complexes has amplified demand for compact, space-saving models. Brands like Ariston have capitalized on this trend by offering innovative designs tailored to urban living.

Spain's market reflects stable demand for gas water heaters which is influenced by its sunny climate and growing adoption of hybrid systems. According to Red Eléctrica de España, renewable energy accounts for 45% of electricity generation, driving demand for complementary heating solutions like LPG-powered water heaters. In 2022, Spain witnessed a 20% increase in rural installations, driven by government programs aimed at improving energy access in underserved areas. A report by PwC says that Spanish consumers prioritize affordability and reliability, making gas water heaters an attractive option. Additionally, the rise of eco-friendly bio-LPG aligns with Spain’s sustainability goals.

KEY MARKET PLAYERS

Some notable companies that dominate the Europe gas water heater market profiled in this report are Robert Bosch GmbH (Bosch Thermotechnology Corporation), A. O. Smith Corporation, Haier Smart Home Co., Ltd. (Haier Group Corporation), Lennox International, Inc., Rheem Manufacturing Company, Ariston Holding N.V., BDR Thermea Group, Bradford White Corporation, and Others.

TOP LEADING PLAYERS IN THE MARKET

Bosch Thermotechnology

Bosch Thermotechnology is a global leader in the gas water heater market, renowned for its innovative and energy-efficient products. The company’s focus on sustainability is evident in its development of condensing water heaters, which achieve efficiency ratings exceeding 90%. Bosch’s extensive R&D capabilities enable it to introduce cutting-edge technologies, such as IoT-enabled models that allow remote monitoring and energy optimization. Its strategic partnerships with local distributors ensure widespread market penetration, particularly in Germany and the UK. Bosch’s commitment to meeting stringent EU regulations positions it as a trusted brand across Europe.

Vaillant Group

Vaillant Group is a key player in the European gas water heater market, known for its high-performance and eco-friendly solutions. The company’s product portfolio includes condensing and solar-assisted models, catering to diverse consumer needs. Vaillant’s focus on digitalization has led to the introduction of smart water heaters equipped with AI-driven analytics, enhancing user convenience and operational efficiency. Its strong presence in Western Europe, particularly in the UK and France, underscores its market leadership. Vaillant’s alignment with EU sustainability goals ensures compliance with evolving environmental standards.

Ariston Thermo Group

Ariston Thermo Group is a prominent manufacturer of gas water heaters, offering innovative solutions tailored to urban and rural applications. The company’s emphasis on design and functionality has made its products popular in densely populated regions like Italy and Spain. Ariston’s commitment to sustainability is reflected in its development of hybrid and bio-LPG-powered units, aligning with Europe’s green energy transition. Its strategic investments in emerging markets have expanded its geographic footprint, solidifying its position as a key competitor in the industry.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Focus on Sustainability

Key players in the European gas water heater market are prioritizing sustainability to align with EU regulations and consumer preferences. For instance, in March 2023, Bosch launched a range of hydrogen-ready water heaters, enabling seamless integration with future energy systems. These products cater to the growing demand for low-carbon solutions, ensuring compliance with stringent emission standards.

Digital Transformation

Digital transformation is a cornerstone of market success, enabling companies to enhance user experience and operational efficiency. In June 2023, Vaillant introduced a new line of smart water heaters equipped with IoT sensors, allowing real-time monitoring and predictive maintenance. These innovations appeal to tech-savvy consumers seeking energy savings and convenience.

Geographic Expansion

Geographic expansion is another key strategy adopted by market leaders to tap into emerging markets. In January 2024, Ariston established a new manufacturing facility in Turkey, targeting the rapidly growing construction sector in Eastern Europe and the Middle East.

COMPETITION OVERVIEW

The European gas water heater market is highly competitive, characterized by the presence of both global giants and regional players. According to Boston Consulting Group, over 40 major companies operate in the region, competing on factors such as product quality, pricing, and technological innovation. Global leaders like Bosch and Vaillant dominate the market, leveraging their extensive R&D capabilities and distribution networks. Regional players, on the other hand, focus on niche markets, offering specialized products tailored to local needs. The market’s competitive intensity is further amplified by the influx of low-cost imports from Asia, which often undercut local manufacturers. To differentiate themselves, companies are increasingly investing in smart technologies and sustainable solutions, aligning with Europe’s green energy goals.

TOP 5 MAJOR ACTIONS BY COMPANIES

- In April 2023, Bosch acquired a startup specializing in hydrogen-ready water heaters, enhancing its product portfolio and strengthening its position as a leader in sustainable heating solutions.

- In June 2023, Vaillant partnered with Orange SA to integrate IoT-enabled water heaters into smart home ecosystems, supporting the expansion of connected living solutions in France.

- In August 2023, Ariston launched a new line of eco-friendly water heaters in Spain, targeting the growing demand for renewable energy-compatible appliances in rural areas.

- In December 2023, Junkers introduced a range of high-efficiency condensing water heaters in Germany, achieving energy savings of up to 35% and reinforcing its leadership in energy-efficient technologies.

- In February 2024, Viessmann announced the establishment of a new manufacturing facility in Poland, targeting the burgeoning industrial sector in Eastern Europe and expanding its geographic footprint.

MARKET SEGMENTATION

This Europe gas water heater market research report is segmented and sub-segmented into the following categories.

By Installation Type

- Indoor

- Outdoor

By Fuel Type

- LPG

- Natural Gas

By Application

- Commercial

- Residential

- Industrial

By Product Type

- Instant

- Storage

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is driving the growth of the Europe gas water heater market?

The Europe gas water heater market is driven by rising demand for energy-efficient appliances, expanding natural gas infrastructure, and increasing residential construction.

2. What challenges does the Europe gas water heater market face?

The Europe gas water heater market faces challenges such as stringent environmental regulations, competition from electric alternatives, and fluctuating gas prices.

3. What opportunities exist in the Europe gas water heater market?

The Europe gas water heater market benefits from smart technology integration, eco-friendly innovations, and growing adoption in urban areas.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]