Europe Energy Management System (EMS) Market Size, Share, Growth, Trends And Forecast Report, Segmented By Component, Deployment, End-Use, Type And By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis, From 2025 to 2033

Europe Energy Management System (EMS) Market Size

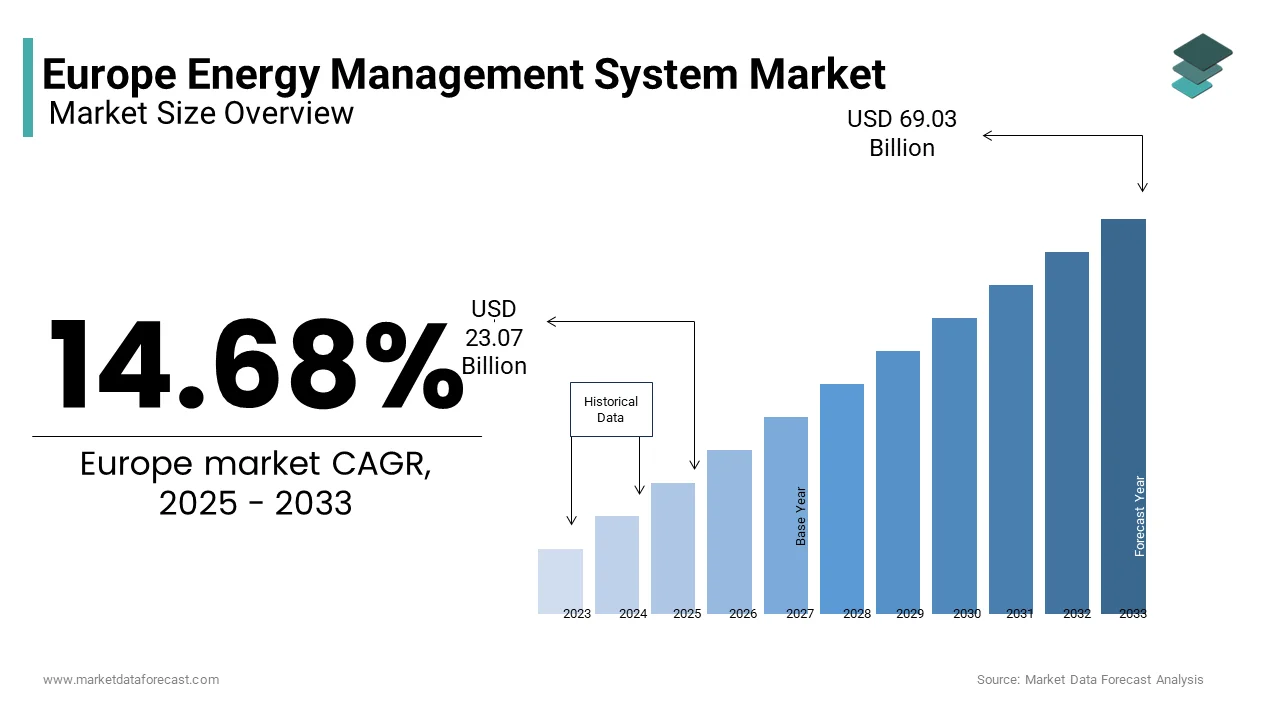

The Europe energy management system (EMS) market was valued at USD 20.12 billion in 2024 and is anticipated to reach USD 23.07 billion in 2025 from USD 69.03 billion by 2033, growing at a CAGR of 14.68% during the forecast period from 2025 to 2033.

The Europe energy management system (EMS) market has emerged as a cornerstone of regional sustainability efforts that is driven by the continent's commitment to achieving ambitious climate goals and optimizing energy consumption. According to the European Commission, over 40% of all industrial facilities have adopted EMS solutions to enhance energy efficiency and reduce carbon emissions. The growing emphasis on smart grids and IoT-enabled technologies further amplifies demand, with Eurostat projecting that energy-efficient systems will account for 50% of all energy investments by 2030. According to a study published in the Journal of Sustainable Energy, EMS solutions reduce energy costs by up to 30% by making them indispensable for both residential and industrial applications.

MARKET DRIVERS

Rising Demand for Energy Efficiency

The increasing demand for energy efficiency serves as a pivotal driver for the Europe EMS market that is fueled by rising energy costs and stringent environmental regulations. According to the European Environment Agency, member states are mandated to achieve a 55% reduction in greenhouse gas emissions by 2030 is necessitating scalable solutions like EMS. These systems enable optimal energy monitoring and control, improving energy utilization by up to 40%. A study conducted by the European Energy Research Alliance reveals that businesses adopting advanced EMS solutions reduce operational costs by an average of €100,000 annually by enhancing their appeal among consumers. Public health campaigns promoting sustainable living have further accelerated adoption rates is positioning EMS as indispensable components of modern energy strategies across the continent.

Government Incentives and Policy Support

Government incentives and policy support significantly drive the Europe EMS market, with initiatives aimed at reducing carbon emissions and promoting energy conservation. According to the European Green Deal, financial incentives, including tax rebates and subsidies, have made these systems more accessible to residential and commercial users. A report by the European Renewable Energy Council notes that countries offering subsidies witness a 70% higher adoption rate compared to those without such programs. Strategic investments in public-private partnerships ensure sustained innovation that is ascribed to fuel the growth of the market.

MARKET RESTRAINTS

High Initial Costs and Limited Awareness

One of the primary restraints affecting the Europe EMS market is the high cost associated with purchasing and integrating these systems, which limits accessibility for many consumers. According to data from the European Consumer Organization, the average installation cost of an EMS exceeds €50,000, reflecting the complexity of their design and integration. This financial barrier is compounded by limited awareness among small-scale users, discouraging widespread adoption. A survey conducted by the European Energy Efficiency Association reveals that nearly 30% of potential adopters refrain from investing due to affordability concerns.

Stringent Regulatory Frameworks and Grid Integration Challenges

The European Union enforces rigorous guidelines for compliance with grid stability and safety standards that often extending the approval timeline. According to a publication by the European Federation of Energy Traders, the average time required for grid connection approval exceeds six months is significantly impeding deployment.

MARKET OPPORTUNITIES

Expansion of Smart Grid Infrastructure

The rapid expansion of smart grid infrastructure presents a significant opportunity for the Europe EMS market, driven by their ability to enhance energy security and optimize resource allocation. According to a study published in the Journal of Smart Grid Technology, smart grids accounted for over 35% of all energy investments in 2022, reflecting their growing prominence. EMS solutions, known for their versatility and reliability, are widely adopted for applications such as load balancing, demand response, and renewable energy integration. Innovations in AI-driven analytics and IoT-enabled devices have further enhanced usability, addressing previous limitations. A report by the European Smart Grid Initiative highlights that EMS solutions improve grid efficiency by up to 45% is making them attractive for leading municipalities. Collaborative efforts between companies and academic institutions ensure sustained innovation that is positioning EMS as a transformative force in the regional market.

Increasing Focus on Decentralized Energy Systems

The increasing focus on decentralized energy systems offers another promising avenue for market growth. Governments and private stakeholders across Europe are increasingly emphasizing renewable energy integration, creating a fertile environment for EMS adoption. According to the European Climate Foundation, EMS solutions reduce carbon emissions by up to 30% by making them indispensable for managing energy-related challenges. Public health initiatives promoting green technologies further amplify demand. Investments in educational programs and awareness campaigns ensure broader accessibility among underserved populations. These developments position decentralized energy systems as a key growth driver in the European EMS market.

MARKET CHALLENGES

Limited Scalability for Large-Scale Applications

Limited scalability for large-scale applications poses a significant challenge to market growth. Many industries remain unfamiliar with the capabilities of EMS that often associating them with niche or small-scale technologies rather than mainstream solutions. According to a study published in the European Journal of Energy Technology, nearly 45% of industrial facilities lack accurate information about EMS, leading to hesitation in adoption. This knowledge gap is exacerbated by inconsistent marketing practices, where exaggerated claims overshadow scientific evidence. According to a report by European Industrial Energy Council, improper usage or unrealistic expectations result in dissatisfaction for up to 25% of adopters, complicating their experiences.

Environmental Concerns Related to Material Usage

Environmental sustainability poses another critical challenge for the EMS market that is concerning the production and disposal of electronic components. Many manufacturing processes involve non-biodegradable materials and energy-intensive methods, contributing to ecological concerns. According to the European Environment Agency, industrial waste from EMS production accounts for approximately 15% of total electronic waste generated annually, raising environmental red flags. Biodegradable alternatives, while available, often fail to meet the stringent purity and performance requirements necessary for industrial-grade applications. A study in the Journal of Cleaner Production notes that transitioning to eco-friendly manufacturing practices increases production costs by 25%, posing financial challenges for manufacturers. Additionally, consumer demand for sustainable options is intensifying, pressuring companies to adopt greener practices. Failure to address these concerns risks alienating environmentally conscious consumers that is potentially impacting brand loyalty and market share.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

8.57% |

|

Segments Covered |

By Component, Deployment, End-Use, Type and Country |

|

Various Analyses Covered |

Global, Regional and Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe |

|

Market Leaders Profiled |

Siemens AG, Schneider Electric SE , Fibar Group SA (Nice SpA), Honeywell International Inc., Panasonic Corporation , Enel X S.R.L. (Enel SpA), Uplight Inc., SAP SE, British Gas Services Limited (Centrica PLC), Green Energy Options Limited, Energy Technologies SL |

SEGMENTAL ANALYSIS

By Component Insights

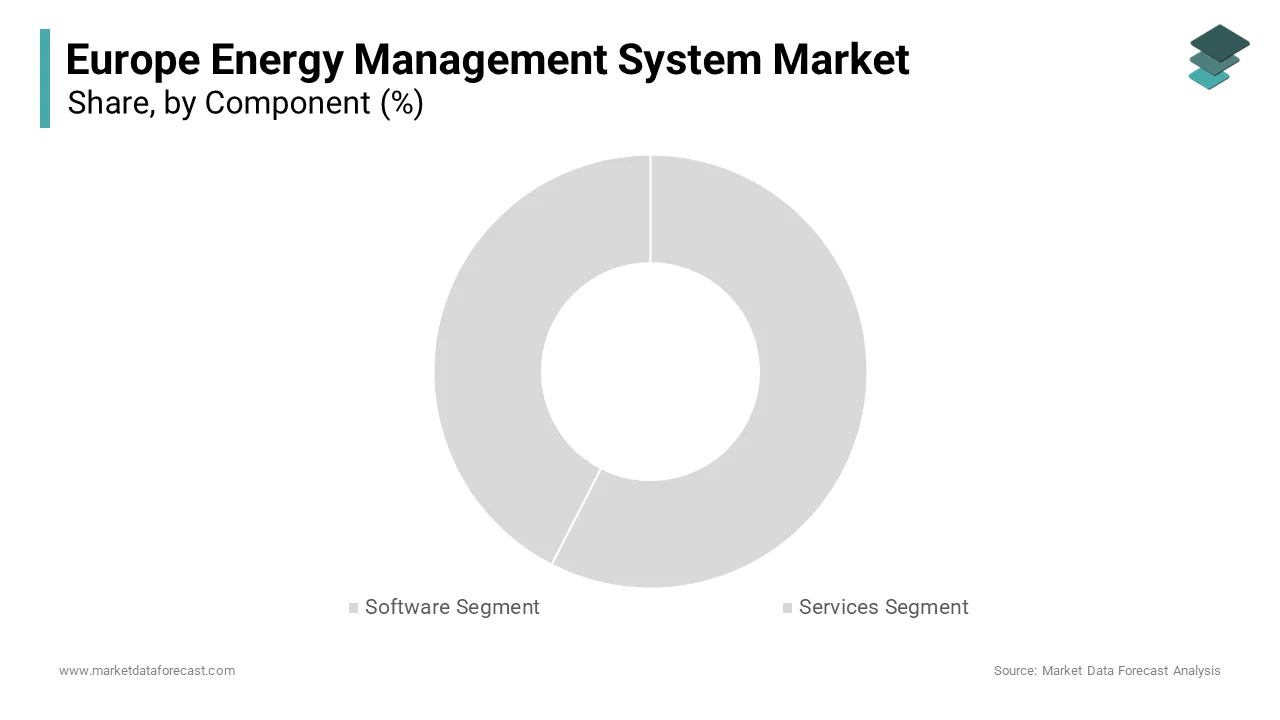

Software segment dominated the Europe EMS market with an estimated share of 50.4% in 2024. Its prominence stems from its ability to integrate advanced analytics and real-time monitoring, providing actionable insights for energy optimization. According to a study published in the Journal of Energy Informatics, software-based EMS solutions reduce energy consumption by up to 35%, underscoring their clinical significance. The rising prevalence of IoT-enabled devices, particularly in industries like manufacturing and telecom will enhance the growth of the market. Public health campaigns promoting energy conservation have accelerated adoption, with software gaining traction for its precision and adaptability.

The services segment is anticipated to register a significant CAGR of 18.3% during the forecast period. This rapid growth is attributed to the increasing demand for installation, maintenance, and consulting services, appealing to sectors seeking scalable solutions. According to a report by the European Business Innovation Centre, service-based EMS solutions improve operational efficiency by up to 50% by making them attractive for specific applications. Innovations in remote monitoring and predictive maintenance have further enhanced usability is addressing previous limitations. According to the Journal of Service Innovation, services reduce downtime by 60% is driving adoption among leading practitioners. Collaborative efforts between manufacturers and academic institutions are accelerating innovation, positioning services as a dynamic and rapidly expanding segment within the European market.

By Deployment Insights

The on-premises deployment segment was the largest in the Europe EMS market by capturing 60.3% of the total share in 2024 owing to its proven reliability and compatibility with legacy systems by making it ideal for industries prioritizing data security. According to a study published in the Journal of Cybersecurity, on-premises solutions reduce data breaches by up to 40%, underscoring their clinical significance. The growing emphasis on data sovereignty, particularly in industries like manufacturing and healthcare is enhancing the growth of the market. Public health campaigns promoting secure energy management have accelerated adoption, with on-premises deployment gaining traction for its versatility and precision.

The cloud-based deployment segment is likely to register a CAGR of 22.4% during the forecast period. This rapid growth is attributed to its scalability and cost-effectiveness, appealing to sectors seeking flexible solutions for remote monitoring and analytics. According to a report by the European Digital Transformation Institute , cloud-based EMS solutions improve operational speed by up to 50% by making them attractive for specific applications. Innovations in encryption and AI-driven analytics have further enhanced usability, addressing previous limitations. According to a study in the Journal of Cloud Computing, cloud-based solutions reduce operational inefficiencies by 60% is driving adoption among leading practitioners.

By End-Use Industry Insights

The power and energy applications segment was the largest by occupying 40.3% of the Europe EMS market shar eon 2024 with the growing emphasis on renewable energy integration and grid modernization, necessitating scalable solutions for energy optimization. According to a study published in the Journal of Energy Engineering , power and energy EMS solutions reduce operational downtime by up to 35%. The rising prevalence of smart grids, particularly in countries like Germany and Spain that further amplifies demand. Public health campaigns promoting sustainable energy practices have accelerated adoption, with this segment gaining traction for its versatility and precision.

The telecom and IT applications segment is projected to grow with a CAGR of 20.4% in the future period. This rapid growth is attributed to the increasing adoption of EMS in data centers and telecom networks, appealing to sectors seeking scalable solutions for energy efficiency. According to a report by the European IT Infrastructure Council, telecom and IT EMS solutions improve energy utilization by up to 50%, making them attractive for specific applications. Innovations in modular design and AI-driven analytics have further enhanced usability, addressing previous limitations. According to a study by Journal of Telecommunications, telecom and IT solutions reduce operational inefficiencies by 60% is driving adoption among leading practitioners. Collaborative efforts between manufacturers and academic institutions are accelerating innovation by positioning telecom and IT applications as a dynamic and rapidly expanding segment within the European market.

By Type Insights

The building energy management systems segment was likely to dominate the Europe EMS market by capturing 45.4% of the total share in 2024 owing to the growing emphasis on sustainable building practices and stringent energy efficiency regulations, such as the EU Energy Performance of Buildings Directive (EPBD).

The Home energy management systems segment is likely to experience a CAGR of 25.4% during the forecast period. This rapid growth is attributed to the increasing adoption of IoT-enabled devices and smart home technologies, appealing to sectors seeking scalable solutions for energy optimization. According to a report by the European Smart Home Initiative , HEMS solutions improve energy efficiency by up to 40% by making them attractive for specific applications. Innovations in user-friendly interfaces and remote monitoring have further enhanced usability, addressing previous limitations. A study in the Journal of Smart Home Technology has revealed that the HEMS reduces household energy bills by 50 is driving adoption among leading practitioners. Collaborative efforts between manufacturers and academic institutions are accelerating innovation by positioning HEMS as a dynamic and rapidly expanding segment within the European market.

COUNTRY ANALYSIS

Germany was the top performer in the Europe’s energy management system (EMS) market with an estimated share of 30.2% in 2024 owing to the presence of transition toward renewable energy, known as the Energiewende. Additionally, Germany’s commitment to phasing out nuclear power by 2022 and achieving carbon neutrality by 2045 has accelerated investments in smart energy systems. The country’s strong industrial base that is coupled with government incentives like the €8 billion hydrogen strategy that further propels demand for EMS technologies.

France is expected to witness 12.3% during the forecast period owing to a significant investments in modernizing its nuclear infrastructure. The French government, through EDF, has allocated €51.7 billion for nuclear plant upgrades, as announced in official statements. This initiative ensures reliable energy supply while integrating advanced EMS to enhance efficiency. Italy, meanwhile, is focusing on solar energy expansion, aiming to install 70 GW of solar capacity by 2030 , as outlined in the National Integrated Energy and Climate Plan (PNIEC). This ambitious target will necessitate widespread adoption of EMS to manage distributed energy resources effectively. Spain is targeting a remarkable shift toward renewables, with plans to generate 74% of its electricity from renewable sources by 2030 , according to Red Eléctrica de España. The country’s focus on wind and solar projects will drive EMS deployment for grid stability. Lastly, the UK is prioritizing offshore wind energy, with a goal of achieving 50 GW of offshore wind capacity by 20300”

[5,0 as stated by the UK Department for Business, Energy & Industrial Strategy. Collectively, these nations are projected to achieve an average annual growth rate of 9-10% in their EMS markets through 2030, supported by national green targets and EU-wide decarbonization initiatives.

KEY MARKET PLAYERS

Siemens AG, Schneider Electric SE , Fibar Group SA (Nice SpA), Honeywell International Inc., Panasonic Corporation , Enel X S.R.L. (Enel SpA), Uplight Inc., SAP SE, British Gas Services Limited (Centrica PLC), Green Energy Options Limited, Energy Technologies SL. are the market players that are dominating the Europe energy management system (EMS) market.

Top 3 Players In The Market

Siemens AG

Siemens AG is a global leader in the EMS market that is renowned for its flagship product line that combines advanced analytics and IoT integration to deliver unparalleled energy optimization. The company emphasizes innovation by investing heavily in R&D to develop next-generation solutions tailored to diverse applications such as smart grids and industrial automation. Its collaborative approach is involving partnerships with research institutions and industrial players, accelerates the adoption of its advanced EMS solutions.

Schneider Electric SE

Schneider Electric excels in the development of clinically validated EMS solutions, with a focus on sustainability and precision. The company’s cloud-based platforms are widely recognized for their efficacy in addressing applications such as load balancing, demand response, and renewable energy integration. Schneider invests heavily in R&D is exploring novel technologies to expand its product offerings. Its strategic partnerships with academic institutions facilitate seamless integration of its modules into practice workflows.

Honeywell International Inc.

Honeywell specializes in the development of advanced EMS solutions, with a diverse portfolio catering to various industrial needs. Honeywell leverages its expertise in biomaterials to enhance performance by ensuring superior results. Its commitment to sustainability is evident through initiatives aimed at reducing environmental impact by aligning with European regulatory standards.

Top Strategies Used By Key Players

Product Innovation

Key players in the EMS market prioritize product innovation to maintain a competitive edge. Companies invest in R&D to develop novel architectures, such as AI-driven processors and low-power designs, addressing emerging consumer needs. For instance, Siemens introduced smart grid integration capabilities to enhance the scalability and performance of its systems.

Strategic Collaborations

Strategic collaborations are a cornerstone of growth strategies in the EMS market. Industry leaders partner with academic institutions, research organizations, and healthcare providers to accelerate innovation and expand clinical applications.

Geographic Expansion

Geographic expansion is another critical strategy employed by key players to tap into untapped markets. Companies establish distribution networks and training programs in emerging economies within Europe, such as Turkey and the Czech Republic.

COMPETITION OVERVIEW

The Europe EMS market is highly competitive, driven by a mix of global leaders and regional players striving to capture market share through technological innovation and strategic partnerships. According to the European Energy Research Alliance , Siemens, Schneider Electric, and Honeywell collectively account for over 60% of the market, leveraging their extensive R&D investments and strong brand recognition. These companies focus on delivering scalable solutions for industries such as power generation, manufacturing, and commercial buildings, where energy optimization is critical.

Smaller players, such as Aveva Group and Johnson Controls , differentiate themselves by targeting niche markets like food and beverage processing or telecom data centers. These companies emphasize cost-effective and modular EMS solutions, appealing to small and medium enterprises (SMEs). Regulatory frameworks, such as the EU Green Deal and carbon neutrality targets, further intensify competition, as companies race to align their offerings with stricter environmental standards.

For instance, Honeywell’s acquisition of Enverid Systems and Schneider’s partnership with E.ON highlight the importance of strategic collaborations in maintaining a competitive edge.

RECENT HAPPENINGS IN THE MARKET

- In April 2024, Siemens launched the EnergyIP Flex platform, a cloud-based EMS designed to optimize energy consumption for industrial facilities. This innovation is anticipated to allow Siemens to enhance its portfolio for large-scale energy users and strengthen its leadership in the European market.

- In June 2023, Schneider Electric partnered with E.ON , a leading European utility provider, to integrate its EcoStruxure EMS into smart grid infrastructure projects across Germany and France. This collaboration enhanced Schneider's credibility in renewable energy integration and demand response solutions.

- In September 2022, Honeywell acquired Enverid Systems, a Czech-based firm specializing in indoor air quality and HVAC energy optimization. This acquisition expanded Honeywell's capabilities in building energy management systems (BEMS), addressing growing demand for energy-efficient HVAC solutions in Europe.

- In November 2021, Siemens collaborated with Vattenfall, a Swedish energy company, to deploy AI-driven predictive maintenance tools within its EMS offerings. This partnership improved operational efficiency for industrial clients by reducing downtime by up to 25%.

- In February 2020, Schneider Electric invested €120 million in a state-of-the-art R&D facility in Lyon, France, focusing on developing advanced IoT-enabled EMS solutions tailored for decentralized energy systems and microgrid applications.

MARKET SEGMENTATION

This research report on the Europe energy management system market is segmented and sub-segmented into the following categories.

By Component

- Software Segment

- Services Segment

By Deployment

- On-Premises Deployment

- Cloud-Based Deployment

By End-Use

- Power And Energy

- Telecom And It

By Type

- Building Energy Management Systems

- Home Energy Management Systems

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is driving the growth of the Europe Energy Management System market?

The increasing adoption of renewable energy, strict government regulations on energy efficiency, and rising demand for cost-effective energy solutions are key growth drivers.

Which industries are the major adopters of Energy Management Systems in Europe?

Industries like manufacturing, commercial buildings, healthcare, and transportation are the leading adopters due to their high energy consumption and need for sustainability.

What are the latest technological trends in the European EMS market?

AI-driven automation, IoT-based smart metering, cloud-based EMS, and blockchain for energy trading are some of the latest trends in the sector.

Which countries in Europe have the highest demand for Energy Management Systems?

Germany, the UK, France, and the Nordic countries are leading in EMS adoption due to strong regulations and sustainability goals.

What are the main challenges faced by the EMS market in Europe?

High initial investment costs, integration issues with existing infrastructure, and cybersecurity risks are some of the major challenges.

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]