Europe ePharmacy Market (Online Pharmacy Market) Size, Share, Trends & Growth Forecast Report By Product Type, Drug Type and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) Industry Analysis From 2025 to 2033.

Europe ePharmacy Market Size

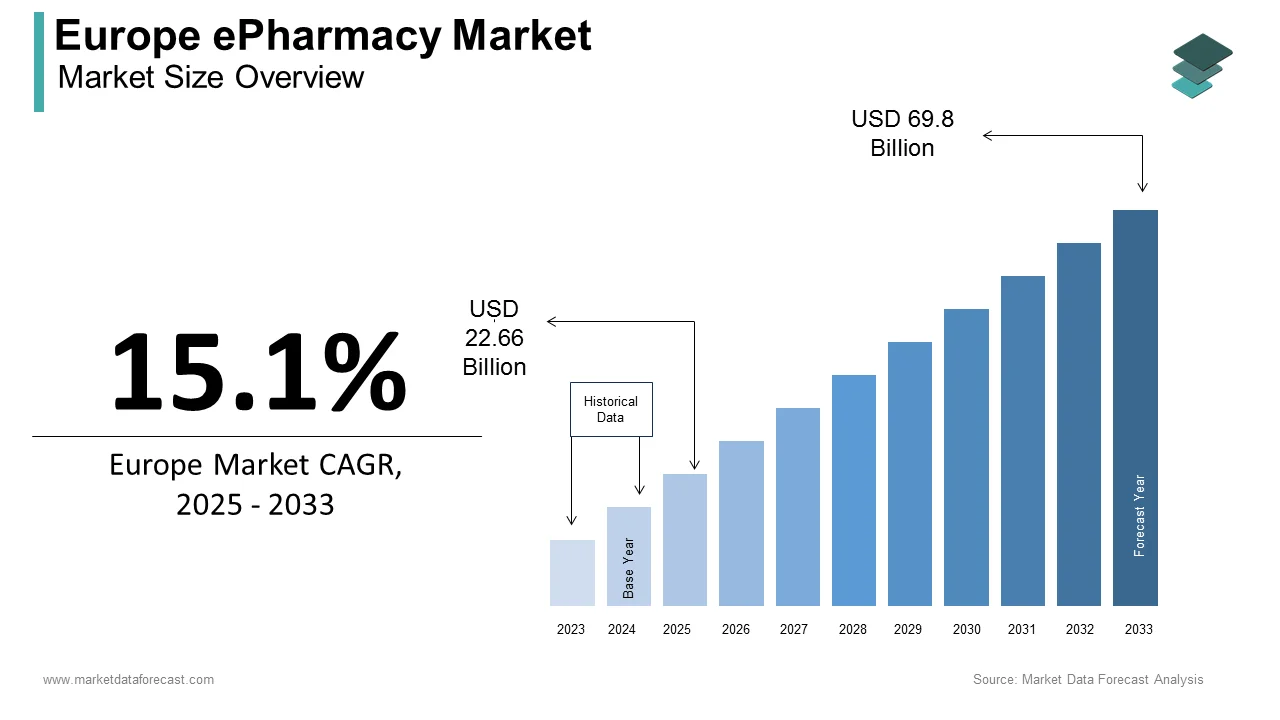

The size of the Europe ePharmacy market was valued at USD 19.7 billion in 2024. This market is expected to grow at a CAGR of 15.1% from 2025 to 2033 and be worth USD 69.8 billion by 2033 from USD 22.66 billion in 2025.

Online pharmacies have emerged as a transformative force in the healthcare sector and changed the way how consumers access medications and healthcare products. Online pharmacies, also known as e-pharmacies, are digital platforms that enable patients to purchase prescription drugs, over-the-counter medications, vitamins, and wellness products through internet-based portals. These platforms offer convenience, competitive pricing, and doorstep delivery, making them increasingly popular among tech-savvy consumers and those with limited access to traditional brick-and-mortar pharmacies. The growth of the online pharmacy market in Europe is driven by rising internet penetration, increasing prevalence of chronic diseases, and the growing demand for cost-effective healthcare solutions.

As of 2023, the European online pharmacy market is experiencing robust expansion. This growth is further fuelled by the COVID-19 pandemic, which accelerated the adoption of telemedicine and online healthcare services. According to a report by the European Federation of Pharmaceutical Industries and Associations (EFPIA), over 60% of European consumers have purchased healthcare products online at least once, citing convenience and accessibility as primary motivators. Countries like Germany, the United Kingdom, and France lead the market due to their advanced digital infrastructure and supportive regulatory frameworks.

MARKET DRIVERS

Rising Prevalence of Chronic Diseases and Aging Population in Europe

The increasing prevalence of chronic diseases and the growing aging population in Europe are majorly driving the growth of the Europe ePharmacy market growth. According to the European Centre for Disease Prevention and Control (ECDC), 70% of Europeans aged 65 and above suffer from at least one chronic condition, such as diabetes, cardiovascular diseases, or cancer, necessitating long-term medication management. This demographic shift has amplified the demand for convenient access to medications, which online pharmacies effectively address. Eurostat reports that over 20% of Europe’s population will be aged 65 or older by 2030, further driving the need for accessible healthcare solutions. Online pharmacies offer features like automated prescription refills, home delivery, and teleconsultations, catering to the needs of elderly patients and those with mobility challenges. The convenience and cost-effectiveness of these platforms make them indispensable for managing chronic conditions, thereby propelling market growth across the region.

Growing Internet Penetration and Digital Transformation in Healthcare

The rapid expansion of internet penetration and digital transformation in healthcare is another major driver of the European online pharmacy market. Eurostat highlights that 85% of households in the EU have internet access as of 2023, enabling widespread adoption of e-commerce platforms, including online pharmacies. The COVID-19 pandemic further accelerated this trend, with a report by the European Commission revealing that online healthcare consultations increased by 40% during the pandemic, fostering trust in digital health services. Additionally, advancements in mobile applications and secure payment gateways have enhanced user experience, encouraging consumers to purchase medications online. The integration of AI-driven tools for personalized recommendations and blockchain technology for drug traceability has also bolstered consumer confidence. These technological advancements, coupled with the convenience of doorstep delivery, are reshaping consumer behaviour and driving the exponential growth of the online pharmacy market in Europe.

MARKET RESTRAINTS

Stringent Regulatory Frameworks and Compliance Challenges

Stringent regulatory frameworks aimed at ensuring patient safety and preventing counterfeit drugs are primarily restraining the growth of the European ePharmacy market. The European Medicines Agency (EMA) enforces the EU Falsified Medicines Directive, which mandates drug traceability and authentication through unique identifiers and anti-tampering devices. While these measures are critical for safeguarding consumers, they impose operational complexities and high compliance costs on online pharmacies. Eurostat reports that 40% of online pharmacies face difficulties in meeting regulatory standards, particularly smaller players with limited resources. Additionally, cross-border sales of prescription medications remain restricted in many EU countries, limiting market expansion. These regulatory hurdles create barriers to entry and slow down the regional market growth, as businesses must invest heavily in compliance infrastructure while navigating fragmented national laws, which hinder the seamless operation of online pharmacy platforms across Europe.

Cybersecurity Risks and Consumer Trust Issues

Cybersecurity risks and consumer trust issues are further hindering the growth of the European ePharmacy market. The increasing reliance on digital platforms has made online pharmacies vulnerable to data breaches and cyberattacks. According to the European Union Agency for Cybersecurity (ENISA), cyberattacks on healthcare-related platforms increased by 50% between 2020 and 2023, raising concerns about the security of sensitive patient data. A survey by Eurostat reveals that only 50% of European consumers fully trust online pharmacies, citing fears of counterfeit drugs and payment fraud as primary concerns. This lack of trust is exacerbated by the presence of unregulated or illegal online pharmacies operating outside EU jurisdictions. Ensuring robust cybersecurity measures and building consumer confidence remain critical challenges, requiring significant investments in secure technologies and awareness campaigns to foster trust and ensure long-term market sustainability.

MARKET OPPORTUNITIES

Integration of Telemedicine and AI-Driven Personalization

The integration of telemedicine and AI-driven personalization is a lucrative opportunity for the European ePharmacy market. The European Commission reports that telemedicine adoption surged by 60% during the COVID-19 pandemic, creating a seamless ecosystem where patients can consult doctors and purchase medications online. Online pharmacies leveraging AI algorithms can offer personalized recommendations, such as suggesting over-the-counter products or reminding patients to refill prescriptions. A study by Eurostat highlights that 45% of European consumers prefer platforms offering tailored health solutions, underscoring the demand for personalized services. Additionally, AI-powered tools enhance operational efficiency by streamlining inventory management and predicting consumer behavior. By integrating telemedicine and AI, online pharmacies can improve customer retention, expand their service offerings, and address unmet healthcare needs, positioning themselves as comprehensive digital health hubs in Europe.

Expansion into Rural and Underserved Areas

Expanding access to rural and underserved areas are notable opportunities for the European online pharmacy market. Eurostat reports that 25% of Europe’s population resides in rural regions, where access to traditional pharmacies is often limited due to geographic and infrastructural challenges. Online pharmacies can bridge this gap by providing doorstep delivery of medications and wellness products, ensuring equitable access to healthcare. The European Federation of Pharmaceutical Industries and Associations (EFPIA) notes that 30% of rural patients face difficulties in obtaining timely medications, making online platforms a critical solution. Furthermore, government initiatives promoting digital inclusion, such as subsidies for internet access, are enhancing connectivity in remote areas. By targeting these underserved markets, online pharmacies can tap into new customer bases, drive revenue growth, and contribute to reducing healthcare disparities across Europe, fostering a more inclusive healthcare system.

MARKET CHALLENGES

Prevalence of Counterfeit Medications

Counterfeit medications is a major challenge in the European ePharmacy market. According to the European Union Intellectual Property Office (EUIPO), counterfeit pharmaceuticals cost the EU economy approximately €10 billion annually, accounting for around 4% of total pharmaceutical sales in Europe. These fake drugs often lack efficacy or may contain harmful substances, posing severe health risks to consumers. The World Health Organization (WHO) estimates that up to 10% of medicines worldwide are counterfeit, with higher rates observed in less regulated markets but still present within Europe. This alarming issue undermines consumer trust and highlights the urgent need for stricter regulations and advanced authentication technologies to combat this growing threat.

Regulatory Fragmentation Across Member States

Regulatory fragmentation across European countries is another major challenge for the European online pharmacy market. The European Medicines Agency (EMA) notes that while there is a unified framework for online pharmacies, individual member states interpret and enforce these rules differently. For example, Germany has over 30,000 registered pharmacies, yet only about 200 are authorized to sell online, reflecting stringent national controls. In contrast, other nations have more lenient policies, creating inconsistencies that complicate cross-border operations. A report by the European Commission emphasizes this disparity, suggesting that harmonization efforts could save €12 billion annually by streamlining processes and reducing administrative burdens, thereby fostering a more integrated digital health market.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Product Type, Drug Type, and Country. |

|

Various Analysis Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and Rest of Europe. |

|

Market Leader Profiled |

Wal-Mart Stores, Inc.; CVS Health; Express Scripts Holding Company; DocMorris (Zur Rose Group AG); The Kroger Co.; Walgreen Co.; Rowlands Pharmacy; OptumRx, Inc, Giant Eagle, Inc., and Others. |

SEGMENTAL ANALYSIS

By Product Type

The vitamins segment held the major share of 30.8% in the European market in 2024. The domination of vitamins segment in the European market is attributed to the rising health consciousness, with over 30% of Europeans regularly consuming supplements. The COVID-19 pandemic further amplified demand, as consumers prioritized immunity-boosting products. The segment's importance lies in its accessibility and wide range of offerings, from multivitamins to specialized supplements targeting energy and wellness. Online platforms benefit from subscription models, ensuring recurring revenue. With an aging population and increasing focus on preventive healthcare, vitamins remain pivotal in addressing nutritional gaps.

The weight loss segment is anticipated to expand at a CAGR of 7.5% over the forecast period. The obesity rates of Europe have doubled since the 1980s, with over 50% of adults overweight or obese, driving demand for weight management solutions. Rising awareness of fitness and the popularity of e-commerce platforms offering diet plans and supplements contribute to this growth. Its importance lies in addressing public health concerns while catering to consumer preferences for convenience. As lifestyle diseases rise, this segment plays a critical role in promoting healthier living through accessible online solutions.

By Drug Type

The prescription medicines segment accounted for the largest share of 60.6% in the European market in 2024. The growth of the prescription segment in the European market is driven by the rising prevalence of chronic diseases, with Eurostat estimating that over 50 million Europeans suffer from conditions like diabetes and hypertension. Strict regulatory frameworks, such as mandatory prescription verification, ensure safety and build consumer trust. Additionally, the integration of telemedicine has further boosted this segment, enabling seamless digital consultations and medication orders, making it indispensable for modern healthcare.

The OTC segment is predicted to witness the highest CAGR of 8.5% over the forecast period owing to the increasing health awareness and the convenience of purchasing non-prescription drugs online. During the COVID-19 pandemic, over 70% of consumers turned to online platforms for OTC products, as reported by Eurostat. Its importance lies in empowering consumers to self-manage minor ailments, reducing the strain on healthcare systems. The rise of preventive healthcare trends and the ease of e-commerce have positioned OTC medicines as a key driver of innovation and accessibility in the online pharmacy market.

REGIONAL ANALYSIS

Germany accounted for the dominating share of 30.9% in the European market in 2024. The dominance of Germany in the European market is driven from its advanced healthcare infrastructure, high internet penetration, and stringent regulatory frameworks ensuring consumer trust. Germany has over 30,000 registered pharmacies, with approximately 200 authorized for online sales, reflecting its structured approach to digital health. The Federal Ministry of Health emphasizes telemedicine adoption, further boosting online prescription services. Additionally, Germany's aging population drives demand for chronic disease medications, making it a pivotal player in the e-pharmacy sector.

The UK is a key player in the Europe ePharmacy market and expected to account for a promising share of the European market over the forecast period. The prominent position of the UK in the European market is driven by its tech-savvy population, with 96% of adults using the internet regularly, enabling seamless online transactions. The National Health Service (NHS) supports telemedicine initiatives, which have expanded access to prescription medicines. Post-Brexit, the UK has streamlined its digital health regulations, encouraging innovation in online pharmacy platforms. Its strategic focus on preventive healthcare and self-medication trends has solidified its position as a key contributor to the European online pharmacy market.

France is predicted to register a prominent CAGR in the European market over the forecast period. France's success is driven by its strong emphasis on skincare and OTC products, aligning with consumer preferences for wellness and beauty solutions. The French government has implemented supportive policies for telehealth, enabling easier access to online prescriptions. With 85% of the population actively using e-commerce platforms, France benefits from a digitally connected populace. Furthermore, the growing prevalence of chronic diseases and the convenience of home delivery for medications have positioned France as a critical hub for online pharmacy growth in Europe.

KEY MARKET PLAYERS

Companies playing a leading role in the Europe ePharmacy market and are profiled in the report include Wal-Mart Stores, Inc.; CVS Health; Express Scripts Holding Company; DocMorris (Zur Rose Group AG); The Kroger Co.; Walgreen Co.; Rowlands Pharmacy; OptumRx, Inc, Giant Eagle, Inc., and Others.

MARKET SEGMENTATION

This Europe ePharmacy market research report is segmented and sub-segmented into the following categories.

By Product Type

- Skin Care

- Cold and Flu

- Vitamin

- Dental Care

- Weight Loss

- Others

By Drug Type

- Prescription Drugs

- Over The Counter (OTC)

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the growth rate of the Europe ePharmacy market?

The Europe ePharmacy market is projected to grow at a CAGR of 15.1%, reaching USD 69.8 billion by 2033.

2. What drives the Europe ePharmacy market?

The Europe ePharmacy market is fueled by chronic diseases, aging populations, and digital healthcare adoption.

3. What are the key challenges in the Europe ePharmacy market?

The Europe ePharmacy market faces regulatory hurdles, counterfeit drug risks, and cybersecurity concerns.

4. How is AI impacting the Europe ePharmacy market?

The Europe ePharmacy market benefits from AI-driven personalization, automated prescriptions, and fraud detection.

5. What opportunities exist in the Europe ePharmacy market?

The Europe ePharmacy market can expand via telemedicine integration and reaching underserved rural areas.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com