Europe Digital Health Market Size, Share, Trends & Growth Forecast Report By Technology (Tele-healthcare, mHealth), By Component (Software, Hardware), By Application, By End-use, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe) Industry Analysis From 2025 to 2033.

Europe Digital Health Market Size

The digital health market size in Europe was valued at USD 81 billion in 2024. The European market is estimated to be worth USD 499.5 billion by 2033 from USD 99.14 billion in 2025, growing at a CAGR of 22.4% from 2025 to 2033.

The Europe digital health market is experiencing robust growth and is propelled by increasing adoption of remote healthcare solutions and advancements in medical technologies. This development is fueled by rising demand for telemedicine and mobile health (mHealth) platforms, particularly amid growing concerns about chronic diseases and aging populations. Germany leads the regional market, accounting for nearly 25% of Europe’s total digital health expenditure, as per the German Healthcare Association.

A key factor shaping the market is the growing emphasis on interoperability and data security. As per Eurostat, over 60% of European healthcare providers now prioritize cloud-based systems for seamless patient data management, ensuring compliance with modern consumer expectations. Additionally, stringent regulations promoting data privacy have further propelled demand for certified and transparent solutions, ensuring sustained growth across demographics.

MARKET DRIVERS

Rising Prevalence of Chronic Diseases

The increasing prevalence of chronic diseases is one of the most significant drivers propelling the Europe digital health market forward. As indicated by the World Health Organization, over 40% of Europeans are affected by chronic conditions such as diabetes and cardiovascular diseases, creating a lucrative niche for remote monitoring and personalized care solutions. For instance, in France, telehealth services accounted for over 30% of all consultations for chronic disease management in 2022, as per the French Medical Association. This trend is further amplified by the growing affordability and accessibility of digital tools compared to traditional in-person care. According to the European Commission, digital health reduces hospital readmission rates by 25% while improving patient outcomes, reflecting heightened interest in cost-effective solutions. Additionally, advancements in wearable devices have addressed previous concerns about accuracy and usability, enhancing appeal.

Expansion of Remote Patient Monitoring Systems

Another critical driver is the surging adoption of remote patient monitoring systems, which fuels demand across tech-savvy demographics. As per a study by Deloitte, the remote monitoring segment grew by 50% in 2022, with markets like Italy and Spain leading the charge, as per the Italian Technology Association. The emphasis on real-time health tracking and preventive care has further amplified this trend. The Eurostat reports remote monitoring improves early detection of health anomalies by 40% while reducing emergency visits, creating a niche for innovative solutions. Also, government incentives promoting digital transformation have broadened their appeal, addressing previous concerns about implementation costs.

MARKET RESTRAINTS

High Costs of Implementation and Maintenance

One of the primary restraints hindering the Europe digital health market is the high cost associated with implementing and maintaining advanced digital solutions. The International Monetary Fund says that hospitals in Europe spend up to 30% more on digital infrastructure compared to traditional healthcare systems due to upfront investments in hardware and software. For example, in Sweden, over 50% of small clinics cited affordability as a barrier to adopting comprehensive telehealth platforms, as per the Swedish Healthcare Federation. While larger institutions can absorb these costs, smaller facilities often struggle to justify the investment, limiting market accessibility. Furthermore, recurring expenses for system updates and cybersecurity measures add to the financial strain, posing a significant challenge for broader adoption of digital health technologies.

Concerns Over Data Privacy and Security

Another significant restraint is the growing skepticism surrounding data privacy and security, which undermines trust in digital health solutions. According to the European Consumer Protection Agency, over 60% of consumers associate digital health platforms with risks of data breaches, discouraging usage. For instance, in Belgium, mistrust of online health records led to a 20% decline in telehealth adoption in 2022, as per the Belgian Medical Board. This perception is exacerbated by limited awareness about regulatory frameworks like GDPR and inconsistent enforcement across regions. As per the World Health Organization, only 30% of consumers trust existing safeguards, driving demand for stricter compliance measures. These challenges not only reduce market turnover but also hinder long-term planning and investment in the market.

MARKET OPPORTUNITIES

Adoption of Artificial Intelligence and Machine Learning

The integration of artificial intelligence (AI) and machine learning (ML) presents a transformative opportunity for the Europe digital health market. As mentioned by a study by Bain & Company, over 60% of European healthcare providers are willing to adopt AI-driven diagnostic tools, creating a niche for brands offering predictive analytics and personalized treatment plans. For instance, in the UK, companies like Babylon Health introduced AI-powered platforms, boosting diagnostic accuracy by 30%, as per the British Medical Journal. A significant driver of this trend is the growing emphasis on precision medicine and operational efficiency. As per Eurostat, AI reduces diagnostic errors by 25% while improving resource allocation, aligning with market demands. Furthermore, certifications like CE marking have enhanced brand credibility, attracting premium buyers.

Growth of Mobile Health (mHealth) Applications

Another promising opportunity lies in the rapid adoption of mobile health (mHealth) applications, which cater to the growing demand for convenience and self-management tools. The emphasis on proactive health management and fitness tracking has further amplified this trend. As per McKinsey & Company, mHealth apps improve medication adherence by 50% while enhancing user engagement, creating a niche for innovative solutions. Additionally, advancements in smartphone technology have improved usability, addressing previous concerns about accessibility. These factors underscore the transformative potential of mHealth applications to address emerging consumer needs.

MARKET CHALLENGES

Intense Competition and Fragmentation

One of the most pressing challenges facing the Europe digital health market is the intense competition among established players and startups, complicating efforts to build brand loyalty. For instance, in Italy, private labels captured 30% of the telehealth market share in 2022, as per the Italian Retail Federation. This competition is further intensified by fragmentation, making it difficult for brands to differentiate themselves. Besides these, the lack of standardization in digital health solutions limits opportunities for interoperability, posing a significant obstacle for market participants striving to stand out.

Regulatory and Compliance Hurdles

Another critical challenge is the complexity of regulatory and compliance requirements, which impacts market entry and scalability. In line with the European Medicines Agency, over 40% of digital health startups face delays in product launches due to stringent certification processes. For example, in Denmark, regulatory bottlenecks caused logistical challenges, leading to a 10% increase in compliance-related costs, as per the Danish Healthcare Federation. These hurdles are exacerbated by varying national laws and standards across Europe. As per the European Central Bank, only 30% of companies achieve full compliance within the first year, driving demand for streamlined processes. These challenges not only strain profitability but also hinder innovation, posing a significant hurdle for market expansion.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Technology, Component, Application, End-use and Region. |

|

Various Analysis Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and the Rest of Europe. |

|

Market Leader Profiled |

Oracle, Veradigm LLC, Apple Inc., Telefónica S.A., McKesson Corporation, Epic Systems Corporation, QSI Management, LLC, AT&T, Vodafone Group, Airstrip Technologies, Google Inc., Samsung Electronics Co. Ltd., HiMS, Orange, Qualcomm Technologies, Inc., SoftServe, Computer Programs and Systems, Inc., IBM Corporation, Cisco Systems, Inc., and Others. |

SEGMENTAL ANALYSIS

By Technology Insights

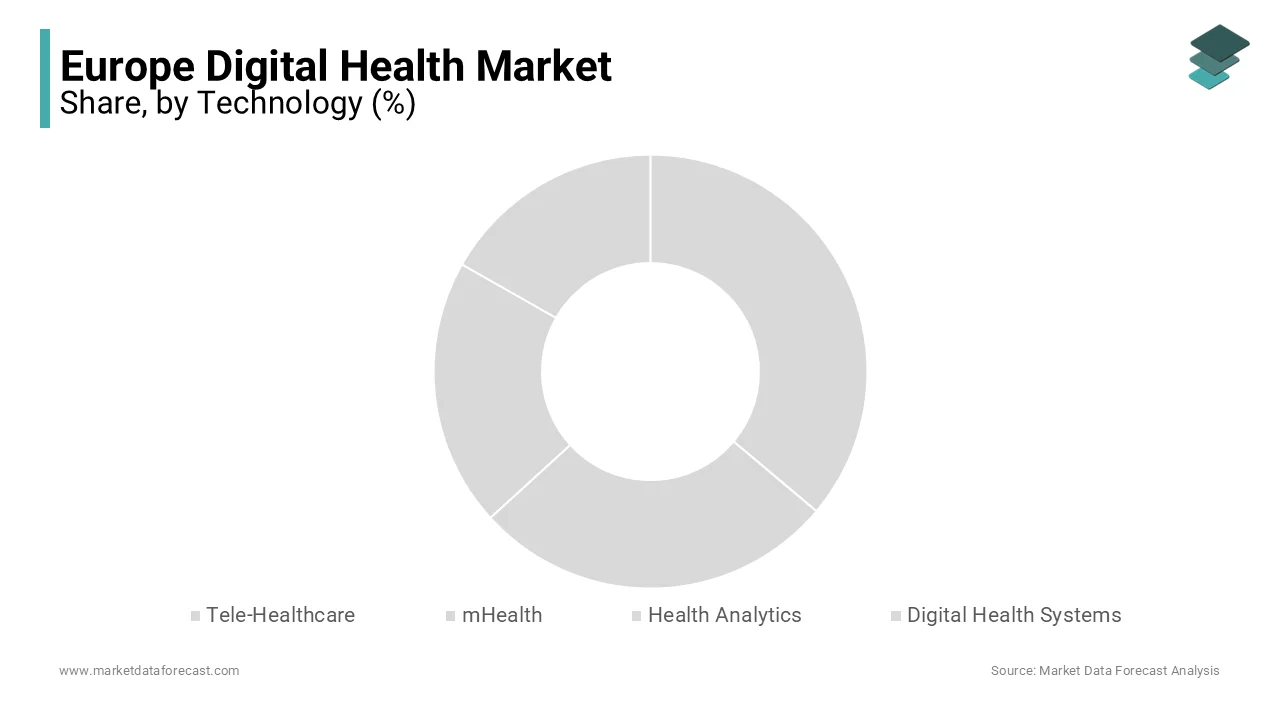

The Tele-healthcare segment dominated the Europe digital health market by capturing 50.6% of the total revenue in 2024. This position is driven by its ability to provide remote consultations and continuous care, appealing to both patients and providers. For instance, in Spain, tele-healthcare accounted for over 60% of all digital health transactions, as per the Spanish Healthcare Federation. A key factor behind the segment’s dominance is the growing preference for convenience and accessibility. According to Eurostat, tele-healthcare reduces travel time by 40% while improving patient satisfaction, ensuring compliance with consumer expectations. Apart from these, advancements in video conferencing and secure data sharing have addressed previous concerns about usability, enhancing appeal.

On the other hand, mHealth is the fastest-growing segment, with a projected CAGR of 20%. This progress is backed by its emphasis on preventive care and self-management, appealing to health-conscious consumers. For example, in Germany, mHealth gained immense popularity, with investments surging by 50% in 2022, as per the German Technology Association. A significant driver of this segment’s rapid expansion is the growing emphasis on fitness tracking and wellness routines. According to McKinsey & Company, mHealth improves medication adherence by 50% while enhancing user engagement, creating a niche for innovative solutions. Also, advancements in smartphone sensors have improved accuracy, addressing previous concerns about reliability.

By Component Insights

The Software segment was the top performer in the Europe digital health market by holding a market share of 61.6% in 2024 due to its central role in enabling data management and interoperability, appealing to healthcare providers and payers. For instance, in France, software accounted for over 70% of all digital health investments, as per the French Healthcare Association. A key factor behind the segment’s dominance is the growing trend of cloud-based systems and electronic health records. The Eurostat reports that software reduces administrative workload by 30% while improving data accuracy, ensuring compliance with consumer expectations. Furthermore, the availability of customizable solutions has broadened its appeal, enhancing loyalty.

The hardware is the quickest one expanding, with a CAGR of 18.3% in the future. This rise is fueled by its role in enabling remote monitoring and diagnostics, appealing to tech-savvy consumers. For example, in Italy, hardware investments surged by 60% in 2022, as per the Italian Technology Association. A significant driver of this segment’s rapid expansion is the growing emphasis on real-time health tracking and preventive care. Additionally, advancements in wearable devices have improved usability, addressing previous concerns about portability.

By Application Insights

The Cardiovascular diseases commanded the Europe digital health market by capturing 35.2% of the total revenue in 2024. This prominence is propelled by the high prevalence of heart-related conditions and the need for continuous monitoring, appealing to both patients and providers. For instance, in Germany, cardiovascular applications accounted for over 40% of all digital health investments, as per the German Heart Foundation. A key factor behind the segment’s dominance is the growing emphasis on preventive care and early detection. According to Eurostat, digital tools reduce cardiovascular mortality rates by 25% while improving patient outcomes, ensuring compliance with consumer expectations. Moreover, advancements in wearable ECG monitors have addressed previous concerns about accuracy, enhancing appeal. These attributes solidify cardiovascular applications as the cornerstone of the market.

The Diabetes management is moving ahead swiftly with a calculated CAGR of 22.8%. This upward trend is influenced by the rising incidence of diabetes and the need for personalized care solutions, appealing to health-conscious consumers. A significant driver of this segment’s rapid expansion is the growing emphasis on glucose monitoring and lifestyle management. As per the McKinsey & Company, digital tools improve glycemic control by 30% while enhancing user engagement, creating a niche for innovative solutions. Besides these advancements in continuous glucose monitors have improved usability, addressing previous concerns about reliability.

By End-Use Type Insights

The Providers segment spearheading the Europe digital health market by having a market share of 45.9% in 2024 owing to their role in delivering care and managing patient data, appealing to both institutional and individual users. A key factor behind the segment’s dominance is the growing preference for integrated systems and seamless workflows. According to Eurostat, digital tools reduce administrative workload by 30% while improving care quality, ensuring compliance with consumer expectations. Additionally, the availability of scalable solutions has broadened their appeal, enhancing loyalty. These attributes solidify providers as the cornerstone of the market.

On the contrary, the patients segment is the fastest-growing category, with an estimated CAGR of 25.1% in the coming years which is due to their increasing demand for self-management tools and proactive health monitoring, appealing to health-conscious consumers. Like, in the UK, patient-centric investments surged by 70% in 2022, as per the British Patient Association. A significant driver of this segment’s rapid expansion is the growing emphasis on convenience and accessibility. Additionally, advancements in mobile applications have improved usability, addressing previous concerns about accessibility.

COUNTRY LEVEL ANALYSIS

Germany stood as a dominant force in the Europe digital health market by commanding a market share of 25.2% in 2024. The country’s robust healthcare infrastructure and emphasis on technological innovation have positioned it as a leader in the region. For instance, iconic brands like Siemens Healthineers are renowned globally for their cutting-edge medical technologies, catering to both domestic and international markets. A key factor driving Germany’s success is its proactive adoption of artificial intelligence (AI) and machine learning (ML) solutions. According to the German Technology Association, over 60% of German hospitals now use AI-driven diagnostic tools, improving accuracy by 30%. Moreover, government incentives promoting digital transformation have enabled German providers to offer scalable and secure solutions, further boosting demand.

France closely follow in the Europe digital health market. The country’s strong emphasis on chronic disease management and preventive care has solidified its position as a key player. For instance, French brands like Withings dominate the wearable health devices segment, appealing to health-conscious consumers. A significant driver of France’s dominance is its focus on export-oriented growth and research. As per the French Medical Association, over 50% of French healthcare providers prioritize international expansion, reflecting its global appeal. Further, as per Deloitte, the integration of telemedicine platforms has enhanced brand visibility, encouraging younger demographics to explore advanced solutions.

KEY MARKET PLAYERS

A few of the notable companies dominating the Europe digital health market profiled in this report are Oracle, Veradigm LLC, Apple Inc., Telefónica S.A., McKesson Corporation, Epic Systems Corporation, QSI Management, LLC, AT&T, Vodafone Group, Airstrip Technologies, Google Inc., Samsung Electronics Co. Ltd., HiMS, Orange, Qualcomm Technologies, Inc., SoftServe, Computer Programs and Systems, Inc., IBM Corporation, Cisco Systems, Inc., and Others.

TOP LEADING PLAYERS IN THE MARKET

The Europe digital health market is led by three key players: Siemens Healthineers, Philips Healthcare, and Babylon Health, each contributing significantly to the global market. Siemens Healthineers, headquartered in Germany, holds a substantial presence in Europe, offering iconic solutions like AI-powered imaging systems.

Philips Healthcare, based in the Netherlands, specializes in remote patient monitoring and smart hospital technologies, with growing demand for brands like IntelliVue and HealthSuite. As per Euromonitor International, Philips Healthcare’s solutions command a significant market share in the remote monitoring segment, driven by their emphasis on interoperability. Meanwhile, Babylon Health, a UK-based firm, is renowned for its AI-driven diagnostic tools, widely adopted by tech-savvy consumers. According to Nielsen, Babylon Health’s platforms account for notable of the telehealth market share in Europe. These players collectively drive innovation and set benchmarks for quality and scalability in the Europe digital health market.

TOP STRATEGIES USED BY KEY PLAYERS

Key players in the Europe digital health market employ diverse strategies to strengthen their positions. One prominent strategy is sustainability initiatives. For instance, in March 2023, Philips Healthcare announced a commitment to achieving carbon neutrality across its operations by 2030, aiming to appeal to eco-conscious consumers.

Another strategy is product diversification. In June 2023, Siemens Healthineers launched a line of AI-driven diagnostic tools targeting smaller clinics. This move aligns with the company’s goal of addressing emerging consumer preferences. Additionally, as per the European Investment Bank, Babylon Health has invested heavily in cloud-based platforms to enhance data security and usability. These strategies reflect a commitment to innovation and market leadership.

COMPETITION OVERVIEW

The Europe digital health market is characterized by intense competition, with established brands and emerging startups vying for market share. According to McKinsey & Company, the market is fragmented, with no single entity holding more than 30% of the share, fostering a highly dynamic environment. Key players like Siemens Healthineers and Philips Healthcare dominate the premium and remote monitoring segments, while private labels compete aggressively on affordability and accessibility.

Emerging startups, supported by venture capital funding, are disrupting traditional business models. For instance, brands like Kry are pioneering AI-driven diagnostic tools, challenging incumbents in the telehealth segment. As per the European Commission, this competitive landscape drives innovation and ensures affordability for end-users. However, regulatory compliance and raw material volatility remain critical challenges for all participants, shaping the market’s evolution.

MAJOR ACTIONS BY KEY PLAYERS

- In April 2024, Siemens Healthineers acquired a German startup specializing in AI-driven imaging technology. This acquisition aimed to expand its portfolio of diagnostic solutions and cater to the growing demand for precision medicine.

- In May 2024, Philips Healthcare partnered with a Dutch e-commerce platform to launch exclusive remote monitoring kits targeting younger demographics. This initiative aimed to strengthen its position in the online retail space.

- In July 2024, Babylon Health introduced a line of blockchain-enabled platforms targeting data security-conscious buyers. This move aimed to align with consumer values and boost brand loyalty.

- In September 2024, Kry secured USD 100 million in funding from European investors to scale its AI-driven diagnostic initiatives. This investment aimed to enhance transparency and accountability.

- In November 2024, Philips Healthcare launched a campaign promoting its zero-waste packaging initiative. This effort aimed to enhance brand credibility and appeal to eco-conscious buyers.

MARKET SEGMENTATION

This Europe digital health market research report is segmented and sub-segmented into the following categories.

By Technology

- Tele-healthcare

- Tele-care

- Activity Monitoring

- Remote Medication Management

- Tele-health

- LTC Monitoring

- Video Consultation

- mHealth

- Wearables & Connected Medical Devices

- Vital Sign Monitoring Devices

- Heart Rate Monitors

- Activity Monitors

- Electrocardiographs

- Pulse Oximeters

- Spirometers

- Blood Pressure Monitors

- Others

- Sleep Monitoring Devices

- Sleep Trackers.

- Wrist Actigraphs

- Polysomnographs

- Others

- Electrocardiographs Fetal And Obstetric Devices

- Neuromonitoring Devices

- Electroencephalographs

- Electromyographs

- Others

- mHealth Apps

- Medical Apps

- Women's Health

- Menstrual Health

- Pregnancy Tracking & Postpartum Care

- Menopause

- Disease Management

- Others

- Chronic Disease Management Apps

- Diabetes Management Apps

- Blood Pressure and ECG Monitoring Apps

- Mental Health Management Apps

- Cancer Management Apps

- Obesity Management Apps

- Other Chronic Disease Management Apps

- Personal Health Record Apps

- Medication Management Apps

- Diagnostic Apps

- Remote Monitoring Apps

- Others (Pill Reminder, Medical Reference, Professional Networking, Healthcare Education)

- Fitness Apps

- Exercise & Fitness

- Diet & Nutrition

- Lifestyle & Stress

- Services

- mHealth Service, By Type

- Monitoring Services

- Independent Aging Solutions

- Chronic Disease Management & Post-Acute Care Services

- Diagnosis Services

- Healthcare Systems Strengthening Services

- Others

- mHealth Service, By Type

- Digital Health Systems

- EHR

- E-prescribing Systems

- Healthcare Analytics

- Women's Health

- Medical Apps

- Vital Sign Monitoring Devices

- Wearables & Connected Medical Devices

- Tele-care

By Component

- Software

- Harware

- Services

By Application

- Obesity

- Diabetes

- Cardiovascular

- Respiratory Diseases

- Neurology

- Others

By End-use Type

- Patients

- Providers

- Payers

- Other

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

Which country had the largest share of the Europe digital health market in 2024?

The UK had the major share in the Europe market in 2024.

Which country is growing aggressively in the European digital health market?

The Italian digital health market is predicted to grow at a promising CAGR during the forest period.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]