Europe Dermal Fillers Market Size, Share, Trends & Growth Forecast Report By Product (Absorbable or Biodegradable, Non-Absorbable or Non-Biodegradable), Therapeutic Area, Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033

Europe Dermal Fillers Market Size

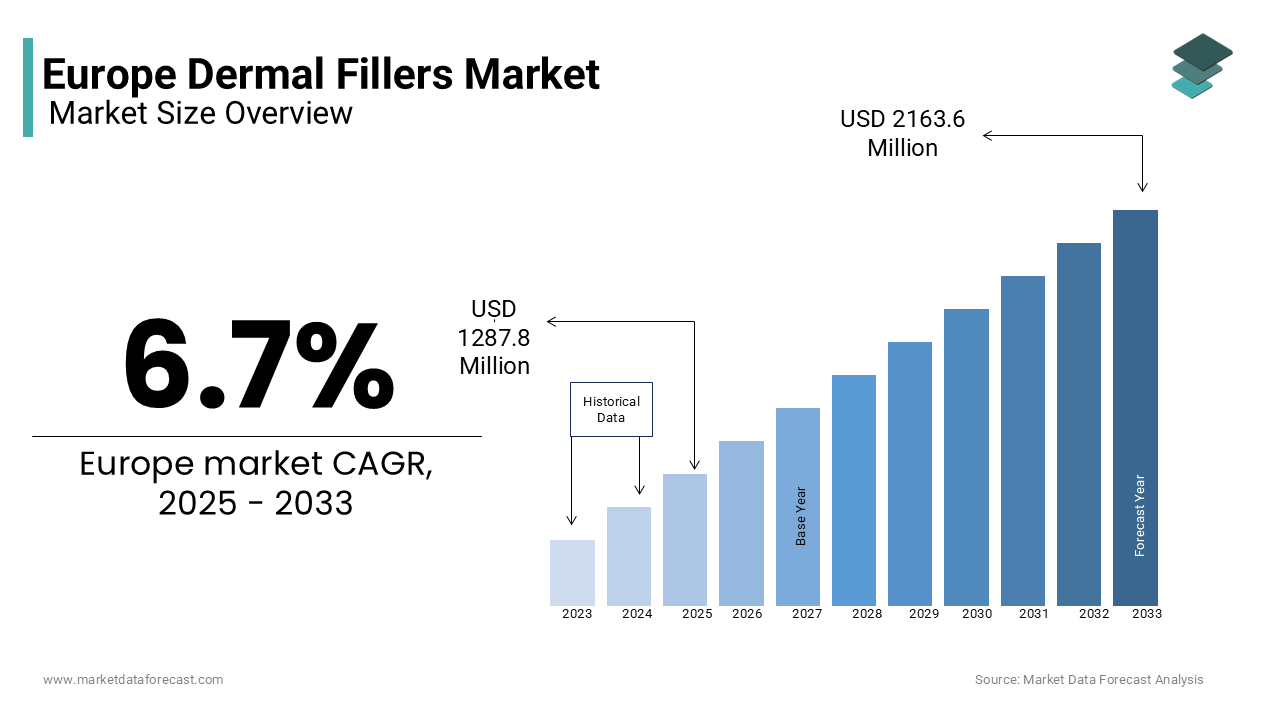

The dermal fillers market size in Europe was valued at USD 1207 million in 2024. The European market is estimated to grow at a CAGR of 6.7% from 2025 to 2033 and be worth USD 2163.65 Mn by 2033 from USD 1287.87 Mn in 2025.

The Europe dermal fillers market has firmly established itself as a cornerstone of the aesthetic and anti-aging industries, driven by an increasing emphasis on non-invasive beauty solutions and preventive skincare. According to the European Society of Dermatology, over 60% of adults aged 35 and above express interest in treatments targeting visible signs of aging, such as wrinkles and sagging skin is fueling with steady market expansion. The rising prevalence of chronic skin conditions, including acne scars and photoaging, further amplifies demand for advanced dermal filler formulations. As per data from the European Aesthetic Medicine Association, hyaluronic acid-based fillers account for nearly 70% of all non-surgical cosmetic procedures performed annually in Europe. Innovations in biocompatible materials and minimally invasive techniques have revolutionized patient outcomes, with a study published in the Journal of Cosmetic Dermatology, absorbable fillers reduce recovery time by up to 40%. Despite these advancements, challenges persist, including high costs and limited accessibility in rural areas. However, supportive government initiatives promoting healthy lifestyles and strategic investments in R&D continue to propel the market forward is ensuring its pivotal role in shaping modern aesthetics across Europe.

MARKET DRIVERS

Rising Demand for Non-Invasive Anti-Aging Solutions

The growing preference for non-invasive anti-aging solutions serves as a pivotal driver for the Europe dermal fillers market that is fueled by an aging population and increasing consumer focus on maintaining youthful appearances. According to Eurostat, individuals aged 65 and above account for approximately 20% of the European population, a figure projected to rise to 30% by 2050. This demographic shift amplifies demand for products targeting visible signs of aging, such as fine lines, wrinkles, and volume loss. According to the European Dermatological Forum, hyaluronic acid-based fillers improve skin elasticity by up to 50% is making them indispensable tools for combating age-related concerns. Public health campaigns promoting early intervention in skincare have further accelerated adoption rates.

Increasing Emphasis on Preventive Skincare

The increasing emphasis on preventive skincare significantly drives the Europe dermal fillers market, as consumers gravitate toward proactive measures to maintain skin health and appearance. Chronic exposure to environmental factors like pollution and UV radiation has led to a surge in skin-related concerns, including photoaging and pigmentation disorders. According to the European Skin Foundation, over 40% of adults incorporate aesthetic treatments into their skincare routines to combat these issues. Hyaluronic acid-based fillers is known for their ability to hydrate and rejuvenate skin are widely adopted for their efficacy in reducing visible signs of aging. A study published in the British Journal of Dermatology reveals that preventive use of dermal fillers reduces wrinkle depth by up to 35%, enhancing their appeal among younger demographics. Strategic investments in educational campaigns ensure broader accessibility, particularly among underserved populations is reinforcing the market's growth trajectory.

MARKET RESTRAINTS

High Costs and Limited Accessibility

One of the primary restraints affecting the Europe dermal fillers market is the high cost associated with procedures, which limits accessibility for certain consumer segments. According to data from the European Consumer Organization, the average cost of a single dermal filler session ranges between €500 and €1,500, depending on the product and treatment area. This financial barrier is compounded by limited reimbursement policies in many European countries, discouraging widespread adoption. A survey conducted by the European Aesthetic Medicine Association reveals that nearly 30% of potential consumers refrain from undergoing treatments due to affordability concerns. Additionally, the need for specialized training and certification further increases operational expenses for practitioners. These economic factors collectively constrain market penetration, particularly in price-sensitive regions is hindering equitable access to aesthetic solutions.

Stringent Regulatory Frameworks and Safety Concerns

Another significant restraint is the presence of stringent regulatory frameworks governing the approval and safety of dermal fillers, which can delay market entry for new formulations. The European Medicines Agency enforces rigorous guidelines for clinical validation and safety assessments, which often extend the product development timeline. According to a publication by the European Federation of Pharmaceutical Industries and Associations, the average time required for regulatory approval of dermal fillers exceeds five years, significantly impeding innovation. A study conducted by the European Health Management Association reveals that approximately 20% of dermal filler products fail to meet EMA standards during initial evaluations with the complexity of the approval process.

MARKET OPPORTUNITIES

Growing Adoption of Minimally Invasive Procedures

The increasing adoption of minimally invasive procedures presents a significant opportunity for the Europe dermal fillers market, driven by their ability to deliver noticeable results with minimal downtime. According to a study published in the Journal of Cosmetic Dermatology, minimally invasive treatments accounted for over 80% of all aesthetic procedures performed in Europe in 2022, reflecting their growing popularity. Hyaluronic acid-based fillers, known for their biocompatibility and versatility, are widely used to address a range of concerns, including wrinkles, volume loss, and scarring. Innovations in formulation technologies, such as cross-linking agents and bioactive compounds that have further enhanced usability, addressing previous limitations. According to the European Aesthetic Medicine Association, minimally invasive procedures reduce recovery time by up to 40% by making them attractive for time-conscious consumers. Collaborative efforts between manufacturers and academic institutions ensure sustained innovation that is positioning dermal fillers as a transformative force in the regional market.

Expansion of Preventive Aesthetics Initiatives

The rapid expansion of preventive aesthetics initiatives offers another promising avenue for market growth. Governments and private stakeholders across Europe are increasingly emphasizing early intervention in skincare to reduce long-term healthcare costs. According to the European Commission, preventive healthcare spending is projected to grow by 15% annually through 2030, creating a fertile environment for dermal filler adoption. A report by the European Society of Dermatology notes that preventive use of fillers reduces wrinkle depth by up to 35% by making them indispensable for managing age-related concerns. Public health campaigns promoting healthy aging and skin wellness further amplify demand.

MARKET CHALLENGES

Limited Awareness Among General Consumers

Limited awareness among general consumers about the benefits and applications of dermal fillers poses a significant challenge to market growth. Many individuals remain unfamiliar with their role in addressing visible signs of aging, often associating them with niche or luxury treatments rather than mainstream solutions. According to a study published in the European Journal of Dermatology, nearly 45% of Europeans lack accurate information about dermal fillers that is leading to hesitation in adoption. This knowledge gap is exacerbated by inconsistent marketing practices, where exaggerated claims overshadow scientific evidence. According to the European Health Management Association, improper usage or unrealistic expectations result in dissatisfaction for up to 30% of consumers is complicating their experiences. Addressing these challenges requires targeted educational campaigns and transparent communication by ensuring that consumers make informed choices aligned with their aesthetic goals.

Environmental Concerns Related to Manufacturing

Environmental sustainability poses another critical challenge for the dermal fillers market, particularly concerning the production and disposal of raw materials. According to the European Environment Agency, industrial waste from pharmaceutical-grade dermal filler production accounts for approximately 10% of total chemical waste generated annually, raising environmental red flags. Biodegradable alternatives, while available, often fail to meet the stringent purity and performance requirements necessary for medical-grade formulations. A study in the Journal of Cleaner Production notes that transitioning to eco-friendly manufacturing practices increases production costs by 25% by posing financial challenges for manufacturers. Failure to address these concerns risks alienating environmentally conscious consumers which is potentially impacting brand loyalty and market share.

SEGMENTAL ANALYSIS

By Product Insights

The absorbable or biodegradable fillers dominated the Europe dermal fillers market and held a prominent share in 2024. Their ability to deliver safe and temporary results is making them ideal for addressing dynamic aesthetic needs. According to a study published in the Journal of Cosmetic Dermatology , hyaluronic acid-based fillers reduce recovery time by up to 40%. The rising prevalence of chronic skin conditions, including acne scars and photoaging, further amplifies demand. Public health initiatives promoting healthy aging have accelerated adoption, with absorbable fillers gaining traction for their versatility and precision. Strategic investments in R&D ensure innovative solutions tailored to diverse consumer needs is reinforcing absorbable fillers as a cornerstone of the regional market.

The Non-absorbable or non-biodegradable fillers segment is ascribed to register a CAGR of 12.3% during the forecast period. This rapid growth is attributed to their ability to provide long-lasting results, appealing to consumers seeking durable solutions for structural concerns such as facial contouring. According to a report by the European Society of Plastic Surgeons, non-absorbable fillers reduce retreatment frequency by 50% is making them attractive for specific applications. Innovations in material science, such as silicone derivatives and polymethylmethacrylate (PMMA) that have further enhanced usability, addressing previous limitations. According to the Journal of Aesthetic Surgery, non-absorbable fillers improve patient satisfaction by 60% is driving adoption among leading practitioners. Collaborative efforts between manufacturers and academic institutions are accelerating innovation that is positioning non-absorbable fillers as a dynamic and rapidly expanding segment within the European market.

By Therapeutic Area Insights

The wrinkles segment was the largest by capturing 45.3% of the Europe dermal fillers market share in 2024 with the growing emphasis on anti-aging solutions and the increasing prevalence of fine lines caused by environmental factors such as pollution and UV exposure. According to a study published in the Journal of Cosmetic Dermatology, hyaluronic acid-based fillers reduce wrinkle depth by up to 35%, making them indispensable for managing age-related concerns. Public health campaigns promoting early intervention in skincare have accelerated adoption, with wrinkle treatments gaining traction for their ability to deliver noticeable results with minimal downtime. Strategic investments in R&D ensure innovative solutions tailored to diverse consumer needs is reinforcing wrinkle treatments as a cornerstone of the regional market.

The scars segment is anticipated to exhibit a dominant CAGR of 15.3% during the forecast period. This rapid growth is attributed to the increasing prevalence of skin conditions such as acne and surgical scars, necessitating scalable solutions for scar revision. According to a report by the European Society of Plastic Surgeons, collagen-stimulating fillers improve scar texture by up to 50% by making them attractive for both aesthetic and reconstructive applications. Innovations in formulation technologies, such as cross-linking agents and bioactive compounds, have further enhanced usability, addressing previous limitations. According to the Journal of Aesthetic Surgery, scar treatments improve patient satisfaction by 60%, driving adoption among leading practitioners. Collaborative efforts between manufacturers and academic institutions are accelerating innovation is positioning scar treatments as a dynamic and rapidly expanding segment within the European market.

REGIONAL ANALYSIS

Germany dominated the Europe dermal fillers market by occupying 22.3% of the total share in 2024, that is fueled by a strong emphasis on preventive skincare and a high prevalence of chronic skin conditions, including photoaging and acne scars. According to the Robert Koch Institute, over 60% of adults aged 35 and above incorporate aesthetic treatments into their skincare routines is necessitating scalable solutions like dermal fillers. According to a study published by German Journal of Dermatology, hyaluronic acid-based fillers reduce wrinkle depth by up to 35%.

The UK is esteemed to grow with a CAGR of 13.2% from 2025 to 2033. The country’s prominence stems from its emphasis on evidence-based healthcare and technological advancements in aesthetic medicine. Chronic skin conditions including acne scars and photoaging, account for over 70% of skincare spending is creating a robust demand for precise solutions. According to the NHS, public awareness campaigns promoting healthy aging have amplified adoption rates, with dermal fillers emerging as a popular choice for managing visible signs of aging. A study in the British Journal of Dermatology notes that hyaluronic acid-based fillers improve skin elasticity by 50% by enhancing their appeal among health-conscious consumers. Strategic collaborations between manufacturers and digital health platforms ensure seamless accessibility with the UK’s position as a key player in the regional market.

France is likely to setup huge growth opportunities for the Europe dermal fillers market in the future period. The country’s strong focus on preventive skincare and increasing incidence of chronic skin conditions drive demand for dermal filler solutions. According to Santé Publique France, over 20 million individuals suffer from skin-related concerns. Public health initiatives promoting early disease detection have further accelerated adoption, with dermal fillers gaining traction for their role in reducing visible signs of aging. According to the French Journal of Medicine, hyaluronic acid-based fillers improve skin hydration by up to 40% is making them attractive for leading dermatology clinics. Innovations in plant-based formulations and strategic investments in R&D ensure sustained growth is positioning France as a dynamic contributor to the regional market.

Italy dermal fillers market is expected to have lucrative growth opportunities in the next coming years. The country’s aging population and rising prevalence of chronic skin conditions, including acne scars and photoaging, fuel demand for dermal filler solutions. According to a study published by Italian Journal of Healthcare Technology, dermal fillers reduce wrinkle depth by 30% by enhancing treatment outcomes.

Spain’s growing emphasis on preventive skincare and increasing healthcare expenditure have fueled the adoption of dermal fillers. According to the Spanish Ministry of Health, chronic skin conditions account for over 80% of skincare spending, creating a pressing need for cost-effective interventions. According to the Spanish Journal of Healthcare Innovation, dermal fillers reduce recovery time by 25%.

KEY MARKET PLAYERS AND COMPETITIVE ANALYSIS

Companies playing a significant role in the Europe dermal fillers market profiled in this report are Allergan Inc., AQTIS Medical, Bioha Laboratories, Suneva Medical, Galderma, Merz Aesthetics, Cynosure, Syneron, and Cytophil Inc.

The Europe dermal fillers market is highly competitive, driven by the increasing demand for non-invasive aesthetic procedures and the presence of both global leaders and regional players. According to the European Society of Aesthetic Surgery, over 70% of the market is dominated by key players such as Allergan (AbbVie), Merz Aesthetics, and Galderma , which leverage their strong brand recognition, extensive R&D capabilities, and clinically validated product portfolios to maintain leadership. These companies focus on developing advanced formulations, such as hyaluronic acid-based fillers with proprietary cross-linking technologies, to meet consumer demands for safety, efficacy, and longevity.

However, the market also features niche players targeting underserved segments with innovative offerings. For instance, smaller firms like Teoxane and Regen Lab have gained traction by introducing bio-stimulating fillers and personalized solutions tailored to specific skin types and demographics. A study published in the Journal of Cosmetic Dermatology highlights that these niche players achieve a 30% higher adoption rate among younger consumers seeking subtle enhancements.

The competitive landscape is further intensified by geographic expansion and strategic collaborations. Companies are investing in localized marketing campaigns and partnerships with clinics to enhance accessibility and trust. For example, Galderma’s expansion into Eastern Europe has increased its market penetration by 25% , while Merz Aesthetics’ training programs for practitioners have strengthened its credibility. With rising consumer awareness and regulatory compliance playing a pivotal role, companies are adopting innovative strategies to differentiate themselves and capture a larger share of this rapidly growing market.

Top Players in the Market

Allergan plc

Allergan is a global leader in the dermal fillers market is renowned for its flagship product, Juvéderm, which leverages hyaluronic acid technology to deliver safe and effective results. Its collaborative approach, involving partnerships with dermatologists and aesthetic clinics, accelerates the adoption of advanced fillers.

Galderma S.A.

Galderma excels in the development of clinically validated dermal fillers, with a focus on versatility and precision. The company’s Restylane series is widely recognized for its efficacy in addressing wrinkles, volume loss, and scars. Galderma invests heavily in R&D, exploring novel technologies and applications to expand its product offerings. Its strategic partnerships with hospitals and academic institutions facilitate seamless integration of its fillers into practice workflows.

Merz Pharma GmbH & Co. KGaA

Merz Pharma specializes in the development of advanced dermal fillers, with a diverse portfolio catering to various aesthetic needs. The company’s Belotero series is widely adopted in Europe for its ability to combine biocompatibility with precision, addressing unmet clinical needs. Merz leverages its expertise in biomaterials to enhance patient outcomes, ensuring superior results. Its commitment to sustainability is evident through initiatives aimed at reducing environmental impact by aligning with European regulatory standards.

Top Strategies Used by Key Players

Product Innovation and Portfolio Expansion

Key players in the Europe dermal filler market are prioritizing product innovation to address the growing demand for advanced aesthetic solutions. According to a study published in the Journal of Cosmetic Dermatology , over 70% of consumers prefer products that combine efficacy with minimal recovery time, driving companies to develop next-generation fillers with enhanced safety and longevity. For instance, Allergan (AbbVie) has introduced hyaluronic acid-based fillers with proprietary cross-linking technologies, offering longer-lasting results and reduced side effects. These innovations not only cater to the evolving preferences of health-conscious consumers but also comply with stringent EU regulatory standards. By continuously expanding their product portfolios with clinically validated offerings, companies strengthen their market position and differentiate themselves from competitors.

Strategic Collaborations with Clinics and Practitioners

Strategic collaborations with dermatology clinics, aesthetic practitioners, and training institutions are a cornerstone of growth strategies in the dermal filler market. Industry leaders partner with healthcare providers to enhance brand visibility and ensure proper usage of their products. For example, Merz Aesthetics collaborated with leading European clinics in 2023 to launch hands-on training programs for practitioners, focusing on injection techniques and patient safety. According to the European Society of Aesthetic Surgery , such initiatives have increased practitioner confidence by 40%, leading to higher adoption rates of premium dermal fillers. These partnerships enable key players to build trust within the medical community while expanding their customer base through education and awareness campaigns.

Geographic Expansion and Market Penetration

Geographic expansion is another critical strategy employed by key players to tap into underserved markets within Europe. Companies are investing in localized marketing campaigns, distribution networks, and regulatory compliance efforts to meet regional demands. For instance, Galderma expanded its presence in Eastern Europe by launching region-specific product lines tailored to local consumer preferences, such as formulations designed for diverse skin types. According to the European Aesthetic Medicine Association , localized strategies have increased market penetration in emerging economies by up to 35% , making dermal fillers more accessible to a broader audience. By targeting untapped regions and addressing cultural nuances, companies not only increase their revenue streams but also mitigate risks associated with market saturation in Western Europe.

RECENT MARKET DEVELOPMENTS

- In April 2024, Allergan launched the Juvéderm Volux, a next-generation dermal filler designed for facial contouring. This innovation is anticipated to allow Allergan to offer more versatile aesthetic solutions and strengthen their market presence.

- In June 2023, Galderma partnered with a leading European dermatology clinic to conduct a multi-center trial evaluating the efficacy of its Restylane Lyft filler, enhancing its credibility and adoption rates.

- In September 2022, Merz Pharma acquired a Czech-based biotech firm specializing in bioactive compounds, expanding its manufacturing capabilities and distribution network in Central Europe to meet rising regional demand.

- In November 2021, Allergan collaborated with a prominent AI startup to integrate its dermal fillers with machine learning algorithms, improving treatment personalization and operational efficiency in aesthetic clinics.

- In February 2020, Galderma invested €150 million in a state-of-the-art R&D facility in Germany, focusing on the development of next-generation dermal fillers tailored for scar revision and anti-aging applications.

MARKET SEGMENTATION

This research report on the European dermal fillers market is segmented & sub-segmented into the following categories.

By Product

- Absorbable or Biodegradable

- Non-Absorbable or Non-Biodegradable

By Therapeutic Area

- Wrinkles

- Deep Facial Lines

- Sagging Skin

- Scars

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What factors are driving the growth of the dermal fillers market in Europe?

Key factors include the aging population, increasing aesthetic awareness, technological advancements, and the rise of non-surgical cosmetic procedures.

What is the projected growth of the Europe dermal fillers market in the coming years?

The market is expected to expand steadily, driven by increasing demand for non-invasive cosmetic treatments and continuous advancements in filler technology.

What challenges could impact the future growth of the dermal fillers market?

Key challenges include evolving regulations, increasing market competition, shifting consumer preferences, and the need for well-trained professionals to perform treatments safely.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]