Europe Dark Chocolate Market Size, Share, Trends & Growth Forecast Report By Distribution Channel (Retailers, Hypermarkets/ Supermarkets, Online stores), and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2025 to 2033

Europe Dark Chocolate Market Size

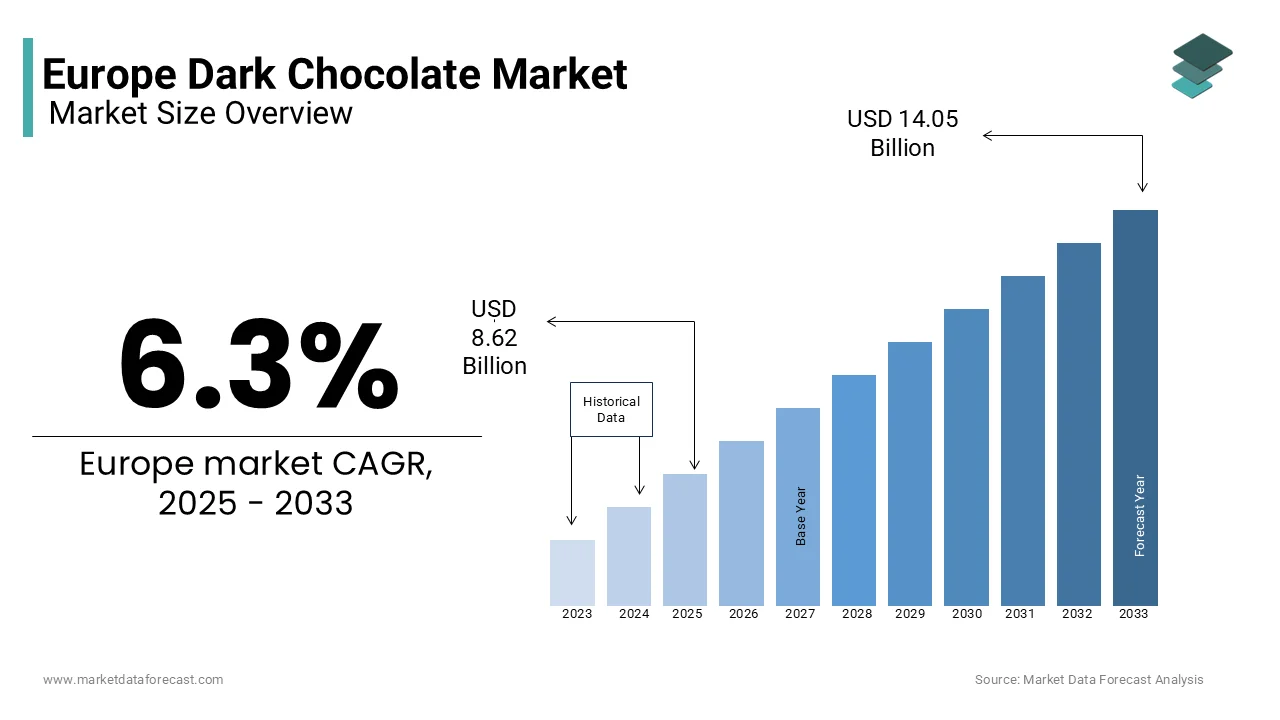

The dark chocolate market size in Europe was valued at USD 8.11 billion in 2024. The European market is estimated to be worth USD 14.05 billion by 2033 from USD 8.62 billion in 2025, growing at a CAGR of 6.3% from 2025 to 2033.

Dark chocolate is celebrated for its high cocoa content and minimal sugar and is a popular choice among European consumers seeking indulgence with health benefits. Factors such as the growing preference for dark chocolate from health-conscious individuals who value the antioxidant properties and cardiovascular benefits associated with dark chocolate, increasing demand for premium and organic products and rising disposable incomes are fuelling the demand for dark chocolate in Europe. Germany is the largest consumer of dark chocolate in the European region and accounts for 28% of total sales, followed by France and the UK.

MARKET DRIVERS

Growing Health Consciousness Among Consumers in Europe

The rising awareness of health and wellness is a major driver of the dark chocolate market in the European region. According to Eurostat, over 65% of European consumers prioritize products with perceived health benefits, with dark chocolate being a popular choice due to its high cocoa content and antioxidant properties. As per the European Nutrition Council, sales of dark chocolate with 70% or higher cocoa content grew by 20% in 2022, particularly in countries like Germany and Sweden. For instance, Sweden reported a 25% increase in premium dark chocolate purchases linked to health-conscious millennials. This trend underscores the growing preference for healthier indulgence options.

Influence of Premiumization Trends

The trend toward premiumization is another significant driver to the European dark chocolate market growth. According to the European Luxury Goods Association, premium dark chocolate sales increased by 18% in 2022 owing to the affluent consumers seeking artisanal and gourmet options. Brands offering single-origin cocoa and ethically sourced ingredients have capitalized on this trend. Highlighting this, France witnessed a 30% rise in demand for luxury dark chocolate brands during festive seasons, underscoring the growing appeal of premium offerings. This shift reflects the increasing willingness of consumers to pay a premium for high-quality and exclusive products.

MARKET RESTRAINTS

Fluctuating Cocoa Prices

Cocoa is a key ingredient in dark chocolate. Fluctuating prices of cocoa in Europe is a key factor hindering the European dark chocolate market growth. According to the European Agricultural Commission, cocoa prices surged by 15% in 2022 due to supply chain disruptions and adverse weather conditions in producing regions. These price fluctuations increase production costs and impact profit margins for manufacturers in Spain and Italy, where small-scale producers dominate the market. Such volatility creates pricing pressures and limits accessibility for price-sensitive consumers, posing a significant challenge to market stability in Europe.

Stringent Labeling and Advertising Regulations

Stringent regulations on labeling and advertising pose challenges for dark chocolate manufacturers. According to the European Food Safety Authority, restrictions on health claims reduced marketing opportunities by 22% in 2022. For example, Italy saw a decline in promotional activities for dark chocolate products, limiting brand visibility and consumer engagement. These regulations make it harder for manufacturers to communicate the health benefits of their products, affecting consumer perception and purchase decisions.

MARKET OPPORTUNITIES

Expansion into Emerging Markets

Emerging markets within Europe, particularly Eastern Europe is providing significant opportunities for dark chocolate market growth in this region. According to the European Bank for Reconstruction and Development, investments in retail infrastructure in Poland and Romania grew by 25% in 2022, creating a conducive environment for premium and health-focused products. Rising urbanization and increasing disposable incomes in these regions are driving demand for indulgent yet healthy snacks, positioning dark chocolate as a promising category for expansion.

Introduction of Functional Dark Chocolate

The introduction of functional dark chocolate, enriched with vitamins, probiotics, or adaptogens, offers immense potential. According to the European HealthTech Alliance, functional food sales grew by 30% in 2022, with dark chocolate positioned as a carrier for added health benefits. Innovations in this space, such as stress-relief chocolates or immunity-boosting variants, cater to the growing demand for products that combine indulgence with wellness, opening new avenues for market growth.

MARKET CHALLENGES

Supply Chain Disruptions

Supply chain disruptions that are exacerbated by geopolitical tensions have impacted raw material availability. According to the European Supply Chain Institute, 30% of dark chocolate manufacturers faced delays in sourcing cocoa and other ingredients in 2022, leading to inconsistent product availability. These disruptions create operational challenges and increase costs, affecting both manufacturers and consumers. Ensuring a stable supply chain remains a critical issue for sustaining market growth.

Competition from Alternative Snacks

Rising competition from alternative snacks, such as protein bars and nut-based treats is a notable challenge to the European dark chocolate market. According to the European Snack Association, alternative snack sales grew by 22% in 2022, diverting consumer spending away from traditional confectionery products. Dark chocolate manufacturers must innovate and differentiate their offerings to retain consumer interest amidst this growing competition.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

6.3% |

|

Segments Covered |

By Distribution Channel, and Region |

|

Various Analyses Covered |

Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled |

Ferrero International, Nestle, Mondelez International Inc., Amul, Ritter Sport, The Hershey Company, Godiva, Lindt & Sprungli AG, Ghirardelli Chocolate co., Patchi, Harry and David Holdings inc., and others. |

SEGMENTAL ANALYSIS

By Distribution Channel Insights

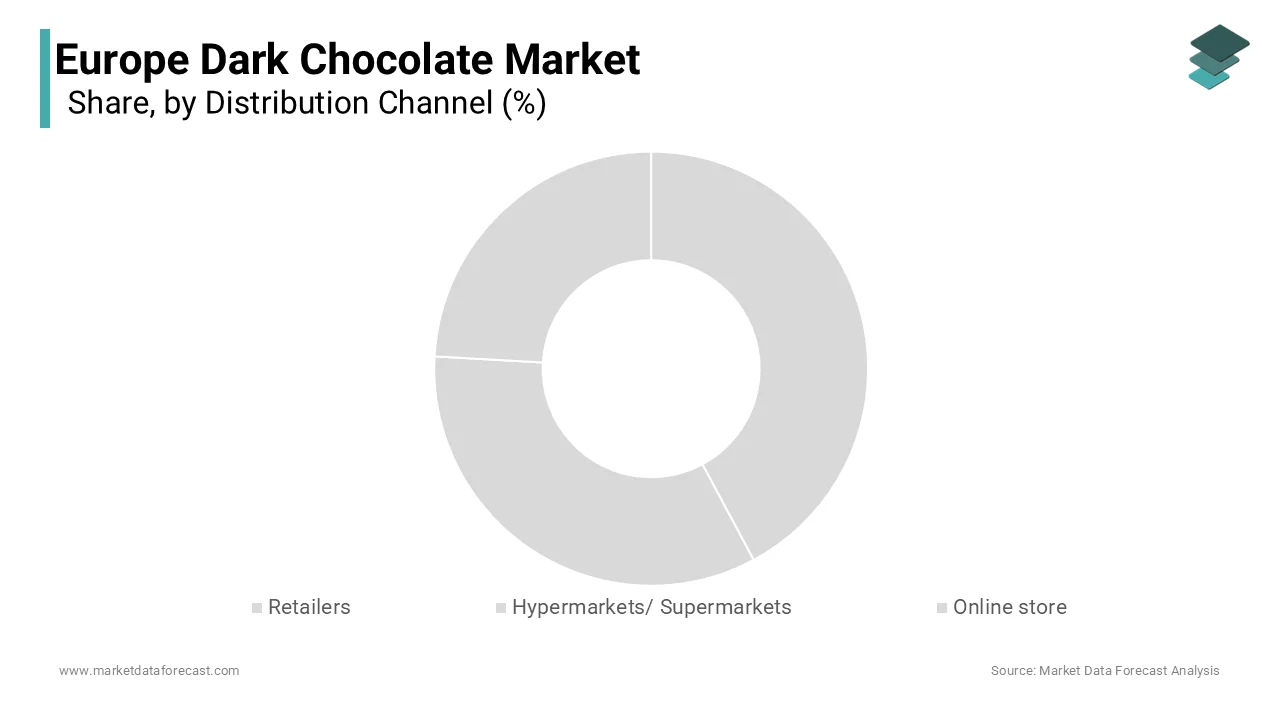

The supermarkets and hypermarkets segment dominated the European dark chocolate market by holding 48.8% of the European market share in 2024. The domination of supermarkets and hypermarkets segment is driven by their widespread presence and ability to offer competitive pricing. Retail giants like Tesco and Carrefour stock a wide variety of dark chocolate brands, catering to diverse consumer preferences. Their established distribution networks and promotional strategies are likely to boost their position of the supermarkets and hypermarkets segment in the European market.

The online stores segment is expected to progress at a notable CAGR of 9.4% over the forecast period. According to the European E-commerce Association, online sales of dark chocolate grew by 40% in 2022 due to the convenience and personalized shopping experiences.

REGIONAL ANALYSIS

Western Europe held the major share of the European dark chocolate market in 2024. The market growth in this side of the European part is driven by advanced retail networks, high disposable incomes, and a strong tradition of indulging in premium chocolates. Countries like Germany, the UK, and France are at the forefront of adopting innovative dark chocolate products, ensuring sustained demand.

On the other hand, Eastern Europe is expected to be growing at a CAGR of 10.7% over the forecast period owing to the rising urbanization and increasing disposable incomes. According to the European Bank for Reconstruction and Development, countries like Poland and Romania are emerging as key markets, offering affordable yet high-quality dark chocolate products to attract price-sensitive consumers.

KEY MARKET PLAYERS

Ferrero International, Nestle, Mondelez International Inc., Amul, Ritter Sport, The Hershey Company, Godiva, Lindt & Sprungli AG, Ghirardelli Chocolate co., Patchi, Harry and David Holdings inc. are some of the notable companies in Europe Dark Chocolate market.

TOP 3 PLAYERS IN THE MARKET

Lindt & Sprüngli, Barry Callebaut, and Ferrero dominate the market. Lindt focuses on premium branding, targeting affluent consumers with its luxurious and high-quality offerings. Barry Callebaut emphasizes sustainable sourcing, launching initiatives like the “Cocoa Horizons” program to promote ethical practices. Ferrero leverages innovative packaging and marketing strategies to maintain its leadership in the competitive market. These players leverage their expertise in product development and sustainability to maintain their dominance.

STRATEGIES USED BY THE MARKET PLAYERS

To strengthen their market positions, key players in the Europe dark chocolate market employ several strategic approaches. Sustainability initiatives are a primary focus, with Barry Callebaut investing in ethical cocoa sourcing and eco-friendly practices to align with consumer preferences. According to the European Innovation Council, Lindt & Sprüngli focuses on premium branding, emphasizing craftsmanship and quality to differentiate itself from competitors. Ferrero leverages digital marketing and e-commerce strategies to enhance visibility and accessibility, particularly among younger demographics. Additionally, product innovation, such as introducing functional chocolates, ensures that these players remain at the forefront of market trends. These strategies not only drive growth but also ensure long-term customer loyalty in a dynamic market environment.

MARKET SEGMENTATION

This research report on the Europe dark chocolate market is segmented and sub-segmented into the following categories.

By Distribution Channel

- Retailers

- Hypermarkets/ Supermarkets

- Online stores

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the projected market size of the European dark chocolate market by 2033?

The European dark chocolate market is estimated to reach USD 14.05 billion by 2033.

2. What are the major challenges facing the European dark chocolate market?

The key challenges include supply chain disruptions and competition from alternative snacks.

3. Which region held the largest share of the European dark chocolate market in 2024?

Western Europe held the major share of the European dark chocolate market in 2024.

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]