Europe Contact Center as a Service (CCaaS) Market Size, Share, Trends, & Growth Forecast Report By Offering (Solution and Services), Organization Size (Large Enterprises and Small and Medium Enterprises (SMEs)), End User (BFSI, IT and Telecommunications, Government, Media and Entertainment, Healthcare, Others), Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2024 to 2033

Europe Contact Center as a Service (CCaaS) Market Size

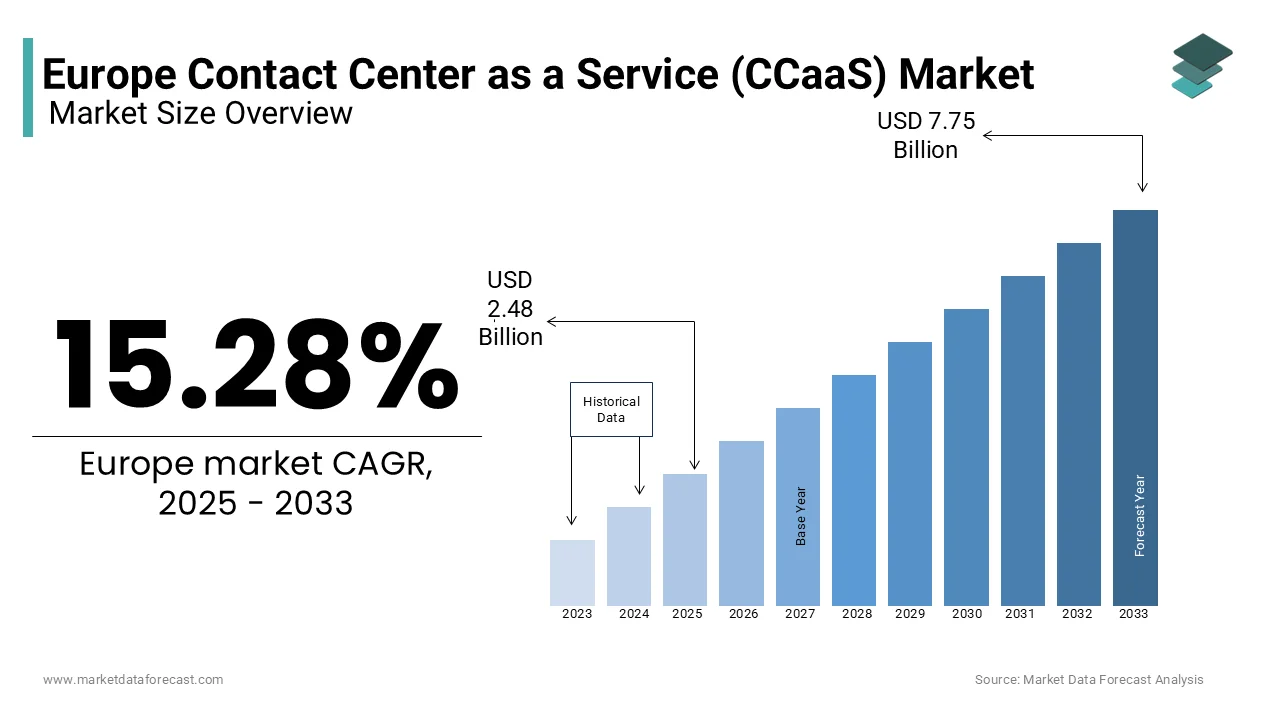

The Europe Contact center as a service (CCaaS) market was worth USD 2.15 billion in 2024. The European market is estimated to reach USD 7.75 billion by 2033 from USD 2.48 billion in 2025, growing at a CAGR of 15.28% from 2025 to 2033.

CCaaS refers to cloud-based solutions that enable organizations to manage customer interactions across multiple channels, including voice, email, chat, and social media, through a unified platform. According to Eurostat, the demand for CCaaS solutions in Europe has surged by 15% annually owing to the increasing adoption of remote work models and the need for scalable, cost-effective customer service solutions. According to the European Commission, more than 60% of enterprises have transitioned from traditional on-premises contact centers to cloud-based systems to enhance operational flexibility and improve customer engagement.

The advancements in artificial intelligence (AI), machine learning, and analytics that enable predictive customer insights and personalized service delivery are promoting the demand for CCaaS in Europe. A report by the European Data Protection Supervisor notes that 70% of businesses prioritize compliance with GDPR when selecting CCaaS providers, ensuring secure handling of sensitive customer data. Germany, France, and the UK are currently leading the CCaaS market share in Europe due to their leadership in digital transformation. With the rise of omnichannel communication and the growing emphasis on customer experience, the European CCaaS market is predicted to have a promising future ahead.

MARKET DRIVERS

Increasing Demand for Omnichannel Customer Support in Europe

The growing demand for omnichannel customer support is a major driver of the Europe contact center as a service (CCaaS) market. As per Eurostat, 75% of European consumers expect seamless interactions across multiple channels, such as voice, email, chat, and social media, to resolve their queries efficiently. Businesses adopting omnichannel strategies experience a 20% increase in customer satisfaction and a 15% rise in retention rates. CCaaS platforms enable enterprises to integrate these channels into a unified system, ensuring consistent and personalized customer experiences. Furthermore, according to the German Federal Ministry for Economic Affairs and Energy, 60% of European businesses have invested in CCaaS solutions to meet evolving customer expectations. As remote work models expand, the flexibility and scalability of CCaaS make it indispensable for delivering real-time, data-driven customer support.

Advancements in Artificial Intelligence and Automation

Advancements in artificial intelligence (AI) and automation are propelling the growth of the Europe CCaaS market. According to the European Data Protection Supervisor, 80% of businesses leverage AI-powered chatbots and predictive analytics to enhance customer interactions and reduce operational costs. These technologies enable automated responses, sentiment analysis, and personalized recommendations, improving efficiency by 30%, according to Eurostat. For instance, AI-driven tools can handle up to 80% of routine inquiries, freeing human agents to focus on complex issues. The French Ministry of Economy underscores that AI adoption in CCaaS has led to a 25% reduction in average call handling times, enhancing productivity. Additionally, the UK Office for National Statistics reports that 45% of European enterprises prioritize AI-enabled CCaaS solutions to stay competitive. These innovations not only optimize customer service but also align with GDPR compliance requirements, ensuring secure data handling.

MARKET RESTRAINTS

Stringent Data Protection Regulations Under GDPR

One major restraint in the Europe contact center as a service (CCaaS) market is the stringent data protection regulations imposed by the General Data Protection Regulation (GDPR). These regulations mandate secure handling of personal data, increasing operational complexity and compliance costs for CCaaS providers. According to the European Commission, businesses spend an average of 2.5% of their annual revenue on GDPR compliance, with smaller firms disproportionately affected. Non-compliance can result in fines up to €20 million or 4% of global turnover, as highlighted by the UK Information Commissioner's Office. This regulatory burden forces companies to invest heavily in security infrastructure and employee training, reducing profit margins and limiting flexibility, especially for smaller CCaaS providers operating on tight budgets.

Inconsistent Internet Connectivity Across Europe

Another significant restraint is the high dependency on reliable internet connectivity, which remains inconsistent across Europe. As per the European Union Agency for Cybersecurity (ENISA), rural areas in countries like Romania and Bulgaria have broadband penetration rates below 60%, compared to over 90% in urban centers. This digital divide poses challenges for deploying cloud-based CCaaS solutions effectively. Eurostat further reveals that approximately 18% of EU households still face difficulties accessing high-speed internet. Frequent connectivity disruptions can degrade customer experience and hinder real-time communication capabilities, making it harder for CCaaS platforms to deliver consistent performance. Such inconsistencies restrict the scalability of CCaaS solutions in underserved regions, impacting market growth.

MARKET OPPORTUNITIES

Increasing Adoption of Remote Work Models

The growing adoption of remote work models in Europe presents a significant opportunity for the contact center as a service (CCaaS) market. According to the European Foundation for the Improvement of Living and Working Conditions, 48% of companies in the EU have implemented remote or hybrid work policies since the pandemic, which is driving demand for cloud-based communication solutions. CCaaS platforms enable businesses to efficiently manage remote agents while maintaining high service standards. According to Eurostat, over 37% of employees in the EU now work remotely at least once a week, creating a robust market for scalable and flexible CCaaS solutions. This shift is further supported by the European Commission’s Digital Decade initiative, which aims to ensure 100% access to fast broadband by 2030, enhancing the infrastructure needed for seamless CCaaS deployment.

Rising Demand for Omnichannel Customer Support

The increasing demand for omnichannel customer support across Europe offers another major opportunity for the CCaaS market. As per a study by the European Consumer Centre Network, 73% of customers expect consistent service across multiple channels, such as voice, email, chat, and social media. CCaaS platforms are uniquely positioned to meet this demand by integrating various communication tools into a single interface. According to the European Commission, businesses investing in omnichannel strategies experience a 15-20% increase in customer satisfaction rates. This trend underscores the potential for CCaaS providers to expand their offerings and capture a larger share of the evolving customer service landscape.

MARKET CHALLENGES

Integration with Legacy Systems

One of the major challenges for the Europe contact center as a service (CCaaS) market is the difficulty in integrating CCaaS solutions with legacy systems used by many businesses. According to the European Union Agency for Cybersecurity (ENISA), more than 60% of European enterprises still rely on outdated infrastructure, which complicates seamless integration with modern cloud-based platforms. This challenge often leads to increased costs and extended implementation timelines. According to a report of European Commission’s Digital Transformation Monitor, businesses spend an average of €150,000 annually to upgrade or integrate legacy systems, deterring smaller firms from adopting CCaaS solutions. Additionally, data silos created by incompatible systems can hinder operational efficiency and customer experience. As companies strive to modernize, the lack of technical expertise further exacerbates this issue, slowing down the widespread adoption of CCaaS technologies across Europe.

Resistance to Cloud Adoption Due to Security Concerns

Another significant challenge is the resistance to cloud adoption driven by concerns over data security and privacy. According to a survey by Eurostat, 42% of European businesses cite cybersecurity risks as a primary barrier to migrating their operations to the cloud. The European Data Protection Supervisor notes that despite robust regulations like GDPR, high-profile data breaches have made organizations wary of storing sensitive customer information on third-party servers. This hesitancy is particularly pronounced in industries like finance and healthcare, where data sensitivity is critical. Furthermore, the European Central Bank reports that cyberattacks targeting European businesses increased by 30% in 2022, intensifying fears about cloud vulnerabilities. These concerns limit the growth potential of CCaaS providers, as they must invest heavily in building trust and demonstrating compliance with stringent security standards to overcome this resistance.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

15.28% |

|

Segments Covered |

By Offering, Organization Size, End User, and Country |

|

Various Analyses Covered |

Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and Rest of Europe |

|

Market Leaders Profiled |

8x8 Inc., ALE International (China Huaxin Post and Telecom Technologies Co. Limited), Amazon Web Services Inc. (Amazon.Com Inc.), Anywhere365 Enterprise Dialogue Management, Atos SE, Avaya LLC, Cisco Systems Inc, Enghouse Interactive Inc. (Enghouse Systems Limited), Five9 Inc., Genesys, Microsoft Corporation, and NICE Ltd. |

SEGMENTAL ANALYSIS

By Offering Insights

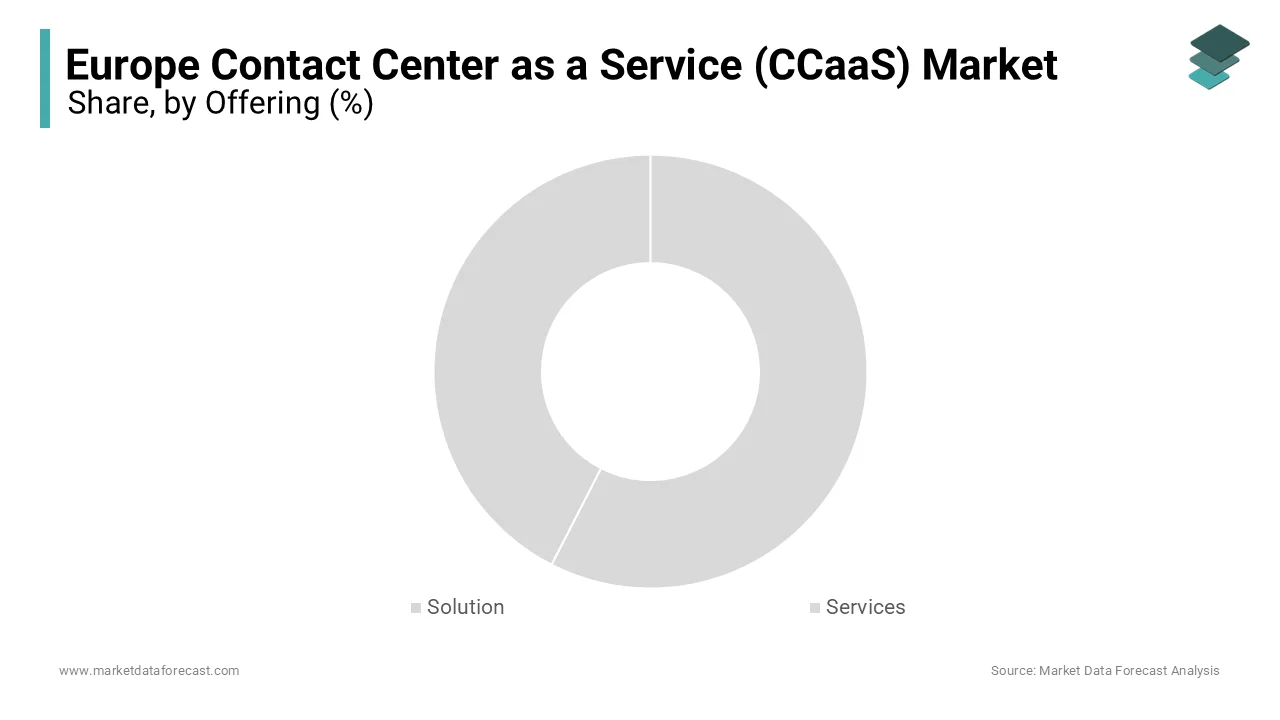

The solution segment dominated the Europe contact center as a service (CCaaS) market by accounting for a 65.8% of the European market share in 2024 due to its ability to address integration challenges with legacy systems, which over 60% of European enterprises face, as reported by the European Commission. Hybrid solutions bridging on-premise and cloud systems are critical for industries like finance and healthcare, driving demand. The importance lies in enabling seamless data exchange, reducing costs by up to 40%. By offering scalable, industry-specific solutions, CCaaS providers ensure compliance and operational efficiency, making this segment indispensable for digital transformation across Europe.

The services segment is anticipated to register the fastest CAGR of 18.7% over the forecast period. The rising cybersecurity concerns is majorly propelling the growth of the services segment in the European market. Managed services, including encryption and real-time threat monitoring, reduce cyberattack losses by 50%, as highlighted by Eurostat. The growing emphasis on GDPR compliance and 24/7 customer support further accelerates adoption. Its importance lies in building trust and ensuring secure, uninterrupted operations, making it vital for enterprises prioritizing data protection and customer experience in an increasingly digital landscape.

By Organization Size Insights

The large enterprises segment held the leading share of 60.7% in the Europe contact center as a service (CCaaS) market in 2024. The domination of large enterprises segment in the European market is driven by their extensive customer bases and complex operational needs, requiring scalable and feature-rich CCaaS solutions. As per the European Commission, large enterprises allocate 10-15% of their IT budgets to cloud services to prioritize omnichannel support and advanced analytics. Their dominance is further driven by the need for compliance with GDPR and other regulations, ensuring secure data handling. The importance of this segment lies in its ability to influence market trends, drive innovation, and set benchmarks for smaller players, fostering broader adoption of CCaaS technologies across industries.

The small and medium enterprises (SMEs) segment is estimated to witness the highest CAGR of 20.5% over the forecast period owing to their affordability and flexibility of CCaaS solutions that enable SMEs to enhance customer experience without heavy upfront investments. According to Eurostat, SMEs make up over 99% of businesses in the EU, which is creating a vast untapped market. As per the European Investment Bank, SMEs adopting CCaaS achieve a 25% boost in operational efficiency.

By End User Insights

The BFSI segment was the largest end-user segment in the Europe contact center as a service (CCaaS) market and accounted for 32.3% of the European market share in 2024. The domination of BFSI segment is primarily credited to the sector's need for secure, scalable, and compliant communication solutions to handle sensitive customer data. According to the European Banking Authority, BFSI firms spend approximately 15% of their IT budgets on cloud-based services, prioritizing omnichannel support and fraud detection. With stringent GDPR compliance requirements, CCaaS platforms enable BFSI organizations to enhance customer experience while ensuring data security and regulatory adherence.

The healthcare segment is anticipated to showcase the fastest CAGR of 22.7% over the forecast period owing to the increasing demand for telehealth services and remote patient support, especially post-pandemic. The European Health and Digital Executive Agency (HaDEA) states that over 60% of healthcare providers are investing in digital tools to improve patient engagement. Additionally, the sector benefits from CCaaS solutions that ensure secure handling of sensitive medical data, complying with regulations like GDPR.

REGIONAL ANALYSIS

The UK played the dominating role in the Europe contact center as a service (CCaaS) market in 2024 by holding a 28.4% of the European market share. The robust digital infrastructure of the UK and high adoption of cloud-based technologies, with the government’s Digital Economy Act ensuring widespread broadband access are boosting the position of the UK in the European market. According to the UK Office for National Statistics, over 85% of businesses in the UK have transitioned to digital solutions, fostering CCaaS growth. Additionally, the presence of major financial hubs like London boosts demand for advanced customer support systems. The importance of the UK lies in its role as a technological innovator, setting trends for other European nations while leveraging its strong regulatory framework, including GDPR compliance, to ensure secure and scalable CCaaS implementations.

Germany is another top performer in the European market. The growth of the Germany in the European market is majorly due to the strong industrial base and emphasis on digital transformation, supported by the Federal Ministry for Economic Affairs and Energy’s initiatives to boost cloud adoption. Germany’s IT sector invests heavily in omnichannel communication tools, with Statista reporting a 30% annual increase in cloud spending among enterprises. The country’s strict data protection laws align well with CCaaS platforms, ensuring compliance and security. Germany’s prominence is vital as it bridges traditional industries with modern technologies, driving innovation and operational efficiency across sectors like manufacturing, BFSI, and healthcare, making it a cornerstone of the European CCaaS market.

France holds a significant position in the European CCaaS market. The growth of France in the European market is fueled by France’s focus on digital sovereignty and investments in smart city initiatives, which encourage cloud adoption. The Banque de France notes that over 70% of French companies prioritize enhancing customer experience through digital tools, boosting CCaaS demand. France’s leadership is also driven by its thriving IT and telecommunications sector, which accounts for 6% of the nation’s GDP. The importance of France lies in its ability to integrate CCaaS solutions into public services and private enterprises alike, fostering innovation while adhering to GDPR standards, thereby solidifying its role as a key driver of the European CCaaS landscape.

KEY MARKET PLAYERS

The major players in the Europe contact center as a service (CCaaS) market include 8x8 Inc., ALE International (China Huaxin Post and Telecom Technologies Co. Limited), Amazon Web Services Inc. (Amazon.Com Inc.), Anywhere365 Enterprise Dialogue Management, Atos SE, Avaya LLC, Cisco Systems Inc, Enghouse Interactive Inc. (Enghouse Systems Limited), Five9 Inc., Genesys, Microsoft Corporation, and NICE Ltd.

MARKET SEGMENTATION

This research report on the Europe contact center as a service (CCaaS) market is segmented and sub-segmented into the following categories.

By Offering

- Solution

- Services

By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

By End User

- BFSI

- IT and Telecommunications

- Government

- Media and Entertainment

- Healthcare

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is driving the growth of the Europe Contact Center as a Service (CCaaS) market?

The increasing demand for cloud-based solutions, AI-powered automation, and omnichannel customer support is driving the growth of the CCaaS market in Europe.

Which industries are the primary adopters of CCaaS solutions in Europe?

The major industries using CCaaS include BFSI, retail, healthcare, IT & telecom, and travel & hospitality.

What is the role of omnichannel support in CCaaS adoption?

Omnichannel capabilities allow businesses to integrate voice, chat, email, and social media for seamless customer interactions.

What future trends will shape the Europe CCaaS market?

The rise of AI-driven automation, cloud-native solutions, hybrid cloud adoption, and enhanced self-service capabilities will shape the market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]