Europe Commercial Gensets Market Size, Share, Trends & Growth Forecast Report By Power Rating, Fuel Types, End-Use, and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2025 to 2033

Europe Commercial Gensets Market Size

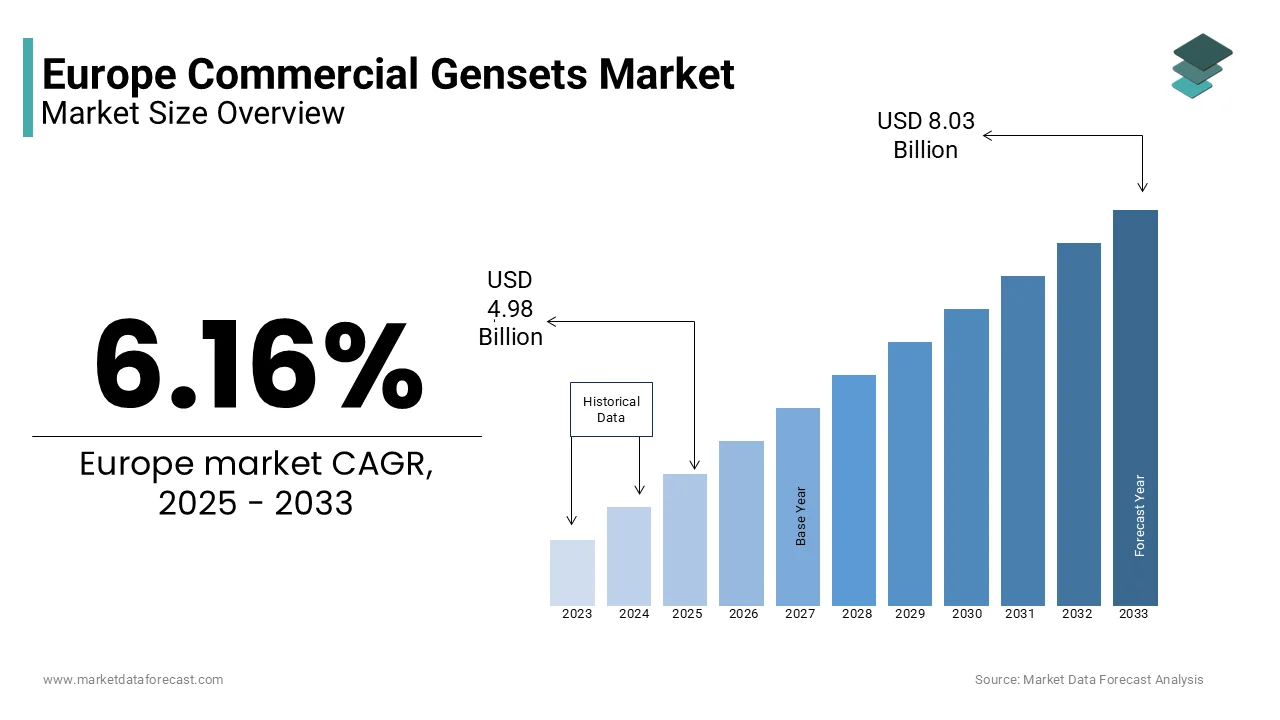

The Europe commercial gensets market size was valued at USD 4.69 billion in 2024. The European market is estimated to be worth USD 8.03 billion by 2033 from USD 4.98 billion in 2025, growing at a CAGR of 6.16% from 2025 to 2033.

The European commercial gensets market is witnessing steady growth, driven by the region's reliance on reliable power solutions amid increasing energy demands. According to Statista, the European genset market was valued at approximately €4.5 billion in 2022, with projections indicating a compound annual growth rate (CAGR) of 5.3% through 2030. This growth is fueled by the rising adoption of gensets across key sectors such as healthcare, data centers, and telecommunications. The European Union’s commitment to renewable energy integration has also spurred demand for hybrid gensets, which combine traditional fuel sources with renewable energy systems.

Germany leads the regional market, accounting for nearly 22% of total sales in 2022, as per a report by Roland Berger. This dominance stems from the country’s robust industrial base and stringent regulations ensuring uninterrupted power supply in critical infrastructure. Furthermore, the UK and France are emerging as significant contributors, driven by investments in smart city projects and the expansion of 5G networks. A study by Frost & Sullivan has revealed that the demand for gensets below 125 kVA is particularly strong, catering to small-scale enterprises and residential complexes.

Despite economic uncertainties, the market remains resilient due to ongoing urbanization and the need for backup power solutions in regions prone to grid instability. The growing emphasis on sustainability is also encouraging manufacturers to innovate, offering eco-friendly gensets that align with Europe’s green energy goals.

MARKET DRIVERS

Rising Demand for Uninterrupted Power Supply

The escalating demand for uninterrupted power supply across various industries is propelling the European commercial gensets market. Sectors such as healthcare, data centers, and telecommunications require consistent power to ensure operational continuity. According to Eurostat, the healthcare sector in Europe witnessed a 15% increase in power consumption between 2018 and 2022 is primarily due to the proliferation of advanced medical equipment and digital health records. Similarly, the exponential growth of data centers in Europe, with over 400 facilities operational as of 2022 with the need for reliable backup power systems. The increasing frequency of power outages, particularly in rural areas, further amplifies the necessity for commercial gensets. For instance, in 2021, Germany experienced an average of 12 minutes of power interruptions per customer, as reported by the Federal Network Agency.

Expansion of Renewable Energy Integration

The integration of renewable energy sources into the European power grid is another significant driver of the commercial gensets market. As per the International Energy Agency, renewable energy accounted for 40% of Europe’s electricity generation in 2022 by marking a substantial shift toward sustainable practices. However, the intermittent nature of renewables like solar and wind necessitates backup power solutions to stabilize the grid during periods of low generation. Hybrid gensets, which combine conventional fuel sources with renewable energy systems are gaining traction as a viable solution. A study by BloombergNEF reveals that hybrid gensets are expected to capture 25% of the European market by 2030 with government incentives and corporate sustainability goals. For example, the European Green Deal has allocated €1 trillion to support clean energy initiatives by encouraging businesses to adopt hybrid technologies. This trend is particularly prominent in countries like Sweden and Denmark, where renewable energy penetration exceeds 50%.

MARKET RESTRAINTS

Stringent Environmental Regulations

Stringent environmental regulations imposed by the European Union pose a significant challenge to the commercial gensets market. The EU’s Emissions Trading System (ETS) mandates strict limits on greenhouse gas emissions by compelling manufacturers to develop gensets that comply with these standards. According to the European Environment Agency, non-compliance can result in penalties exceeding €100 per ton of CO2 emitted by creating financial burdens for companies. Additionally, the Medium Combustion Plant Directive (MCPD) requires all gensets above 1 MW to adhere to emission thresholds. According to the Wood Mackenzie, compliance costs have increased by 18% since 2020 is impacting profit margins. These regulations disproportionately affect diesel-powered gensets, which account for over 60% of the market, as they emit higher levels of nitrogen oxides and particulate matter.

High Initial Investment Costs

The high initial investment required for commercial gensets acts as a deterrent for small and medium-sized enterprises (SMEs) is limiting market expansion. According to McKinsey & Company, the average cost of a commercial genset ranges from €5,000 to €500,000 by depending on capacity and fuel type. This significant upfront expense is exacerbated by additional costs associated with installation, maintenance, and fuel procurement. For instance, a genset operating on natural gas may incur annual maintenance costs of up to €2,000, as per a study by Ernst & Young. Furthermore, the economic uncertainty following the COVID-19 pandemic has tightened budgets for many businesses, reducing their willingness to invest in capital-intensive equipment. In 2022, SMEs accounted for 99% of all businesses in Europe but contributed only 15% to the genset market with the impact of financial constraints.

MARKET OPPORTUNITIES

Growing Adoption of Smart Gensets

The integration of smart technologies into commercial gensets presents a lucrative opportunity for market growth in Europe. Smart gensets, equipped with IoT-enabled sensors and AI-driven analytics, offer real-time monitoring, predictive maintenance, and remote-control capabilities. According to a study by Capgemini, the adoption of smart gensets could reduce maintenance costs by up to 30% while improving operational efficiency by 20%. This technological advancement aligns with Europe’s push toward Industry 4.0, where interconnected systems play a crucial role in enhancing productivity. For instance, in 2023, Siemens launched a range of smart gensets tailored for data centers by enabling seamless integration with existing infrastructure. Additionally, the European Commission’s Digital Decade initiative aims to achieve 100% coverage of gigabit connectivity by 2030 that is further driving demand for smart power solutions. Countries like Germany and France are at the forefront of this transition, with over 40% of new genset installations featuring smart capabilities.

Expansion into Emerging Markets

Emerging markets within Europe, particularly in Eastern and Southern regions, present untapped potential for the commercial gensets market. According to Deloitte, countries like Turkey and Poland are experiencing rapid industrialization, with GDP growth rates exceeding 4% annually. This economic expansion is accompanied by increased energy consumption, creating a surge in demand for reliable power solutions. For example, Turkey’s energy demand grew by 7% in 2022, as reported by the Turkish Electricity Transmission Corporation. Moreover, infrastructure development projects, such as the Belt and Road Initiative, are driving investments in power generation and distribution systems. Manufacturers can capitalize on this opportunity by offering cost-effective and energy-efficient gensets tailored to the unique needs of these markets.

MARKET CHALLENGES

Intense Market Competition

The European commercial gensets market is characterized by intense competition by posing a significant challenge for manufacturers striving to maintain market share. According to a report by Boston Consulting Group, over 50 major players operate in the region by including global giants like Caterpillar and Cummins, as well as regional firms specializing in niche products. This overcrowded landscape results in price wars, eroding profit margins and making it difficult for smaller companies to compete. For instance, in 2022, the average selling price of diesel gensets dropped by 8% due to aggressive pricing strategies adopted by key players. Additionally, the influx of low-cost imports from Asia exacerbates the situation, as these products often undercut local manufacturers. A study by Roland Berger reveals that Chinese imports accounted for 15% of the European genset market in 2021, further intensifying competition.

Fluctuating Fuel Prices

Fluctuating fuel prices represent a persistent challenge for the commercial gensets market, particularly for diesel-powered units. According to the European Central Bank, crude oil prices surged by 40% in 2022 due to geopolitical tensions and supply chain disruptions. This volatility directly impacts the operational costs of gensets, as fuel expenses constitute a significant portion of total expenditures. For example, a diesel genset operating continuously for 10 hours consumes approximately 200 liters of fuel, translating to substantial monthly costs. According to the KPMG, rising fuel prices have led to a 12% decline in genset rentals in Southern Europe, where businesses are increasingly opting for alternative energy solutions. Furthermore, the unpredictability of fuel costs complicates budgeting for end-users in sectors like retail and hospitality, where profit margins are already narrow. Manufacturers must address this challenge by promoting hybrid and gas-powered gensets, which offer greater cost stability.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

6.16% |

|

Segments Covered |

By Power Rating, Fuel Types, End-Use, and Region |

|

Various Analyses Covered |

Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled |

Briggs & Stratton, SDMO, Generac, Yamaha Motor, Powerica, Himoinsa, Caterpillar, Ingersoll Rand, Mitsubishi Power, Wärtsilä, Siemens and Huu Toan Group, and others. |

SEGMENTAL ANALYSIS

By Power Rating Insights

The ≤ 50 kVA segment dominated the European commercial gensets market by capturing 45.7% of the total share in 2024. This segment’s prominence is attributed to its widespread adoption in small-scale enterprises, retail outlets, and residential complexes. The affordability and compact design of these gensets make them an attractive choice for businesses with limited space and budget constraints. According to Eurostat, SMEs account for 99% of all businesses in Europe is driving demand for cost-effective power solutions. Additionally, the proliferation of microgrids and decentralized energy systems has bolstered the popularity of ≤ 50 kVA gensets in rural areas where grid connectivity is unreliable. For instance, in 2021, Italy recorded a 10% increase in microgrid installations, with gensets serving as a critical component of these systems. Government initiatives promoting energy independence further amplify demand, as businesses seek to mitigate risks associated with centralized power grids.

The > 330 kVA - 750 kVA segment is likely to show up with a prominent CAGR of 7.2% throughout the forecast period. This growth is fueled by the expanding infrastructure and industrial sectors, which require high-capacity gensets to meet their energy demands. For example, the construction of large-scale data centers in Germany and the Netherlands has significantly increased demand for gensets in this power range. A study by McKinsey & Company reveals that data centers consume approximately 3% of Europe’s total electricity, necessitating robust backup systems. Furthermore, the rise of electric vehicle (EV) charging stations across Europe has created new opportunities for high-capacity gensets. By 2025, the EU aims to install 1 million public EV chargers, as per the European Automobile Manufacturers' Association, driving demand for reliable power sources. Technological advancements, such as improved fuel efficiency and reduced emissions, have also enhanced the appeal of > 330 kVA - 750 kVA gensets is positioning them as a key growth driver.

By Fuel Types Insights

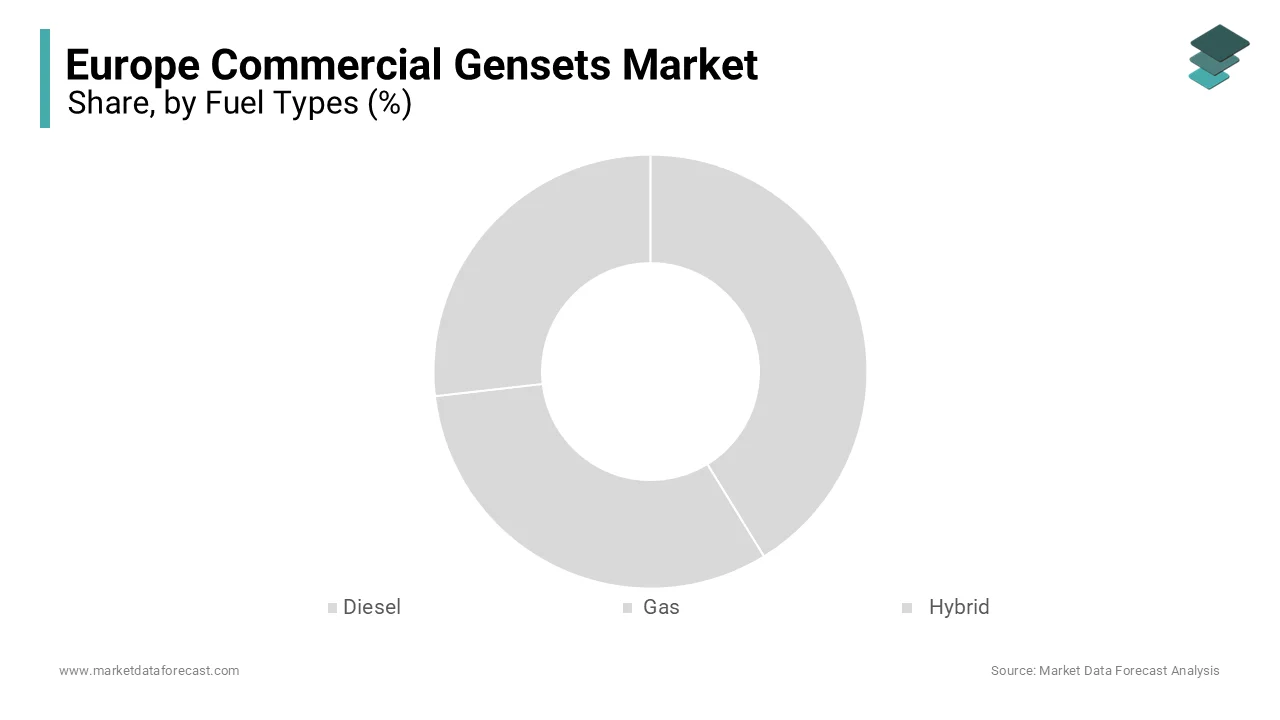

The diesel segment was the largest by occupying 60.1% of the European commercial gensets market share in 2024. Their prevalence is driven by their reliability, durability, and ability to deliver high power output, making them ideal for industrial applications. The European Industrial Association reports that diesel gensets are widely used in sectors such as manufacturing, mining, and construction, where uninterrupted power supply is critical. Additionally, diesel fuel’s widespread availability and relatively lower cost compared to alternatives like natural gas or hydrogen contribute to its dominance. For instance, in 2021, diesel accounted for 35% of Europe’s total fuel consumption, as per the European Fuel Quality Directive. Despite environmental concerns, advancements in emission control technologies have enabled diesel gensets to comply with stringent regulations by ensuring their continued relevance.

The hybrid segment is anticipated to witness a CAGR of 8.5% throughout the forecast period. This growth is fueled by the increasing adoption of renewable energy and the need for sustainable power solutions. Hybrid gensets integrate traditional fuel sources with renewable energy systems, such as solar panels or wind turbines by offering a balance between reliability and environmental responsibility. The European Green Deal has allocated €1 trillion to support clean energy initiatives, encouraging businesses to transition to hybrid technologies. For example, in 2022, Sweden witnessed a 25% increase in hybrid genset installations, driven by government subsidies and corporate sustainability goals. According to the PwC, hybrid gensets can reduce carbon emissions by up to 40% compared to conventional models by making them an attractive option for environmentally conscious consumers.

By End-Use Insights

The data centers segment was accounted in holding 25.5% of the European commercial gensets market in 2024. The exponential growth of digital services, cloud computing, and AI applications has driven the expansion of data centers across Europe. According to Eurostat, the number of hyperscale data centers in Europe increased by 30% between 2018 and 2022 by necessitating robust backup power systems. Gensets play a critical role in ensuring uninterrupted power supply, as even a brief outage can result in significant financial losses and data corruption. For instance, in 2021, a power outage at a major data center in Frankfurt caused estimated damages of €10 million with the importance of reliable backup solutions. Furthermore, the EU’s Digital Decade initiative aims to achieve 100% gigabit connectivity by 2030, further boosting demand for gensets in this segment.

The telecom sector is projected to register a CGAR of 7.8% in the next coming years. This growth is driven by the rapid deployment of 5G networks and the expansion of rural connectivity. According to the European Telecommunications Network Operators’ Association, over 200,000 new 5G base stations are expected to be installed by 2025, each requiring reliable backup power to ensure seamless communication. Additionally, the increasing frequency of natural disasters and cyberattacks has amplified the need for resilient telecom infrastructure. For example, in 2022, a series of storms in Northern Europe disrupted power supply to thousands of telecom towers, prompting operators to invest in gensets. According to the McKinsey & Company, telecom companies are prioritizing energy-efficient gensets to reduce operational costs and align with sustainability goals.

REGIONAL ANALYSIS

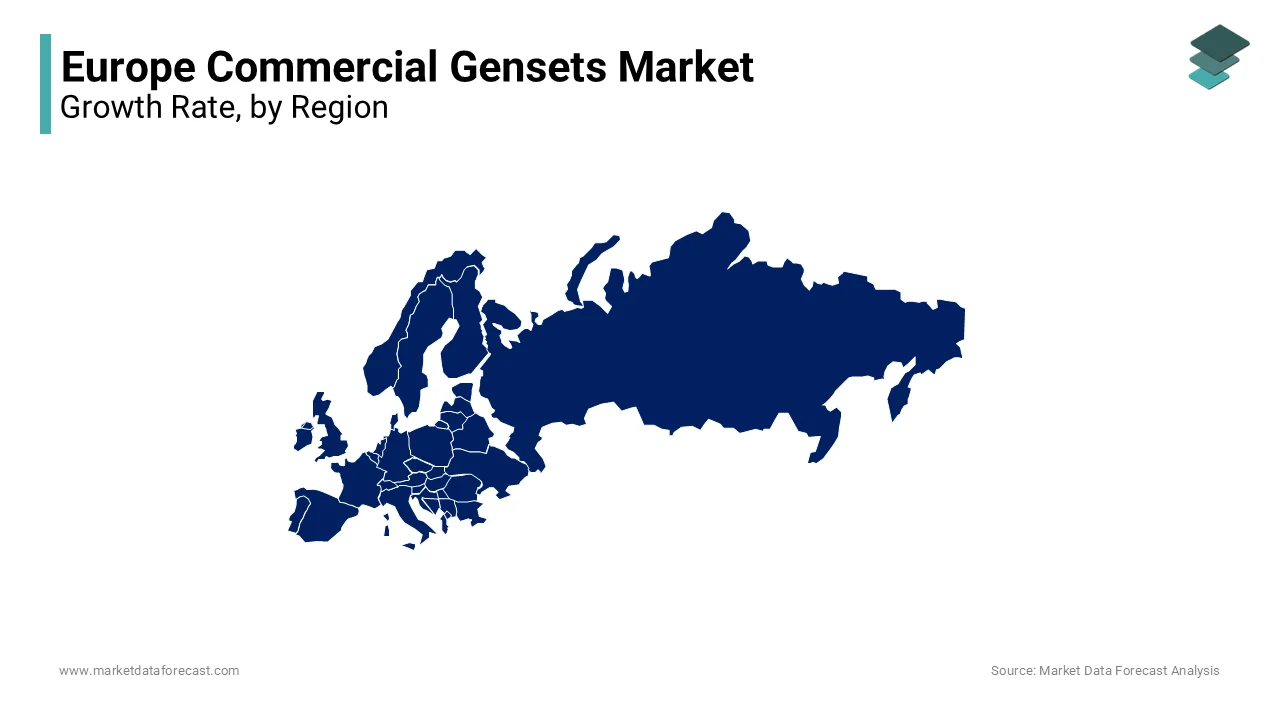

Germany commercial gensets market held a dominant share of 22.3% in 2024 owing to the presence of robust industrial base and stringent regulations ensuring uninterrupted power supply in critical infrastructure drive demand for gensets. According to the Federal Ministry for Economic Affairs and Climate Action, Germany’s manufacturing sector accounts for 23% of its GDP, necessitating reliable backup power solutions. Additionally, the country’s dominance in renewable energy integration, with renewables contributing 46% of electricity generation in 2022, has spurred demand for hybrid gensets. For instance, in 2021, Siemens partnered with local utilities to deploy hybrid gensets in rural areas is addressing grid instability issues.

The UK is likely to grow with an anticipated CAGR of 12.7% during the forecast period. The country’s focus on smart city initiatives and digital transformation drives demand for gensets. According to the UK Department for Business, Energy & Industrial Strategy, investments in smart infrastructure exceeded £10 billion in 2022. The expansion of 5G networks and data centers further amplifies demand, with London hosting over 80 data centers. For example, in 2021, Equinix installed high-capacity gensets in its London facility to support growing cloud computing needs.

France commercial gensets market is growing steadily owing to its strong healthcare and telecommunications sectors. According to the French Ministry of Health, the healthcare sector’s power consumption increased by 12% in 2022, necessitating reliable backup systems. Additionally, the rollout of 5G networks across major cities has boosted demand for gensets. For instance, Orange SA invested in gensets to support its 5G infrastructure in Paris. According to Deloitte, France’s commitment to renewable energy also supports hybrid genset adoptio

TOP PLAYERS IN THIS MARKET

Caterpillar Inc.

Caterpillar Inc. is a global leader in the commercial gensets market, renowned for its innovative and durable products. The company offers a wide range of gensets, from portable units to high-capacity systems by catering to diverse industries such as mining, construction, and healthcare. Caterpillar’s commitment to sustainability is evident in its development of hybrid gensets, which combine traditional fuel sources with renewable energy systems. The company’s extensive dealer network ensures prompt service and support by enhancing customer satisfaction.

Cummins Inc.

Cummins Inc. is a key player in the European commercial gensets market, known for its high-performance and energy-efficient products. The company’s gensets are widely used in data centers, telecommunications, and industrial applications. Cummins has made significant investments in R&D to develop low-emission gensets that comply with stringent EU regulations. Its focus on digitalization has led to the introduction of smart gensets equipped with IoT-enabled sensors by enabling real-time monitoring and predictive maintenance.

Kohler Co.

Kohler Co. is a prominent manufacturer of commercial gensets, offering innovative solutions tailored to the needs of various sectors. The company’s gensets are designed for reliability and ease of use, making them ideal for small-scale enterprises and residential complexes. Kohler’s commitment to sustainability is reflected in its development of hybrid and gas-powered gensets, which align with Europe’s green energy goals. The company’s strategic partnerships with local distributors ensure widespread market penetration.

TOP STRATEGIES USED BY KEY MARKET PLAYERS

Product Innovation

Key players in the European commercial gensets market are investing heavily in product innovation to stay ahead of competitors. For instance, in March 2023, Caterpillar launched a new line of hybrid gensets featuring advanced emission control technologies. These products cater to the growing demand for sustainable power solutions, aligning with EU regulations.

Strategic Partnerships

Strategic partnerships are a cornerstone of market success, enabling companies to expand their reach and enhance product offerings. In June 2023, Cummins partnered with a leading European utility provider to deploy smart gensets in urban areas by supporting smart city initiatives.

Geographic Expansion

Geographic expansion is another key strategy adopted by market leaders to tap into emerging markets. In January 2024, Kohler established a new manufacturing facility in Poland by targeting the rapidly growing industrial sector in Eastern Europe.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Briggs & Stratton, SDMO, Generac, Yamaha Motor, Powerica, Himoinsa, Caterpillar, Ingersoll Rand, Mitsubishi Power, Wärtsilä, Siemens and Huu Toan Group are playing dominating role in the Europe commercial gensets market.

The European commercial gensets market is highly competitive, characterized by the presence of both global giants and regional players. According to a report by Boston Consulting Group, over 50 major companies operate in the region, competing on factors such as product quality, pricing, and technological innovation. Global leaders like Caterpillar and Cummins dominate the market, leveraging their extensive R&D capabilities and distribution networks. Regional players, on the other hand, focus on niche markets, offering specialized products tailored to local needs. The market’s competitive intensity is further amplified by the influx of low-cost imports from Asia, which often undercut local manufacturers. To differentiate themselves, companies are increasingly investing in smart technologies and sustainable solutions by aligning with Europe’s green energy goals.

RECENT HAPPENINGS IN THE MARKET

- In April 2023, Caterpillar acquired a German-based startup specializing in hybrid genset technologies, enhancing its product portfolio and strengthening its market position.

- In June 2023, Cummins partnered with Orange SA to deploy smart gensets in France, supporting the expansion of 5G networks and bolstering its presence in the telecom sector.

- In August 2023, Kohler launched a new line of eco-friendly gensets in Italy, targeting the growing demand for sustainable power solutions in rural areas.

- In December 2023, Siemens introduced IoT-enabled gensets in Sweden, enabling real-time monitoring and predictive maintenance, and reinforcing its leadership in smart technologies.

- In February 2024, Rolls-Royce announced the establishment of a new manufacturing facility in Poland, targeting the burgeoning industrial sector in Eastern Europe and expanding its geographic footprint.

MARKET SEGMENTATION

This research report on the Europe commercial gensets market is segmented and sub-segmented into the following categories.

By Power Rating

- ≤ 50 kVA

- 50 kVA - 125 kVA

- 125 kVA - 200 kVA

- 200 kVA - 330 kVA

- 330 kVA - 750 kVA

- 750 kVA

By Fuel Types

- Diesel

- Gas

- Hybrid

By End-Use

- Data centers

- Telecom

- Healthcare

- Commercial complex

- Construction

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the projected market size of the Europe Commercial Gensets Market by 2033?

The Europe Commercial Gensets market is estimated to reach USD 8.03 billion by 2033.

2. What factors are driving the growth of the Europe Commercial Gensets Market?

Key drivers include increasing power outages, demand for reliable backup power, and expanding infrastructure projects across Europe.

3. Which industries contribute significantly to the demand for commercial gensets in Europe?

Major industries include healthcare, data centers, manufacturing, and construction sectors requiring dependable power solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]