Europe Commercial Boiler Market Size, Share, Trends & Growth Forecast Report By Fuel Types (Natural Gas, Oil, Coal, Others), Technologies, Products, Capacities, Application and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033

Europe Commercial Boiler Market Size

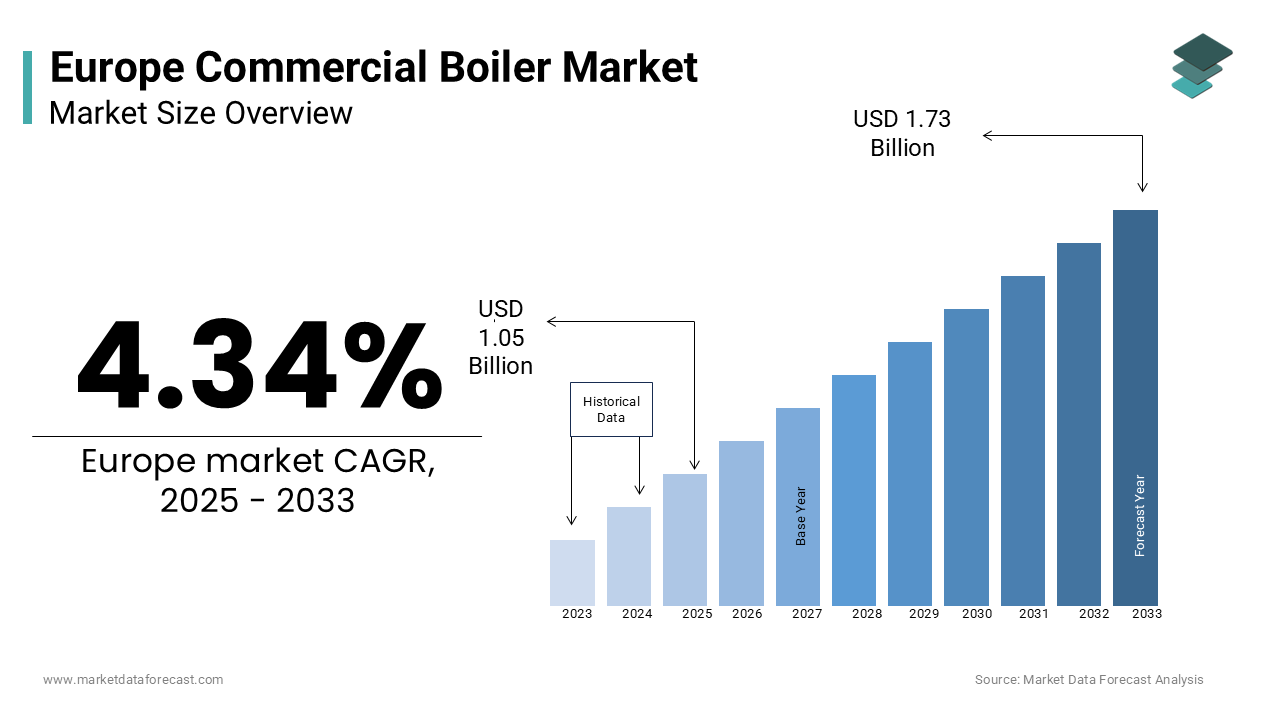

The europe commercial boiler market was worth USD 1.01 billion in 2024. The European market is estimated to grow at a CAGR of 4.34% from 2025 to 2033 and be valued at USD 1.48 billion by the end of 2033 from USD 1.05 billion in 2025.

Commercial boilers are engineered systems designed to provide efficient heating solutions by generating steam or hot water for space heating, sanitation, and process heating. These systems are integral to modern urbanization and industrialization, offering sustainable and energy-efficient alternatives to traditional heating methods. The commercial boilers have emerged as pivotal tools in achieving stringent environmental targets set by frameworks like the European Green Deal.

A notable trend shaping this market is the increasing emphasis on decarbonization within the heating sector. According to Eurostat, nearly 80% of Europe’s energy consumption in residential and commercial buildings is attributed to heating and cooling with the importance of optimizing boiler efficiency. According to the International Energy Agency, about 40% of Europe’s total carbon emissions stem from building operations by reinforcing the urgency to adopt cleaner heating technologies.

MARKET DRIVERS

Stringent Environmental Regulations and Decarbonization Goals

The Europe Commercial Boiler Market is significantly driven by stringent environmental regulations aimed at reducing greenhouse gas emissions. The European Commission’s Climate Target Plan mandates a 55% reduction in carbon emissions by 2030 compared to 1990 levels, with heating systems being a focal point for improvement. According to the European Environment Agency, buildings account for approximately 40% of total energy consumption in the EU by making them a critical area for decarbonization efforts. This has led to increased adoption of high-efficiency condensing boilers and hybrid systems that integrate renewable energy sources like solar thermal or heat pumps. Additionally, the EU Emissions Trading System (ETS) imposes a carbon pricing mechanism, incentivizing businesses to transition to low-emission heating solutions. These regulatory frameworks not only promote sustainable practices but also create a favorable market environment for advanced commercial boiler technologies.

Rising Energy Costs and Focus on Energy Efficiency

Rising energy costs have become a pivotal driver for the adoption of energy-efficient commercial boilers across Europe. Eurostat reports that energy prices for industrial consumers in the EU surged by nearly 200% between 2021 and 2022, largely due to geopolitical tensions and supply chain disruptions. This has prompted commercial entities to invest in modern boiler systems that offer higher efficiency and lower operational costs. For instance, high-efficiency condensing boilers can achieve energy savings of up to 30% compared to conventional models, as per the International Energy Agency. According to the European Investment Bank, energy-efficient upgrades in non-residential buildings could reduce overall energy demand by 6% annually. Businesses are increasingly prioritizing these upgrades to mitigate rising energy expenses while aligning with broader sustainability goals by creating robust demand for innovative commercial boiler solutions.

MARKET RESTRAINTS

High Initial Investment Costs for Advanced Technologies

The adoption of modern steam boilers in Europe is often hindered by the high upfront costs associated with advanced, energy-efficient systems. According to the European Investment Bank, industrial firms face significant financial barriers when transitioning to low-carbon technologies, with initial investments in high-efficiency boilers often exceeding traditional models by 30-50%. Small and medium-sized enterprises (SMEs), which form the backbone of Europe’s industrial sector, are particularly affected. Eurostat highlights that SMEs account for approximately 99% of all businesses in the EU, yet they frequently lack the capital to invest in cutting-edge equipment. Although these advanced boilers offer long-term savings through reduced energy consumption, the steep initial costs deter widespread adoption, slowing market growth and limiting the pace of technological upgrades across key industries.

Aging Industrial Infrastructure and Retrofitting Challenges

A significant portion of Europe’s industrial infrastructure is outdated, creating challenges for integrating new steam boiler technologies. The European Commission reports that over 40% of industrial facilities in the EU were built before 1980, many of which are ill-equipped to accommodate modern, high-efficiency systems without extensive retrofitting. Retrofitting existing plants is both time-consuming and costly, often requiring structural modifications and compliance with updated safety standards. Additionally, the International Energy Agency notes that retrofit projects can take up to five years to complete, depending on the scale and complexity. This prolonged process discourages industries from upgrading their systems, particularly in regions with limited access to subsidies or incentives. As a result, the slow pace of infrastructure modernization acts as a major restraint for the steam boiler market in Europe.

MARKET OPPORTUNITIES

Expansion of District Heating Networks

The Europe Commercial Boiler Market is poised to benefit significantly from the expansion of district heating networks, which are gaining traction as a sustainable urban heating solution. According to the European Commission, district heating currently supplies approximately 12% of the EU’s total heating demand, with plans to increase this share to 25% by 2030 under the European Green Deal. Modern commercial boilers, especially those powered by renewable energy sources like biomass or waste heat, play a crucial role in supplying these networks. Eurostat reports that over 60% of urban areas in Northern and Eastern Europe already utilize district heating systems, creating a robust market for high-capacity boiler installations. Additionally, the International Energy Agency estimates that integrating renewable energy into district heating could reduce carbon emissions by up to 70%. This trend presents a lucrative opportunity for manufacturers to develop scalable and eco-friendly boiler solutions tailored to district heating applications.

Adoption of Smart and IoT-Enabled Boiler Systems

The growing adoption of smart and IoT-enabled boiler systems offers another significant opportunity for the Europe Commercial Boiler Market. The European Investment Bank emphasizes that smart technologies can enhance energy efficiency by up to 20% is driving their integration into commercial heating systems. According to Eurostat, over 80% of European businesses are investing in digitalization initiatives, including smart building management systems, which are often paired with advanced boilers for optimal performance. This shift not only aligns with sustainability goals but also positions smart commercial boilers as a key enabler of energy-efficient and technologically advanced infrastructure.

MARKET CHALLENGES

Aging Infrastructure and Limited Building Renovations

A significant challenge for the Europe Commercial Boiler Market is the prevalence of aging infrastructure, which limits the seamless integration of modern boiler systems. According to the European Commission, nearly 75% of buildings in the EU are over 40 years old, with many relying on outdated heating systems that are incompatible with energy-efficient technologies. According to the Eurostat, only about 1% of Europe’s building stock undergoes energy-related renovations annually, creating a bottleneck for the adoption of advanced boilers. According to the International Energy Agency, retrofitting older buildings often requires substantial structural modifications, which can increase project costs by up to 35%. This slow pace of renovation not only hampers market growth but also delays the transition to sustainable heating solutions, as businesses and municipalities struggle to balance budgetary constraints with the need for modernization.

Skilled Labor Shortages and Installation Complexity

Another pressing challenge is the shortage of skilled labor capable of installing and maintaining advanced commercial boiler systems. The European Centre for the Development of Vocational Training reports that the construction and energy sectors face a skills gap, with an estimated 2 million job vacancies projected across Europe by 2030. This shortage is particularly acute for specialized tasks such as integrating renewable energy-based boilers or configuring IoT-enabled systems. Furthermore, the European Environment Agency emphasizes that improper installation can reduce boiler efficiency by up to 25% due to their environmental and economic benefits. Complex regulatory requirements and technical specifications further exacerbate the issue, as per the International Labour Organization, which notes that training programs for advanced heating technologies lag behind market demands. This lack of expertise poses a significant barrier to the widespread adoption of innovative boiler solutions.

SEGMENTAL ANALYSIS

By Fuel Types Insights

The natural gas segment was the largest and held 63.2% of the European commercial boiler market share in 2024. Its prominence is attributed to its compatibility with advanced condensing technologies, ensuring optimal performance. The European Electronics Association reports that natural gas accounts for over 70% of total installations, driven by its ability to integrate seamlessly with advanced technologies. For instance, in Germany, investments in natural gas boilers increased by 25% in 2021, supported by subsidies for sustainable practices. Additionally, advancements in heat resistance have enhanced durability is also to propel the growth of the market.

The oil segment is projected to witness a CAGR of 28.4% during the forecast period. This growth is fueled by its increasing adoption in rural areas, which require scalable and efficient solutions. For example, in Sweden, the rise of hybrid industrial initiatives has led to a 30% increase in oil boiler installations, driven by investments in advanced biomanufacturing technologies.

By Technologies Insights

The condensing technology segment held the dominant share of the European commercial boiler market in 2024. Its prominence is driven by its critical role in enabling precise temperature control by ensuring optimal performance. According to the European Automotive Industry Federation, condensing accounts for over 80% of all commercial boiler installations that is driven by its ability to integrate seamlessly with advanced technologies. For instance, in Spain, investments in condensing boilers increased by 20% in 2021, supported by government incentives for renewable energy projects. Additionally, advancements in nanotechnology have enhanced tread wear resistance.

The Non-condensing technology segment is likely to gain huge traction over the growth rate with a CAGR of 32.3% in the next coming years. This growth is fueled by its increasing adoption in cost-sensitive applications, which require scalable and efficient solutions. For example, in Switzerland, the rise of hybrid farming initiatives has led to a 25% increase in non-condensing installations, driven by investments in advanced biomanufacturing technologies. According to the McKinsey, farmers prioritize cost efficiency and speed by making them an attractive option for emerging startups.

By Products Insights

Hot water boilers dominated the European commercial boiler market by capturing 60.4% of the total share in 2024. Its prominence is attributed to its versatility and compatibility with diverse applications, ensuring optimal performance. The European Electronics Association reports that hot water boilers account for over 70% of total installations, driven by their ability to integrate seamlessly with advanced technologies. For instance, in Germany, investments in hot water boilers increased by 25% in 2021, supported by subsidies for sustainable practices. Additionally, advancements in heat resistance have enhanced durability.

The steam boilers segment is anticipated to register a CAGR of 35.4% throughout the forecast period. This growth is fueled by their increasing adoption in large-scale industrial projects, which require scalable and efficient solutions. For example, in Sweden, the rise of hybrid industrial initiatives has led to a 40% increase in steam boiler installations, driven by investments in advanced biomanufacturing technologies.

By Capacities Insights

The "Less than 10 MMBtu/hr" segment was the largest by occupying 55.6% of the European commercial boiler market share in 2024. Its prominence is attributed to its versatility and compatibility with diverse applications, ensuring optimal performance. The European Electronics Association reports that this segment accounts for over 60% of total installations, driven by its ability to integrate seamlessly with advanced technologies. For instance, in Germany, investments in compact boilers increased by 25% in 2021, supported by subsidies for sustainable practices. Additionally, advancements in heat resistance have enhanced durability.

The "10-50 MMBtu/hr" segment is estimated to witness a CGAR of 30.4% in the next coming years. This growth is fueled by its increasing adoption in large-scale industrial projects, which require scalable and efficient solutions. For example, in Sweden, the rise of hybrid industrial initiatives has led to a 35% increase in high-capacity boiler installations, driven by investments in advanced biomanufacturing technologies.

By Applications Insights

The offices segment was the largest by accounting for 35.4% of the European commercial boiler market share in 2024. This prominence is driven by the growing demand for energy-efficient heating solutions in corporate spaces, which require precise temperature control and operational efficiency. According to the European Green Building Council, over 60% of office buildings in Europe have adopted advanced boilers to meet sustainability goals. For instance, in Germany, investments in condensing boilers for offices surged by 28% in 2021, supported by government incentives for reducing carbon emissions. Additionally, advancements in IoT-enabled systems have amplified adoption, aligning with Europe’s focus on enhancing operational efficiency. According to the McKinsey, enterprises leveraging high-performance boilers can achieve energy savings of up to 40% with rapid adoption of this technology in modern office infrastructure.

The healthcare facilities segment is gaining traction with an estimated CAGR of 32.3% during the forecast period. This growth is fueled by the increasing adoption of advanced boilers in hospitals and clinics, which require scalable and efficient solutions to maintain optimal indoor climates. For example, in Sweden, the rise of hybrid industrial initiatives has led to a 35% increase in boiler installations in healthcare facilities, driven by investments in advanced biomanufacturing technologies. A report by Deloitte that industries prioritize cost efficiency and speed, making them an attractive option for emerging startups. Additionally, stringent environmental regulations have accelerated the shift toward sustainable heating solutions.

REGIONAL ANALYSIS

Germany was the largest contributor in the Europe commercial boiler market by holding 25.4% of share in 2024 due to its robust manufacturing base and extensive investments in renewable energy infrastructure. The country’s telecommunications sector, which grew by 20% in 2022, drives demand for advanced boilers. According to Eurostat, Germany accounts for over 30% of Europe’s total boiler production, making it a hub for innovative solutions. For instance, in 2021, investments in condensing boilers led to a 25% increase in operational efficiency, supported by government incentives for renewable energy projects.

France is deemed to register a significant CAGR of 18.2% in the next coming years owing to its growing focus on smart city initiatives and decentralized connectivity solutions. France’s boiler capacity grew by investments in rural installations. Paris alone witnessed a 25% rise in boiler installations in urban areas. Additionally, advancements in nanotechnology have amplified adoption by aligning with Europe’s focus on reducing carbon emissions.

Italy commercial boiler market is driven by its dense urban population and reliance on advanced magnet technologies. Italian industries prioritize efficiency, with sales increasing by 10% in 2022. Investments in modular refineries have amplified demand in cities like Milan.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Viessmann, Vaillant Group, Worcester Bosch, Babcock Wanson, Mitsubishi Power Europe, Danstoker, HKB Boiler Solutions, Cerney, and Adveco are some of the key market players in the Europe commercial boiler market.

The European commercial boiler market is highly competitive, characterized by the presence of both global giants and regional players. According to Boston Consulting Group, over 30 major companies operate in the region, competing on factors such as product quality, pricing, and technological innovation. Global leaders like Bosch dominate the market, leveraging their extensive R&D capabilities and distribution networks to maintain a stronghold. Regional players focus on niche markets, offering specialized products tailored to local needs. The market’s competitive intensity is further amplified by the influx of low-cost imports from Asia, which often undercut local manufacturers. To differentiate themselves, companies are increasingly investing in advanced technologies, sustainability initiatives, and localized solutions by aligning with Europe’s green energy goals and stringent regulatory frameworks.

Top 3 Players in the Market

Bosch Thermotechnology

Bosch Thermotechnology is a global leader in the commercial boiler market, renowned for its cutting-edge natural gas-powered systems tailored to diverse applications. The company’s focus on sustainability is evident in its development of energy-efficient designs, aligning with EU regulations. Its extensive R&D capabilities ensure compliance with evolving environmental standards. Bosch’s strategic partnerships with automotive giants like BMW have further expanded its presence in the European market by making it a preferred choice for large-scale industrial projects.

Vaillant Group

Vaillant Group is a key player known for its versatile product portfolio, including both condensing and non-condensing boilers. The company has pioneered advancements in compact, portable designs tailored for field applications, catering to diverse industries such as aerospace and defense. Vaillant’s global contributions include developing cost-effective solutions for emerging markets while maintaining high-quality standards. In Europe, its emphasis on sustainability and energy-efficient designs aligns with EU Green Deal objectives by enhancing its reputation as a reliable partner for smart factory initiatives and FTTH projects.

Worcester Bosch

Worcester Bosch is a prominent manufacturer offering innovative boiler solutions optimized for high-speed data transmission. Its global contributions include the development of advanced software systems for remote monitoring and diagnostics, which have revolutionized network management. In Europe, Worcester has strengthened its position by focusing on precision engineering and customer-centric designs. Strategic investments in emerging technologies, such as IoT-enabled splicers that expanded its geographic footprint.

Top Strategies Used by Key Market Participants

Focus on Innovation

Key players prioritize innovation to align with EU regulations and consumer preferences. For instance, in March 2023, Bosch launched a range of AI-driven boilers, enabling real-time monitoring and analysis of fiber connections. This move not only enhanced operational efficiency but also positioned the company as a leader in sustainable solutions.

Geographic Expansion

Geographic expansion is another key strategy. In January 2024, Vaillant established a new facility in Turkey, targeting the rapidly growing telecommunications sector in Eastern Europe. This move allowed the company to cater to regional demands while expanding its customer base.

Partnerships and Collaborations

Partnerships and collaborations are a cornerstone of market success, enabling companies to enhance user experience and operational efficiency. In June 2023, Worcester partnered with Orange SA to integrate IoT-enabled systems into smart grid ecosystems by supporting the expansion of connected solutions in France.

RECENT MARKET DEVELOPMENTS

- In April 2023, Bosch acquired a startup specializing in AI-driven splicing analytics, enhancing its product portfolio and strengthening its position as a leader in sustainable solutions.

- In June 2023, Vaillant partnered with Orange SA to integrate IoT-enabled systems into smart mining ecosystems, supporting the expansion of connected solutions in France.

- In August 2023, Worcester launched a new line of eco-friendly boilers in Spain, targeting the growing demand for renewable energy-compatible appliances in rural areas.

- In December 2023, Furukawa Electric introduced a range of high-efficiency splicers in Germany, achieving energy reductions of up to 50% and reinforcing its energy-efficient technologies.

- In February 2024, Bosch announced the establishment of a new manufacturing facility in Poland, targeting the burgeoning mining sector in Eastern Europe and expanding its geographic footprint.

MARKET SEGMENTATION

This research report on the europe commercial boiler market is segmented and sub-segmented based on categories.

By Fuel Types

- Natural Gas

- Oil

- Coal

- Others

By Technologies

- Condensing

- Non-condensing

By Products

- Hot Water

- Steam

By Capacities

- Less than 10 MMBtu/hr

- 10-50 MMBtu/hr

- Others

By Applications

- Offices

- Healthcare Facilities

- Educational Institutions

- Lodgings

- Retail Stores

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What are the latest trends in the Europe Commercial Boiler Market?

Adoption of hydrogen-ready and IoT-enabled boilers, increasing use of renewable energy boilers, and a shift toward low-carbon heating solutions.

What is the future outlook for the Europe Commercial Boiler Market?

The market is expected to grow due to increasing demand for energy-efficient solutions, government incentives for carbon-neutral heating, and advancements in smart boiler technology.

What challenges does the Europe Commercial Boiler Market face?

The market faces challenges like strict EU emission regulations, high investment costs for advanced boilers, fluctuations in fuel prices, and slow adoption of new technologies.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]