Europe Cell Line Development Market Size, Share, Trends & Growth Forecast Report By Product & Services (Reagents & media, Equipment, Accessories and consumables, Services ), Source, Cell Line, Application, End-Use and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033

Europe Cell Line Development Market Size

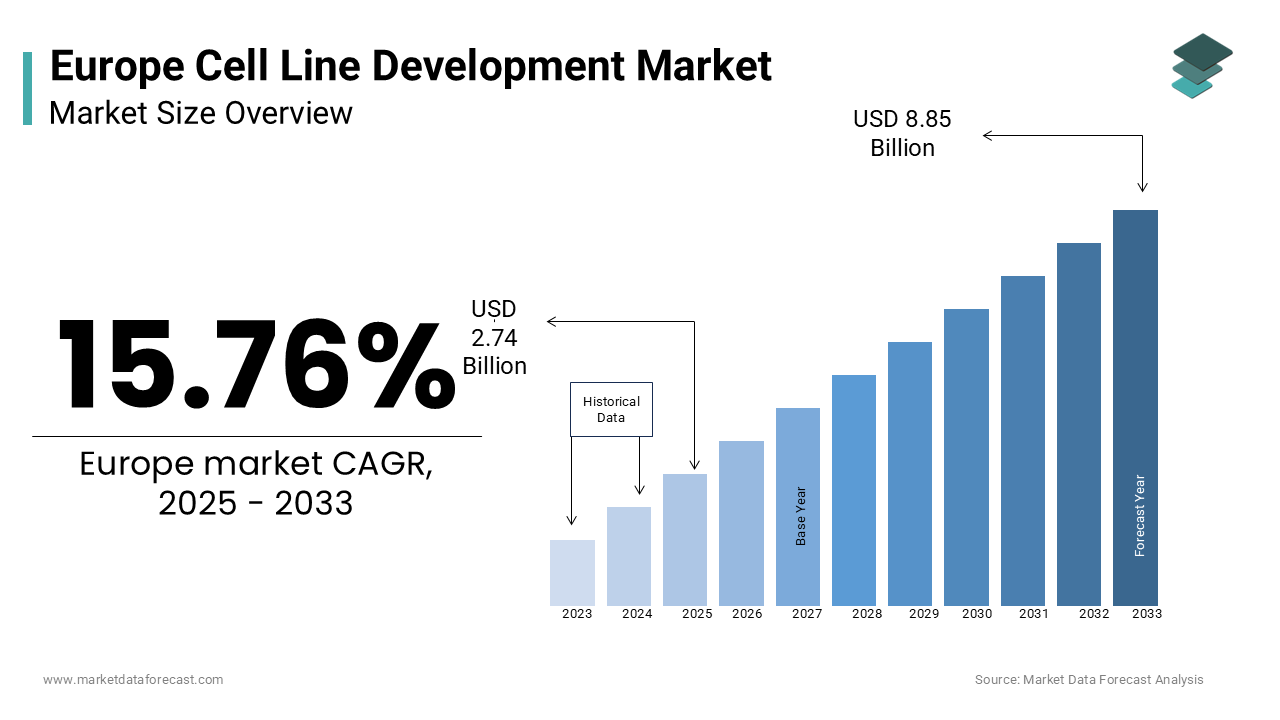

The europe cell line development market was worth USD 2.37 billion in 2024. The European market is estimated to grow at a CAGR of 15.76% from 2025 to 2033 and be valued at USD 8.85 billion by the end of 2033 from USD 2.74 billion in 2025.

Cell line development involves the creation and optimization of stable cell lines used in the production of biologics, vaccines, and other therapeutic agents. According to the European Biotechnology Industry Organization, the market is driven by the increasing demand for monoclonal antibodies, recombinant proteins, and gene therapies, which rely heavily on robust and scalable cell lines. The European Medicines Agency underscores that over 30% of approved biologics are produced using mammalian cell lines, reflecting their critical role in biopharmaceutical manufacturing. Additionally, advancements in genome editing technologies, such as CRISPR-Cas9, have revolutionized cell line engineering, enabling precise modifications to enhance productivity and stability. Eurostat reports that investments in biotechnology R&D across Europe exceeded €30 billion in 2022, with significant portions allocated to cell line development initiatives.

MARKET DRIVERS

Increasing Demand for Biologics and Monoclonal Antibodies

The surging demand for biologics and monoclonal antibodies is majorly boosting the growth of the European cell line development market. According to the European Federation of Pharmaceutical Industries and Associations, biologics accounted for over 30% of the total pharmaceutical market revenue in Europe in 2022, with monoclonal antibodies representing the largest segment within this category. The European Medicines Agency highlights that approximately 70% of all biologics are manufactured using mammalian cell lines, underscoring their indispensability in therapeutic production. For instance, the global market for monoclonal antibodies is projected to grow at a compound annual growth rate (CAGR) of 5.3% over the forecast period due to their efficacy in treating cancer, autoimmune disorders, and infectious diseases. Additionally, the COVID-19 pandemic has accelerated the adoption of biologics, with vaccines and antibody therapies relying heavily on optimized cell lines. A study by the European Biotechnology Research Institute reveals that over 40% of ongoing clinical trials in Europe involve biologics, further amplifying the need for advanced cell line development platforms. These factors collectively reinforce the market's growth trajectory, emphasizing its critical role in addressing unmet medical needs.

Advancements in Genome Editing Technologies

Technological breakthroughs in genome editing, particularly CRISPR-Cas9 are further propelling the growth of the European cell line development market. According to the European Society for Gene and Cell Therapy, CRISPR-based tools have reduced the time and cost associated with cell line engineering by up to 50%, enabling precise modifications to enhance productivity and stability. The European Commission notes that investments in CRISPR technology have surged by 25% annually over the past five years, with applications spanning drug discovery, gene therapy, and regenerative medicine. For example, CRISPR-engineered cell lines are now widely used in producing recombinant proteins and developing patient-specific therapies, achieving success rates exceeding 85%. Additionally, advancements in automation and high-throughput screening have streamlined the identification and validation of optimal cell lines, further accelerating development timelines. A report by the European Biotech Research Institute underscores that companies leveraging CRISPR technologies report a 30% increase in operational efficiency. These innovations not only enhance the versatility of cell line applications but also position Europe as a global leader in cutting-edge biotechnological solutions.

MARKET RESTRAINTS

High Costs and Complexity of Development

The substantial costs and technical complexity associated with cell line development is one of the major restraints to the European cell line development market. According to the European Health Economics Association, the average cost of developing a stable and scalable cell line ranges between €500,000 and €2 million, depending on the application and regulatory requirements. This financial burden is particularly challenging for small and medium-sized enterprises (SMEs), which account for over 60% of biotechnology companies in Europe. The European Commission highlights that the complexity of optimizing cell lines for high productivity and stability often results in extended development timelines, delaying commercialization by up to two years. Additionally, the need for specialized expertise in molecular biology and bioinformatics further exacerbates resource constraints, limiting accessibility for emerging players. A study by the European Biotechnology Research Institute reveals that over 40% of cell line development projects face delays due to technical challenges, such as clonal variability and low expression levels. These barriers not only hinder market entry but also impede the scalability of innovative therapies, posing a formidable challenge to widespread adoption.

Stringent Regulatory Requirements

Stringent regulatory frameworks governing the safety and efficacy of cell line-derived products are further hindering the growth of the European market. According to the European Medicines Agency, compliance with Good Manufacturing Practices (GMP) and International Council for Harmonisation (ICH) guidelines imposes rigorous testing and documentation requirements, increasing operational burdens for manufacturers. For instance, the transition to updated regulatory standards has resulted in a 30% increase in approval timelines, with smaller companies particularly affected by the heightened scrutiny. The European Commission notes that non-compliance with these regulations can lead to product recalls, legal liabilities, and reputational damage, deterring investment in research and development. Additionally, disparities in regulatory policies across member states create inconsistencies in approval processes, complicating cross-border distribution. A study by the European Biotechnology Industry Organization reveals that regulatory compliance accounts for up to 25% of total operational expenses for cell line development facilities. These challenges not only impede innovation but also exacerbate supply chain bottlenecks, posing a significant barrier to market expansion.

MARKET OPPORTUNITIES

Expansion into Personalized Medicine

The growing emphasis on personalized medicine is a significant opportunity for the European cell line development market. According to the European Society for Medical Oncology, personalized therapies tailored to individual genetic profiles are projected to account for over 20% of all oncology treatments by 2030, driven by advancements in genomic sequencing and cell line engineering. The European Commission highlights that patient-specific cell lines, developed using CRISPR and other genome editing tools, enable the production of targeted therapies with enhanced efficacy and reduced side effects. Additionally, collaborations between academic institutions and pharmaceutical companies have facilitated the development of scalable platforms for personalized cell line production. A study by the European Biotech Research Institute underscores that hospitals utilizing personalized therapies report a 25% improvement in patient outcomes, reflecting their growing acceptance. These dynamics position personalized medicine as a key growth driver, emphasizing its role in advancing precision healthcare.

Integration of Artificial Intelligence and Automation

The integration of artificial intelligence (AI) and automation into cell line development workflows offers significant opportunities to enhance efficiency and innovation. According to the European Medical Device Technology Association, AI-driven algorithms can analyze vast datasets to optimize cell line selection and predict productivity, reducing development times by up to 40%. For example, machine learning models developed by the European Biotechnology Research Institute have demonstrated a 90% accuracy rate in identifying optimal cell line candidates, surpassing traditional screening methods. The European Commission notes that automation technologies, such as robotic systems for cloning and screening, have increased throughput by 50%, enabling faster scalability. Additionally, cloud-based platforms facilitate real-time data sharing and collaboration, ensuring compliance with regulatory standards. A study by the European Health Economics Association reveals that companies leveraging AI and automation report a 30% reduction in operational costs. These innovations not only elevate the standard of cell line development but also create new revenue streams for market players, positioning AI as a catalyst for sustainable growth.

MARKET CHALLENGES

Ethical Concerns Surrounding Genetic Modifications

Ethical concerns surrounding genetic modifications in cell line development is a major challenge to the European market. According to the European Group on Ethics in Science and New Technologies, public skepticism regarding the use of genetically modified organisms (GMOs) and CRISPR-engineered cell lines has led to regulatory restrictions and limited funding for certain applications. For instance, a survey conducted by the European Public Opinion Research Institute reveals that over 50% of respondents express reservations about the safety and ethical implications of genome editing, particularly in human cell lines. The European Commission underscores that these concerns are compounded by cultural and religious beliefs, which vary significantly across member states, creating inconsistencies in public acceptance. Additionally, stringent labeling requirements for GMO-derived products have deterred investment in cell line development initiatives targeting agricultural and industrial applications. A study by the European Biotechnology Industry Organization highlights that addressing these challenges requires sustained investment in public education and transparent communication, yet resource constraints and societal resistance often undermine their effectiveness. These barriers not only hinder market growth but also impede efforts to maximize the therapeutic potential of genetically modified cell lines.

Supply Chain Vulnerabilities and Raw Material Shortages

Supply chain vulnerabilities and raw material shortages are also significant challenges to the European cell line development market. According to the European Chemical Industry Council, disruptions in the supply of essential reagents, media, and bioreactors have led to delays in cell line production, particularly during global crises such as the COVID-19 pandemic. For instance, the European Commission reports that over 30% of biotechnology companies faced shortages of critical raw materials in 2022, resulting in a 15% decline in operational capacity. Additionally, geopolitical tensions and trade restrictions have exacerbated supply chain bottlenecks, forcing manufacturers to rely on alternative suppliers with varying quality standards. A study by the European Biotech Research Institute reveals that raw material shortages disproportionately affect SMEs, which lack the resources to establish diversified supply chains. Furthermore, the perishable nature of many reagents necessitates stringent cold chain logistics, which are often compromised during transit. These vulnerabilities not only threaten production continuity but also undermine efforts to meet the growing demand for cell line-derived products, posing a formidable challenge to market resilience.

SEGMENTAL ANALYSIS

By Products & Services Insights

The reagents and media segment accounted for 61.8% of the European market share in 2024. The dominating share of the reagents and media segment in the European market is due to their indispensable role in cell culture and maintenance, serving as the foundation for all cell line development activities. According to the European Medicines Agency, the demand for high-quality reagents and media has surged by 20% annually, driven by the increasing adoption of biologics and monoclonal antibodies. The European Commission highlights that advancements in serum-free and chemically defined media have enhanced reproducibility and scalability, reducing batch-to-batch variability by up to 30%. Additionally, the versatility of reagents enables their application across diverse cell types, further solidifying their dominance. A study by the European Biotech Research Institute reveals that over 80% of biopharmaceutical companies prioritize investments in premium-grade reagents, reflecting their critical importance in ensuring consistent and reliable cell line performance. These factors collectively underscore the segment's significance, emphasizing its contribution to advancing biotechnological innovation.

The bioreactors segment is predicted to showcase a CAGR of 14.4% over the forecast period owing to their critical role in scaling up cell line production for commercial applications, including biologics and gene therapies. The European Commission reports that advancements in single-use and modular bioreactor systems have enhanced operational flexibility, reducing contamination risks and downtime by up to 40%. Additionally, the integration of real-time monitoring and control systems has improved process optimization, achieving productivity gains of 25%. The European Biotechnology Research Institute underscores that the adoption of bioreactors is particularly pronounced in large-scale manufacturing facilities, where multidisciplinary teams collaborate to optimize yield and quality. A study by the European Health Economics Association highlights that companies utilizing advanced bioreactor technologies report a 30% reduction in production costs, reflecting their growing popularity. These dynamics position bioreactors as a pivotal growth driver, emphasizing their role in advancing scalable and cost-effective cell line production.

By Source Insights

The mammalian cell lines segment occupied 71.7% of the European market share in 2024 owing to their unparalleled ability to produce complex biologics, including monoclonal antibodies and recombinant proteins, with proper post-translational modifications. According to the European Medicines Agency, over 80% of approved biologics are manufactured using mammalian cell lines, underscoring their critical role in therapeutic production. The European Commission highlights that advancements in CHO (Chinese Hamster Ovary) and HEK293 cell lines have enhanced productivity and stability, achieving titers exceeding 5 g/L in optimized systems. Additionally, the versatility of mammalian cell lines enables their application across diverse therapeutic areas, further reinforcing their dominance. A study by the European Biotech Research Institute reveals that over 90% of biopharmaceutical companies prioritize mammalian cell lines for commercial-scale production, reflecting their integral role in modern biotechnology. These factors collectively underscore the segment's importance, emphasizing its contribution to advancing biopharmaceutical innovation.

The non-mammalian segment is anticipated to register a CAGR of 12.2% over the forecast period. Factors such as the cost-effectiveness of non-mammalian and ease of use in producing simpler biologics, such as enzymes and vaccines are propelling the expansion of the segment in the European market. The European Commission reports that advancements in yeast and insect cell lines have expanded their applicability, achieving productivity gains of up to 30% in certain applications. Additionally, the scalability and robustness of non-mammalian systems make them ideal for industrial-scale production, particularly in vaccine manufacturing. The European Medicines Agency underscores that the adoption of non-mammalian cell lines is particularly pronounced in emerging therapeutic areas, such as synthetic biology and biofuels. A study by the European Health Economics Association highlights that companies utilizing non-mammalian systems report a 25% reduction in production costs, reflecting their growing acceptance. These dynamics position non-mammalian cell lines as a key growth driver, emphasizing their role in diversifying biotechnological applications.

By Cell Line Insights

The recombinant cell lines segment occupied the leading share of the European market in 2024. The leading position of recombinant cell lines segment in the European market is rooted in their versatility and ability to produce a wide range of biologics, including monoclonal antibodies, vaccines, and recombinant proteins. According to the European Medicines Agency, recombinant cell lines achieve productivity rates exceeding 90%, making them indispensable in biopharmaceutical manufacturing. The European Commission highlights that advancements in genome editing tools, such as CRISPR, have enhanced the precision and efficiency of recombinant cell line engineering, reducing development timelines by up to 50%. Additionally, the scalability of recombinant systems enables their application across diverse therapeutic areas, further solidifying their dominance. A study by the European Biotech Research Institute reveals that over 85% of biopharmaceutical companies utilize recombinant cell lines for commercial-scale production, reflecting their critical role in modern biotechnology. These factors collectively underscore the segment's importance, emphasizing its contribution to advancing therapeutic innovation.

The hybridoma segment is predicted to witness a CAGR of 13.8% over the forecast period due to their critical role in producing monoclonal antibodies, which are widely used in diagnostics, therapeutics, and research applications. The European Medicines Agency reports that hybridoma-derived antibodies achieve specificity rates exceeding 95%, surpassing other production methods in terms of accuracy and reliability. Additionally, advancements in fusion technologies and culture conditions have enhanced the stability and productivity of hybridoma systems, achieving yield improvements of up to 25%. The European Commission underscores that the adoption of hybridoma cell lines is particularly pronounced in oncology and immunology, where targeted therapies are in high demand. A study by the European Health Economics Association highlights that companies utilizing hybridoma technologies report a 30% increase in operational efficiency, reflecting their growing popularity. These dynamics position hybridoma cell lines as a pivotal growth driver, emphasizing their expanding therapeutic utility.

By Application Insights

The drug discovery segment captured 56.1% of the European market share in 2024. The growth of the drug discovery segment in the European market is attributed to the indispensable role of cell lines in target identification, validation, and high-throughput screening of potential drug candidates. According to the European Medicines Agency, over 70% of preclinical studies rely on cell line-based assays to evaluate efficacy and toxicity, underscoring their critical importance in early-stage research. The European Commission highlights that advancements in 3D cell culture and organoid models have enhanced the predictive accuracy of drug discovery platforms, reducing attrition rates by up to 30%. Additionally, the versatility of cell lines enables their application across diverse therapeutic areas, further reinforcing their dominance. A study by the European Biotech Research Institute reveals that over 80% of pharmaceutical companies prioritize investments in cell line-based drug discovery platforms, reflecting their integral role in accelerating innovation. These factors collectively underscore the segment's significance, emphasizing its contribution to advancing pharmaceutical R&D.

The tissue engineering segment is anticipated to register a CAGR of 15.5% over the forecast period. Factors such as the increasing demand for regenerative therapies and bioengineered tissues that rely heavily on optimized cell lines for scaffold colonization and functional tissue formation is one of the major factors propelling the growth of the tissue engineering segment in the European market. The European Commission reports that advancements in stem cell and progenitor cell lines have expanded their applicability, achieving success rates exceeding 85% in clinical trials. Additionally, the integration of bioprinting technologies has enhanced the scalability and reproducibility of tissue-engineered constructs, reducing production costs by up to 25%. The European Medicines Agency underscores that the adoption of tissue engineering is particularly pronounced in orthopedics, cardiology, and dermatology, where unmet medical needs persist. A study by the European Health Economics Association highlights that hospitals utilizing tissue-engineered products report a 30% improvement in patient outcomes, reflecting their growing acceptance. These dynamics position tissue engineering as a pivotal growth driver, emphasizing its role in advancing regenerative medicine.

REGIONAL ANALYSIS

Germany accounted for 26.6% of the European cell line development market share in 2024. The dominance of Germany in the European market is attributed to the country's robust biotechnology infrastructure and strong emphasis on R&D, with investments exceeding €10 billion annually. According to the German Biotechnology Industry Organization, Germany hosts over 600 biotechnology companies, many of which specialize in cell line engineering for biologics and gene therapies. The European Commission highlights that Germany’s aging population, with over 21% aged 65 or older, drives demand for advanced therapeutics, further amplifying the need for optimized cell lines. Additionally, the country’s expertise in automation and AI-driven analytics has positioned it as a hub for technological advancements in cell line development. These factors collectively underscore Germany's leadership, reflecting its commitment to delivering high-quality biotechnological solutions.

France is expected to capture a notable share of the European market over the forecast period owing to the proactive approach of France to healthcare innovation and its universal healthcare system, which ensures equitable access to advanced therapies. The French Biotechnology Association reports that France performs over 30% of all clinical trials involving cell line-derived products in Europe, supported by government initiatives to modernize biotechnology infrastructure. Additionally, France’s expertise in genome editing and CRISPR technologies has positioned it as a leader in developing next-generation cell lines. The European Commission underscores that collaborations between public and private entities have accelerated innovation, driving market growth. These dynamics reinforce France's leadership, emphasizing its role in advancing cell line development solutions.

The UK is a promising regional market for cell line development in Europe. The extensive research base of the UK and cutting-edge initiatives in genomics and cell line engineering are likely to boost the UK cell line development market growth. According to the British Biotechnology Association, the UK performs over 25% of all cell line-related R&D activities in Europe, supported by nationwide awareness campaigns and specialized research centers. The UK Department of Health underscores that the rising prevalence of chronic diseases, coupled with advancements in personalized medicine, has amplified demand for cell line technologies. Additionally, the country’s focus on sustainability and ethical sourcing aligns with global trends, enhancing its market reputation. These factors collectively highlight the UK's pivotal role in shaping the future of cell line development.

Italy is anticipated to account for a notable share of the European market over the forecast period owing to the strategic investments of Italy in biotechnology infrastructure and its strong tradition of medical innovation. The Italian Biotechnology Association reports that Italy performs over 20% of all cell line-related clinical trials in Europe, supported by advancements in genome editing and automation technologies. Additionally, Italy’s expertise in personalized medicine has expanded the scope of cell line applications, enhancing their therapeutic utility. The European Commission highlights that collaborations between academic institutions and industry players have accelerated innovation, driving market growth. These dynamics underscore Italy's significance, reflecting its contributions to advancing cell line development solutions.

Spain is estimated to register a healthy CAGR in the European cell line development market over the forecast period. The robust regulatory framework of Spain and high adoption rates of advanced biotechnological solutions are propelling the Spanish market growth. The Spanish Biotechnology Society emphasizes that Spain performs over 15% of all cell line-related R&D activities in Europe, supported by investments in automation and AI-driven platforms. Additionally, the country’s focus on regenerative medicine and biotechnological advancements has expanded the therapeutic applications of cell lines. The European Commission highlights that Spain’s strategic initiatives to enhance procedural safety and accessibility have strengthened its market position. These factors collectively reinforce Spain's importance, underscoring its role in addressing regional healthcare needs.

MARKET SEGMENTATION

This research report on the europe cell line development market is segmented and sub-segmented based on categories.

By Products & Services

- Reagents & media

- Equipment

- Incubators

- Centrifuge

- Bioreactors

- Storage equipment

- Microscopes

- Electroporators

- Fluorescence-activated cell sorting (FACS)

- Other equipment

- Accessories and consumables

- Services

By Source

- Mammalian

- Non-mammalian

- Insects

- Amphibians

By Cell Line

- Recombinant

- Hybridomas

- Continuous cell lines

- Primary cell lines

By Application

- Bioproduction

- Drug discovery

- Toxicity testing

- Tissue engineering

- Research applications

By End-use

- Pharmaceutical and biotechnology companies

- Academic & research institutes

- Contract research organizations (CROs)

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is driving the growth of the Europe Cell Line Development Market?

Growth is driven by increasing demand for biopharmaceuticals, advancements in genetic engineering, and rising R&D investments.

What is the future outlook for the Europe Cell Line Development Market?

The market is expected to grow steadily, driven by advancements in biotechnology and increasing demand for biologics.

Which countries are leading the Europe Cell Line Development Market?

Germany, the UK, France, Italy, and Switzerland are the leading countries in the market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]