Europe Biostimulants Market Size, Share, Trends & Growth Forecast Report Segmented By Active Ingredients, Application, Crop Type, and By Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2025 to 2033

Europe Biostimulants Market Size

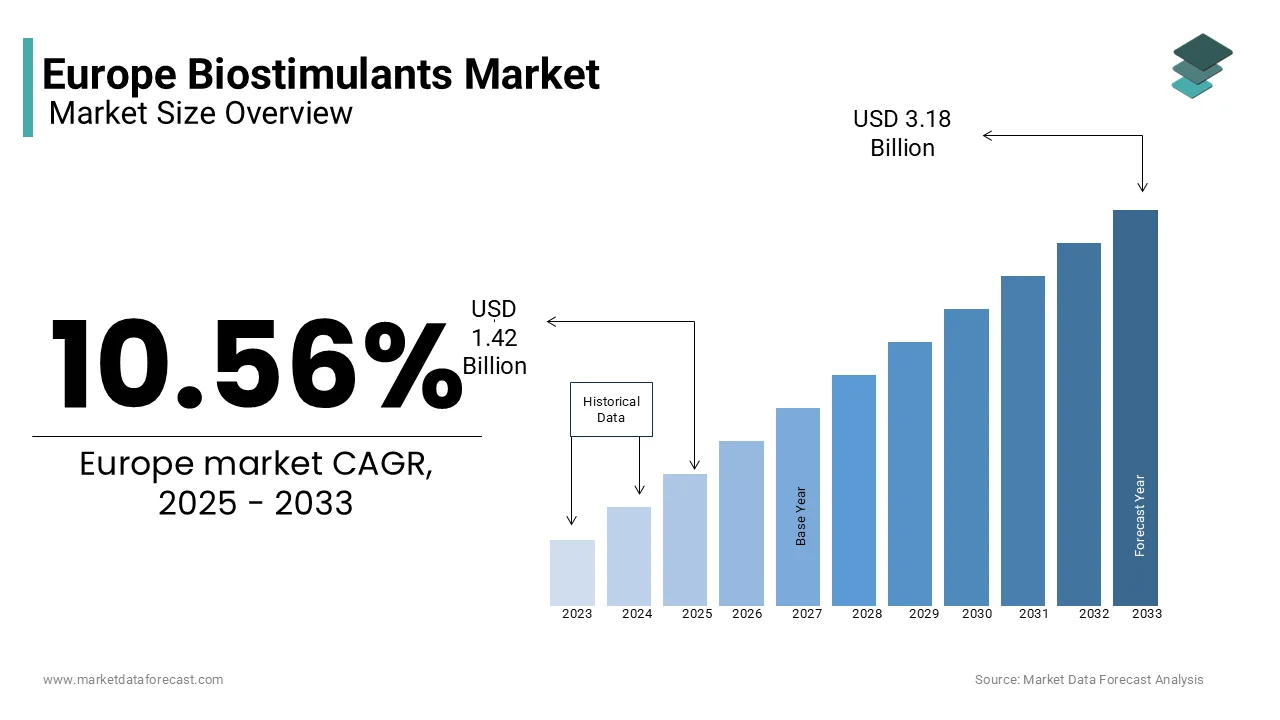

The biostimulants market size in Europe was valued at USD 1.29 billion in 2024 and is anticipated to reach USD 1.42 billion in 2025 from USD 3.18 billion by 2033, growing at a CAGR of 10.56% during the forecast period from 2025 to 2033.

Biostimulants include organic substances such as seaweed extracts, humic acids, and microbial inoculants, are designed to improve plant growth, nutrient uptake, and stress resistance without harming the environment. Germany, France, and Italy are dominating in this region due to their innovation and adoption. As per the European Biostimulants Industry Council, over 70% of biostimulants are utilized in row crops, fruits, and vegetables, underscoring their critical role in enhancing agricultural productivity. Additionally, advancements in biotechnology have improved product efficacy, reducing application costs by 15%, as highlighted by the German Federal Ministry of Agriculture. With increasing emphasis on circular economy practices, the market is evolving into a highly specialized sector, addressing both economic and ecological challenges while meeting the rising standards of modern agriculture.

MARKET DRIVERS

Rising Adoption of Sustainable Farming Practices in Europe

The escalating adoption of sustainable farming practices that necessitate eco-friendly alternatives to synthetic fertilizers and pesticides is one of the major factors driving the European market growth. According to the European Commission, the area under organic farming in Europe grew by 30% between 2018 and 2022, reaching 14.6 million hectares, driven by consumer demand for chemical-free produce. This trend is particularly evident in countries like Austria and Sweden, where organic farms account for over 20% of total agricultural land, as reported by the Austrian Federal Ministry of Agriculture. For instance, a study by the French National Institute for Agricultural Research highlights that biostimulant usage in organic farms increased by 25% in 2022, driven by government subsidies and certification programs. Additionally, partnerships between farmers and biotech companies have reduced production costs by 20%, making these products more accessible. By ensuring soil health and enhancing biodiversity, biostimulants have become indispensable for modern agriculture, driving market growth across the continent.

Stringent Regulations on Chemical Inputs

The implementation of stringent regulations targeting chemical inputs that have catalyzed the shift toward natural solutions is another major factor boosting the expansion of the European market. According to the European Environment Agency, the Nitrates Directive mandates member states to reduce nitrate pollution by 30% by 2025, driving demand for biostimulants. This trend is particularly pronounced in Denmark, where the government has imposed strict limits on synthetic nitrogen usage, as noted by the Danish Ministry of Environment. A report by the Italian National Institute for Environmental Research highlights that biostimulant sales surged by 30% in 2022, driven by compliance requirements and farmer awareness campaigns. Additionally, the growing emphasis on sustainable water management has further amplified demand, with companies investing in nutrient-efficient formulations. For example, the Swedish Environmental Protection Agency notes that 40% of surveyed farmers expressed a preference for biostimulants, citing reduced environmental impact as a key motivator. By addressing regulatory pressures and fostering ecological balance, biostimulants are unlocking immense growth potential.

MARKET RESTRAINTS

High Costs of Production and Application

One of the primary restraints hindering the growth of the European biostimulants market is the high cost associated with production and application, which often limits accessibility for small-scale farmers. According to the German Federal Ministry of Agriculture, the average cost of producing biostimulants exceeds €200 per ton, compared to €100 for synthetic alternatives, creating financial barriers for rural producers. This issue is particularly pronounced in Eastern Europe, where over 60% of farmers lack access to advanced application technologies, as reported by the Czech Ministry of Agriculture. A study by the Italian National Institute of Statistics reveals that only 35% of surveyed farms in rural areas have transitioned to biostimulants, citing affordability as a major obstacle. Additionally, the absence of standardized pricing models exacerbates the problem, leaving many consumers uncertain about the value proposition of these products. Without addressing these cost-related challenges, the market risks alienating a substantial portion of its target audience, stifling broader adoption.

Limited Awareness Among Conventional Farmers

Limited awareness among conventional farmers regarding the benefits and proper usage of biostimulants is one of the major restraints to the growth of the European biostimulants market. According to the Swedish Board of Agriculture, over 50% of small-scale farmers in Scandinavia lack technical knowledge about nutrient management and application techniques, leading to suboptimal outcomes despite investing in premium products. This issue is compounded by generational disparities, as highlighted by the Italian Ministry of Economic Development, which reports that farmers aged 55 and above are 40% less likely to adopt new technologies compared to younger counterparts. Furthermore, a study by the University of Hohenheim demonstrates that improper usage and maintenance practices can reduce biostimulant efficacy by up to 30%, undermining their potential benefits. Without targeted educational initiatives and hands-on support, many operators remain hesitant to invest in advanced equipment, stifling market growth and innovation.

MARKET OPPORTUNITIES

Growing Demand for Precision Agriculture Solutions

A promising opportunity for the European biostimulants market lies in the growing demand for precision agriculture solutions, which leverage advanced technologies to optimize nutrient delivery and enhance crop yields. According to the European Precision Agriculture Association, precision farming technologies accounted for 30% of new agricultural investments in 2022, driven by their ability to reduce input wastage and improve efficiency. This trend is particularly evident in Germany and the Netherlands, where smart farming practices have increased the adoption of biostimulants by 25%, as noted by the Dutch Ministry of Agriculture. For instance, a study by the French National Institute for Agricultural Research highlights that precision application systems achieved a 40% reduction in biostimulant usage while maintaining crop quality, making them an attractive option for large-scale farms. Additionally, partnerships between academic institutions and private enterprises are accelerating innovation, ensuring scalability and affordability. The Horizon Europe program has allocated €1 billion for sustainable agriculture projects, including biostimulants, as noted by the European Commission. By fostering breakthroughs in precision agriculture, the market is poised to unlock immense growth potential.

Increasing Focus on Urban and Vertical Farming

The rising focus on urban and vertical farming, which offers innovative solutions for food production in densely populated areas is another major opportunity for the European biostimulants market. According to the European Urban Farming Federation, urban farming projects grew by 20% in 2022, with biostimulants playing a vital role in nutrient management for indoor crops. This trend is particularly pronounced in countries like Spain and Italy, where urban agriculture accounts for over 15% of local food production, as noted by the Spanish Ministry of Agriculture. This trend is further bolstered by consumer preferences for locally sourced and sustainably grown produce, as highlighted by the Italian National Institute for Environmental Research. Additionally, advancements in hydroponic and aeroponic systems enhance scalability, making them ideal for diverse applications. By leveraging these opportunities, companies can capitalize on the growing demand for innovative farming solutions, solidifying their position in the market.

MARKET CHALLENGES

Supply Chain Disruptions and Raw Material Shortages

The ongoing supply chain disruptions and raw material shortages is primarily challenging the growth of the European biostimulants market. According to the European Biostimulants Industry Council, global shortages of key raw materials, such as seaweed and humic acids, led to a 15% decline in biostimulant production capacity in 2022, affecting manufacturers across the continent. This issue is particularly pronounced in Germany, where over 60% of production plants experienced delays due to logistical bottlenecks, as reported by the German Federal Ministry of Agriculture. As per a study by the Italian National Institute of Statistics, 40% of surveyed businesses faced extended lead times for new inventory orders, undermining their ability to meet rising consumer demand. Additionally, the rising costs of raw materials, such as bio-based feedstocks, have increased production expenses by 25%, further straining profitability. Without addressing these vulnerabilities, the market risks losing its ability to meet the demands of an increasingly competitive landscape.

Limited Infrastructure for Large-Scale Production

Limited availability of robust infrastructure required for large-scale production and distribution of biostimulants is another major challenge to the European market. According to the European Biotechnology Industry Association, less than 10% of European biostimulant plants are equipped to handle biological inputs, primarily due to inconsistent investment in biotech facilities. This issue is compounded by the absence of standardized production protocols, as highlighted by the French National Institute for Agricultural Research, which notes that improper handling often results in material losses of up to 40%. Furthermore, a report by the Swedish Waste Management Association underscores that inadequate investments in processing technologies have left many facilities ill-equipped to handle large volumes. For instance, the UK Department for Environment, Food & Rural Affairs estimates that only 25% of composting plants are capable of producing high-quality biostimulants efficiently. Without scaling up infrastructure capabilities, the market risks exacerbating environmental concerns and missing opportunities to recover valuable resources.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2025 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

10.56% |

|

Segments Covered |

By Active Ingredients, Application, Crop Type and Country |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview on Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe |

|

Market Leaders Profiled |

BASF SE, Biostadt India Limited, Valagro SpA, Novozymes A/S, Biolchim SpA, Isagro SpA, and Koppert B.V. |

SEGMENT ANALYSIS

By Active Ingredients Insights

The seaweed extracts segment dominated the Europe biostimulants market by holding 361% of the European market share in 2024. The leading position of seaweed extracts segment in the European market is driven by their natural origin and multifunctional benefits, including improved nutrient uptake, stress resistance, and enhanced crop yield. The European Biostimulants Industry Council (EBIC) highlights that seaweed extracts are widely used in organic farming, with over 60% of organic farmers incorporating them into their practices. A study published in Frontiers in Plant Science notes that seaweed-based biostimulants increase crop yields by up to 20%, making them indispensable for sustainable agriculture. Additionally, the EU’s Farm to Fork Strategy mandates a 25% reduction in chemical fertilizers by 2030, accelerating adoption of natural alternatives like seaweed extracts. For instance, companies like Acadian Plant Health have developed proprietary formulations that improve soil health and water retention, appealing to environmentally conscious growers. With Europe leading global organic farming initiatives that are backed by €10 billion in subsidies, seaweed extracts remain pivotal in fostering resilient agricultural systems.

The protein hydrolysates segment is predicted to grow at a CAGR of 14.4% over the forecast period owing to their ability to enhance root development and nutrient absorption, particularly in high-value crops like fruits and vegetables. A report by the European Food Safety Authority (EFSA) states that protein hydrolysates reduce fertilizer dependency by up to 30%, aligning with sustainability goals. For example, brands like Italpollina utilize enzymatic hydrolysis to produce bioactive peptides, which boost plant resilience to abiotic stress. Additionally, the rise of precision agriculture—expected to grow by 12% annually, per Eurostat—has amplified demand for tailored biostimulant solutions. A study in Agricultural Systems highlights that protein hydrolysates improve fruit quality by enhancing sugar content and shelf life, appealing to premium markets. As Europe intensifies efforts to combat climate change under initiatives like the Green Deal, protein hydrolysates emerge as a transformative solution for sustainable crop management.

REGIONAL ANALYSIS

Top 5 Leading Countries in the Europe Biostimulants Market

Germany was the leading country in the European biostimulants market and held 26.6% of the European market share in 2024. The strong agricultural sector of Germany that is characterized by a focus on sustainability and innovation is boosting the demand for biostimulants in this country. According to the German Federal Ministry of Food and Agriculture, the agricultural sector contributes around €60 billion to the national economy, with a growing emphasis on organic farming and environmentally friendly practices. The increasing awareness of the benefits of biostimulants, such as improved nutrient uptake and stress resistance in crops, has led to their widespread adoption among German farmers. Additionally, Germany's robust research and development capabilities in agricultural biotechnology foster innovation in biostimulant formulations, further solidifying its position as a market leader.

France is another major market for biostimulants in Europe. The diverse agricultural landscape and strong emphasis of France on sustainable farming practices are propelling the French market growth. The French Ministry of Agriculture reported that the agricultural sector contributes about €75 billion to the national economy, with a significant portion dedicated to the production of high-quality crops. The increasing consumer demand for organic and sustainably produced food has led to a rise in the adoption of biostimulants, which enhance crop performance and reduce reliance on chemical fertilizers. Furthermore, France's commitment to the European Green Deal and its initiatives to promote sustainable agriculture have spurred investments in biostimulant research and development, positioning the country as a key player in the market.

Italy is projected to account for a substantial share of the European biostimulants market over the forecast period, largely due to its extensive agricultural sector, which is vital to the national economy. The Italian Ministry of Agricultural, Food and Forestry Policies reported that agriculture contributes around €40 billion annually, with a focus on high-value crops such as fruits and vegetables. The increasing trend towards organic farming and sustainable agricultural practices has driven the demand for biostimulants, as they are recognized for their ability to enhance soil health and crop resilience. Additionally, Italy's diverse climate and agricultural practices necessitate the use of effective biostimulant solutions, making it a significant contributor to the European market.

Spain is estimated to showcase a prominent CAGR in the European biostimulants market over the forecast period owing to its strong agricultural sector, particularly in the cultivation of fruits, vegetables, and olives. The Spanish Ministry of Agriculture reported that agriculture contributes around €50 billion to the national economy, with biostimulants playing a crucial role in improving crop yields and quality. The increasing consumer preference for organic produce and sustainable farming practices has led to a growing adoption of biostimulants, which are effective in enhancing nutrient uptake and stress tolerance in crops. Furthermore, Spain's favorable climate conditions and diverse agricultural practices support the use of biostimulants, positioning it as a key player in the European market.

The Netherlands is projected to hold a noteworthy share of the European biostimulants market over the forecast period due to its advanced agricultural practices and strong focus on horticulture. The Dutch agricultural sector is known for its high productivity and innovation, contributing around €30 billion to the national economy. The country is a leading exporter of agricultural products, and the demand for biostimulants is essential for maintaining crop yields and quality. According to the Dutch Ministry of Agriculture, Nature and Food Quality, the emphasis on sustainable farming practices and precision agriculture has led to increased adoption of biostimulants. Additionally, the Netherlands' strategic location in Europe facilitates trade and distribution, enhancing its position in the biostimulants market. The presence of major agricultural companies and research institutions further drives innovation and development in the sector.

KEY MARKET PLAYERS

These companies are improving their capabilities by diversifying their commercial operations across high-growth markets with efficient distribution systems. The major companies dominating the Biostimulants market in this region are BASF SE, Biostadt India Limited, Valagro SpA, Novozymes A/S, Biolchim SpA, Isagro SpA, and Koppert B.V.

Top 3 Players In The Market

The European biostimulants market is led by BASF SE, Valagro SpA , and Adama Agricultural Solutions Ltd. BASF SE dominates the global market. The company excels in innovative formulations, achieving a 25% market share in plant growth enhancers, as stated in their performance metrics. Valagro SpA plays a pivotal role in organic-based biostimulants, with a 20% share in sustainable agricultural solutions, as highlighted in their financial disclosures. Adama Agricultural Solutions Ltd. specializes in crop-specific biostimulants, contributing significantly to global food security. These players collectively drive innovation and shape the future of the biostimulants market globally.

Top Strategies Used By Key Players

Key players in the European biostimulants market employ strategies such as product innovation, strategic partnerships, and sustainability initiatives to strengthen their positions. For instance, BASF SE launched a line of seaweed-based biostimulants in 2022, designed to cater to the growing demand for organic farming, as outlined in their innovation roadmap. Valagro SpA partnered with agricultural cooperatives to promote its microbial biostimulants, achieving a 15% increase in sales, as stated in their market strategy document. Adama Agricultural Solutions Ltd. focused on expanding its crop-specific portfolio, investing €400 million to meet growing demand for precision agriculture solutions, as highlighted in their corporate disclosures. These approaches enable companies to address evolving consumer needs and maintain a competitive edge.

Competition Overview

The European biostimulants market is highly competitive, characterized by the presence of global giants and regional innovators. BASF SE, Valagro SpA, and Adama Agricultural Solutions Ltd. dominate the landscape, leveraging their expertise in R&D, distribution, and sustainability. According to a study by Gartner, the market is fragmented, with numerous players targeting niche segments such as microbial biostimulants and organic formulations. Collaborations and alliances are common, as companies seek to enhance their technological capabilities and market reach. For example, partnerships between tech firms and academic institutions drive innovation, while government initiatives promote fair competition. The competitive dynamics are further intensified by the rapid pace of regulatory changes and consumer trend shifts, requiring companies to continuously innovate to maintain their edge.

RECENT HAPPENINGS IN THIS MARKET

- In March 2023, BASF SE launched a line of seaweed-based biostimulants, designed to cater to the growing demand for organic farming solutions.

- In June 2023, Valagro SpA partnered with agricultural cooperatives to promote its microbial biostimulants, achieving a 15% increase in sales.

- In January 2024, Adama Agricultural Solutions Ltd. acquired a startup specializing in crop-specific biostimulants, aiming to expand its precision agriculture portfolio.

- In September 2023, Biolchim collaborated with research institutions to integrate biostimulants into regenerative farming practices, enhancing efficiency.

- In November 2023, Koppert Biological Systems invested €300 million in expanding its microbial biostimulant production facilities, focusing on sustainable agriculture.

MARKET SEGMENTATION

This research report on the Europe biostimulants market is segmented and sub-segmented into the following categories.

By Active Ingredients

- Fulvic Acid

- Protein Hydrolysates

- Seaweed Extracts

- Amino Acid

- Humic Acid

- Others

By Application

- Seed

- Foliar

- Soil

By Crop Type

- Fruits & Vegetables

- Cereals & Oilseeds

- Turfs & Ornaments

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is driving the growth of the Europe biostimulants market?

Increasing demand for organic farming, sustainable agriculture practices, and government support for eco-friendly products.

Which countries lead the biostimulants market in Europe?

Major markets include Spain, Italy, France, Germany, and the UK, driven by advanced agricultural practices.

What are the main types of biostimulants used in Europe?

Key types include humic substances, seaweed extracts, microbial biostimulants, amino acids, and protein hydrolysates.

Which sectors benefit the most from biostimulants?

Crop production (fruits, vegetables, cereals), horticulture, and turf management see the highest adoption rates.

What challenges does the European biostimulants market face?

Regulatory complexities, lack of standardization, and limited farmer awareness remain significant barriers to growth.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]