Europe Bancassurance Market Size, Share, Trends, & Growth Forecast Report By Type of Insurance (Life Insurance and Non-life Insurance), Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2024 to 2033

Europe Bancassurance Market Size

The Europe bancassurance market was worth USD 655.8 billion in 2024. The European market is expected to reach USD 981.32 billion by 2033 from USD 685.84 billion in 2025, rising at a CAGR of 4.58% from 2025 to 2033.

Bancassurance, a portmanteau of "bank" and "insurance," refers to the strategic partnership between banks and insurance companies to offer insurance products through banking channels. This model has gained significant traction in Europe, where financial institutions leverage their extensive customer bases and distribution networks to cross-sell insurance policies such as life, health, property, and casualty insurance. The European bancassurance market is driven by regulatory frameworks like the Payment Services Directive (PSD2) and Solvency II, which have encouraged collaboration between banks and insurers. According to a report by the European Insurance and Occupational Pensions Authority (EIOPA), bancassurance accounted for approximately 30% of total insurance sales in Europe in 2022, with countries like France, Italy, and Spain are leading.

The market's growth is due to the increasing demand for integrated financial solutions, as consumers seek convenience and personalized services. A study by McKinsey & Company revealed that over 60% of European customers prefer purchasing insurance products directly from their banks due to trust and familiarity. Furthermore, the rise of digitalization has transformed bancassurance by enabling seamless online policy issuance and claims management. For instance, in 2021, according to the European Banking Federation, digital bancassurance platforms contributed to a 15% increase in insurance product sales across the region. However, challenges such as stringent data privacy regulations under the General Data Protection Regulation (GDPR) and competition from standalone insurers persist. Despite these hurdles, the European bancassurance market remains a cornerstone of the financial ecosystem, with projections indicating steady growth as banks continue to innovate and expand their service portfolios.

MARKET DRIVERS

Increasing Consumer Trust in Banks

The high level of consumer trust in banks, which facilitates the sale of insurance products through banking channels. According to a 2022 survey by the European Banking Federation, over 70% of European customers expressed greater confidence in purchasing insurance from their banks compared to standalone insurers. This trust stems from the long-standing relationships banks have with their clients and the perception of banks as secure and reliable institutions. As per the European Insurance and Occupational Pensions Authority (EIOPA), bancassurance accounted for nearly 35% of life insurance sales in countries like France and Italy, where banks are deeply integrated into the financial ecosystem. Additionally, banks’ ability to offer tailored solutions, such as bundled insurance packages with loans or mortgages that enhances customer convenience. This alignment of trust and product personalization continues to drive the growth of bancassurance across Europe.

Digital Transformation and Technological Advancements

Digital transformation has emerged as a significant driver of the Europe bancassurance market by enabling seamless integration of banking and insurance services. According to the European Commission, digital bancassurance platforms contributed to a 20% increase in policy sales between 2020 and 2022, as customers increasingly prefer online and mobile channels for financial transactions. The rise of technologies like artificial intelligence and data analytics has allowed banks to analyze customer behavior and offer personalized insurance products. As per the McKinsey & Company, digitally enabled bancassurance models have reduced operational costs by 15% while improving customer engagement. Furthermore, regulatory frameworks like the Payment Services Directive (PSD2) have facilitated secure data sharing between banks and insurers by enhancing collaboration. These technological advancements not only streamline processes but also position bancassurance as a key enabler of financial inclusion and innovation in Europe’s evolving financial landscape.

MARKET RESTRAINTS

Stringent Data Privacy Regulations

The stringent data privacy regulations imposed by the General Data Protection Regulation (GDPR) is one of the restraints for the Europe bancassurance market. According to the European Data Protection Board, non-compliance with GDPR can result in fines of up to €20 million or 4% of annual global turnover is creating significant operational challenges for banks and insurers. Sharing customer data between banks and insurance partners requires explicit consent, which complicates cross-selling efforts. A 2022 study by the European Banking Federation revealed that 40% of financial institutions reported difficulties in aligning their data-sharing practices with GDPR requirements. This regulatory hurdle limits the seamless integration of services and increases compliance costs. Furthermore, customers’ growing concerns about data security discourage them from opting for bundled products, thereby hindering the growth potential of bancassurance despite its convenience and efficiency.

Intense Competition from Standalone Insurers

Another key restraint is the intense competition faced by bancassurance providers from standalone insurance companies, which often have more specialized offerings and established brand loyalty. According to the European Insurance and Occupational Pensions Authority (EIOPA), standalone insurers captured over 65% of the European insurance market in 2021 is leaving limited room for bancassurance to expand. Standalone insurers leverage advanced digital tools and targeted marketing strategies to attract customers by making it challenging for banks to differentiate their insurance products. According to the McKinsey & Company, standalone insurers often provide more competitive pricing due to economies of scale that further pressuring bancassurance profit margins. This competitive landscape forces banks to invest heavily in product innovation and customer acquisition by straining resources and slowing market penetration. As a result, bancassurance providers must navigate these challenges to maintain relevance in an increasingly crowded marketplace.

MARKET OPPORTUNITIES

Expansion of Digital Bancassurance Platforms

One significant opportunity in the Europe bancassurance market lies in the expansion of digital bancassurance platforms, which is driven by the increasing adoption of online and mobile banking services. According to the European Commission, over 70% of Europeans now use internet banking is creating a fertile ground for integrating insurance products into digital banking ecosystems. As per the McKinsey & Company, digitally enabled bancassurance models have led to a 25% increase in customer engagement and a 15% reduction in operational costs since 2020. Furthermore, the Payment Services Directive (PSD2) has facilitated secure data sharing between banks and insurers by enabling personalized product offerings. For instance, real-time analytics allows banks to recommend insurance policies based on customer behavior, such as travel or home purchases. Bancassurance providers are well-positioned to capitalize on this trend by enhancing user experience and expanding their reach across Europe.

Growing Demand for Integrated Financial Solutions

Another major opportunity is the rising demand for integrated financial solutions with the customers increasingly seek convenience and holistic financial planning. According to the European Banking Federation, over 60% of European consumers prefer bundled services that combine banking and insurance products, such as mortgage-linked life insurance or loan protection plans. This trend is particularly prominent in countries like France and Italy, where bancassurance accounts for nearly 40% of total insurance sales. According to the European Insurance and Occupational Pensions Authority (EIOPA), banks are uniquely positioned to meet this demand due to their extensive customer bases and trusted relationships. Additionally, the growing emphasis on financial inclusion has encouraged banks to offer affordable and accessible insurance products tailored to underserved populations. Banks can address this demand while strengthening customer loyalty and driving revenue growth in the bancassurance sector.

MARKET CHALLENGES

Regulatory Complexity and Compliance Costs

One of the major challenges in the Europe bancassurance market is the complexity of regulatory frameworks, which impose significant compliance burdens on banks and insurers. According to the European Insurance and Occupational Pensions Authority (EIOPA), regulations such as Solvency II and the General Data Protection Regulation (GDPR) require extensive documentation, reporting, and customer consent management along with increasing operational costs. A 2022 report by the European Banking Federation revealed that financial institutions spend approximately 10-15% of their annual budgets on compliance-related activities. These stringent regulations often slow down product launches and limit cross-selling opportunities for smaller players with limited resources. Furthermore, the lack of harmonization across EU member states creates additional challenges, as banks must navigate varying national laws while offering insurance products. This regulatory complexity acts as a barrier to innovation and scalability in the bancassurance market.

Limited Customer Awareness and Education

Another significant challenge is the limited awareness and understanding of bancassurance products among European consumers, which hinders adoption rates. According to a study by the European Commission, nearly 40% of banking customers are unaware of the insurance products offered by their banks, despite being frequent users of other financial services. This knowledge gap is particularly pronounced in rural areas, where access to financial education is limited. According to the European Banking Federation, low awareness leads to missed opportunities for banks, as customers often turn to standalone insurers for their perceived expertise. Additionally, misconceptions about the cost and coverage of bancassurance products further deter potential buyers. Addressing this challenge requires targeted educational campaigns and transparent communication strategies to build trust and demonstrate the value proposition of bancassurance offerings in meeting customers’ financial protection needs.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

4.58% |

|

Segments Covered |

By Type of Insurance, and Country |

|

Various Analyses Covered |

Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

|

Countries Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, and Rest of Europe |

|

Market Leaders Profiled |

Allianz, Generali, Zurich, AG Insurance, and AXA. |

SEGMENTAL ANALYSIS

By Type of Insurance Insights

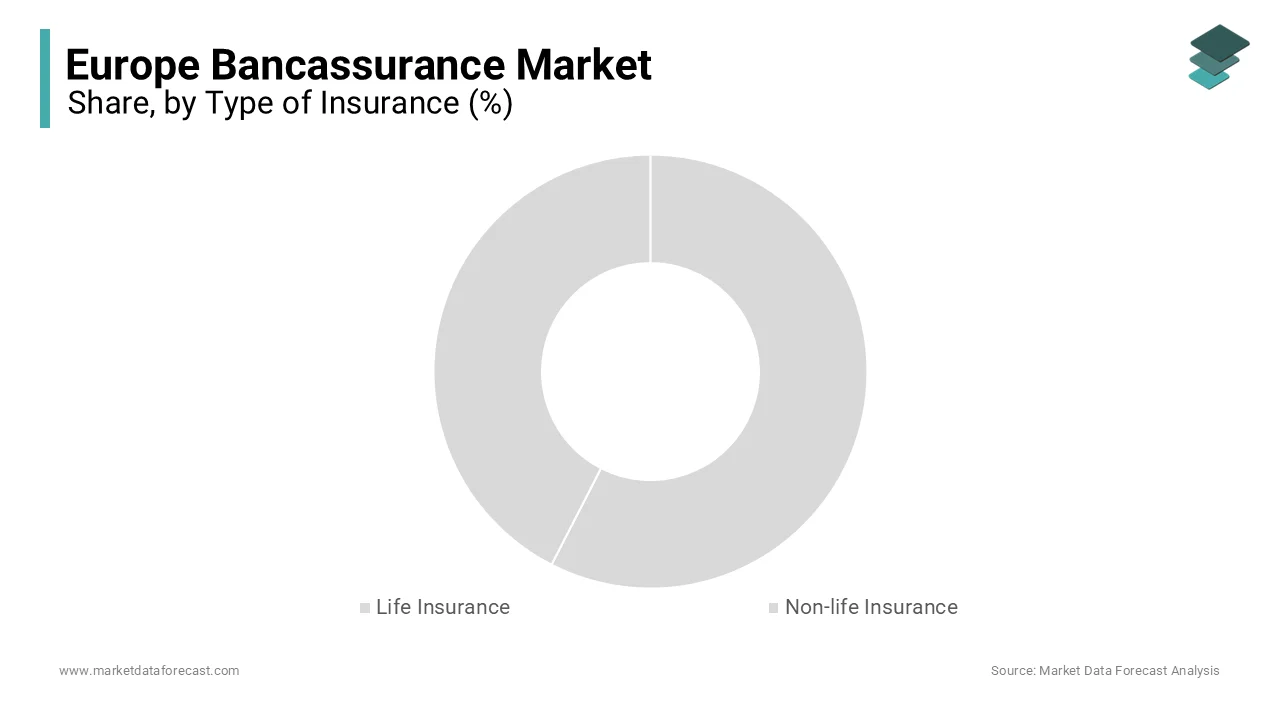

Life insurance segment was the largest by capturing 60.1% of the total Europe Bancassurance market share in 2024. The long-term financial goals, such as retirement planning and mortgage protection is attributed in leveraging the growth of the market. According to the Eurostat, over 20% of Europeans aged 65 and above rely on life insurance. Banks benefit from their trusted customer relationships, with 70% of life insurance policies sold through bancassurance linked to loans or savings plans. This segment's importance lies in its contribution to financial stability and wealth management amid an aging population. However, low interest rates challenge profitability, prompting innovation in hybrid products.

Non-life insurance segment is likely to experience a fastest CAGR of 9.5% from 2025 to 2033. This growth is fueled by rising awareness of risk management, which is driven by frequent natural disasters and health crises. According to the McKinsey & Company, over 50% of home loan customers opt for bundled property insurance is showcasing its convenience. Digital platforms have further accelerated adoption by enabling real-time issuance of policies like travel and health insurance. The segment’s importance lies in addressing evolving consumer needs for protection and flexibility. Banks are capitalizing on their integrated service models to capture this rapidly expanding market share as standalone insurers face competition.

REGIONAL ANALYSIS

France dominated the Europe’s bancassurance market with 25.5% share in 2024. The presence of integrated financial ecosystem, where banks like BNP Paribas and Crédit Agricole have long-standing partnerships with insurers. According to the French Banking Federation, over 60% of life insurance policies in France are sold through bancassurance channels which is driven by customer trust and convenience. Additionally, regulatory support for cross-selling has strengthened this model. France’s aging population further boosts demand for retirement-focused products by making bancassurance a cornerstone of its financial services sector. This robust framework ensures France remains a pioneer in delivering seamless banking and insurance solutions.

Italy is anticipated to witness a CAGR of 7.8% during the forecast period. The country’s success is rooted in its high penetration of bancassurance, with banks like Intesa Sanpaolo and UniCredit dominating the landscape. Eurostat notes that bancassurance contributes to nearly 50% of Italy’s total insurance sales, particularly in life insurance linked to savings and pensions. Italians’ strong loyalty to their primary banks facilitates cross-selling, while digital transformation has enhanced accessibility. Furthermore, Italy’s focus on financial inclusion ensures affordable insurance products for underserved populations. These factors are combined with favorable regulatory conditions that escalates the Italy’s bancassurance market growth.

Spain bancassurance market is solely to gain huge growth opportunities in the next coming years. The country’s growth is fueled by rapid digitalization by enabling banks like Santander and BBVA to offer seamless online insurance solutions. According to the McKinsey & Company, digital platforms have increased bancassurance sales by 20% since 2020 in non-life products like home and auto insurance. Spain’s young, tech-savvy population embraces mobile banking that drives adoption rates. Additionally, the government’s push for financial education has raised awareness about bundled products by enhancing customer engagement. Spain’s strategic focus on innovation and customer-centric services positions it as a dynamic player in Europe’s bancassurance landscape.

KEY MARKET PLAYERS

The major players in the Europe bancassurance market include Allianz, Generali, Zurich, AG Insurance, and AXA.

MARKET SEGMENTATION

This research report on the Europe bancassurance market is segmented and sub-segmented into the following categories.

By Type of Insurance

- Life Insurance

- Non-life Insurance

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What factors are driving the growth of the Bancassurance market in Europe?

Increased digitalization, regulatory support, customer preference for bundled financial products, and banks’ efforts to diversify revenue streams are fueling growth.

How is digital transformation impacting Bancassurance in Europe?

Digital platforms and AI-driven customer engagement are making insurance sales more efficient, improving policyholder experience and increasing penetration.

How do European regulations affect the Bancassurance market?

Regulations such as the Insurance Distribution Directive (IDD) ensure transparency, fair practices, and better consumer protection, shaping how banks sell insurance.

What is the future outlook for the Europe Bancassurance market?

The market is expected to grow steadily, with digitalization, personalized insurance products, and stronger bank-insurer collaborations shaping its evolution.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]