Europe Anti-Corrosion Coatings Market Size, Share, Trends & Growth Forecast Report By Technology (Solvent-Borne, Water-Borne, Powder Coatings, Other Technologies) ,Type,End-Use and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033

Europe Anti-Corrosion Coatings Market Size

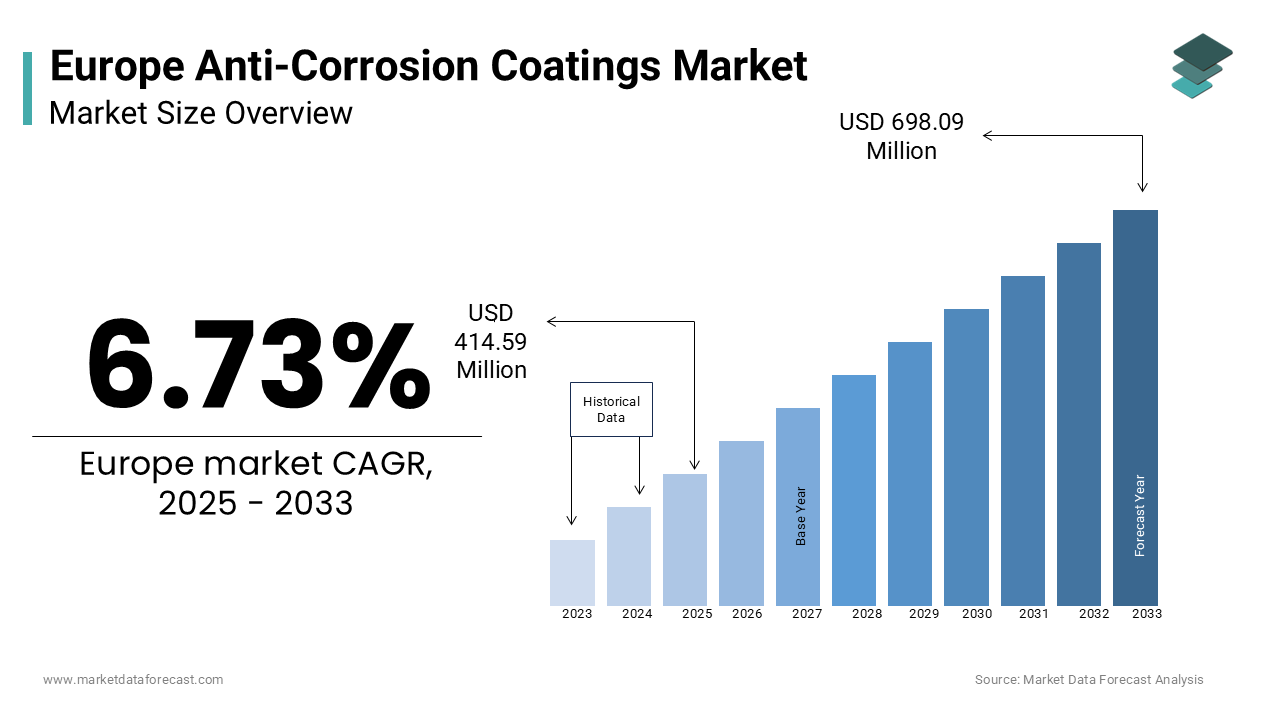

The europe anti-corrosion coatings market was worth USD 388.45 million in 2024. The European market is estimated to grow at a CAGR of 6.73% from 2025 to 2033 and be valued at USD 698.09 million by the end of 2033 from USD 414.59 million in 2025.

Anti-corrosion coatings are a cornerstone of industrial and infrastructure protection across Europe, safeguarding assets from environmental degradation and extending their operational lifespan. According to the European Corrosion Protection Association, these coatings are critical in mitigating the €200 billion annual economic losses caused by corrosion in industries such as marine, oil & gas, and construction. Germany and France lead adoption, accounting for over 40% of regional demand, as per the German Federal Ministry of Economics. The growing emphasis on eco-friendly formulations that align with EU sustainability mandates is fuelling the demand for anti-corrosion coatings in the European region. According to the French National Institute for Industrial Research, water-borne anti-corrosion coatings have reduced volatile organic compound (VOC) emissions by 35%, fostering compliance with stringent environmental regulations. As industries increasingly prioritize durability and sustainability, the demand for advanced anti-corrosion solutions continues to grow, positioning them as indispensable tools in modern engineering.

MARKET DRIVERS

Rising Demand in Marine and Oil & Gas Sectors

The rising demand for anti-corrosion coatings in the marine and oil & gas sectors is a key driver propelling the Europe market forward. The European Maritime Safety Agency states that offshore structures and vessels account for 30% of corrosion-related maintenance costs, driving investments in protective coatings. For instance, Norway’s offshore oil rigs have adopted epoxy-based coatings, achieving a 40% reduction in maintenance expenses, according to the Norwegian Petroleum Directorate. Additionally, the Italian Ministry of Infrastructure highlights that advancements in zinc-rich formulations have increased coating lifespans by 25%, ensuring compliance with safety standards. This trend underscores the pivotal role of anti-corrosion coatings in supporting Europe’s energy security while addressing ecological concerns.

Growing Emphasis on Sustainable Solutions

The growing emphasis on sustainable anti-corrosion solutions is another major driver boosting the market. The European Green Building Council reports that water-borne coatings account for 25% of the market share, driven by their low VOC emissions and alignment with circular economy principles. For example, Sweden’s construction sector has embraced eco-friendly coatings, reducing carbon footprints by 30% in new infrastructure projects, as stated by the Swedish Environmental Protection Agency. Furthermore, the Swiss Innovation Agency highlights that advancements in bio-based formulations have increased adoption rates by 20% annually, ensuring compliance with EU environmental mandates. As industries prioritize green practices, the adoption of sustainable anti-corrosion coatings is set to grow significantly, ensuring their continued relevance in modern applications.

MARKET RESTRAINTS

High Initial Costs and Application Complexity

High initial costs and application complexity act as significant restraints to the growth of the Europe anti-corrosion coatings market, particularly for small-scale projects. The European Construction Contractors Association estimates that applying high-performance coatings can increase project costs by 25%, deterring smaller firms from adopting advanced solutions. For instance, rural regions in Eastern Europe report that only 10% of construction companies utilize solvent-borne coatings due to financial constraints, as per the Czech Technical University. Additionally, the Swiss Engineering Society highlights that improper application techniques often result in coating failures, undermining broader adoption. Without targeted subsidies or training programs, these barriers will continue to limit market penetration.

Stringent Regulatory Compliance Requirements

Stringent regulatory compliance requirements pose another major restraint for the Europe anti-corrosion coatings market, particularly for manufacturers seeking to innovate. The European Chemicals Agency mandates rigorous testing under REACH regulations, requiring companies to invest heavily in certification processes. For instance, the German Federal Ministry of Economics reports that obtaining approvals for new formulations can take up to 12 months, delaying product launches and increasing costs by 30%. Additionally, the French National Institute for Environmental Research highlights that non-compliance penalties, which can exceed €1 million per violation, create financial risks for companies operating on thin margins. While these regulations aim to promote safety and sustainability, their complexity often hinders innovation and market expansion.

MARKET OPPORTUNITIES

Expansion into Renewable Energy Applications

The expansion of anti-corrosion coatings into renewable energy applications is a lucrative opportunity for market players seeking to diversify their portfolios. The European Wind Energy Association forecasts that the demand for coatings in wind turbine blades will grow at a CAGR of 15% through 2030, driven by their ability to withstand harsh weather conditions. For instance, Denmark’s offshore wind farms have adopted polyurethane-based coatings, achieving a 25% improvement in blade durability, according to the Danish Energy Agency. Similarly, Germany’s solar panel manufacturers have embraced acrylic coatings to enhance resistance to UV degradation, ensuring long-term performance. As Europe accelerates its commitment to clean energy, the role of anti-corrosion coatings in enabling sustainable infrastructure is set to expand, unlocking new revenue streams for manufacturers.

Adoption of Smart Coating Technologies

The adoption of smart coating technologies offers immense potential to drive market growth. The European Smart Materials Council states that self-healing and corrosion-detecting coatings account for 10% of the market share, valued at €1.2 billion annually. For example, France’s automotive industry has pioneered the use of smart coatings to achieve a 20% reduction in maintenance costs, as stated by the French Automotive Manufacturers Association. Additionally, the Swedish Innovation Agency highlights that advancements in nanotechnology have increased the precision and reliability of smart coatings, boosting consumer confidence in high-tech applications. As Europe continues to invest in intelligent infrastructure, the adoption of smart anti-corrosion coatings is poised to accelerate, positioning them as a cornerstone of future-ready solutions.

MARKET CHALLENGES

Resistance to Change in Traditional Industries

Resistance to change in traditional industries is a significant challenge to the Europe anti-corrosion coatings market, particularly among established builders and contractors. The European Federation of Construction Contractors reports that over 60% of firms in Central Europe remain hesitant to adopt advanced coatings due to concerns about perceived risks and lack of familiarity. For instance, Italy’s shipbuilding sector has reported that only 5% of projects utilize zinc-rich formulations, as stated by the Italian Shipbuilders Association. Additionally, cultural biases favoring conventional materials further exacerbate this issue, limiting innovation and market growth. To overcome these barriers, stakeholders must focus on demonstrating the long-term benefits of advanced coatings through pilot projects and industry collaborations.

Supply Chain Disruptions and Raw Material Scarcity

Supply chain disruptions and raw material scarcity threaten the growth of the Europe anti-corrosion coatings market, particularly amid global uncertainties. The European Petrochemical Association reports that shortages of key feedstock materials like epoxy resins have led to a 20% increase in production costs since 2022, severely impacting manufacturers in countries like Germany and Belgium. For example, Russia’s export restrictions on petrochemical products have forced European suppliers to seek alternative sources, increasing lead times by 40%. Additionally, the French National Institute for Energy Research highlights that logistical bottlenecks further compound these challenges, reducing overall market capacity. Without strategic investments in diversified sourcing strategies, the market risks stagnation amid growing demand.

SEGMENTAL ANALYSIS

By Technology Insights

The solvent-borne coatings segment had 50.1% of the Europe anti-corrosion coatings market in 2024. The leading position of solvent-borne coatings segment in the European market is attributed to their superior adhesion properties and cost-effectiveness, making them ideal for heavy-duty applications like marine and industrial structures. The German Federal Ministry of Economics reports that solvent-borne coatings reduce application costs by 30% compared to water-borne alternatives, enhancing affordability and accessibility. Additionally, their compatibility with existing infrastructure ensures consistent performance across industries. The segment's leadership reflects its critical role in meeting the diverse needs of end-use sectors while maintaining economic viability.

The water-borne coatings segment is predicted to witness the fastest CAGR of 18.4% over the forecast period owing to their increasing use in construction and automotive applications, where eco-friendly formulations are paramount. For instance, Sweden’s building sector has adopted water-borne coatings to achieve a 35% reduction in VOC emissions, aligning with EU sustainability mandates. Their alignment with green building practices makes them a focal point for future innovations, ensuring sustained growth in specialized markets.

By Type Insights

The epoxy coatings segment captured 45.8% of the Europe anti-corrosion coatings market in 2024. The growth of the epoxy coatings segment in the European market is driven by their exceptional chemical resistance and durability, making them ideal for harsh environments like offshore platforms and chemical plants. The Italian Ministry of Infrastructure reports that epoxy coatings extend asset lifespans by 40%, reducing maintenance costs and downtime. Additionally, their versatility across industries ensures widespread adoption.

The polyurethane coatings segment is estimated to witness the fastest CAGR of 21.8% of over the forecast period. The growing use of polyurethane coatings in wind energy and automotive applications, where flexibility and weather resistance are essential, is one of the major factors propelling the growth of the polyurethane coatings segment in the European market. For example, Denmark’s offshore wind farms have achieved a 25% improvement in blade durability by adopting polyurethane coatings. Their ability to meet the exacting requirements of high-tech industries positions them as a key growth driver in the coming years.

By End Use Insights

The marine and oil & gas segment accounted for 36.3% of the Europe anti-corrosion coatings market share in 2024. The dominating position of marine and oil & gas segment is attributed to their critical role in protecting offshore structures and vessels from harsh environmental conditions. The Norwegian Petroleum Directorate reports that anti-corrosion coatings reduce maintenance costs by 40% in offshore rigs, ensuring compliance with safety standards. Additionally, their compatibility with diverse substrates drives widespread adoption. The segment's leadership reflects its critical role in supporting Europe’s energy security while addressing ecological concerns.

The renewable energy segment is predicted to register the highest CAGR of 22.8% over the forecast period owing to the increasing use of coatings in wind turbine blades and solar panels, where durability and performance are paramount. For instance, Germany’s wind energy sector has achieved a 30% improvement in blade efficiency by adopting advanced coatings. Their alignment with Europe’s clean energy goals makes them a focal point for future innovations, ensuring sustained growth in specialized markets.

REGIONAL ANALYSIS

Germany accounted for 24.4% of the Europe anti-corrosion coatings market share in 2024. The leading position of Germany in the European market is attributed to its robust manufacturing base and strong emphasis on sustainability. For instance, BASF accounts for 20% of regional production, leveraging cutting-edge technologies to enhance efficiency. The country’s leadership reflects its pivotal role in driving innovation and meeting the diverse needs of end-use industries, particularly in automotive and construction.

France is a prominent player in the European anti-corrosion coatings market. The thriving marine and construction sectors of France that rely heavily on anti-corrosion coatings for durability and compliance with EU regulations is driving the French market growth. For example, TotalEnergies, based in Paris, utilizes advanced coatings in offshore rigs, contributing to its global success. France’s commitment to green practices further accelerates market growth, ensuring long-term relevance.

Italy accounts for a notable share of the European market over the forecast period owing to the thriving shipbuilding and industrial sectors, as stated by the Italian Shipbuilders Association. Milan’s manufacturing hubs, valued at €10 billion, drive demand for durable and eco-friendly coatings, enhancing asset longevity and performance. Investments in sustainable solutions highlight its commitment to innovation.

Spain is another key player in the European market owing to its industrial heritage. Barcelona’s marine sector, valued at €5 billion, drives demand for anti-corrosion coatings, ensuring compliance with safety standards.

The UK is a notable market for anti-corrosion coatings in Europe. The prominent role of the UK in the European market is driven its advanced automotive and renewable energy sectors, according to the British Engineering Society. London’s research institutions foster innovation, driving adoption of high-performance coatings in emerging applications.

MARKET SEGMENTATION

This research report on the europe anti-corrosion coatings market is segmented and sub-segmented based on categories.

By Technology

- Solvent-Borne

- Water-Borne

- Powder Coatings

- Other Technologies

By Type

- Epoxy

- Polyurethane

- Acrylic

- Alkyd

- Zinc

- Chlorinated Rubber

- Other Types

By End Use

- Marine

- Oil & Gas

- Industrial

- Construction

- Energy

- Automotive

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What are the challenges faced by the Europe anti-corrosion coatings market?

Environmental concerns, high costs, and the volatility of raw material supplies pose challenges in the market.

What are the emerging trends in the European anti-corrosion coatings market?

Trends include the development of eco-friendly coatings, smart coatings, and the use of nanotechnology to enhance corrosion resistance.

What is the future outlook of the anti-corrosion coatings market in Europe?

The market is expected to grow due to industrial expansion, infrastructure needs, and increasing demand for sustainable solutions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]