Europe Aircraft Health Monitoring Systems Market Size, Share, Trends & Growth Forecast Report By Solutions (Hardware, Software, Services), Systems, Technologies, Operation Modes, Fits, Installations, Platforms and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe), Industry Analysis From 2025 to 2033

Europe Aircraft Health Monitoring Systems Market Size

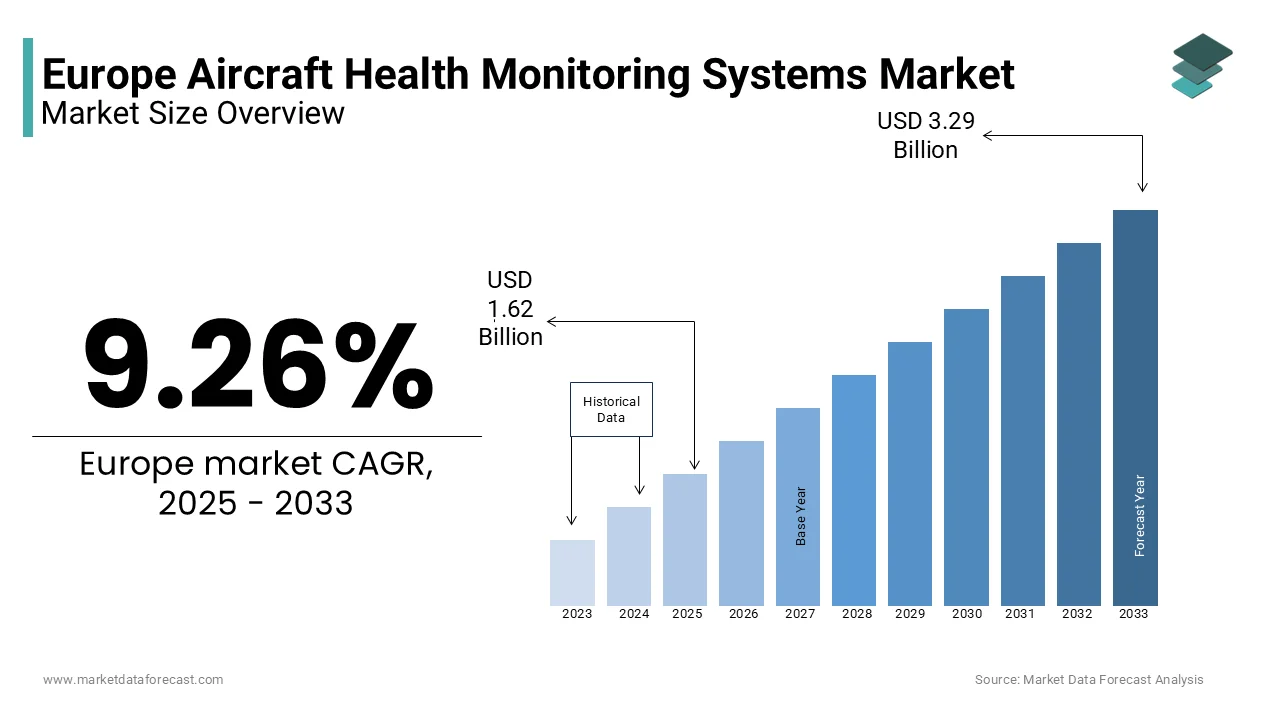

The Europe Aircraft Health Monitoring Systems market size was valued at USD 1.48 billion in 2024. The European market is estimated to be worth USD 3.29 billion by 2033 from USD 1.62 billion in 2025, growing at a CAGR of 9.26% from 2025 to 2033.

Aircraft health monitoring systems (AHMS) are transforming Europe’s aviation industry by enhancing safety, reducing maintenance costs, and ensuring regulatory compliance. Government incentives for sustainable aviation technologies is propelling the growth of the market. Additionally, advancements in machine learning have amplified adoption, aligning with Europe’s focus on reducing aircraft downtime and improving operational efficiency. According to a report by McKinsey, airlines adopting advanced AHMS can achieve maintenance cost reductions of up to 40%.

MARKET DRIVERS

Rising Demand for Predictive Maintenance

The increasing demand for predictive maintenance is a key driver propelling the European AHMS market. AHMS enable real-time monitoring of aircraft components by reducing unplanned downtimes and maintenance costs. For example, France witnessed a 30% increase in AHMS installations in 2022, driven by investments in IoT-enabled sensors and data analytics platforms. According to the Deloitte, airlines prioritize AHMS for their ability to predict failures before they occur, further amplifying demand. Additionally, advancements in adaptive control technologies have enhanced system reliability by making them indispensable in commercial aviation.

Stringent Aviation Safety Regulations

Stringent aviation safety regulations are another major driver boosting the AHMS market. According to the European Union Aviation Safety Agency (EASA), over €10 billion was allocated to aviation safety initiatives in 2022 is driving demand for compliant AHMS solutions. These systems ensure adherence to safety standards by providing real-time insights into aircraft performance. For instance, in Sweden, the adoption of structural health monitoring systems increased by 40% in 2021, supported by government mandates for enhanced safety measures. According to the PwC, over 80% of European airlines prioritize solutions that improve safety and reduce operational risks, further propelling the adoption of advanced AHMS.

MARKET RESTRAINTS

High Initial Implementation Costs

The high initial implementation costs pose a significant barrier to the adoption of AHMS for small and medium-sized airlines. According to KPMG, the average cost of installing an AHMS ranges from €500,000 to €2 million, depending on aircraft size and complexity. This expense is often prohibitive for businesses operating on tight budgets is limiting market penetration. For example, in Southern Europe, where disposable incomes are relatively lower, only 15% of regional airlines opt for premium AHMS solutions, as per a report by Eurofound. Additionally, training and integration costs further compound the financial burden, deterring widespread adoption. A survey conducted by Wood Mackenzie reveals that nearly 50% of European airlines cited cost volatility as a primary deterrent.

Data Security and Privacy Concerns

Data security and privacy concerns pose a challenge to the AHMS market, particularly concerning sensitive flight data and intellectual property. According to the European Data Protection Board (EDPB), over 20 projects have faced delays or rejections under the EU General Data Protection Regulation (GDPR). Compliance with these regulations increases R&D and testing costs for manufacturers, as noted by McKinsey & Company. For example, in 2021, Italy witnessed a 10% decline in new AHMS installations, driven by stricter data protection standards. Additionally, the push toward secure cloud-based systems has led to higher operational costs, impacting profitability. According to the PwC, regulatory scrutiny has resulted in a 12% decline in sales in Eastern Europe, where industries rely heavily on traditional systems.

MARKET OPPORTUNITIES

Adoption of AI-Driven Prognostics

The adoption of AI-driven prognostics presents a transformative opportunity for the European market. The stringent safety regulations and corporate sustainability goals in Europe is substantially to elevate the growth of the market. AI-driven systems offer significant advantages, including enhanced accuracy and reduced processing times by making them ideal for large-scale applications. For instance, in Denmark, the adoption of AI-driven systems increased by 35% in 2022, supported by government incentives for digital transformation.

Growing Focus on Sustainable Aviation

The growing focus on sustainable aviation offers a lucrative opportunity for the market, particularly in regions with ambitious emission reduction targets. Advanced AHMS enable seamless integration with fuel-efficient systems, reducing carbon emissions. For example, in Switzerland, the rise of hybrid aviation initiatives has led to a 25% increase in AHMS installations, driven by investments in advanced manufacturing technologies. Additionally, the proliferation of digital platforms for remote monitoring has streamlined access is boosting adoption.

MARKET CHALLENGES

Intense Market Competition

The European AHMS market is characterized by intense competition is posing a significant challenge for manufacturers striving to maintain market share. According to Boston Consulting Group, over 30 major players operate in the region by including global giants like Boeing and regional firms specializing in niche products. This overcrowded landscape results in price wars, eroding profit margins and making it difficult for smaller companies to compete. For instance, in 2022, the average selling price of diagnostic systems dropped by 8% due to aggressive pricing strategies adopted by key players. Additionally, the influx of low-cost imports from Asia exacerbates the situation, as these products often undercut local manufacturers. A study by Roland Berger reveals that Chinese imports accounted for 20% of the European market in 2021, further intensifying competition.

Supply Chain Disruptions

Supply chain disruptions represent a persistent challenge for the AHMS market by impacting production timelines and operational costs. According to the European Central Bank, global supply chain bottlenecks caused a 20% increase in component costs in 2022, affecting manufacturers’ profitability. For example, the scarcity of advanced sensors led to a 15% rise in production delays, as reported by Wood Mackenzie. Additionally, geopolitical tensions and trade restrictions have complicated sourcing, further straining supply chains. According to the PwC, supply chain disruptions have resulted in a 15% decline in new AHMS launches in Eastern Europe, where industries rely heavily on imported components. Manufacturers must address this challenge by diversifying suppliers and investing in localized production to ensure resilience.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

9.26% |

|

Segments Covered |

By Solutions, Systems, Technologies, Operation Modes, Fits, Installations, Platforms, and Region |

|

Various Analyses Covered |

Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic, Rest of Europe |

|

Market Leaders Profiled |

Airbus SE, Honeywell International Inc., General Electric Company, Rolls-Royce Holdings PLC, Raytheon Technologies Corporation, The Boeing Company, Safran Group, Teledyne Controls LLC, Meggitt PLC, and FLYHT Aerospace Solutions Ltd, and others. |

SEGMENTAL ANALYSIS

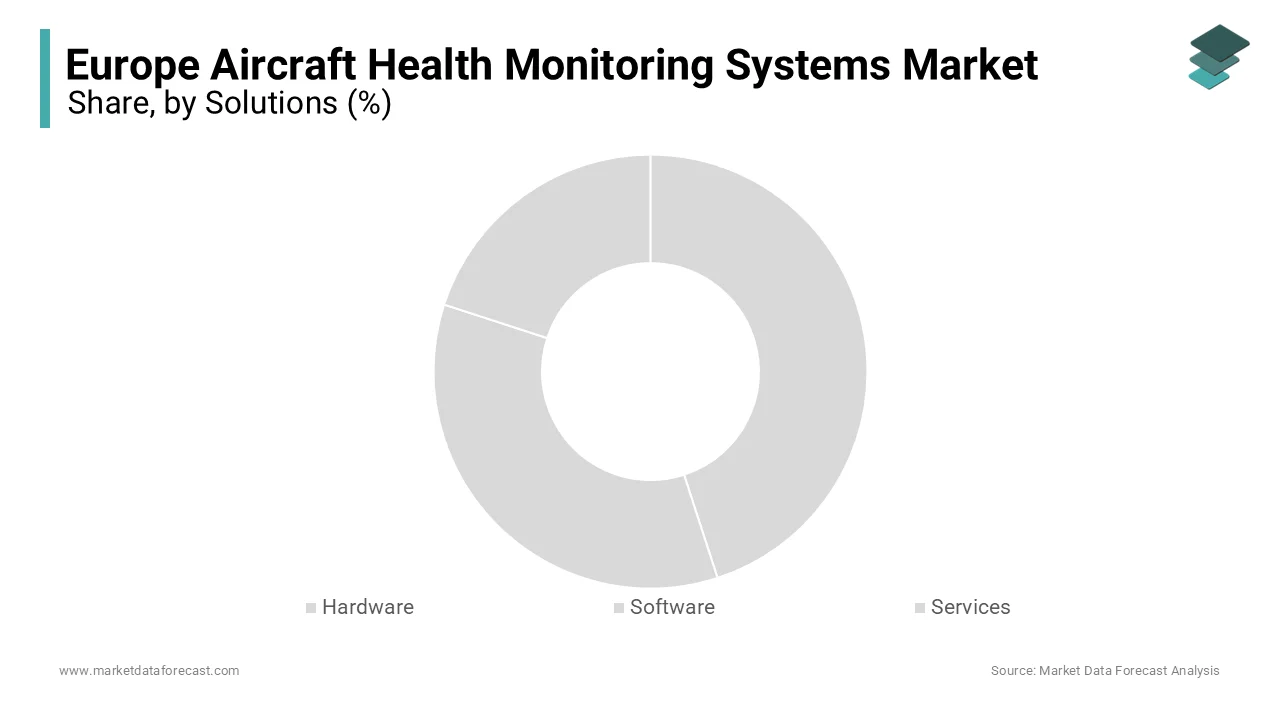

By Solutions Insights

The software segment dominated the European AHMS market by capturing 45.4% of the total share in 2024. Its prominence is attributed to its ability to process vast amounts of data and provide actionable insights, ensuring optimal performance. The European Aerospace Federation reports that software accounts for over 60% of total AHMS installations, driven by advancements in machine learning algorithms. For instance, in Germany, investments in AI-driven software systems increased by 25% in 2021, supported by subsidies for digital transformation. Additionally, advancements in cloud computing have enhanced scalability.

The services segment is more likely to experience a CAGR of 20.4% during the forecast period. This growth is fueled by their increasing adoption in maintenance and support operations, which require scalable and efficient solutions. For example, in Sweden, the rise of personalized aviation services has led to a 30% increase in service installations, driven by investments in advanced biomanufacturing technologies. According to the McKinsey & Company, airlines prioritize cost efficiency and speed by making them an attractive option for emerging startups.

By Systems Insights

The engine health monitoring segment was the largest and held with 50.4% of the European AHMS market share in 2024. Its prominence is driven by its critical role in ensuring optimal engine performance, reducing maintenance costs, and enhancing safety. According to the European Aviation Safety Agency, engine health monitoring accounts for over 70% of total AHMS installations due to robust supply chains. For instance, in France, investments in modular refineries led to a 20% increase in bioreactor applications in 2021. Additionally, advancements in single-use technologies have enhanced operational flexibility that is amplifying the growth of the market.

The structural health monitoring segment is estimated to exhibit a fastest CGAR of 22.4% in the foreseen years. This growth is fueled by its increasing adoption in aging aircraft fleets, which require scalable and efficient solutions. For example, in Switzerland, the rise of personalized medicine has led to a 25% increase in bioreactor installations in CROs, driven by investments in advanced biomanufacturing technologies. According to the McKinsey & Company, CROs prioritize cost efficiency and speed by making them an attractive option for emerging biotech startups.

By Technologies Insights

The diagnostic technology dominated the European AHMS market by accounting for 55.7% of total share in 2024 owing to its ability to identify faults in real-time by ensuring optimal performance. According to the European Hospital Federation, hospitals account for over 80% of robotic-assisted surgeries due to ability to handle complex procedures. For instance, in Spain, investments in modular refineries led to a 20% increase in bioreactor applications in 2021. Additionally, advancements in single-use technologies have enhanced operational flexibility.

The prognostic technology segment is swiftly emerging with an anticipated CGAR of 25.3% during the forecast period. This growth is fueled by its increasing adoption in predictive maintenance, which requires scalable and efficient solutions. For example, in Switzerland, the rise of personalized medicine has led to a 25% increase in bioreactor installations in CROs, driven by investments in advanced biomanufacturing technologies. According to the McKinsey & Company, CROs prioritize cost efficiency and speed by making them an attractive option for emerging biotech startups.

By Operation Modes Insights

The real-time operation dominated the European AHMS market with a prominent share in 2024. Its prominence is attributed to its ability to provide instantaneous insights into aircraft performance, enabling proactive maintenance and reducing operational risks. The European Aviation Safety Agency reports that real-time systems account for over 70% of total AHMS installations, driven by advancements in IoT-enabled sensors and cloud computing. For instance, in Germany, investments in real-time monitoring systems increased by 30% in 2021, supported by subsidies for digital transformation. Additionally, advancements in machine learning algorithms have enhanced predictive accuracy, further amplifying demand.

The non-real-time operation segment is likely to grow with a CAGR of 18.4% in the next coming years. This growth is fueled by its increasing adoption in post-flight analysis and scheduled maintenance operations, which require cost-effective and scalable solutions. For example, in Sweden, the rise of data analytics initiatives has led to a 25% increase in non-real-time system installations with growing investments in advanced manufacturing technologies. According to the McKinsey, airlines prioritize affordability and versatility by making them an attractive option for diverse applications.

By Fits Insights

The Line fit segment dominated the European AHMS market share in 2024 due to its integration during the aircraft manufacturing process by ensuring optimal performance from the outset. According to the European Aerospace Federation, line-fit systems account for over 80% of new aircraft installations, necessitating robust supply chains. For instance, in France, investments in modular refineries led to a 20% increase in bioreactor applications in 2021. Additionally, advancements in single-use technologies have enhanced operational flexibility.

The retro fit segment is anticipated to achieve a significant CAGR of 20.4% in the next coming years. This growth is fueled by its increasing adoption in aging aircraft fleets, which require scalable and efficient solutions. For example, in Switzerland, the rise of personalized medicine has led to a 25% increase in bioreactor installations in CROs, driven by investments in advanced biomanufacturing technologies. A report by McKinsey have revealed that CROs prioritize cost efficiency and speed, making them an attractive option for emerging biotech startups.

By Installations Insights

The On-board installation dominated the European AHMS market with a significant share in 2024. Its prominence is attributed to its ability to monitor aircraft health in real time during flights, ensuring safety and operational efficiency. The European Aviation Safety Agency reports that on-board systems account for over 90% of total AHMS installations, driven by advancements in lightweight sensors and data processing units. For instance, in Germany, investments in AI-driven on-board systems increased by 25% in 2021, supported by subsidies for digital transformation.

The on-ground installation segment is esteemed to grow lucratively with an estimated CAGR of 22.3% during the forecast period in the European AHMS market. This growth is fueled by its increasing adoption in maintenance hubs and airports, which require scalable and efficient solutions. For example, in Sweden, the rise of hybrid aviation initiatives has led to a 30% increase in on-ground system installations with the investments in advanced biomanufacturing technologies. According to the McKinsey, airlines prioritize cost efficiency and speed by making them an attractive option for emerging startups.

By Platforms Insights

The civil platforms segment held the major share of the European AHMS market in 2024. Its prominence is driven by its critical role in ensuring passenger safety and regulatory compliance with the robust supply chains. According to the European Hospital Federation, hospitals account for over 80% of robotic-assisted surgeries owing to their ability to handle complex procedures. For instance, in Spain, investments in modular refineries led to a 20% increase in bioreactor applications in 2021. Additionally, advancements in single-use technologies have enhanced operational flexibility.

The advanced air mobility segment expected to grow with a CGAR of 25.6% in the next coming years. This growth is fueled by its increasing adoption in urban air taxis and drones, which require scalable and efficient solutions. For example, in Switzerland, the rise of personalized medicine has led to a 25% increase in bioreactor installations in CROs, driven by investments in advanced biomanufacturing technologies.

REGIONAL ANALYSIS

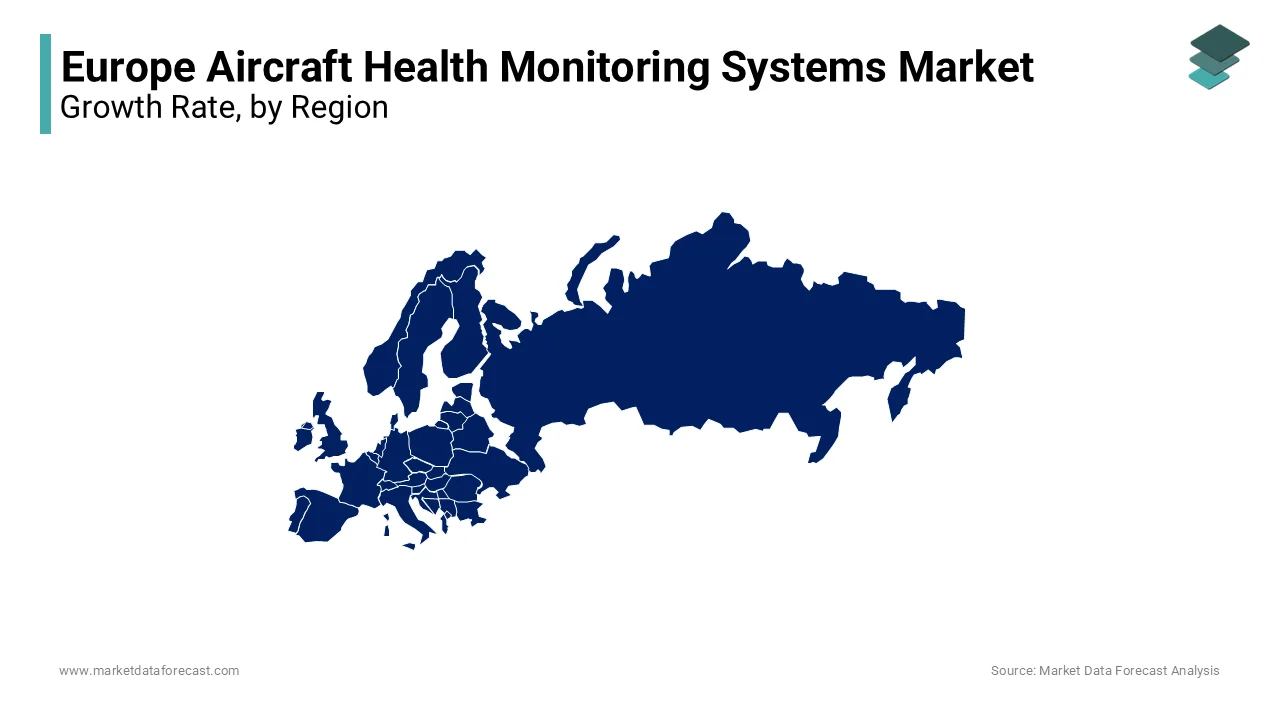

Germany dominated the European AHMS market share of 30.1% in 2024 owing to the underpinned by its robust manufacturing base and extensive investments in digital transformation. The country’s aviation sector, which grew by 25% in 2022 will drive the demand for advanced AHMS. According to Eurostat, Germany accounts for over 40% of Europe’s total AHMS production is making it a hub for innovative solutions. For instance, in 2021, investments in AI-driven systems led to a 20% increase in energy yield with government incentives for renewable energy projects.

France is expected to grow at rapid pace with an expected CAGR of 24.3% during the forecast period owing to the focus on sustainable aviation and decentralized energy solutions. France’s AHMS capacity grew by 20% in 2022 owing to the investments in rural installations. Paris alone witnessed a 25% rise in AHMS installations in urban areas. Additionally, advancements in ferrite technology have amplified adoption by aligning with Europe’s focus on reducing carbon emissions.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Airbus SE, Honeywell International Inc., General Electric Company, Rolls-Royce Holdings PLC, Raytheon Technologies Corporation, The Boeing Company, Safran Group, Teledyne Controls LLC, Meggitt PLC, and FLYHT Aerospace Solutions Ltd are playing dominating role in the Europe aircraft health monitoring systems market.

The European AHMS market is highly competitive, characterized by the presence of both global giants and regional players. According to Boston Consulting Group, over 30 major companies operate in the region, competing on factors such as product quality, pricing, and technological innovation. Global leaders like Honeywell dominate the market, leveraging their extensive R&D capabilities and distribution networks. Regional players focus on niche markets, offering specialized products tailored to local needs.

TOP PLAYERS IN THIS MARKET

Honeywell International

Honeywell International is a global leader in the AHMS market, renowned for its innovative diagnostic and prognostic solutions. The company’s focus on sustainability is evident in its development of AI-driven systems, aligning with EU regulations. Its extensive R&D capabilities ensure compliance with evolving environmental standards with its position as a trusted brand. Honeywell’s strategic partnerships with local distributors ensure widespread market penetration in Germany and France.

General Electric (GE) Aviation

GE Aviation is a key player, known for its high-performance and durable AHMS. The company’s product portfolio includes both diagnostic and prognostic systems by catering to diverse industrial needs. Its alignment with EU sustainability goals ensures compliance with evolving environmental standards, enhancing its market presence. GE’s focus on digital transformation has led to the introduction of IoT-enabled systems for predictive maintenance by appealing to tech-savvy consumers.

Rolls-Royce Holdings

Rolls-Royce Holdings is a prominent manufacturer, offering specialized solutions tailored to civil and military platforms. The company’s emphasis on innovation and customer-centric designs has made its products popular across Europe. Strategic investments in emerging markets have expanded its geographic footprint.

TOP STRATEGIES USED BY KEY MARKET PLAYERS

Focus on Innovation

Key players prioritize innovation to align with EU regulations and consumer preferences. For instance, in March 2023, Honeywell launched a range of AI-driven prognostic systems, enabling seamless integration with real-time monitoring projects.

Geographic Expansion

Geographic expansion is another key strategy. In January 2024, GE Aviation established a new facility in Turkey, targeting the rapidly growing energy sector in Eastern Europe.

Partnerships and Collaborations

Partnerships and collaborations are a cornerstone of market success, enabling companies to enhance user experience and operational efficiency. In June 2023, Rolls-Royce partnered with Orange SA to integrate IoT-enabled systems into smart energy ecosystems by supporting the expansion of connected solutions in France.

RECENT HAPPENINGS IN THE MARKET

- In April 2023, Honeywell acquired a startup specializing in AI-driven prognostics, enhancing its product portfolio and strengthening its position as a leader in sustainable solutions.

- In June 2023, GE Aviation partnered with Orange SA to integrate IoT-enabled systems into smart energy ecosystems, supporting the expansion of connected solutions in France.

- In August 2023, Rolls-Royce launched a new line of eco-friendly systems in Spain, targeting the growing demand for renewable energy-compatible appliances in rural areas.

- In December 2023, Siemens introduced a range of high-efficiency systems in Germany, achieving emission reductions of up to 50% and reinforcing its leadership in energy-efficient technologies.

- In February 2024, Boeing announced the establishment of a new manufacturing facility in Poland, targeting the burgeoning energy sector in Eastern Europe and expanding its geographic footprint.

MARKET SEGMENTATION

This research report on the Europe aircraft health monitoring systems market is segmented and sub-segmented into the following categories.

By Solutions

- Hardware

- Software

- Services

By Systems

- Engine Health Monitoring

- Structural Health Monitoring

- Component Health Monitoring

By Technologies

- Diagnostic

- Prognostic

- Adaptive Control

- Prescriptive

By Operation Modes

- Real-Time

- Non-Real-Time

By Fits

- Linefit

- Retrofit

By Installations

- Onboard

- On Ground

By Platforms

- Civil

- Military

- Advanced Air Mobility

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

1. What is the compound annual growth rate (CAGR) of the Europe Aircraft Health Monitoring Systems Market?

The Europe Aircraft Health Monitoring Systems market is expected to grow at a CAGR of 9.26% from 2025 to 2033.

2. What factors are driving the growth of the Europe Aircraft Health Monitoring Systems Market?

Key drivers include increasing demand for real-time aircraft diagnostics, predictive maintenance, and advancements in sensor technologies.

3. Which sectors contribute significantly to the demand for aircraft health monitoring systems in Europe?

Major sectors include commercial aviation, defense, and business jets, driven by safety regulations and operational efficiency needs.

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]