Europe Genetic Testing Market Size, Share, Trends & Growth Forecast Report By Type (Cancer Testing, Pharmacogenomics Testing, Prenatal Testing, Predisposition Testing), Application and Country (United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands and Rest of Europe), Industry Analysis from 2025 to 2033

Europe Genetic Testing Market Size

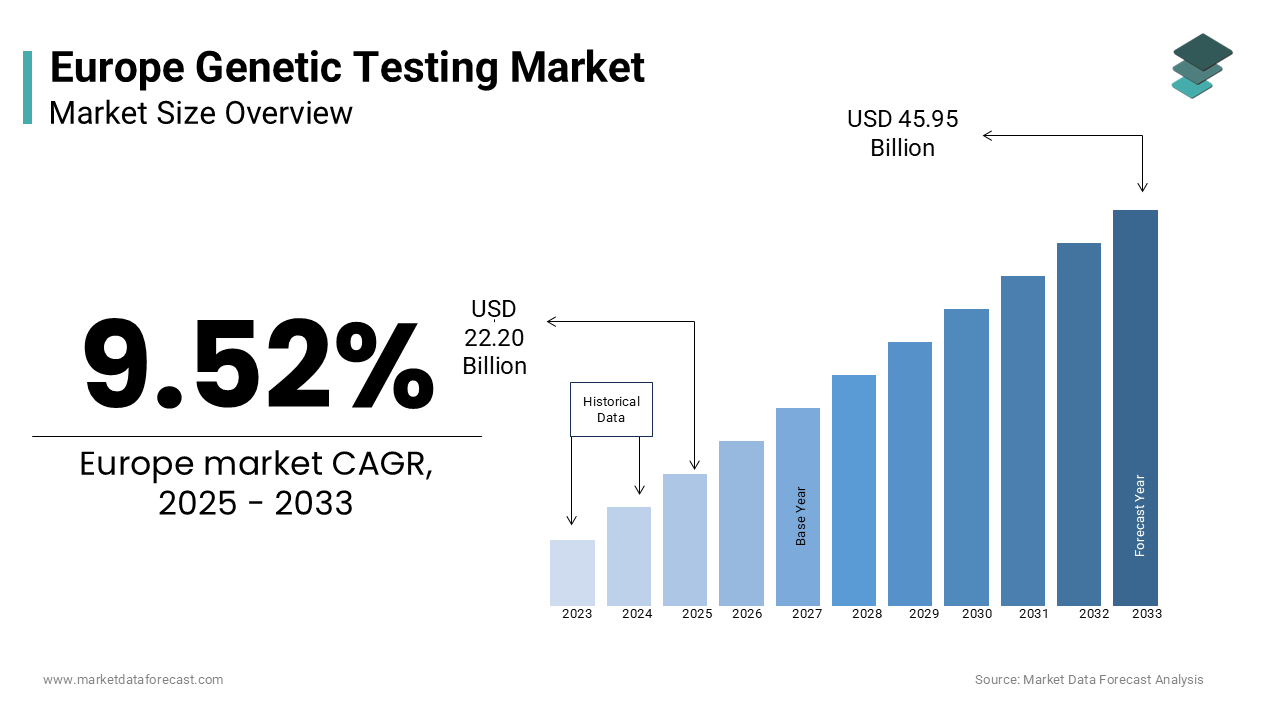

The genetic testing market size in Europe was valued at USD 20.27 billion in 2024. The European market is further expected to grow from USD 22.20 billion in 2025 to USD 45.95 billion by 2033, growing at a CAGR of 9.52% during the forecast period.

The Europe genetic testing market has emerged as a pivotal player in healthcare innovation, driven by advancements in genomics and personalized medicine.

A significant factor shaping the market is the growing burden of chronic diseases across Europe. As per the European Cancer Organisation, cancer cases are projected to rise by 25% by 2030 by creating a critical need for early detection through genetic testing. Additionally, collaborations between biotech firms and healthcare providers have amplified adoption by positioning Europe as a leader in genetic diagnostics globally.

MARKET DRIVERS

Rising Prevalence of Chronic Diseases

The rising prevalence of chronic diseases, particularly cancer, is a cornerstone driving the Europe genetic testing market. According to the European Cancer Patient Coalition, genetic predisposition accounts for 5-10% of all cancer cases owing to the advanced testing solutions for early detection and prevention. These tests enable personalized treatment plans that is by improving patient outcomes and reducing healthcare costs.

A pivotal factor amplifying this growth is the integration of genetic testing into mainstream healthcare. European hospitals adopted genetic testing protocols in 2023 owing to the partnerships with diagnostic labs. For instance, breast cancer genetic testing kits reduced late-stage diagnoses by 30%, saving an estimated €2 billion annually in treatment costs. These innovations not only enhance accessibility but also align with EU goals for sustainable healthcare systems.

Advancements in Genomic Technologies

Advancements in genomic technologies are significantly bolstering demand for genetic testing. According to Frost & Sullivan, investments in next-generation sequencing (NGS) platforms grew by 40% in 2023 by enabling faster and more accurate analysis of genetic mutations. These technologies are particularly valuable for pharmacogenomics by allowing tailored drug prescriptions based on individual genetic profiles. According to a study by Accenture, NGS-based tests improved medication efficacy by 50% by reducing adverse drug reactions in European populations. Additionally, government funding for genomic research has expanded adoption by reinforcing genetic testing’s role in modernizing healthcare delivery. These factors collectively drive the adoption of advanced testing solutions.

MARKET RESTRAINTS

High Costs and Limited Reimbursement Policies

One of the primary barriers impeding the growth of the Europe genetic testing market is the high cost of testing and limited reimbursement policies. According to Deloitte, the average cost of a comprehensive genetic test can exceed €1,000 is deterring patients and healthcare providers from adopting these solutions. Additionally, disparities in insurance coverage remain a concern in countries like Italy and Spain. According to a report by PwC, only 30% of European insurers offered reimbursement for genetic tests in 2023, creating financial barriers for patients. While larger institutions can absorb these expenses, smaller clinics often struggle to justify the investment by creating a fragmented market landscape.

Ethical and Privacy Concerns

Ethical and privacy concerns pose another significant restraint for the Europe genetic testing market. According to Capgemini, over 70% of European consumers expressed fears about unauthorized access to genetic data by raising questions about data security and compliance with GDPR regulations.

For instance, a study by KPMG reveals that privacy-related issues delayed the adoption of direct-to-consumer genetic tests by 20% in 2023 among older demographics. Addressing these concerns requires significant investments in encryption technologies and threat detection systems, which may not be feasible for all stakeholders.

MARKET OPPORTUNITIES

Expansion into Personalized Medicine

The expansion into personalized medicine presents a transformative opportunity for the Europe genetic testing market. European pharmaceutical companies integrated genetic testing into drug development pipelines in 2023 by creating a pressing need for scalable solutions. These tests enable tailored treatments owing to the improved efficacy and reducing side effects.

According to a report by EvaluatePharma, pharmacogenomics testing grew by 35% in 2023 with collaborations between biotech firms and cleanroom providers. These systems ensure precise control over environmental conditions, ensuring optimal results. Additionally, government incentives promoting biotechnology research have expanded adoption by reinforcing the segment’s rapid expansion.

Growth of Direct-to-Consumer Testing

The growth of direct-to-consumer (DTC) genetic testing offers another promising avenue for growth in the Europe genetic testing market. According to Frost & Sullivan, DTC test sales grew by 50% in 2023 owing to the consumer demand for ancestry and health insights. These products cater to younger demographics, who prioritize accessible and affordable solutions. The fitness and wellness brands expanded functionality by enabling features like personalized nutrition plans. These innovations not only drive revenue but also position genetic testing as a cornerstone of preventive healthcare ecosystems.

MARKET CHALLENGES

Technological Limitations and Data Interpretation

Technological limitations and challenges in data interpretation represent a significant challenge for the Europe genetic testing market. The current NGS platforms face difficulties in analyzing rare genetic mutations in complex diseases like neurodegenerative disorders. This limitation is particularly evident in predisposition testing, where accuracy is critical for patient outcomes.

For example, a report by ABB reveals that misinterpretation of genetic data led to incorrect diagnoses in 15% of cases in 2023 with the persistent gaps in analytical tools. The rapid pace of technological disruption underscores the need for continuous adaptation and differentiation while innovation in AI-driven algorithms can mitigate this challenge.

Competition from Alternative Diagnostic Tools

Intense competition from alternative diagnostic tools poses another pressing challenge for the Europe genetic testing market. These alternatives offer advantages like non-invasive procedures and faster results, threatening the dominance of traditional genetic tests. For instance, a study by the German Aerospace Center (DLR) has shown that the liquid biopsy captured 20% of the cancer diagnostics market share in 2023, driven by its superior performance in early-stage detection. While collaboration with academic institutions can address this challenge, the sheer scale of required R&D investments remains a persistent hurdle, slowing market progress.

SEGMENTAL ANALYSIS

By Application Insights

The cancer testing segment dominated the Europe genetic testing market by capturing 40.3% of the total share in 2024 owing to the growing burden of cancer cases and the increasing adoption of genetic testing for early detection and personalized treatment. A key factor fueling this dominance is the emphasis on precision medicine. According to the European Cancer Organisation, genetic testing reduced late-stage cancer diagnoses by 25% in 2023 by improving survival rates and reducing treatment costs. Additionally, government funding for cancer research has amplified adoption.

The pharmacogenomics testing segment is gaining traction with a projected CAGR of 15.8% during the forecast period. This growth is fueled by the increasing adoption of genetic testing for drug response prediction by ensuring tailored prescriptions and minimizing adverse reactions. The growth is also driven by collaborations between pharmaceutical companies and testing labs. These innovations not only improve patient outcomes but also align with EU goals for sustainable healthcare systems.

By Test Insights

The diagnostic testing segment dominated the Europe genetic testing market by capturing 45.4% of the total share in 2024 owing to the growing demand for accurate and early detection of genetic disorders in chronic diseases like cancer and cardiovascular conditions.

A key factor fueling this dominance is the emphasis on reducing healthcare costs through early intervention. According to the European Society of Human Genetics, diagnostic testing reduced hospital readmissions by 30% in 2023 by enabling timely treatment and improving patient outcomes. Additionally, advancements in next-generation sequencing (NGS) technologies have improved accuracy and accessibility. According to a report by PwC, over 70% of European hospitals prioritize diagnostic testing for chronic disease management.

The Neonatal testing segment is likely to hit a CAGR of 14.5% during the forecast period. This growth is fueled by the increasing adoption of genetic testing for newborn screening by ensuring early detection of metabolic and genetic disorders. The neonatal testing enable early intervention by reducing long-term healthcare costs and improving quality of life. Additionally, collaborations with pediatric clinics have expanded functionality by enabling seamless integration with national healthcare systems.

REGIONAL ANALYSIS

Germany genetic testing market held the dominant share of 22.3% in 2024 with its robust healthcare infrastructure and strong emphasis on precision medicine, supported by initiatives like the National Genome Strategy.

A pivotal factor fueling this dominance is the growing burden of cancer cases. According to the German Cancer Society, genetic testing reduced late-stage diagnoses by 30% in 2023 by creating a surge in demand for advanced solutions. Additionally, partnerships with biotech firms have amplified adoption.

The UK is anticipated to register a CAGR of 13.2% during the forecast period. London and Cambridge have emerged as critical hubs owing to the robust investments in genomics and personalized medicine.

The transition to precision healthcare has significantly bolstered demand. As per the UK Genomics Medicine Service, genetic testing enabled tailored treatments for over 50,000 patients in 2023 by improving outcomes and reducing costs. Additionally, government funding for cancer research has expanded accessibility with the UK’s prominence in sustainable healthcare solutions.

France is likely to gain huge popularity in the genetic testing market in next coming years. Paris has emerged as a key player by hosting major genomic research labs and startups.

A major driver of this growth is the increasing adoption of NGS platforms. According to the French Ministry of Health, NGS-based tests improved diagnostic accuracy by 40% in 2023, necessitating reliable genetic testing systems. Additionally, urbanization initiatives have amplified demand for scalable and efficient solutions in hospitals and diagnostic centers.

Italy genetic testing market is expected to have significant growth opportunities in the next coming years. Milan and Rome are rapidly emerging as key hubs, supported by a growing emphasis on chronic disease management. A key factor driving Italy’s growth is the increasing adoption of pharmacogenomics testing. According to the Italian Society of Human Genetics, these tests improved medication efficacy by 50% in 2023, ensuring compliance with EU regulations. Additionally, government incentives supporting industrial modernization have expanded adoption by ensuring scalability and safety.

Spain genetic testing market is also to have significant growth opportunities during the forecast period. A pivotal driver of Spain’s growth is the emphasis on neonatal screening. According to the Spanish Health Ministry, genetic testing improved early detection rates by 60% in 2023 by creating a surge in demand for consumables and equipment. Additionally, collaborations with private sector players have expanded functionality by enabling seamless integration with national healthcare systems.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

A few of the noteworthy companies operating in the European genetic testing market profiled in this report are Abbott Laboratories, Roche Molecular Diagnostics Inc., Abbott Molecular Inc., AutoGenomics Inc., Celera Group, ELITech Group, BioRad Laboratories, PerkinElmer Inc., Roche Diagnostics Corp., Quest Diagnostics Inc., Transgenomic Inc., and Applied Biosystems Inc.

The Europe genetic testing market is characterized by intense competition with the presence of global giants and regional innovators vying for market share. Major players like Thermo Fisher Scientific, Illumina Inc., and Myriad Genetics dominate the landscape by leveraging their extensive expertise in genomics and personalized medicine. However, the market also features niche players specializing in direct-to-consumer testing and rare disease diagnostics is creating a fragmented yet dynamic ecosystem.

Technological innovation is a key battleground, with companies investing heavily in NGS platforms, AI-driven analytics, and blockchain to differentiate themselves. According to McKinsey, over 60% of European enterprises prioritize secure and scalable genetic testing solutions by intensifying competition among providers to offer cutting-edge technologies. Additionally, stringent EU regulations mandating data privacy have forced companies to innovate responsibly.

Mergers and acquisitions are another hallmark of the competitive landscape. Larger firms acquire smaller innovators to expand their product portfolios and geographic reach. Meanwhile, price wars and aggressive marketing strategies are common, particularly in saturated markets like Germany and the UK. Despite these challenges, the market remains ripe for growth, with opportunities in emerging segments such as pharmacogenomics and DTC testing driving future competition

Top Players in the Europe Genetic Testing Market

Thermo Fisher Scientific

Thermo Fisher Scientific is a global leader in the genetic testing market, playing a pivotal role in shaping the Europe segment. The company offers a comprehensive portfolio of NGS platforms, reagents, and diagnostic tools tailored to diverse applications. Its focus on innovation and scalability has positioned it as a trusted partner for hospitals and research institutions. Thermo Fisher ensures widespread adoption while maintaining compliance with stringent EU regulations by leveraging partnerships with governments and academic institution.

Illumina Inc.

Illumina Inc. specializes in advanced genomic technologies, emphasizing precision and affordability. The company’s NGS platforms are widely adopted in oncology and prenatal testing, enabling accurate analysis of genetic mutations. Illumina’s commitment to sustainability aligns with EU Green Deal objectives, earning it a loyal customer base. Collaborations with tech startups have expanded functionality, reinforcing its leadership in genomic research.

Myriad Genetics

Myriad Genetics is renowned for its cutting-edge diagnostic tests, particularly in cancer predisposition and hereditary disorders. The company’s focus on cost-effectiveness and ease of use has made it a leader in hospital and clinical applications. Its contributions to Europe’s healthcare infrastructure have propelled its position as a cornerstone of modern diagnostics.

Top Strategies Used by Key Market Participants

1. Emphasis on Innovation

Leading players in the Europe genetic testing market have embraced innovation as a core strategy to enhance their competitive edge. For instance, the development of AI-driven diagnostic tools and cloud-based data platforms has resonated with healthcare providers seeking scalable solutions. These initiatives not only align with EU regulations but also foster brand loyalty among stakeholders prioritizing cutting-edge technologies.

2. Investment in R&D

Investments in research and development are a cornerstone strategy for staying ahead in the market. Companies focus on developing advanced genetic testing platforms with higher accuracy and lower costs to address evolving customer needs. This approach allows them to tackle challenges such as scalability while maintaining leadership in technological advancements.

3. Geographic Expansion

Expanding into emerging markets within Europe, such as Eastern Europe and Scandinavia, has become a priority for key players. Companies can better serve regional demands while capitalizing on favorable regulatory frameworks. This strategy ensures sustained growth amid intensifying competition.

RECENT MARKET DEVELOPMENTS

- In March 2024, Thermo Fisher Scientific partnered with the German government to develop an AI-driven genomic platform for cancer diagnostics. This initiative aims to reduce late-stage diagnoses while improving treatment outcomes.

- In June 2023, Illumina Inc. launched its next-generation sequencing system in France, designed to achieve 99.9% accuracy in genetic mutation analysis. This move underscores the company’s commitment to technological innovation.

- In September 2023, Myriad Genetics acquired a UK-based startup specializing in rare disease diagnostics, expanding its portfolio of advanced testing solutions. This acquisition strengthens Myriad’s leadership in precision medicine applications.

- In January 2024, Siemens introduced a cloud-based data platform for genetic testing in Switzerland, targeting pharmaceutical companies. This launch positions Siemens as a leader in genomic data management.

- In November 2023, Roche unveiled its direct-to-consumer genetic testing kit in Italy, catering to younger demographics. This initiative enhances accessibility while addressing space constraints in urban areas.

MARKET SEGMENTATION

The research report on the European genetic testing market is segmented and sub-segmented into the following categories.

By Application

- Cancer Testing

- Pharmacogenomics Testing

- Prenatal Testing

- Predisposition Testing

By Test

- Carrier Testing

- Diagnostic Testing

- Prenatal Testing

- Neonatal Testing

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

How has the demand for genetic testing changed in Europe in recent years?

Due to the factors such as advancements in technology, increasing public awareness, and the growing emphasis on personalized medicine, the demand for genetic testing in Europe has grown significantly.

What are the challenges facing the genetic testing market in Europe?

Factors such as limited access to testing in some areas, high costs, and limited reimbursement for testing are some of the major challenges to the European genetic testing market.

What are the trends in the European genetic testing market?

The growing demand for non-invasive prenatal testing, the increasing use of genetic testing in personalized medicine, and the growing interest in pharmacogenetic testing are some of the current trends in the European genetic testing market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com