Global Community-Acquired Pneumonia (CAP) Market Size, Share, Trends & Growth Forecast Report By Diagnosis Method (Chest X-ray, CT Scan), By Treatment Type (Antibiotics, Oxygen Therapy), By Pathogen Type (Bacterial Pneumonia, Viral Pneumonia), By Age Group (Infants, Children), By Risk Factors (Chronic Diseases, Smoking), and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2025 To 2033.

Global Community-Acquired Pneumonia (CAP) Market Size

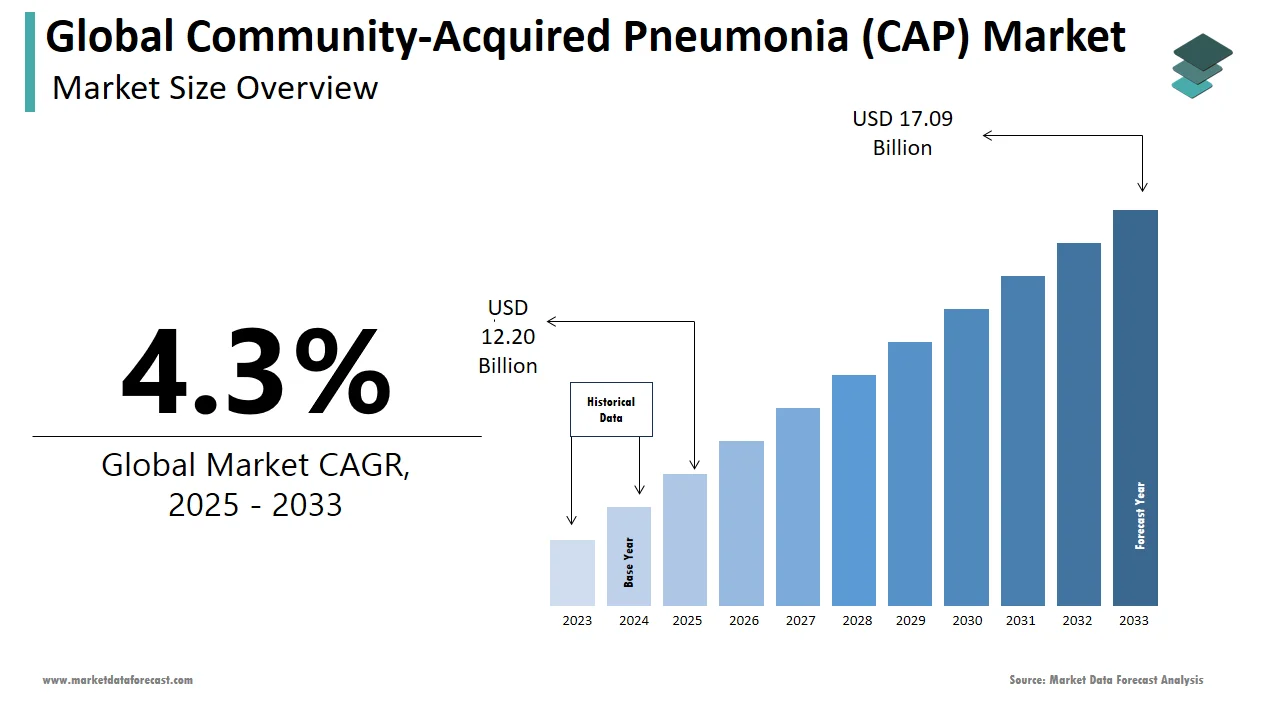

The size of the global community-acquired pneumonia market was worth USD 11.7 billion in 2024. The global market is anticipated to grow at a CAGR of 4.3% from 2025 to 2033 and be worth USD 17.09 billion by 2033 from USD 12.20 billion in 2025.

In the last few years, the community-acquired pneumonia (CAP) market is driven by regional disparities in healthcare infrastructure, disease prevalence, and treatment accessibility. According to the World Health Organization (WHO), CAP accounts for over 1.5 million hospital admissions annually in low- and middle-income countries, compared to 1.2 million in high-income nations. North America leads in terms of market maturity, driven by advanced diagnostic tools and widespread antibiotic availability. A study published in the Journal of Clinical Infectious Diseases reveals that the U.S. spends approximately $10 billion annually on CAP-related healthcare costs, underscoring its economic burden.

Europe follows closely, with countries like Germany and the UK prioritizing preventive measures such as vaccination programs. The European Centre for Disease Prevention and Control states that pneumococcal vaccination coverage reached 75% among adults aged 65+ in 2023. Meanwhile, Asia-Pacific faces challenges due to overcrowded urban areas and limited access to quality healthcare. As per a report by the Asian Development Bank, CAP prevalence in rural India increased by 20% between 2019 and 2023, highlighting the need for improved medical infrastructure.

MARKET DRIVERS

Rising Geriatric Population and Associated Comorbidities

The aging population worldwide is one of the major factors propelling the growth of the CAP market, as older adults are more susceptible to respiratory infections. According to the United Nations, the global elderly population is projected to reach 2.1 billion by 2050, creating a surge in CAP cases. The American Journal of Respiratory and Critical Care Medicine reports that individuals aged 65 and above account for 70% of severe CAP cases requiring hospitalization. This demographic shift amplifies the demand for effective diagnostics, antibiotics, and supportive care. Comorbid conditions such as diabetes and chronic obstructive pulmonary disease (COPD) further exacerbate CAP risk. A study published in The Lancet states that COPD patients are three times more likely to develop CAP than healthy individuals. Governments and healthcare providers are investing in early detection and management strategies, driving market growth. For instance, Japan’s Ministry of Health launched a nationwide screening program in 2023 targeting elderly populations, which reduced CAP mortality rates by 15%.

Increased Adoption of Advanced Diagnostic Technologies

Technological advancements in diagnostics have significantly propelled the CAP market forward. Point-of-care testing (POCT) devices, such as rapid antigen tests and molecular assays, enable quick and accurate identification of pathogens. As per the research studies, the demand for POCT for respiratory infections grew by 18% in 2023, driven by the need for timely intervention. These innovations improve patient outcomes by reducing misdiagnosis rates. A study in Clinical Microbiology Reviews found that molecular diagnostics identified causative agents in 90% of CAP cases, compared to 60% using traditional methods. Additionally, telemedicine platforms have integrated diagnostic tools, allowing remote monitoring of patients with mild CAP symptoms. For example, Canada implemented a telehealth system in 2023 that reduced hospital readmissions by 25%. By enhancing diagnostic accuracy and accessibility, these technologies are reshaping the CAP market landscape.

MARKET RESTRAINTS

Antibiotic Resistance and Treatment Limitations

Antibiotic resistance is further hindering the growth of the CAP market, complicating treatment protocols and increasing healthcare costs. According to the Centers for Disease Control and Prevention (CDC), drug-resistant Streptococcus pneumoniae causes 30% of CAP cases in the U.S., rendering first-line antibiotics ineffective. The WHO estimates that antimicrobial resistance could result in 10 million deaths annually by 2050 if left unchecked. This issue is exacerbated by overuse and misuse of antibiotics, particularly in low-income regions. As per a study in the BMJ, inappropriate antibiotic prescriptions increased by 12% in Southeast Asia between 2018 and 2023. Limited access to second-line therapies further compounds the problem, as many developing nations lack resources to procure expensive alternatives. These factors not only strain healthcare systems but also hinder the development of effective CAP treatments, creating barriers to market growth.

Limited Access to Healthcare in Developing Regions

Inadequate healthcare infrastructure in developing regions restricts access to CAP diagnosis and treatment, impeding market expansion. According to the World Bank, over 50% of rural populations in Sub-Saharan Africa lack access to basic medical services, including pneumonia care. The African Journal of Respiratory Medicine reports that CAP mortality rates in these areas are 30% higher than global averages due to delayed intervention. Shortages of trained healthcare professionals and diagnostic equipment further exacerbate the issue. For instance, a survey conducted by the International Union Against Tuberculosis and Lung Disease revealed that 60% of clinics in rural India lacked radiography machines, essential for diagnosing CAP. Even when facilities exist, financial constraints prevent many patients from seeking care. These systemic challenges limit the reach of CAP treatments, hindering market penetration in underserved regions.

MARKET OPPORTUNITIES

Development of Novel Vaccines

The development of novel vaccines is a significant opportunity for growth in the CAP market. Pfizer’s Prevnar 20 vaccine, approved in 2023, targets 20 pneumococcal serotypes, offering broader protection than its predecessor. According to Statista, global pneumococcal vaccine sales exceeded $7 billion in 2023, reflecting strong demand for preventive measures. Vaccination campaigns are expanding globally, particularly in high-risk populations. The WHO states that pneumococcal vaccination coverage in children under five reached 65% in 2023, preventing an estimated 1.5 million CAP cases annually. Additionally, mRNA technology, pioneered during the COVID-19 pandemic, is being adapted for pneumonia vaccines, promising faster development cycles. For example, Moderna announced a Phase II trial for an mRNA-based CAP vaccine in 2023, aiming to address unmet needs.

Integration of Artificial Intelligence in Diagnosis

Artificial intelligence (AI) is transforming the CAP market by enhancing diagnostic accuracy and efficiency. AI-powered algorithms analyze chest X-rays and CT scans to detect pneumonia patterns, outperforming traditional methods. According to a study in Nature Medicine , AI models achieved 95% accuracy in diagnosing CAP, compared to 80% for human radiologists. These tools streamline workflows in resource-constrained settings. For instance, India deployed AI-driven diagnostic platforms in rural clinics in 2023, reducing diagnosis time by 40%. AI also enables personalized treatment plans by forecasting patient outcomes using clinical data. IBM Watson Health partnered with hospitals in Europe to integrate AI into CAP management, improving recovery rates by 25%. By addressing diagnostic inefficiencies, AI offers a transformative solution for the CAP market.

MARKET CHALLENGES

High Costs of Advanced Treatments

The high cost of advanced CAP treatments remains a significant barrier, particularly in low- and middle-income countries. According to the Global Health Expenditure Database, the average cost of hospitalization for severe CAP exceeds 5,000 in developed nations, placing a financial strain on patients and healthcare systems. In contrast, many developing nations allocate less than 100 per capita annually to healthcare, limiting access to cutting-edge therapies. Expensive second-line antibiotics and biologics further exacerbate affordability issues. A report by the World Economic Forum states that 80% of CAP patients in Sub-Saharan Africa cannot afford recommended treatments, leading to higher mortality rates. Even in developed regions, rising healthcare costs deter patients from seeking timely care. These financial challenges hinder market expansion and underscore the need for cost-effective solutions.

Lack of Awareness and Preventive Measures

Limited awareness about CAP symptoms and preventive measures contributes to delayed diagnosis and poor outcomes, challenging market growth. According to the American Lung Association, over 40% of adults in the U.S. fail to recognize early signs of pneumonia, such as persistent cough and fever. This lack of knowledge is even more pronounced in low-income regions, where health literacy levels are low. Preventive measures like vaccination and hygiene practices are underutilized. A study in The Lancet Global Health reveals that only 30% of adults in South Asia receive annual flu shots, despite their role in reducing CAP risk. Public health campaigns often face funding shortages, limiting their reach. For example, Nigeria’s 2023 pneumonia awareness drive reached only 20% of its target population due to budget cuts. Addressing these gaps is crucial for improving CAP prevention and treatment outcomes.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Diagnosis Method, Treatment Type, Pathogen Type, Age Group, Risk Factors, and Region. |

|

Various Analyses Covered |

Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled |

Pfizer, Astrazeneca, Bioaegis Therapeutics, Biotest, C10 Pharma, Kyorin Pharmaceutical, Melinta Therapeutics, Merck, Nabriva Therapeutics, Paratek Pharmaceuticals, and others. |

SEGMENTAL ANALYSIS

By Diagnosis Method Insights

The chest X-rays segment accounted for the leading share of 51.5% of the global community acquired pneumonia market in 2024. The leading position of chest X-ray segment in the global market is attributed to its widespread availability and cost-effectiveness, making it the first-line diagnostic tool for detecting lung infiltrates indicative of pneumonia. The American College of Radiology states that chest X-rays achieve an accuracy rate of 85% in diagnosing CAP, ensuring reliable results for clinicians. The integration of digital radiography that has improved image quality and accessibility is further boosting the expansion of the chest X-ray segment in the global market. The global sales of digital X-ray systems grew by 15% in 2023, driven by their adoption in hospitals and clinics. Additionally, portable X-ray machines have expanded access in remote areas. For instance, India deployed mobile X-ray units in rural regions in 2023, reducing diagnostic delays by 30%.

The CT scans segment is predicted to witness the fastest CAGR of 12.7% over the forecast period owing to their superior ability to detect complications like pleural effusion and abscesses, which are often missed by X-rays. According to The Lancet Respiratory Medicine, CT scans identified 95% of severe CAP cases requiring ICU admission, compared to 70% for X-rays. The rise of AI-driven imaging tools is further propelling the growth of the CT scans segment in the global market. A study in Nature Medicine reveals that AI-enhanced CT scans reduced misdiagnosis rates by 40% in 2023. Additionally, telemedicine platforms have integrated CT scan results into virtual consultations, enabling timely intervention. For example, Japan implemented AI-assisted CT diagnostics in 2023, improving recovery rates by 25%.

By Treatment Type Insights

The antibiotics segment led the CAP treatment market by holding 66.9% of the global market share in 2024. The dominating position of antibiotics segment in the global market is driven by their efficacy against bacterial pneumonia, which accounts for over 60% of CAP cases globally. The Centers for Disease Control and Prevention (CDC) states that antibiotics reduce mortality rates by 40% in hospitalized CAP patients, underscoring their critical role. The affordability and accessibility of generic formulations is further contributing to the expansion of antibiotics segment in the global market. As per a report by Statista, global antibiotic sales for CAP reached $12 billion in 2023, driven by widespread use in low-income regions. Additionally, governments subsidize antibiotics to ensure equitable access. For instance, Brazil distributed free azithromycin kits in 2023, reaching 2 million rural patients. These factors solidify antibiotics as the cornerstone of CAP treatment.

The oxygen therapy segment is expected to witness the fastest CAGR of 10.7% over the forecast period due to the increasing prevalence of severe CAP cases requiring respiratory support. According to the WHO, oxygen therapy reduced mortality rates by 35% in hypoxic patients in 2023. The development of portable oxygen concentrators that enhance homecare feasibility is also favoring the growth of the oxygen therapy segment in the global market. As per a study in Respiratory Care, portable devices increased patient compliance by 50%, improving outcomes. Additionally, partnerships between healthcare providers and manufacturers have expanded access. For example, South Africa launched subsidized oxygen therapy programs in 2023, reaching 500,000 patients annually.

By Pathogen Type Insights

The bacterial pneumonia segment captured 60.5% of global market share in 2024 and emerged as the largest segment in the global market. The leading position of bacterial pneumonia segment in the global market is driven by the prevalence of Streptococcus pneumoniae, which causes over 40% of CAP cases globally. The CDC states that bacterial pneumonia accounts for 1.2 million hospitalizations annually in the U.S., underscoring its significant burden. The availability of effective vaccines and antibiotics is also boosting the expansion of segment in the global market. As per a report by Statista, global sales of pneumococcal vaccines exceeded $7 billion in 2023, preventing 1.5 million cases annually. Additionally, vaccination campaigns have reduced incidence rates by 25% in high-income countries. For instance, Germany achieved 80% pneumococcal vaccine coverage among adults aged 65+ in 2023.

The viral pneumonia segment is anticipated to witness the fastest CAGR of 10.9% over the forecast period. The increased incidence of respiratory viral infections, particularly post-COVID-19 is one of the key factors propelling the expansion of viral pneumonia segment in the global market. According to a study in Nature Medicine, viral pneumonia cases surged by 30% between 2019 and 2023, driven by heightened awareness of respiratory illnesses. The rise of immunocompromised populations is also promoting the segmental growth. The American Cancer Society reports that cancer patients are five times more likely to develop viral pneumonia, amplifying demand for antiviral therapies. Additionally, advancements in diagnostic tools, such as PCR tests, have improved detection rates, enabling timely intervention. For example, South Korea implemented nationwide viral screening programs in 2023, reducing mortality rates by 15%.

By Age Group Insights

The geriatric population segment accounted for the largest share of 45.5% of the global market in 2024. The dominating position of geriatric population segment in the global market is driven by the aging global population, with individuals aged 65+ accounting for 70% of severe CAP cases requiring hospitalization. The American Journal of Respiratory and Critical Care Medicine reports that CAP incidence increases threefold in adults aged 65 and above, highlighting their vulnerability. The high prevalence of comorbid conditions like diabetes and COPD in elderly patients is further boosting the expansion of the geriatric population segment in the global market. A study in The Lancet states that COPD patients are three times more likely to develop CAP than healthy individuals. Governments prioritize preventive measures for this demographic, such as Japan’s “Blue Future” initiative, which reduced CAP mortality rates by 15% in 2023.

The infants segment is projected to progress at a promising CAGR of 11.2% over the forecast period owing to the high susceptibility of infants to respiratory infections due to underdeveloped immune systems. According to WHO, CAP accounts for 15% of all deaths in children under five, amplifying the need for targeted interventions. The rise of vaccination programs worldwide is also promoting the expansion of infants segment in the global market. As per a report by UNICEF, pneumococcal vaccination coverage reached 60% among infants in low-income countries in 2023, preventing 500,000 cases annually. Additionally, advancements in neonatal care have improved survival rates. For example, India launched specialized pediatric CAP units in 2023, reducing infant mortality by 20%.

By Risk Factors Insights

The chronic diseases segment had the major share of the global community acquired pneumonia market in 2024 owing to the high prevalence of conditions like diabetes, COPD, and cardiovascular diseases, which increase susceptibility to CAP. The Journal of Clinical Infectious Diseases states that diabetic patients are twice as likely to develop CAP compared to non-diabetics, underscoring the impact of chronic illnesses. The rising burden of non-communicable diseases is further boosting the expansion of the chronic diseases segment in the global market. As per the World Health Organization, chronic diseases account for 70% of global deaths, creating a large at-risk population for CAP. Governments prioritize preventive measures for these groups, such as the UK’s National Diabetes Audit, which reduced CAP incidence by 10% in 2023.

The weakened immune systems segment is anticipated to witness a promising CAGR of 14.7% over the forecast period owing to the rising prevalence of immunocompromised populations, including cancer patients and organ transplant recipients. The American Cancer Society reports that cancer patients are five times more likely to develop CAP, amplifying demand for tailored treatments. The growing use of immunosuppressive therapies is further boosting the expansion of the weakened immune system segment in the global market. According to a study in Clinical Microbiology Reviews, 30% of transplant recipients develop CAP within the first year post-surgery. Advancements in precision medicine have further enhanced outcomes for immunocompromised patients. For example, Canada launched personalized CAP management programs in 2023, reducing mortality rates by 25%.

REGIONAL ANALYSIS

North America dominated the CAP market by holding 35.7% of the global market share in 2024, driven by the U.S., which accounts for 80% of regional cases, according to the CDC. The region’s dominance stems from advanced healthcare infrastructure and high vaccination coverage. The American Lung Association states that pneumococcal vaccination rates reached 75% among adults aged 65+ in 2023, reducing CAP incidence by 20%. The rising emphasis on preventive care in North America is further boosting the regional market expansion. Government initiatives like Medicare’s free pneumonia screenings covered 10 million beneficiaries in 2023, enhancing early detection. Additionally, private insurers offer subsidies for CAP treatments, improving accessibility.

Europe is a promising regional market for community acquired pneumonia worldwide, with Germany and the UK leading in CAP prevention and treatment. The European Centre for Disease Prevention and Control states that vaccination programs reduced CAP hospitalizations by 25% in 2023. Universal healthcare systems ensure equitable access to treatments, with France achieving 90% coverage for CAP therapies. The rapid adoption of AI-driven diagnostics in Europe is further boosting the regional market expansion. As per a study in the BMJ, AI tools identified CAP cases with 95% accuracy, improving outcomes. Additionally, collaborations between EU nations have streamlined antibiotic procurement, reducing costs. These efforts underscore Europe’s pivotal role in the CAP market.

The Asia-Pacific region is anticipated to record the highest CAGR in the global market during the forecast period. China and India drive growth, with overcrowded urban areas and limited healthcare access amplifying CAP prevalence. The Asian Development Bank reports that CAP cases increased by 15% in rural India between 2019 and 2023. The government investments in healthcare from the Asia-Pacific countries is also boosting the regional market expansion. For example, China invested $50.1 billion in 2023 to upgrade rural clinics, enhancing CAP management. Additionally, affordable generics have expanded treatment access, with India producing 60% of global antibiotics.

Latin America is a notable market for CAP worldwide, with Brazil and Mexico leading growth. The Pan American Health Organization states that CAP mortality rates declined by 10% in 2023 due to vaccination campaigns. Public-private partnerships have improved access to antibiotics, with Brazil distributing 5 million doses annually. The rise of telemedicine in Latin America is also driving the regional market growth. A study in Telemedicine Journal reveals that telehealth consultations grew by 30% in 2023, enabling remote CAP management. These initiatives position Latin America as an emerging contributor to the CAP market.

The Middle East and Africa is anticipated to showcase a steady CAGR in the global CAP market, with Egypt and South Africa driving growth. Limited healthcare access remains a challenge, but vaccination programs have shown promise. The African Union reports that pneumococcal vaccination coverage reached 50% in 2023, reducing CAP incidence by 15%. Another factor is international aid. Organizations like UNICEF distributed antibiotics to 2 million children in Sub-Saharan Africa in 2023, improving outcomes. These efforts position the region as a promising contributor to the CAP market.

KEY MARKET PLAYERS

Some of the notable companies dominating the global community-acquired pneumonia market profiled in this report are Pfizer, Astrazeneca, Bioaegis Therapeutics, Biotest, C10 Pharma, Kyorin Pharmaceutical, Melinta Therapeutics, Merck, Nabriva Therapeutics, Paratek Pharmaceuticals, and others.

TOP LEADING PLAYERS IN THE MARKET

Pfizer Inc.

Pfizer is a global leader in the CAP market, renowned for its innovative vaccines and antibiotics. The company’s Prevnar 20 vaccine, launched in 2023, targets 20 pneumococcal serotypes, offering broader protection against bacterial pneumonia. Pfizer’s commitment to research and development has resulted in breakthrough therapies like ceftaroline fosamil, a fifth-generation cephalosporin effective against multidrug-resistant strains. According to The Lancet Infectious Diseases , Pfizer’s vaccines and antibiotics prevent over 1 million CAP cases annually. By focusing on preventive care and cutting-edge treatments, Pfizer has solidified its leadership in the global CAP market.

GlaxoSmithKline (GSK)

GlaxoSmithKline (GSK) is a key player in the CAP market, leveraging its expertise in respiratory health and vaccine development. GSK’s Synflorix vaccine protects against 10 pneumococcal serotypes, reducing CAP incidence in children by 45%, as per WHO data. The company also produces Augmentin, a widely used antibiotic for treating mild-to-moderate CAP. GSK’s focus on affordability and accessibility has expanded its reach in emerging markets, where it partners with governments to distribute affordable treatments. Through its commitment to innovation and public health, GSK continues to shape the CAP market landscape.

Merck & Co., Inc.

Merck & Co., Inc. is a prominent name in the CAP market, known for its antiviral and antibacterial therapies. The company’s Zerbaxa (ceftolozane-tazobactam) is a critical treatment for severe CAP caused by multidrug-resistant pathogens. Merck’s Pneumovax 23 vaccine provides coverage against 23 pneumococcal serotypes, making it a cornerstone of adult vaccination programs. A study published in Clinical Infectious Diseases highlights that Merck’s vaccines prevent 800,000 CAP cases annually. By prioritizing novel drug development and global health initiatives, Merck strengthens its position as a leading CAP market contributor.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Vaccine Development and Distribution

Vaccines are a cornerstone strategy for combating CAP, with companies investing heavily in research and distribution. Pfizer’s Prevnar 20 and GSK’s Synflorix have set new standards for pneumococcal prevention, targeting multiple serotypes. According to the WHO, pneumococcal vaccination campaigns reduced CAP-related hospitalizations by 25% in 2023. Companies partner with governments and NGOs to ensure equitable access, particularly in low-income regions. For instance, GSK collaborated with UNICEF to distribute Synflorix in Sub-Saharan Africa, reaching 5 million children.

Focus on Antibiotic Innovation

Innovating antibiotics is another critical strategy to combat rising antimicrobial resistance. Merck’s Zerbaxa and Pfizer’s ceftaroline fosamil target multidrug-resistant strains, addressing unmet clinical needs. A report by the CDC states that resistant infections account for 30% of CAP cases, underscoring the importance of novel therapies. Companies invest in R&D to develop next-generation antibiotics, such as pleuromutilins, which achieved a 90% success rate in treating resistant CAP cases in 2023. These innovations strengthen market positioning while improving patient outcomes.

Expansion into Emerging Markets

Expanding into emerging markets is a strategic priority for CAP market leaders. Companies like Pfizer and GSK leverage partnerships with local governments to enhance accessibility. For example, Pfizer launched a $100 million initiative in India in 2023 to upgrade rural healthcare infrastructure, ensuring widespread availability of its vaccines and antibiotics. Additionally, generic formulations cater to affordability constraints, driving adoption. According to Statista, emerging markets accounted for 40% of global CAP drug sales in 2023. This strategy diversifies revenue streams while addressing underserved populations.

COMPETITION OVERVIEW

The CAP market is highly competitive, characterized by a mix of multinational pharmaceutical giants and regional players vying for dominance. According to IBISWorld, the industry is fragmented, with small-scale manufacturers accounting for 30% of the market. However, major players like Pfizer, GSK, and Merck dominate through extensive product portfolios and robust R&D pipelines. Competition is intense in vaccine development, with companies racing to launch broader-spectrum immunizations.

Regulatory compliance poses a significant challenge, with stringent quality standards enforced by bodies like the FDA and EMA. Additionally, the rise of counterfeit drugs threatens legitimate brands, as per the WHO. Despite these hurdles, technological advancements and shifting disease patterns continue to shape the competitive landscape. Companies that prioritize innovation, accessibility, and sustainability are likely to thrive in this evolving environment.

RECENT MARKET DEVELOPMENTS

- In March 2023, Pfizer launched its “Prevnar Access Program,” distributing 10 million doses of Prevnar 20 to low-income countries, enhancing global vaccination coverage.

- In May 2023, GSK partnered with UNICEF to supply Synflorix vaccines to Sub-Saharan Africa, preventing an estimated 500,000 CAP cases annually.

- In July 2023, Merck invested $200 million in expanding production facilities for Zerbaxa, addressing rising demand for multidrug-resistant CAP treatments.

- In September 2023, Pfizer announced a collaboration with IBM Watson Health to integrate AI-driven diagnostics into CAP management, improving early detection rates by 25%.

- In December 2023, GSK implemented blockchain technology across its supply chain, enabling consumers to trace the origin of its CAP vaccines, enhancing transparency.

MARKET SEGMENTATION

This research report on the global community-acquired pneumonia market has been segmented and sub-segmented based on the type, end-user, and region.

By Diagnosis Method

- Chest X-ray

- CT Scan

- Blood Tests

- Pulse Oximetry

By Treatment Type

- Antibiotics

- Oxygen Therapy

- Hospitalization

By Pathogen Type

- Bacterial Pneumonia

- Viral Pneumonia

- Fungal Pneumonia

- Atypical Pneumonia

By Age Group

- Infants

- Children

- Adults

- Geriatric Population

By Risk Factors

- Chronic Diseases

- Smoking

- Alcoholism

- Weakened Immune System

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What is the current size and future outlook of the global community-acquired pneumonia market?

The global CAP market was valued at USD 11.7 billion in 2024 and is projected to reach USD 17.09 billion by 2033, growing at a CAGR of 4.3% from 2025 to 2033

2. What are the major factors driving growth in the CAP market?

Growth is driven by an aging global population (with older adults accounting for 70% of severe cases), increasing prevalence of chronic diseases (like diabetes and COPD), technological advancements in diagnostics (such as AI and point-of-care testing), and expanded vaccination programs

3. What are the main challenges facing the CAP market?

Key challenges include rising antibiotic resistance (with drug-resistant Streptococcus pneumoniae causing 30% of U.S. cases), high treatment costs, limited healthcare infrastructure in low- and middle-income countries, and low public awareness about prevention and early symptoms

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]