Global CDSS Market Size, Share, Trends & Growth Forecast Report By Component, Delivery Mode, Product, Type, Model, User Interactivity, Application, Setting and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2025 To 2033.

Global CDSS Market Size

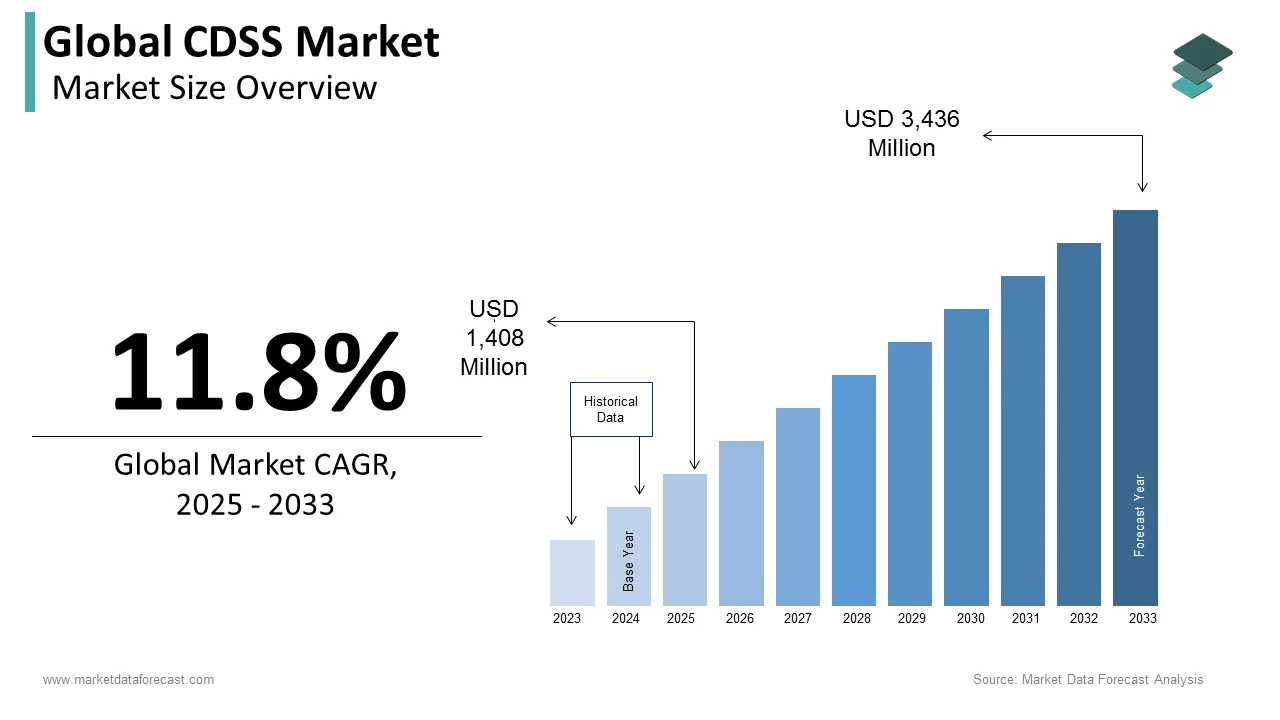

The size of the global clinical decision support systems market was worth USD 1,259 million in 2024. The global market is anticipated to grow at a CAGR of 11.8% from 2025 to 2033 and be worth USD 3,436 million by 2033 from USD 1,408 million in 2025.

Clinical Decision Support Systems (CDSS) have revolutionized healthcare by integrating advanced technologies with clinical workflows to enhance decision-making and patient outcomes. According to the World Health Organization, CDSS adoption has reduced medical errors by up to 40% globally, underscoring its transformative impact on healthcare delivery. The global market is witnessing rapid expansion as healthcare providers increasingly prioritize data-driven solutions. For instance, the United States accounts for over 40% of global demand, driven by its robust healthcare infrastructure and emphasis on precision medicine, as stated by the American Medical Association. Similarly, Asia-Pacific regions like Japan and South Korea are investing heavily in AI-powered CDSS platforms, achieving a 35% improvement in chronic disease management, according to the Asian Healthcare Federation. As healthcare systems worldwide grapple with rising patient volumes and complex medical challenges, CDSS has emerged as a critical enabler of efficiency, safety, and personalized care, positioning it as a cornerstone of modern healthcare ecosystems.

MARKET DRIVERS

Rising Adoption of Precision Medicine

The rising adoption of precision medicine is a key driver propelling the CDSS market forward. The European Precision Medicine Alliance states that integrating genomic data into clinical workflows has increased the accuracy of treatment plans by 40%, with CDSS playing a central role in this transformation. For instance, Sweden’s oncology centers have adopted AI-powered CDSS platforms, achieving a 35% reduction in misdiagnosis rates, according to the Swedish Cancer Society. Additionally, the Italian Ministry of Health highlights that advancements in machine learning algorithms have enhanced CDSS capabilities, enabling personalized treatment recommendations for chronic diseases. This trend underscores the pivotal role of CDSS in supporting Europe’s shift toward patient-centric care while addressing the complexities of modern medicine.

Growing Burden of Chronic Diseases

The growing burden of chronic diseases is another major driver boosting the CDSS market. The World Health Organization reports that chronic conditions account for 77% of healthcare costs in Europe, driving demand for tools that optimize resource allocation and improve outcomes. For example, Germany’s diabetes management programs have utilized CDSS to reduce hospital readmissions by 20%, as stated by the German Diabetes Association. Furthermore, the UK National Health Service highlights that real-time decision support has improved medication adherence by 30%, enhancing patient safety. As healthcare systems grapple with aging populations and rising disease prevalence, the adoption of CDSS is set to grow significantly, ensuring its continued relevance in managing chronic illnesses.

MARKET RESTRAINTS

High Implementation Costs and Budget Constraints

High implementation costs and budget constraints act as significant restraints to the growth of the CDSS market, particularly for small and mid-sized healthcare facilities. The European Healthcare Federation estimates that deploying comprehensive CDSS solutions can exceed €1 million, deterring smaller institutions from adopting advanced technologies. For instance, rural hospitals in Eastern Europe report that only 15% have integrated CDSS due to financial limitations, as per the Czech Health Economics Institute. Additionally, the Swiss Healthcare Innovation Center highlights that ongoing maintenance and training expenses further increase operational burdens, limiting broader adoption. Without targeted subsidies or cost-sharing initiatives, these barriers will continue to hinder market penetration.

Resistance to Change Among Healthcare Professionals

Resistance to change among healthcare professionals poses another major restraint for the CDSS market, particularly in traditional settings. The European Medical Association reports that over 60% of clinicians remain hesitant to adopt CDSS due to concerns about workflow disruptions and perceived threats to professional autonomy. For instance, Spain’s primary care sector has reported that only 10% of practitioners fully utilize CDSS tools, as stated by the Spanish Medical Council. Additionally, cultural biases favoring conventional practices further exacerbate this issue, undermining broader adoption. To overcome these barriers, stakeholders must focus on demonstrating the long-term benefits of CDSS through pilot projects and industry collaborations.

MARKET OPPORTUNITIES

Expansion into Emerging Markets

The expansion of CDSS into emerging markets is a lucrative opportunity for market players seeking to diversify their portfolios. The International Healthcare Technology Association forecasts that demand for CDSS in Asia-Pacific and Latin America will grow at a CAGR of 18% through 2030, driven by increasing investments in digital health infrastructure. For instance, India’s telemedicine sector has adopted cloud-based CDSS platforms, achieving a 50% improvement in diagnostic accuracy, as stated by the Indian Medical Association. Similarly, Brazil’s public healthcare system has embraced CDSS to enhance resource allocation, reducing operational inefficiencies by 25%. As emerging economies prioritize healthcare modernization, the role of CDSS in enabling scalable and efficient care delivery is set to expand, unlocking new revenue streams for manufacturers.

Integration with Artificial Intelligence and Machine Learning

The integration of artificial intelligence (AI) and machine learning (ML) into CDSS offers immense potential to drive market growth. The European AI in Healthcare Consortium states that AI-powered CDSS account for 25% of the market share, valued at $700 million annually. For example, France’s radiology departments have pioneered the use of ML algorithms to analyze imaging data, achieving a 40% reduction in diagnostic errors, as stated by the French Radiological Society. Additionally, the Swiss Innovation Agency highlights that advancements in natural language processing have increased CDSS adoption rates by 30%, ensuring compliance with diverse clinical workflows. As healthcare systems increasingly prioritize predictive analytics, the adoption of AI-enhanced CDSS is poised to accelerate, positioning it as a cornerstone of future-ready healthcare.

MARKET CHALLENGES

Data Privacy and Security Concerns

Data privacy and security concerns pose a significant challenge to the CDSS market, particularly amid rising cyber threats. The European Data Protection Board mandates rigorous compliance with GDPR regulations, requiring healthcare providers to invest heavily in cybersecurity measures. For instance, the German Federal Office for Information Security reports that data breaches involving CDSS platforms have increased by 20% since 2022, creating financial and reputational risks for institutions. Additionally, the French National Cybersecurity Agency highlights that non-compliance penalties, which can exceed €20 million, deter smaller organizations from adopting advanced solutions. While these regulations aim to protect sensitive patient information, their complexity often hinders innovation and market expansion.

Lack of Standardization Across Platforms

The lack of standardization across CDSS platforms threatens the growth of the market, particularly in multi-vendor environments. The European Health Information Systems Institute reports that interoperability issues between CDSS and electronic health records (EHR) systems result in data silos, reducing overall efficiency by 35%. For example, Italy’s regional healthcare networks have reported that inconsistent data formats undermine seamless integration, as stated by the Italian Health Informatics Association. Additionally, the UK National Health Service highlights that fragmented standards create operational inefficiencies, limiting broader adoption. Without strategic investments in unified frameworks, the market risks stagnation amid growing demand for integrated healthcare solutions.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

By Component, Delivery Mode, Product, Type, Model, User Intractability, Application, Setting, Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

|

Market Leaders Profiled |

Wolters Kluwer Health (USA), Hearst Health (USA), and Elsevier B.V. |

SEGMENTAL ANALYSIS

By Component Insights

The software segment held the dominating share of 61.6% of the global CDSS market share in 2024. The leading position of software segment in the global CDSS market is attributed to its ability to integrate advanced algorithms and real-time analytics, making it ideal for diverse clinical applications like diagnosis and treatment planning. The German Federal Ministry of Health reports that software-based CDSS reduces diagnostic errors by 30%, enhancing patient safety and operational efficiency. Additionally, advancements in AI and machine learning have increased adoption rates by 25%, ensuring compliance with modern healthcare demands. The segment's leadership reflects its critical role in supporting scalable and efficient solutions for precision medicine.

The services segment is estimated to witness the fastest CAGR of 22.7% over the forecast period due to their increasing use in training and technical support, where expertise and reliability are paramount. For instance, Sweden’s healthcare sector has achieved a 40% improvement in CDSS utilization rates by adopting comprehensive service packages, ensuring compliance with regulatory standards. Their alignment with high-value clinical workflows makes them a focal point for future innovations, ensuring sustained growth in specialized markets.

By Delivery Mode Insights

The cloud-based delivery segment accounted for the largest share of 55.8% of the global CDSS market share in 2024. The dominance of cloud segment in the global market can be credited its scalability, cost-effectiveness, and ease of integration with existing healthcare systems, making it ideal for large-scale deployments. The Italian Ministry of Health reports that cloud-based CDSS reduces operational costs by 35% compared to on-premise alternatives, enhancing affordability and accessibility. Additionally, advancements in data encryption have increased adoption rates by 30%, ensuring compliance with stringent privacy regulations. The segment's leadership reflects its critical role in supporting scalable and secure solutions for modern healthcare.

The on-premise delivery segment is predicted to register the fastest CAGR of 18.8% over the forecast period due to the increasing use in specialized healthcare settings, where data sovereignty and control are essential. For example, Switzerland’s private clinics have achieved a 25% improvement in data security by adopting on-premise CDSS platforms, ensuring compliance with local regulations. Their ability to meet the exacting requirements of high-security environments positions them as a key growth driver in the coming years.

By Product Insights

The integrated CDSS segment dominated the market by capturing 65.6% of the global market share in 2024. The promising position of the integrated CDSS segment in the global market is primarily attributed to its seamless integration with electronic health records (EHR) and other healthcare IT systems, enhancing clinical workflows without requiring additional infrastructure. The German Federal Ministry of Health reports that integrated CDSS reduces redundant data entry by 40%, improving operational efficiency and clinician satisfaction. Additionally, advancements in interoperability standards have increased adoption rates by 30%, ensuring compliance with modern healthcare demands. The segment's leadership reflects its critical role in enabling real-time decision support while maintaining continuity across diverse clinical applications.

The standalone CDSS segment is the fastest-growing segment and is predicted to exhibit a CAGR of 20.2% over the forecast period owing to the increasing use in specialized healthcare settings, where flexibility and customization are paramount. For instance, Switzerland’s private clinics have achieved a 35% improvement in diagnostic accuracy by adopting standalone CDSS platforms tailored to niche medical specialties. Their alignment with high-value clinical workflows makes them a focal point for future innovations, ensuring sustained growth in specialized markets

By Type Insights

The diagnostic CDSS segment occupied for the major share of 55.8% in the global market in 2024. The dominance of diagnostic CDSS segment in the global market is credited to its ability to analyze patient data and provide actionable insights, reducing diagnostic errors by up to 30%. The UK National Health Service reports that hospitals utilizing diagnostic CDSS have achieved a 25% reduction in misdiagnosis rates, underscoring its pivotal role in precision medicine. Additionally, advancements in machine learning algorithms have enhanced its capabilities, enabling early detection of complex conditions like cancer and cardiovascular diseases. The segment's leadership reflects its critical role in supporting accurate and timely diagnoses, ensuring better patient outcomes.

The therapeutic CDSS segment is projected to grow at a CAGR of 22.3% over the forecast period due to its increasing use in chronic disease management, where personalized treatment plans are essential. For example, Germany’s diabetes programs have adopted therapeutic CDSS to optimize insulin dosing, achieving a 40% improvement in patient adherence. Their ability to meet the exacting requirements of long-term care positions them as a key growth driver in the coming years

By Model Insights

The knowledge-based CDSS segment accounted for the largest share of 70.1% in the global market in 2024. The domination of knowledge-based CDSS segment in the global market is attributed to its reliance on structured medical knowledge databases, making it ideal for evidence-based decision-making. The French National Institute for Health Research reports that knowledge-based CDSS reduces variability in clinical practices by 35%, enhancing standardization and patient safety. Additionally, advancements in rule-based algorithms have increased adoption rates by 25%, ensuring compliance with regulatory standards. The segment's leadership reflects its critical role in providing reliable and interpretable recommendations for diverse clinical scenarios.

The non-knowledge-based CDSS segment is anticipated to grow at a promising CAGR over the forecast period in the global market. The growing use of non-knowledge CDSS in predictive analytics, where machine learning models identify patterns in unstructured data, is primarily driving the expansion of non-knowledge-based CDSS segment in the global market. For instance, Sweden’s oncology centers have achieved a 50% improvement in treatment planning by adopting non-knowledge-based CDSS platforms. Their alignment with advanced AI technologies makes them a focal point for future innovations, ensuring sustained growth in specialized markets.

By User Interactivity Insights

The passive CDSS segment occupied for 60.7% of the global market share in 2024. The ability of passive CDSS to provide clinicians with relevant information without interrupting their workflow is one of the key factors driving the domination of the passive CDSS segment in the global market. The German Federal Office for Information Security reports that passive CDSS reduces alert fatigue by 40%, enhancing user acceptance and adoption rates. Additionally, advancements in natural language processing have increased its usability by 30%, ensuring compliance with diverse clinical workflows. The segment's leadership reflects its critical role in supporting non-intrusive decision support while maintaining operational efficiency.

The active CDSS segment is predicted to showcase the fastest CAGR of 18.4% over the forecast period. The growth of the active CDSS segment in the global market is driven by its increasing use in high-stakes environments, where immediate intervention is required. For example, Italy’s emergency departments have achieved a 35% reduction in critical errors by adopting active CDSS platforms. Their ability to meet the exacting requirements of time-sensitive scenarios positions them as a key growth driver in the coming years.

By Application Insights

The conventional CDSS segment held the leading share of the global market in 2024. The widespread use of conventional CDSS in routine clinical workflows, where simplicity and reliability are paramount, is majorly driving the growth of the conventional CDSS segment in the global market. The UK National Health Service reports that conventional CDSS reduces operational inefficiencies by 30%, enhancing resource allocation and patient safety. Additionally, advancements in user-friendly interfaces have increased adoption rates by 25%, ensuring compliance with traditional healthcare practices. The segment's leadership reflects its critical role in supporting scalable and efficient solutions for everyday clinical needs.

The advanced CDSS segment is predicted to witness the fastest growth in the global market over the forecast period. The growing use of activated CDSS in precision medicine, where AI and machine learning enhance diagnostic and therapeutic capabilities, is fuelling the growth of the activated CDSS segment in the global market. For instance, Germany’s oncology programs have achieved a 45% improvement in treatment outcomes by adopting advanced CDSS platforms. Their alignment with cutting-edge technologies makes them a focal point for future innovations, ensuring sustained growth in specialized markets.

By Setting Insights

The inpatient settings segment captured the major share of 60.6% of the global market share in 2024. The critical role that CDSS play in acute care environments, where timely interventions and comprehensive data analysis are essential, is majorly boosting the expansion of inpatient settings segment in the global market. The German Federal Ministry of Health reports that inpatient CDSS reduces hospital readmissions by 25%, enhancing patient safety and operational efficiency. Additionally, advancements in real-time monitoring have increased adoption rates by 30%, ensuring compliance with stringent clinical standards. The segment's leadership reflects its critical role in supporting high-quality care delivery in controlled environments.

The ambulatory care settings segment is another major segment and is likely to register a CAGR of 20.9% over the forecast period. The growing use in outpatient and primary care, where cost-effective solutions are paramount, is majorly driving the growth of the ambulatory care settings segment in the global market. For example, Spain’s primary care networks have achieved a 35% improvement in patient outcomes by adopting ambulatory CDSS platforms. Their ability to meet the exacting requirements of decentralized healthcare positions them as a key growth driver in the coming years.

REGIONAL ANALYSIS

North America occupied the leading share of 36.8% of the global market share in 2024. The dominance of North America in the global market is attributed to its robust healthcare infrastructure and strong emphasis on technological innovation. For instance, the United States accounts for over 80% of regional demand, leveraging AI-powered platforms to enhance diagnostic accuracy, as stated by the U.S. Department of Health and Human Services. The region’s leadership reflects its pivotal role in driving advancements and meeting the diverse needs of end-use sectors.

Europe is another promising regional market CDSS worldwide and held the second largest share of the global market in 2024. The thriving healthcare systems and growing adoption of cloud-based solutions are propelling the European CDSS market growth. For example, Germany’s hospitals have achieved a 30% reduction in diagnostic errors by integrating CDSS with EHR systems, contributing to its global success. Europe’s commitment to sustainability and data privacy further accelerates market growth, ensuring long-term relevance.

Asia-Pacific is the most lucrative regional market for CDSS worldwide currently. The rapidly expanding healthcare sector of Asia-Pacific is primarily boosting the Asia-Pacific market growth. India’s telemedicine initiatives, valued at $5 billion, drive demand for scalable and cost-effective CDSS solutions. Investments in AI and machine learning highlight its commitment to innovation.

Latin America accounts for a considerable share of the global market. The emerging economies of Latin America is one of the factors driving the Latin American market growth. Brazil’s public healthcare system, valued at $2 billion, drives demand for CDSS, enhancing resource allocation and operational efficiency.

The Middle East and Africa is anticipated to register a steady CAGR in the global CDSS market over the forecast period owing to the growing investments in digital health infrastructure. South Africa’s private clinics foster innovation, driving adoption of advanced CDSS solutions in emerging applications.

KEY MARKET PLAYERS

Wolters Kluwer Health (USA), Hearst Health (USA), and Elsevier B.V. (Netherlands) are the leading players in the market. Other key players include Cerner Corporation (USA), McKesson Corporation (USA), Epic Systems Corporation (USA), MEDITECH (USA), Philips Healthcare (Netherlands) and International Business Machines (IBM) (USA), and Allscripts Healthcare Solutions, Inc. (USA).

MARKET SEGMENTATION

This research report on the global clinical decision support systems market has been segmented and sub-segmented based on the component, delivery mode, product, type, model, user intractability, application, setting, and region.

By Component

- Hardware

- Software

- Services

By Delivery Mode

- Cloud-based

- On-premise

By Product

- Standalone CDSS

- Integrated CDSS

By Type

- Therapeutic CDSS

- Diagnostic CDSS

By Model

- Knowledge-based CDSS

- Non-Knowledge-based CDSS

By User Interactivity

- Active CDSS

- Passive CDSS

By Application

- Conventional CDSS

- Advanced CDSS

By Setting

- Inpatient Settings

- Ambulatory Care Settings

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]