Global Autonomous Vehicle Market Size, Share, Trends & Growth Forecast Report, Segmented By Application (Civil, Robo Taxi, Ride Hail, Rideshare, Self-Driving Truck, Self-Driving Bus), Automation Level (Level 1, Level 2, Level 3, Level 4, Level 5), Component (Hardware, Software, Service) And By Region (North America, Europe, Asia-Pacific, Latin America, Middle East, and Africa) Industry Analysis Forecast 2025 to 2033

Global Autonomous Vehicle Market Size

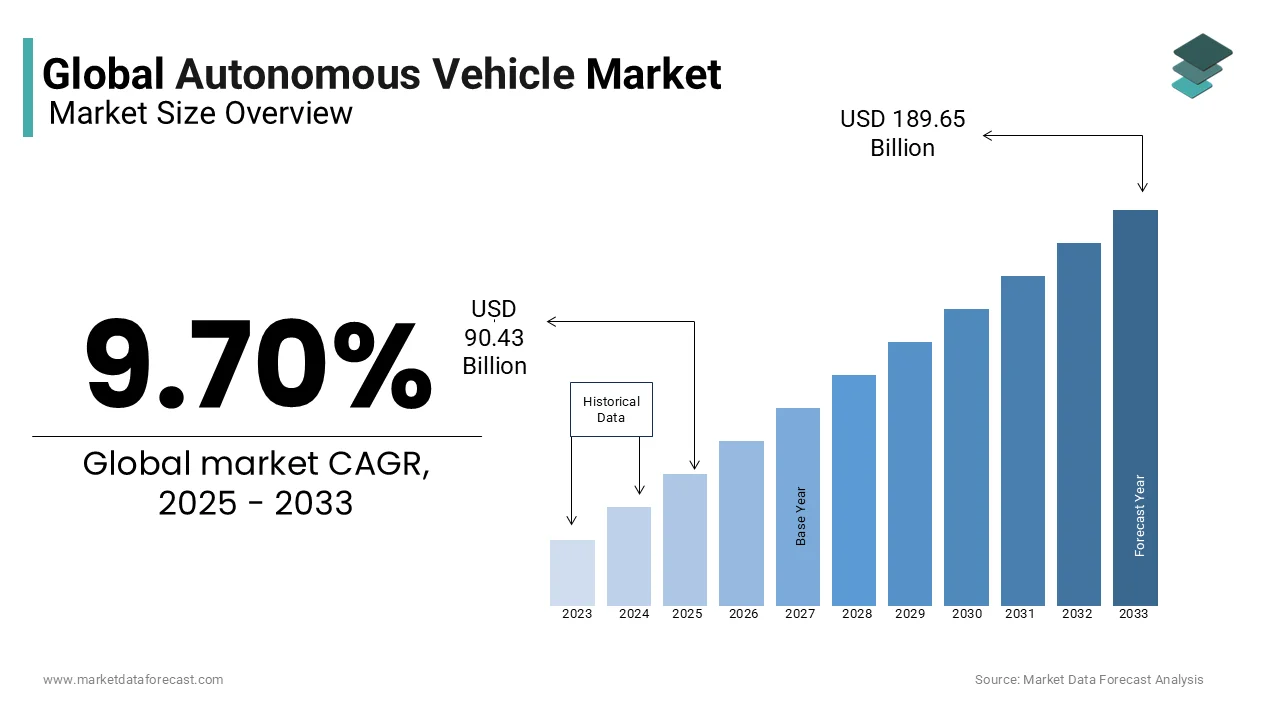

The global autonomous vehicle market was valued at USD 30.74 billion in 2024 and is anticipated to reach USD 34.74 billion in 2025 from USD 92.34 billion by 2033, growing at a CAGR of 13% during the forecast period 2025 to 2033.

The global automotive industry is experiencing a time of wide-ranging and transformative changes with the shift in customer behavior as well as the expanding usage of stringent environmental guidelines. Factors like increasing safety and security concerns, growing demand for dependable transportation framework, and approach of progressive trends, such as the transition from car ownership to "Mobility as a Service" (MaaS), are relied upon to build the interest for autonomous vehicles. These vehicles are the key to changing urban transportation to the point of being indistinguishable in the next few years. There are both conventional OEMs and new vehicle engineers who are working in this biological system to improve and introduce completely-autonomous vehicles on the road. These vehicles will have propelled features from conventional cars that will enhance the driving experience for travelers.

Autonomous vehicles, otherwise called self-driving vehicles, use artificial intelligence (AI) programming, light detection & ranging (LiDAR), and RADAR sensing innovation, which is additionally used to screen a 60-meter range around the vehicle and to shape a functioning 3D guide of the immediate environment. The vehicle is intended to travel between destinations without a human administrator. They consolidate sensors and software to control, explore, and drive the vehicle. Most self-driving frameworks make and maintain an internal map of their environment based on a wide array of sensors, similar to radar.

MARKET DRIVERS

Through the Internet of Things, vehicle drivers improve their performance by accepting the ongoing input from rapid in-memory computing frameworks built into associated cars. These built-in computers offer highlights such as gathering, examining, and storing data, which helps make decisions. The wide selection of related cars is relied upon to create rewarding opportunities for autonomous and semi-autonomous vehicles.

The rapid development of economies guarantees vigorous improvement from transport infrastructure to the advancement of smart cities. Numerous countries, for example, Mexico, Canada, and the US, are conveying digital foundations to encourage connectivity among vehicles and infrastructures to accumulate essential data, thereby decreasing traffic congestion and incrementing road security. Ascend in the advancement of smart cities is likely to drive this market substantially.

MARKET RESTRAINTS

Due to steady innovative advancements, the software in these vehicles needs to be often upgraded to keep them compatible with the outside environment. Likewise, the expense of all components and the sensor assembly in autonomous cars is more than riding in vehicles. In addition, the proportion of premium buyers to that of economic purchasers is very less universally, as it is hard for ordinary people to manage the cost of high-end cars. Therefore, a high introductory price combined with maintenance costs hampers the reception of autonomous vehicles.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

13% |

|

Segments Covered |

By Level of Automation, Component, Application, and Region. |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled |

Uber Technologies Inc., Daimler AG, Google Inc., Toyota Motor Corp, Nissan Motor Co. Ltd, Volvo Cars, General Motors Company, Volkswagen AG, Tesla Inc., BMW, and Others. |

SEGMENTAL ANALYSIS

By Level of Automation Insights

Features such as versatile cruise control or pathkeeping are part of level 1 of automation. In level 2, the vehicle framework can control the braking, steering, or acceleration of the vehicle. These highlights can be applied together, and the coordination between at least two of these help technologies encourages a vehicle to be of Level 2 status.

In level 3, the vehicle framework is able to recognize the environment around utilizing sensors such as LiDARs and settle informed decisions such as surpassing a slower-moving vehicle before it. The vehicle framework can oversee most parts of driving, including checking the environment. The system prompts the driver to mediate when it experiences a situation it can't navigate. In level 4, the vehicle can function without human interruption; however, just in specific conditions. There is an alternative to overriding the vehicle framework functions manually. At this level, the vehicles can work as driverless vehicles in any street condition. These vehicles are being created to be utilized as Robo-taxis, such as Waymo, among others.

By Component Insights

Vehicle-sharing services such as car or taxi sharing are foreseen to reach an ideal adoption rate, as individuals are relied upon to utilize these services more regularly because of affordability and comfort. This aspect is anticipated to increase interest in autonomous vehicles during the projected time.

By Application Insights

Some of the advantages of automation in this field include saving in the cost of work and decrease of carbon dioxide emission on the earth through advanced driving. These variables are relied upon to increase the interest in autonomous vehicles during the estimated period.

REGIONAL ANALYSIS

Western Europe establishes the predominant portion of the global autonomous vehicles market because of the high adoption rate of such vehicles in the locale. North America is the second leading market for autonomous vehicles, following Western Europe. North America and Europe secured the greater part of the global market in 2018 and are prone to continue to expand their market share during the predicted time, attributable to the expanding launch of semi-autonomous car models and developing improvement towards semi-autonomous vehicle systems among players in the automotive industry.

China, India, and Japan are the significant manufacturing nations of autonomous vehicles in the Asia Pacific, which is estimated to surpass Europe and North America regarding interest in autonomous vehicles. Reception of autonomous vehicles in developing regions such as Latin America and the Middle East & Africa is evaluated to be lower than that in the different areas. However, the market for autonomous vehicles is growing in developing nations.

KEY MARKET PLAYERS

Uber Technologies Inc., Daimler AG, Google Inc., Toyota Motor Corp, Nissan Motor Co. Ltd, Volvo Cars, General Motors Company, Volkswagen AG, Tesla Inc., BMW. These are the market players that dominate the global autonomous vehicles market.

Volvo and Chinese internet service provider Baidu have joined hands to create and mass-produce self-driving electric cars in China. Volvo will offer its aptitude for advanced innovations in the auto industry, whereas Baidu gives its autonomous driving platform, Apollo

RECENT HAPPENINGS IN THIS MARKET

- A self-driving car service being tried by Waymo opened up to more individuals in the Phoenix, Arizona area in late 2018.

- Waymo anticipated that organizations should be keen on utilizing the autonomous ride service to carry clients to and from shops.

- Self-driving vehicle innovation is probably to be utilized in long-stretch trucking since distant parts of routes can be monotonous highway stretches with fewer factors to deal with than on local streets.

- In late 2019 Hyundai became the newest car producer to convey autonomous rides in the US market.

- Las Vegas: Not long from now, you could ride one, two, or three wheels or maybe none at all. Some innovators played with long-established ideas like the bicycle or scooter by including artificial intelligence, electric power, and other technologies.

- Adjustments of the bicycle, implanted with new tech for the associated generation, showed up at CES. French start-up Wello showed its open-sided, three-wheeled car-bike that depends on accelerating, electric force, and solar panels on the roof, as of now being used by French postal services.

- Forget driverless cars, SDE's innovative autonomous navigation system - Genesis – can transform any boat or ship into an unmanned vessel. From securing the coastline to clearing waste, the potential for this innovation is boundless.

MARKET SEGMENTATION

This research report on the global autonomous vehicle market is segmented and sub-segmented into the following categories.

By Level of Automation

- Level 1

- Level 2

- Level 3

- Level 4

- Level 5

By Component

- Hardware

- Software

- Service

By Application

- Civil

- Robo taxi

- Ride hail

- Rideshare

- Self-driving truck

- Self-driving bus.

By Application

- Civil

- Robo taxi

- Ride hail

- Rideshare

- Self-driving truck

- Self-driving bus.

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What technologies are driving autonomous vehicles?

AI, LiDAR, radar, V2X communication, and deep learning enhance self-driving capabilities.

How do regulations impact autonomous vehicle adoption?

Safety laws, liability rules, and testing guidelines in the U.S., Europe, and Asia shape deployment.

What are the main challenges in commercializing autonomous vehicles?

Cybersecurity risks, high costs, real-world unpredictability, and infrastructure limitations.

Which industries benefit the most from self-driving technology?

Ride-hailing, logistics, public transport, agriculture, and defense sectors see major gains.

Who are the key players in the autonomous vehicle market?

Tesla, Waymo, Cruise, Baidu Apollo, Mobileye, and Aurora lead innovation these are the market players in the autonomous vehicle market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]