Asia Pacific Pigments Market Size, Share, Trends & Growth Forecast Report By Product Type (Inorganic Organic, Specialty Pigments, Other Product Types), Application, And Country (India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore And Rest of Asia-Pacific), Industry Analysis From 2025 To 2033

Asia Pacific Pigments Market Size

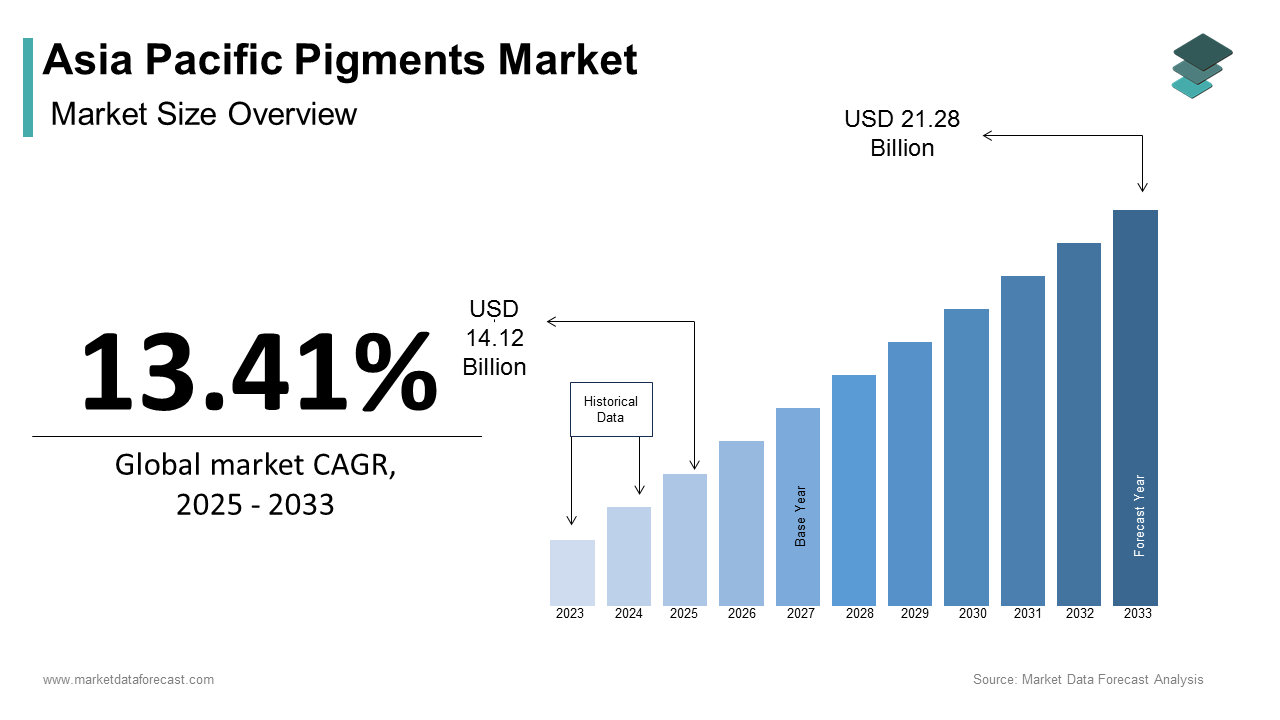

The Asia Pacific pigments market size was calculated to be USD 13.41 billion in 2024 and is anticipated to be worth USD 21.28 billion by 2033, from USD 14.12 billion in 2025, growing at a CAGR of 5.26% during the forecast period.

Pigments play a key role in diverse applications that range from food and beverages to cosmetics, textiles, and industrial coatings. Pigments are finely ground insoluble materials that impart color, opacity, and other functional properties to products, making them indispensable for enhancing aesthetics and performance. According to the Food and Agriculture Organization (FAO), the Asia Pacific region accounts for over 40% of global food production, underscoring the importance of pigments in food coloring and preservation. Similarly, as per the International Trade Centre, the region’s textile exports exceed $400 billion annually, with pigments being integral to dyeing and finishing processes. The advancements in pigment technology that enable the development of sustainable, non-toxic, and high-performance formulations tailored to meet regulatory and consumer demands is primarily driving the growth of the pigments market in Asia-Pacific. As per the United Nations Environment Programme (UNEP), the Asia Pacific region is also at the forefront of adopting eco-friendly manufacturing practices, with pigments increasingly being formulated to reduce environmental impact. With its vast industrial base, growing population, and rising disposable incomes, the Asia Pacific Pigments Market continues to expand, serving as a cornerstone for innovation and economic growth across multiple industries.

MARKET DRIVERS

Rising Demand in the Food and Beverage Industry

The increasing demand for visually appealing and safe food products has emerged as a primary driver for the Asia Pacific Pigments Market. According to the Food Safety and Standards Authority of India (FSSAI), the consumption of processed and packaged foods in the region has grown by over 25% in the past five years, creating significant demand for natural and synthetic pigments used in food coloring. For instance, carotenoids and anthocyanins are widely used to enhance the visual appeal of beverages, confectionery, and snacks, aligning with consumer preferences for vibrant and attractive products. A key factor driving this trend is the growing awareness of health and safety among consumers. As per the studies, over 60% of consumers in the Asia Pacific region prefer food products free from artificial additives, prompting manufacturers to adopt natural pigments derived from fruits, vegetables, and algae. Additionally, stringent food safety regulations enforced by agencies like the China Food and Drug Administration (CFDA) have accelerated the adoption of certified pigments, ensuring compliance with international standards. These factors not only cater to economic considerations but also align with shifting dietary trends, thereby fueling the expansion of the pigments market.

Expansion of the Textile and Apparel Sector

The rapid expansion of the textile and apparel sector in the Asia Pacific region has significantly bolstered the demand for pigments used in fabric dyeing and printing. Asia-Pacific accounts for over 60% of global textile production, with countries like China, India, and Bangladesh leading the way. Synthetic organic pigments, such as azo and phthalocyanine compounds, are extensively used to achieve vibrant colors and long-lasting finishes in fabrics. The growing adoption of digital textile printing technologies that rely heavily on high-performance pigments is also complementing the trend. The demand for digital printing services is projected to grow significantly over the next decade, which is creating immense opportunities for pigment manufacturers. Moreover, as per the United Nations Industrial Development Organization (UNIDO), the shift toward sustainable fashion has amplified the demand for eco-friendly pigments that minimize water usage and reduce chemical waste. These innovations position pigments as a transformative solution for modern textile manufacturing, ensuring both aesthetic appeal and environmental responsibility.

MARKET RESTRAINTS

Stringent Regulatory Frameworks

One of the most significant restraints affecting the Asia Pacific Pigments Market is the stringent regulatory frameworks governing the use of synthetic pigments, particularly in food, cosmetics, and pharmaceuticals. The European Food Safety Authority (EFSA) and the U.S. Food and Drug Administration (FDA) impose strict guidelines on permissible levels of heavy metals and toxic compounds in pigments, which are often mirrored by regional authorities. However, as per the Biotechnology Innovation Organization, the average time required to secure regulatory approval for new pigment formulations can exceed three years, accompanied by substantial R&D expenditures. This prolonged timeline poses significant challenges for manufacturers aiming to introduce innovative solutions tailored to emerging industry needs. Moreover, discrepancies between national and international regulations often lead to fragmented compliance requirements, complicating distribution efforts. For example, Australia’s Therapeutic Goods Administration (TGA) imposes additional restrictions on pigments used in cosmetics, creating hurdles for companies operating across multiple markets. Such inconsistencies deter investment in research and development, stifling innovation and delaying the availability of next-generation products capable of addressing pressing issues like toxicity and sustainability.

Volatility in Raw Material Prices

The volatility in raw material prices, which impacts production costs and profitability is further hampering the growth of the pigments market in Asia-Pacific. For instance, fluctuations in key inputs like titanium dioxide, chromium oxide, and synthetic intermediates have surged by 30% in recent years due to supply chain disruptions and geopolitical tensions. This instability creates challenges for pigment manufacturers, who must navigate rising input costs while maintaining competitive pricing for their products. Such price volatility disproportionately affects small-scale producers who operate on tight margins and lack the resources to absorb sudden cost increases. Larger enterprises, though more resilient, also face pressure to balance input expenses against market dynamics. Additionally, the complexity of reformulating pigments to accommodate changing ingredient availability often requires additional R&D investments, further inflating operational costs. These combined factors limit accessibility to high-quality pigments, impeding their overall market penetration across diverse industrial sectors.

MARKET OPPORTUNITIES

Adoption of Sustainable and Bio-Based Pigments

A burgeoning opportunity lies in the adoption of sustainable and bio-based pigments, driven by growing consumer demand for environmentally friendly products. As per the United Nations Environment Programme (UNEP), the Asia Pacific region is projected to account for over 50% of global green product consumption by 2030, creating significant demand for pigments derived from renewable sources like plant extracts, algae, and microbial fermentation. These bio-based alternatives not only reduce reliance on petrochemicals but also align with regulatory frameworks aimed at promoting circular economies. Simultaneously, the rise of regenerative agriculture presents a novel avenue for innovation. According to the Rodale Institute, regenerative practices could sequester up to 1.5 gigatons of carbon dioxide annually, with bio-based pigments serving as a cornerstone of these systems. For instance, pigments derived from spirulina algae are effective in reducing water pollution and energy consumption during production, as reported by the University of Queensland. By diversifying into these emerging sectors, pigment manufacturers can tap into rapidly expanding markets driven by sustainability goals and shifting consumer preferences, positioning themselves at the forefront of future-oriented industrial practices.

Growth in Digital Printing Technologies

The advent of digital printing technologies is another promising opportunity for the Asia Pacific Pigments Market. The demand for digital textile printing is on the rise and is likely to create immense demand for high-performance pigments compatible with inkjet systems. These pigments are designed to deliver vibrant colors, precise detailing, and long-lasting durability, ensuring maximum aesthetic appeal. For example, advancements in nano-pigment formulations enable manufacturers to achieve superior colorfastness and UV resistance, directly impacting product quality. Additionally, as per the United Nations Industrial Development Organization (UNIDO), adopting sustainable fashion practices has amplified the demand for eco-friendly pigments that minimize water usage and reduce chemical waste. These benefits not only cater to economic considerations but also align with consumer preferences for responsibly produced goods, thereby fueling the expansion of the pigments market.

MARKET CHALLENGES

Resistance to the Adoption of New Technologies

The resistance to the adoption of new technologies exhibited by traditional manufacturers entrenched in conventional practices is one of the significant challenges to the Asia-Pacific pigments market. As per surveys conducted by the Federation of Indian Chambers of Commerce and Industry (FICCI), nearly 40% of small-scale pigment producers remain hesitant to adopt advanced formulations or bio-based alternatives due to skepticism about their effectiveness or unfamiliarity with implementation processes. This reluctance is particularly pronounced among older generations who prioritize tried-and-tested methods over experimental approaches. Furthermore, cultural and regional disparities exacerbate this issue. For example, rural areas in Southeast Asia tend to have lower adoption rates compared to technologically progressive regions like Japan and South Korea, where large-scale operations dominate. Addressing these gaps necessitates tailored communication strategies that resonate with local contexts and priorities. Without overcoming this barrier, the full potential of advanced pigments cannot be realized, limiting their contribution to enhanced productivity and sustainability across the industrial value chain.

Concerns Over Environmental Impact and Regulation

Environmental concerns are further challenging the expansion of the pigments market in Asia Pacific, especially regarding pollution and resource depletion. As per findings from the World Resources Institute, over 70% of water pollution in the region is attributed to industrial activities, including pigment manufacturing, prompting stricter regulations on chemical discharges. Synthetic pigments, despite their efficiency, are often scrutinized for their potential contribution to these issues if not managed responsibly. Such sentiments place immense pressure on manufacturers to develop low-impact alternatives while adhering to complex regulatory frameworks. For example, China’s Ministry of Ecology and Environment imposes strict limits on wastewater and air emissions, creating additional hurdles for companies operating nationwide. Additionally, misinformation spread via social media platforms amplifies public distrust, creating reputational risks for brands associated with controversial pigment practices. To navigate these challenges effectively, industry players must invest in transparent marketing campaigns and engage directly with stakeholders to build trust and dispel misconceptions surrounding pigment safety and functionality.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

5.26% |

|

Segments Covered |

By Product Type, Application, And Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest Of Asia-Pacific |

|

Market Leaders Profiled |

BASF SE, Clariant AG, DIC Corporation, Huntsman Corporation, LANXESS AG, Sudarshan Chemical Industries Limited, KRONOS Worldwide Inc., Cabot Corporation, Ferro Corporation, Heubach GmbH, Tronox Holdings plc, Tokan Material Technology Co. Ltd. |

SEGMENTAL ANALYSIS

By Product Type Insights

The inorganic pigments segment dominated the Asia Pacific pigments market by holding 53.9% of the regional market share in 2024. The dominating position of inorganic pigments segment in the Asia-Pacific market is driven by their widespread use in industries like paints and coatings, plastics, and construction, where durability and cost-effectiveness are critical. According to the World Bank, over 60% of industrial applications in the region rely on inorganic pigments such as titanium dioxide (TiO2) and iron oxide due to their superior opacity, UV resistance, and chemical stability. The affordability and scalability of inorganic pigments is further boosting the expansion of the inorganic pigments segment in the Asia-Pacific market. As per the Federation of Indian Chambers of Commerce and Industry (FICCI), inorganic pigments can reduce production costs by up to 30% compared to organic alternatives, making them an attractive choice for manufacturers operating on tight margins. Additionally, advancements in formulation technologies have enabled the development of eco-friendly inorganic pigments that align with stringent environmental regulations. For instance, nano-sized TiO2 formulations are widely adopted in paints and coatings to improve weather resistance while minimizing environmental impact.

On the other hand, the specialty pigments segment is growing promisingly and is likely to witness a CAGR of 9.12% over the forecast period owing to the rising demand for high-performance pigments in niche applications such as automotive coatings, cosmetics, and digital printing. For example, pearlescent and metallic pigments are extensively used to achieve unique visual effects in luxury vehicles and consumer electronics. The growing adoption of advanced manufacturing technologies is also contributing to the growth of the specialty pigments segment in the Asia-Pacific market. Additionally, as per the United Nations Environment Programme (UNEP), the shift toward sustainable practices has amplified the demand for bio-based specialty pigments derived from renewable sources. These benefits position specialty pigments as a transformative solution for modern industrial applications, ensuring long-term sustainability and innovation.

By Application Insights

The paints and coatings segment accounted for 36.3% of the Asia-Pacific market share in 2024. The growth of the paints and coatings segment in the Asia-Pacific market is attributed to the region's booming construction and infrastructure development sectors, which require durable and aesthetically pleasing finishes. The ability of pigments to enhance the performance and longevity of coatings is further propelling the growth of the paints and coatings segment in the regional market. As per the Federation of Indian Chambers of Commerce and Industry (FICCI), titanium dioxide (TiO2)-based pigments can improve UV resistance and opacity in paints by up to 40%, directly impacting product quality. Additionally, the growing emphasis on sustainable building practices has accelerated the adoption of eco-friendly pigments that minimize volatile organic compound (VOC) emissions.

The digital printing inks segment is projected to exhibit the fastest CAGR of 10.4% over the forecast period owing to the increasing adoption of digital printing technologies in textiles, packaging, and publishing. The ability of digital printing inks to deliver vibrant colors, precise detailing, and long-lasting durability is further boosting the expansion of the digital printing inks segment in the regional market. As per the United Nations Industrial Development Organization (UNIDO), adopting sustainable fashion practices has amplified the demand for eco-friendly pigments that minimize water usage and reduce chemical waste. Additionally, as per the Asian Development Bank, advancements in nano-pigment formulations enable manufacturers to achieve superior colorfastness and UV resistance, directly impacting product quality.

REGIONAL ANALYSIS

China held the major share of 36.1% of the Asia Pacific Pigments Market in 2024. The dominance of China in the Asia-Pacific can be credited to the country's vast industrial base, which supports large-scale production of pigments for diverse applications, including paints, textiles, and plastics. According to the World Bank, China accounts for over 40% of global chemical production, underscoring its critical role in the pigments industry. The presence of advanced manufacturing technologies in China is further aiding the domination of China in the Asia-Pacific market. The Federation of Indian Chambers of Commerce and Industry (FICCI) reports that over 70% of Chinese pigment manufacturers utilize automated systems, enabling seamless integration of innovative formulations. Additionally, stringent environmental regulations enforced by the Ministry of Ecology and Environment have accelerated the adoption of eco-friendly pigments, ensuring compliance with global standards. These factors, combined with the country's technological prowess, cement China’s position as the undisputed leader in the regional market.

India was the second leading player in the Asia Pacific pigments market in 2024 and is estimated to showcase a prominent CAGR over the forecast period. The strong emphasis of India on sustainable practices has positioned it as a hub for eco-friendly pigment solutions. According to the Indian Chemical Council, over 60% of pigment manufacturers in India have adopted green technologies to reduce carbon emissions and water pollution. The thriving textile and apparel industry of India is further boosting the pigments market expansion in India. The Ministry of Textiles reports that India produces over 40 billion meters of fabric annually, creating significant demand for synthetic and natural pigments. Additionally, government incentives for adopting renewable energy sources have spurred the use of bio-based pigments, further bolstering the market's growth. These initiatives highlight India's commitment to balancing economic development with ecological responsibility.

Japan is a notable player in the Asia-Pacific pigments market and is anticipated to account for a significant share of the regional market over the forecast period. The focus of Japan on innovation and precision manufacturing has created a fertile ground for high-performance pigments used in advanced applications like automotive coatings and electronics. According to the Japan External Trade Organization (JETRO), Japan's automotive industry exports exceed $150 billion annually, necessitating advanced pigments to meet global quality standards. The rising adoption of specialty pigments that are facilitated by investments in R&D is also propelling the Japanese market growth. The National Institute of Advanced Industrial Science and Technology reports that nano-pigments have gained traction due to their ability to enhance durability and aesthetic appeal. Additionally, efforts to modernize manufacturing processes through government-funded programs have encouraged small-scale producers to invest in premium pigment solutions, contributing to Japan's steady market expansion.

South Korea is expected to occupy a notable share of the Asia-Pacific market over the forecast period, encompassing smaller economies like Thailand and Vietnam. As per the Korea International Trade Association (KITA), the country is witnessing gradual adoption of pigments due to its growing focus on export-oriented industries. For instance, South Korea's cosmetics exports have surged by 12% annually, driven by investments in advanced pigment formulations. The influx of foreign expertise and technology is also contributing to the pigments market growth in South Korea. The Korea Institute of Industrial Technology reports that partnerships with international organizations have introduced cost-effective pigment solutions tailored to local conditions. These collaborations not only enhance productivity but also promote sustainable practices, laying the foundation for long-term market development.

Australia and New Zealand represent a niche yet emerging player in the Asia Pacific Pigments Market, contributing marginally to the overall share. As per the Australian Department of Industry, Science, Energy and Resources, the region's agricultural sector is undergoing transformation, with a focus on self-sufficiency and resilience against external shocks. Recent droughts have underscored the need for fortified pigments to mitigate production losses. The growing adoption of bio-based pigments that safeguard soil health during adverse weather conditions in these countries is promoting the market growth in Australia and New Zealand. The University of Queensland highlights that these products have increased crop yields by up to 10% in local farms. Additionally, government subsidies aimed at revitalizing rural economies have incentivized farmers to invest in advanced pigment solutions, fostering incremental growth in the market.

LEADING PLAYERS IN THE ASIA PACIFIC PIGMENTS MARKET

BASF SE

BASF SE is a global leader in the Asia Pacific Pigments Market, renowned for its innovative and sustainable pigment solutions tailored to meet the diverse needs of industries such as paints, coatings, textiles, and plastics. The company specializes in producing high-performance organic and inorganic pigments that deliver vibrant colors, durability, and eco-friendly attributes. BASF’s commitment to research and development has positioned it as a pioneer in creating bio-based and low-impact formulations that align with stringent environmental regulations. By fostering partnerships with manufacturers and leveraging advanced technologies, BASF continues to drive advancements in sustainable industrial practices, reinforcing its leadership in the regional market.

Clariant AG

Clariant AG plays a pivotal role in the Asia Pacific Pigments Market by offering specialized pigment solutions designed for niche applications like automotive coatings, cosmetics, and digital printing. The company focuses on developing eco-friendly and high-performance pigments that cater to evolving consumer preferences for sustainability and innovation. Clariant’s emphasis on green chemistry aligns with its efforts to reduce carbon emissions and promote circular economies, making its products a preferred choice for eco-conscious industries. By leveraging cutting-edge R&D capabilities, Clariant ensures its pigments deliver consistent quality and performance, solidifying its reputation as an industry innovator.

DIC Corporation

DIC Corporation is a prominent player in the Asia Pacific Pigments Market, specializing in the production of advanced synthetic pigments for paints, inks, and plastics. The company emphasizes sustainable sourcing practices and invests heavily in developing specialty pigments that enhance product aesthetics and functionality. DIC’s vertically integrated business model allows it to maintain control over the entire supply chain, ensuring traceability and compliance with international standards. By prioritizing customer-centric solutions and investing in next-generation pigment technologies, DIC continues to strengthen its position as a trusted partner for industrial manufacturers.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Strategic Acquisitions and Partnerships

Key players in the Asia Pacific Pigments Market have prioritized strategic acquisitions and partnerships to expand their product portfolios and strengthen their market presence. By acquiring smaller firms specializing in niche pigment formulations or forming alliances with research institutions, these companies gain access to cutting-edge technologies and innovative solutions. Such collaborations enable them to address unmet needs in the industrial sector while enhancing their competitive edge. This strategy also facilitates entry into underserved markets, allowing companies to capitalize on untapped opportunities and diversify their revenue streams.

Investment in Sustainable Solutions

Sustainability has emerged as a cornerstone of competitive strategy in the pigments market. Leading companies are investing heavily in the development of eco-friendly pigments that reduce environmental impact, improve resource efficiency, and align with regulatory standards. By focusing on reducing carbon footprints and promoting circular economies, these players position themselves as champions of sustainable industrial practices. Their commitment to environmental stewardship not only enhances brand loyalty but also ensures compliance with evolving global standards, reinforcing their leadership in the market.

Emphasis on Research and Development

R&D is a critical driver of innovation in the Asia Pacific Pigments Market. Key players are channeling significant resources into exploring novel formulations and advanced manufacturing processes that improve pigment performance and application versatility. By staying at the forefront of technological advancements, these companies can introduce groundbreaking solutions tailored to specific industrial needs. This focus on innovation enables them to differentiate their offerings, meet the demands of modern manufacturing practices, and maintain a strong foothold in an increasingly competitive landscape.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players in the Asia Pacific pigments market include BASF SE, Clariant AG, DIC Corporation, Huntsman Corporation, LANXESS AG, Sudarshan Chemical Industries Limited, KRONOS Worldwide Inc., Cabot Corporation, Ferro Corporation, Heubach GmbH, Tronox Holdings plc, Tokan Material Technology Co. Ltd.

The Asia Pacific Pigments Market is characterized by intense competition, driven by the presence of established multinational corporations and emerging niche players. Companies strive to differentiate themselves through innovation, sustainability, and customer-centric strategies, creating a dynamic and rapidly evolving landscape. Leaders like BASF SE, Clariant AG, and DIC Corporation dominate the market by leveraging their extensive R&D capabilities and global reach to deliver high-performance solutions. At the same time, smaller firms focus on specialized products that cater to specific industrial segments or address unique challenges such as toxicity and environmental impact. Regulatory pressures and shifting consumer preferences further intensify competition, compelling companies to adopt sustainable practices and transparent labeling. Collaborations, mergers, and acquisitions are common strategies used to consolidate market share and expand product portfolios. This competitive environment fosters continuous innovation, ensuring that the market remains responsive to the needs of both producers and consumers.

RECENT HAPPENINGS IN THE MARKET

- In April 2024, BASF SE launched a new line of bio-based pigments designed to enhance sustainability and reduce environmental impact. This move aims to address growing concerns about pollution in the Asia Pacific region.

- In June 2023, Clariant AG partnered with a leading textile manufacturer to develop eco-friendly pigments for digital printing. This collaboration underscores Clariant’s commitment to advancing sustainable fashion practices through innovation.

- In January 2023, DIC Corporation acquired a startup specializing in nano-pigment technology. This acquisition strengthens DIC’s ability to offer high-performance pigments for automotive and electronics applications.

- In September 2022, Lanxess AG introduced a range of UV-resistant pigments aimed at supporting the construction and infrastructure sectors. This initiative aligns with consumer preferences for durable and weather-resistant products.

- In November 2022, Huntsman Corporation expanded its production facilities in India to increase the supply of specialty pigments. This expansion supports the company’s goal of meeting rising demand in the Asia Pacific Pigments Market.

MARKET SEGMENTATION

This research report on the Asia Pacific pigments market has been segmented and sub-segmented based on product type, application and region.

By Product Type

- Inorganic

- Organic

- Specialty Pigments

- Other Product Types

By Application

- Paints and Coatings

- Textiles

- Printing Inks

- Plastics

- Leather

- Other Applications

By Region

- India

- China

- Japan

- South Korea

- Australia

- New Zealand

- Thailand

- Malaysia

- Vietnam

- Philippines

- Indonesia

- Singapore

- Rest of Asia-Pacific

Frequently Asked Questions

1. What is driving the growth of the pigments market in Asia Pacific?

The market growth is driven by rising demand from industries like paints and coatings, plastics, textiles, and printing inks, along with rapid urbanization and industrialization.

2. Which types of pigments are most popular in the Asia Pacific region?

Organic pigments, such as azo and phthalocyanine pigments, and inorganic pigments like titanium dioxide and iron oxide, are highly popular.

3. How are technological innovations influencing pigment production?

Advancements in nanotechnology and organic pigment formulations are enhancing pigment performance and opening new application areas.

4. Who are the major consumers of pigments in Asia Pacific?

Key consumers include the construction, automotive, packaging, and textile industries.

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]