Global AI in Healthcare Market Size, Share, Trends & Growth Forecast Report By Offering (Hardware, Software, and Services), Algorithm (Deep Learning, Querying Method, Natural Language Processing, and Context Aware Processing), Application (Robot-Assisted Surgery, Virtual Nursing Assistant, Administrative Workflow Assistance, Fraud Detection, Dosage Error Reduction, Clinical Trial Participant Identifier, Preliminary Diagnosis, and Others), End-User (Healthcare Provider, Pharmaceutical & Biotechnology, Patient, and Payer) & Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa), Industry Analysis From 2024 to 2033

Global AI in Healthcare Market Size

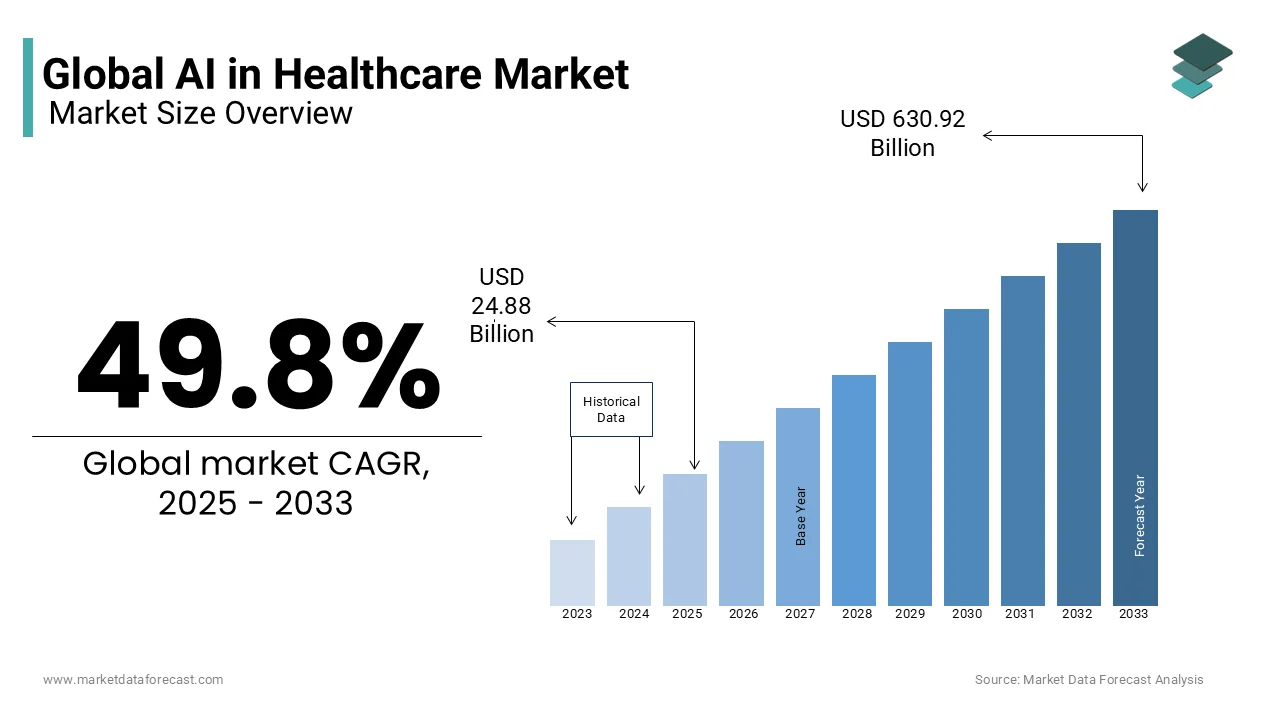

The global AI in the healthcare market size was valued at USD 16.61 billion in 2024 and is expected to register a whopping CAGR of 49.8% from 2025 to 2033. The global market size is anticipated to be valued at USD 630.92 billion by 2033, from USD 24.88 billion in 2025.

Artificial intelligence in healthcare is integrated with machine learning, natural language processing, and computer vision to augment clinical decision-making, automate administrative workflows, and personalize therapeutic interventions. As per the U.S. National Library of Medicine, over 87% of peer-reviewed clinical AI studies published in 2023 demonstrated statistically significant improvements in diagnostic accuracy when algorithms were integrated into radiology and pathology workflows.

MARKET DRIVERS

Surge in Healthcare Data Volume Fuels AI Adoption

The exponential growth in clinically structured and unstructured data, which exceeds human analytical capacity, is driving the growth of artificial intelligence in the healthcare market. The average hospital, particularly a large teaching facility, generates an immense amount of data, as much as 50 petabytes annually, but up to 97% of it remains unused and is effectively "dark data, as per the study. Machine learning models trained on this volume can detect micro-patterns invisible to clinicians, such as subvisual tumor margins in histopathology slides or prodromal arrhythmia signatures in continuous ECG streams.

Dressing Specialist Shortages Through AI Augmentation

The global deficit of clinical specialists in radiology, pathology, and neurology, which AI can partially offset through triage and augmentation, is also escalating the growth of artificial intelligence in healthcare. There has been a shortfall of a notable number of neurologists in low- and middle-income countries, with a gap that AI-enabled EEG interpretation tools are beginning to bridge. AI-powered systems, such as quantitative EEG (qEEG) analysis, are accelerating epilepsy diagnostics in India and globally by streamlining the review process for neurologists.

MARKET RESTRAINTS

Lack of Standardized Clinical Validation Slows AI Adoption

The absence of standardized validation frameworks for clinical AI is leading to fragmented trust and inconsistent regulatory pathways that hinder the rise of artificial intelligence in the healthcare market. The U.S. Food and Drug Administration cleared many AI-enabled medical devices, yet only a few of them underwent prospective and multi-center randomized trials, the gold standard for therapeutic interventions, according to the study. According to a study, in Europe, a portion of CE-marked diagnostic algorithms lacked external validation on demographically diverse cohorts, which risks performance decay in real-world deployment.

Algorithmic Bias in Training Data Limits AI Effectiveness

The algorithmic bias embedded in training data is hampering the growth of artificial intelligence in the healthcare market. Bias in AI diagnostic tools is primarily caused by training data that lacks representation of diverse ethnic groups, leading to decreased accuracy (AUC degradation) when applied to populations different from those in the training datasets. This data bias, rather than the market itself, contributes to poor performance and potential health inequities for underrepresented groups such as African and South Asian populations. According to a study, there has been a drop in melanoma detection sensitivity for darker skin tones due to underrepresentation in training images. AI risks automating inequity rather than resolving it until bias mitigation becomes non-negotiable in model development.

MARKET OPPORTUNITIES

Predictive Deterioration Modeling for Chronic Disease Management

Predictive deterioration modeling for chronic disease management, where AI can convert passive monitoring into preemptive intervention that offers potential opportunities for the artificial intelligence in the healthcare market growth. Continuous glucose monitors, implantable loop recorders, and home spirometers now generate terabytes of longitudinal physiologic data, which is ideal for recurrent neural networks to forecast exacerbations. As per the research, some deep learning models, like Long Short-Term Memory (LSTM), are robust and can be generalized across diverse populations and diabetes types for hypoglycemia prediction. Advanced AI models can improve predictive performance while keeping false alarm rates low, which is a major challenge for user adoption.

Automating Prior Authorization and Clinical Documentation

Automating prior authorization and clinical documentation is expected to give new opportunities for artificial intelligence in the healthcare market. Administrative burdens consume a percentage of U.S. healthcare expenditure, according to the research. Natural language processing engines can parse physician notes, cross-reference payer policies, and auto-generate justification letters with notable accuracy, as per a study. Similarly, ambient scribing tools like Nuance’s DAX Copilot reduced documentation time per patient by 51.7% by freeing 2.5 hours daily for direct care, a productivity gain equivalent to adding physicians to the U.S. workforce without new hires.

MARKET CHALLENGES

Black Box Nature of AI Models

The “black box” nature of deep learning models, which impedes clinician trust and regulatory traceability, is also impeding the growth of artificial intelligence in the healthcare market. Convolutional neural networks diagnosing pneumonia from chest X-rays may achieve notable accuracy, but cannot articulate which pixel clusters triggered the classification, a vital gap in high-stakes environments. The U.K. Medicines and Healthcare products Regulatory Agency’s audit of AI diagnostic tools found that only a few offered interpretable saliency maps or counterfactual explanations, which leaves clinicians unable to override or validate outputs. This opacity has legal consequences. Furthermore, in June 2025, the American Medical Association (AMA) adopted a new policy during its Annual Meeting to increase transparency and trust in AI tools used in healthcare by advocating for "explainable AI" and independent verification of safety and efficacy.

Interoperability Failures with Legacy IT Systems

The interoperability failure between AI systems and legacy hospital IT infrastructure, which fragments data flow and degrades model performance, is acting as a key barrier for the growth of artificial intelligence in the healthcare market. Despite HL7 FHIR adoption, a percentage of U.S. hospitals still operate EHRs incapable of streaming real-time vitals to AI inference engines by forcing manual data export and introducing latency errors. This technological dissonance renders even the most sophisticated algorithms inert at the point of care.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Offering, Algorithm, Application, End-User, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | India, China, Japan, South Korea, Australia, New Zealand, Thailand, Malaysia, Vietnam, Philippines, Indonesia, Singapore, Rest of APAC |

| Market Leaders Profiled | Welltok, Inc., Intel Corporation, Nvidia Corporation, Google Inc., IBM Corporation, Microsoft Corporation, General Vision, Inc., Enlitic, Inc., Next IT Corporation, iCarbonX, Siemens Healthineers, General Electric (GE) Company, Koninklijke Philips N.V., Cloudmedx, Inc., Bay Labs, Inc., and others. |

SEGMENTAL ANALYSIS

By Offering Insights

The software segment dominated the artificial intelligence in healthcare market by accounting for 61.8% share of the global market in 2024. The dominance of the software segment is primarily driven by the clinical and operational workflows where algorithms execute inference, prediction, and automation. These are functions that cannot be outsourced to hardware or consultants. Software’s growth is also due to its dual role as both the cognitive engine and the integration layer. It ingests multimodal data, applies deep learning or NLP models, and outputs actionable insights directly into EHRs, PACS, or robotic systems. According to a study, U.S. hospitals utilize both on-premise software and cloud-based services for AI-powered clinical decision support modules. Regulatory frameworks further support the software segment market growth. This institutional, technical, and regulatory alignment ensures software remains the nucleus of AI’s clinical value.

The services segment is predicted to witness a CAGR of 27.4% from 2025 to 2033. The swift expansion of the services segment is propelled by necessity, where there is an acute shortage of in-house data science talent and clinical informatics expertise within healthcare systems. According to a study, a smaller share of U.S. hospitals employ dedicated AI implementation teams, which forces reliance on third-party consultants for model validation, workflow integration, and clinician training. Also, as per research, a percentage of hospital CIOs outsourced AI deployment due to internal skill gaps, particularly in bias auditing, regulatory documentation, and change management. In emerging markets, this dependency is even more pronounced.

By Algorithm Insights

In 2024, the deep learning segment captured the top position with a 49.6% share of the artificial intelligence in healthcare market. Its unparalleled capacity to extract hierarchical features from high-dimensional and unstructured data, precisely the kind generated in radiology, pathology, and genomics, accelerates the growth of the deep learning segment in the global market. Beyond imaging, deep learning’s sequence modeling capabilities, via transformers and LSTMs, enable predictive analytics on longitudinal EHR data.

The Natural Language Processing segment is estimated to register the fastest CAGR of 31.8% during the forecast period. The swift growth of the Natural Language Processing segment in the global market is propelled by the explosion of unstructured clinical text, physician notes, discharge summaries, and pathology reports, which constitute a portion of all healthcare data yet remain largely unmined, according to the study. NLP transforms this latent resource into structured, analyzable knowledge. Beyond scribing, NLP drives clinical trial matching. Regulatory tailwinds amplify adoption. Simultaneously, multilingual NLP models are unlocking global access.

By Application Insights

The administrative workflow assistance segment held the largest share of 34.9% share of the artificial intelligence in healthcare market in 2024. Administrative waste consumes a share of U.S. healthcare expenditure, and AI is the only scalable solution to compress this inefficiency, which propels the growth of the administrative workflow assistance segment in the global market. Beyondthe revenue cycle, AI streamlines scheduling, credentialing, and supply chain logistics. The regulatory environment further fuels this prominence. This structural alignment of economic burden, regulatory mandate, and technical feasibility ensures administrative AI remains the largest and most entrenched application segment.

The clinical trial participant identifier segment is anticipated to witness the fastest CAGR of 35.2% from 2025 to 2033. The rapid growth of the clinical trial participant identifier segment is driven by the pharmaceutical industry’s existential need to accelerate trial recruitment, a process that consumes a portion of total development time and fails a share of protocols due to enrollment shortfalls, as per the study. AI shatters this barrier. Regulatory incentives amplify momentum. Precision medicine demands narrower biomarker-defined cohorts.

By End-User Insights

The healthcare providers segment was the largest in the artificial intelligence in healthcare market by occupying 57.8% share of the global market. The growth of the healthcare providers segment is due to the irreversible integration of AI into clinical workflows, from diagnostic support to operational efficiency, where hospitals and clinics serve as both the data source and the point of intervention. According to a study, a share of U.S. hospitals now use AI for at least one clinical function, most commonly radiology triage, sepsis prediction, and ambient documentation. Regulatory frameworks also propel the provider adoption. This structural embedding, where AI becomes inseparable from care delivery, reimbursement, and quality reporting, ensures providers remain the dominant end-user segment.

The pharmaceutical & biotechnology companies segment is likely to experience a CAGR of 33.7% over the forecast period, owing to AI’s capacity to compress drug development timelines and de-risk clinical failure. These are objectives that directly impact shareholder value. In June 2023, BenevolentAI announced its AI-enabled platform delivered a preclinical candidate, BEN-34712, for the potential treatment of ALS, rather than identifying a novel mechanism or entering a Phase II trial. The candidate was progressed into Investigational New Drug (IND)-enabling studies, a step before clinical trials. AI also rescues failed assets. Regulatory incentives amplify momentum. AI is no longer optional; it is the core engine of innovation.

REGIONAL ANALYSIS

North America Market Analysis

North America led the artificial intelligence in healthcare market with a 43.6% share in 2024. The United States accounts for a share of regional adoption, propelled by dense EHR penetration, venture capital concentration, and regulatory clarity. According to a study, a share of U.S. hospitals use interoperable EHRs, the essential data substrate for AI. EHR vendors like Epic and Oracle Health (formerly Cerner) offer marketplaces, such as the Epic App Orchard and Cerner Ignite APIs, where third-party developers can create and offer AI modules. This allows healthcare organizations to deploy a wide range of specialized, FDA-cleared tools directly within their existing workflows. Venture funding amplifies innovation. Regulatory frameworks further strengthen dominance. This ecosystem of data-rich, capital-abundant, and regulation-adaptive ensures North America’s command remains unassailable.

Europe Market Analysis

Europe artificial intelligence in healthcare market was positioned second by capturing 28.8% of share in 2024. Germany anchors a portion of regional adoption, driven by industrial precision in medical engineering and strict data governance. For instance, Siemens Healthineers is actively integrating AI across its product line and is involved in collaborations to deploy AI in clinical workflows and digital pathology solutions. France contributes a share to the global market and is concentrated in public health AI.

Asia Pacific Market Analysis

Asia Pacific artificial intelligence in healthcare market. China dominates with a portion of regional volume, fueled by state-backed AI initiatives and massive EHR digitization. Also, China actively supports medical AI development and implementation across various functions in hospitals. It features a growing number of approved AI-powered medical devices as well as advancements. India is growing through public-private pilots. Japan focuses on aging care. Government mandates lock in structural demand. This policy-driven and population-scale deployment ensures Asia’s trajectory remains steep.

Latin America Market Analysis

Latin America artificial intelligence in healthcare market growth is likely to have significant growth opportunities during the forecast period. Brazil leads with a share of regional activity, concentrated in private hospital networks and public epidemiology. Mexico is scaling through medical tourism. Colombia is emerging via regulatory innovations. Government incentives amplify momentum. Latin America’s pragmatic, outcome-focused adoption, which prioritizes mortality reduction over technological novelty that signals accelerating structural relevance.

Middle East and Africa Market Analysis

The Middle East and Africa are likely to grow in the artificial intelligence in healthcare market during the forecast period. The UAE dominates with a share of regional volume, driven by sovereign AI investments and medical tourism. Saudi Arabia is scaling via NEOM’s AI-integrated health city. South Africa is growing through academic innovation. Regional growth is amplified by sovereign wealth.

COMPETITIVE LANDSCAPE

The artificial intelligence in healthcare market exhibits a tripartite competitive structure: hyperscalers dominate infrastructure and foundation models, specialized startups lead vertical clinical applications, and legacy health IT vendors control workflow integration. Competition centers not on market share but on validation depth, FDA clearances, peer-reviewed clinical outcomes, and real-world performance audits. Barriers to entry include access to labeled clinical datasets, clinician trust cycles exceeding several months, and compliance with evolving EU AI Act and HIPAA Safe Harbor provisions. Innovation velocity is highest in generative diagnostics, automated trial recruitment, and ambient scribing.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global AI in the healthcare market include

- Welltok, Inc.

- Intel Corporation

- Nvidia Corporation

- Google Inc.

- IBM Corporation

- Microsoft Corporation

- General Vision, Inc.

- Enlitic, Inc.

- Next IT Corporation

- iCarbonX

- Siemens Healthineers

- General Electric (GE) Company

- Koninklijke Philips N.V.

- Cloudmedx, Inc.

- Bay Labs, Inc.

Top Players in the Artificial Intelligence in Healthcare Market

- NVIDIA’s contribution lies in democratizing high-performance AI infrastructure tailored for clinical environments by allowing developers and providers to build, validate, and deploy latency-sensitive applications at the edge, from robotic guidance to real-time tumor segmentation, without compromising data governance or regulatory compliance.

- IBM now concentrates on accelerating therapeutic innovation by mining multimodal real-world evidence, EHRs, genomics, and imaging, to identify novel targets, rescue failed compounds, and match patients to trials with biomarker precision, which reduces development timelines while enhancing trial diversity and success probability.

- Google Health leverages its foundation model expertise to transform unstructured clinical text into actionable insights, reducing administrative burden while augmenting diagnostic reasoning, all within secure, institution-controlled environments that prioritize clinician oversight and auditability.

Top Strategies Used by Key Market Participants

Strategic acquisition of clinical data assets, co-development of regulatory-cleared algorithms with health systems under joint IP frameworks, deployment of federated learning to preserve data sovereignty, integration of generative AI into EHR and PACS interfaces for real-time clinical augmentation, and establishment of AI validation labs accredited by FDA and EMA constitute the five dominant strategies employed by leading players to ensure algorithmic trust, regulatory compliance, and seamless clinical adoption across global healthcare ecosystems.

GLOBAL AI IN HEALTHCARE MARKET NEWS

- In November 2023, Koninklijke Philips collaborated with Vestre Viken Health Trust to deploy an AI manager platform that enhances radiology workflows. The AI-enabled bone fracture application for diagnosis allows radiologists to focus on complex cases.

- In October 2023, Microsoft launched new data and AI solutions, Microsoft Cloud, at the HLTH 2023 conference to influence healthcare organizations to enhance patient and clinician experiences.

- In October 2023, Harman, a subsidiary of Samsung Electronics, launched HealthGPT, an innovative Healthcare Private Language Model. This advancement focuses on enhancing patient care, medical research, and decision-making.

- In September 2023, Oracle introduced a generative AI service for healthcare organizations. The Oracle Clinical digital assistant, integrated with Oracle's EHR solutions, helps providers perform tasks through voice commands, which enhances patient care.

- In January 2023, Amazon Web Services and Slalom LLC collaborated with an agreement where this collaboration helps to strategize and develop AI-powered solutions for healthcare, life sciences, and financial services industries.

MARKET SEGMENTATION

This research report on the global AI in the healthcare market has been segmented and sub-segmented based on offering, algorithm, application, end-user, and region.

By Offering

- Hardware

- Software

- Services

By Algorithm

- Deep Learning

- Query Method

- Natural Language Processing

- Contextual Processing

By Application

- Robot-Assisted Surgery

- Virtual Nursing Assistant

- Administrative Workflow Assistant

- Fraud Detection

- Dosage Error Reduction

- Clinical Trial Participant Identifier

- Preliminary Diagnosis

- Others

By End-User

- Healthcare Providers

- Pharmaceutical & Biotechnology

- Patient and Payer

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- MEA

Frequently Asked Questions

What are the major applications of AI in the healthcare sector?

AI is extensively used in healthcare for applications such as medical imaging and diagnosis, drug discovery, virtual health assistants, predictive analytics, and personalized treatment planning.

How does AI impact healthcare professionals and their roles?

AI augments healthcare professionals' capabilities by assisting in diagnosis, treatment planning, and patient management. It allows them to focus more on patient care and decision-making while automating routine tasks, leading to increased efficiency and productivity.

How is AI utilized in medical imaging and diagnostics?

AI algorithms are trained on vast datasets of medical images to assist radiologists and clinicians in interpreting images more accurately and efficiently. AI also enables early detection of diseases such as cancer and improves the accuracy of diagnostic tests.

What are the future prospects for AI in healthcare?

The future of AI in healthcare holds immense potential, with advancements expected in areas such as genomics, telemedicine, remote patient monitoring, and AI-driven robotic surgery. Continued innovation and collaboration between healthcare and technology sectors will drive further transformation in healthcare delivery and patient outcomes.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com