Global Anti Snoring Devices Market Size, Share, Trends & Growth Forecast Report By Device Type (MADs, TRD, Nasal Dilator, Chin Strap, Position Control, Pillows, TSD, EPAP), Surgical Procedure (UP3, LAUP, RFA, Sclerotherapy, Pillar, Others (Septoplasty, ESS)) and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034.

Market Size, 2025

$1.65 BnMarket Estimate, 2026

$1.83 BnMarket Forecast, 2034

$4.12 BnCAGR, 2026–2034

10.71%Global Anti-Snoring Devices Market Report Summary

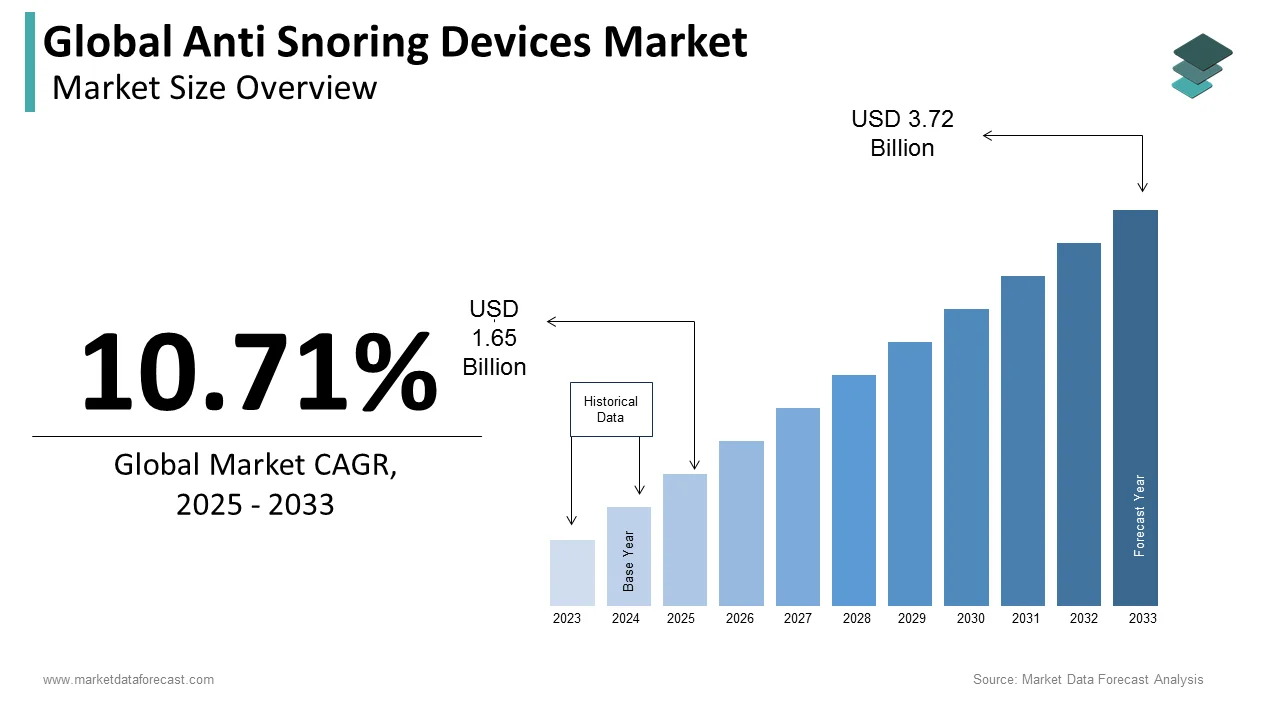

The global anti-snoring devices market was valued at USD 1.65 billion in 2025, is estimated to reach USD 1.83 billion in 2026, and is projected to reach USD 4.12 billion by 2034, growing at a CAGR of 10.71% from 2026 to 2034. Market growth is driven by the increasing prevalence of sleep disorders such as snoring and obstructive sleep apnea, rising awareness about sleep health, and growing adoption of non-invasive treatment options. Lifestyle factors such as obesity, stress, and sedentary habits are contributing to higher demand for anti-snoring solutions. Additionally, technological advancements in wearable and oral devices, along with expanding availability through online channels, are driving global market expansion.

Key Market Trends

- Rising awareness of sleep health and sleep-related disorders.

- Increasing demand for non-invasive and home-based treatment solutions.

- Growth in oral appliances and wearable anti-snoring devices.

- Expansion of e-commerce distribution channels.

- Technological advancements improving comfort and effectiveness of devices.

Segmental Insights

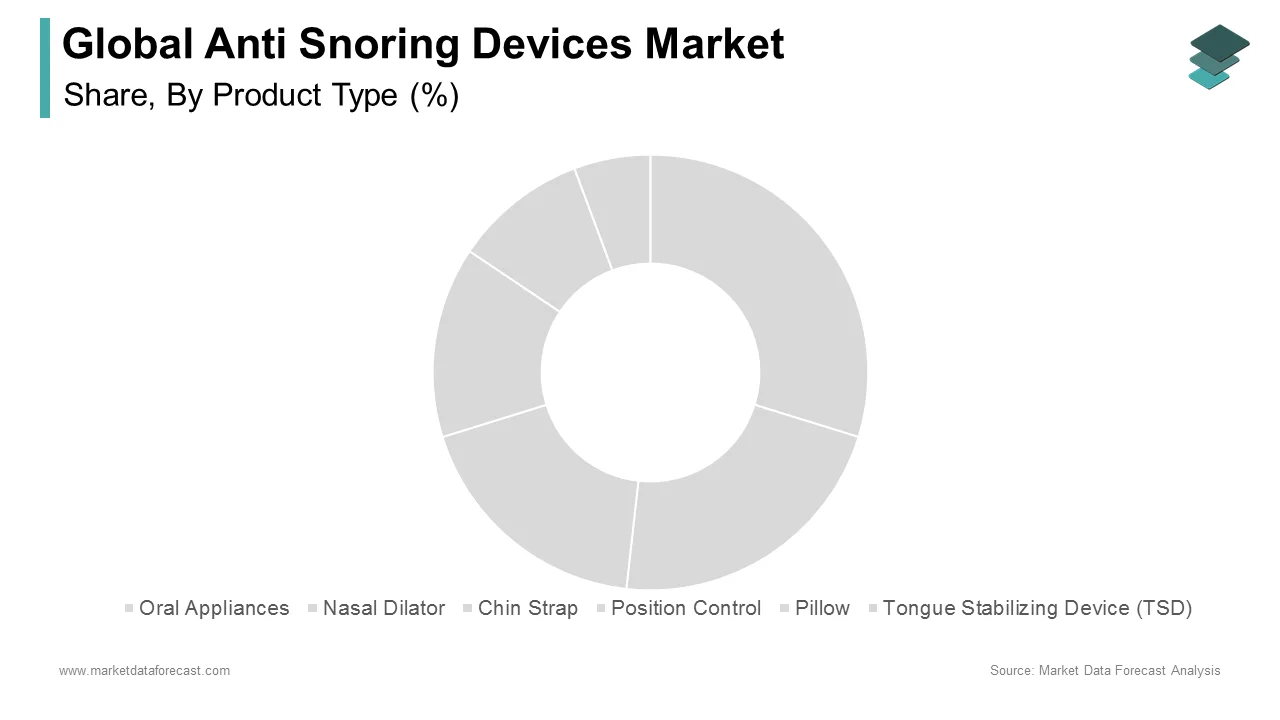

- Based on product type, the mandibular advancement devices (MADs) segment dominated the global anti-snoring devices market by capturing 42.1% share in 2025, driven by their effectiveness and ease of use.

- Based on surgical procedure, the radiofrequency ablation (RFA) segment is expected to capture a leading share during the forecast period due to its minimally invasive nature and growing clinical adoption.

Regional Insights

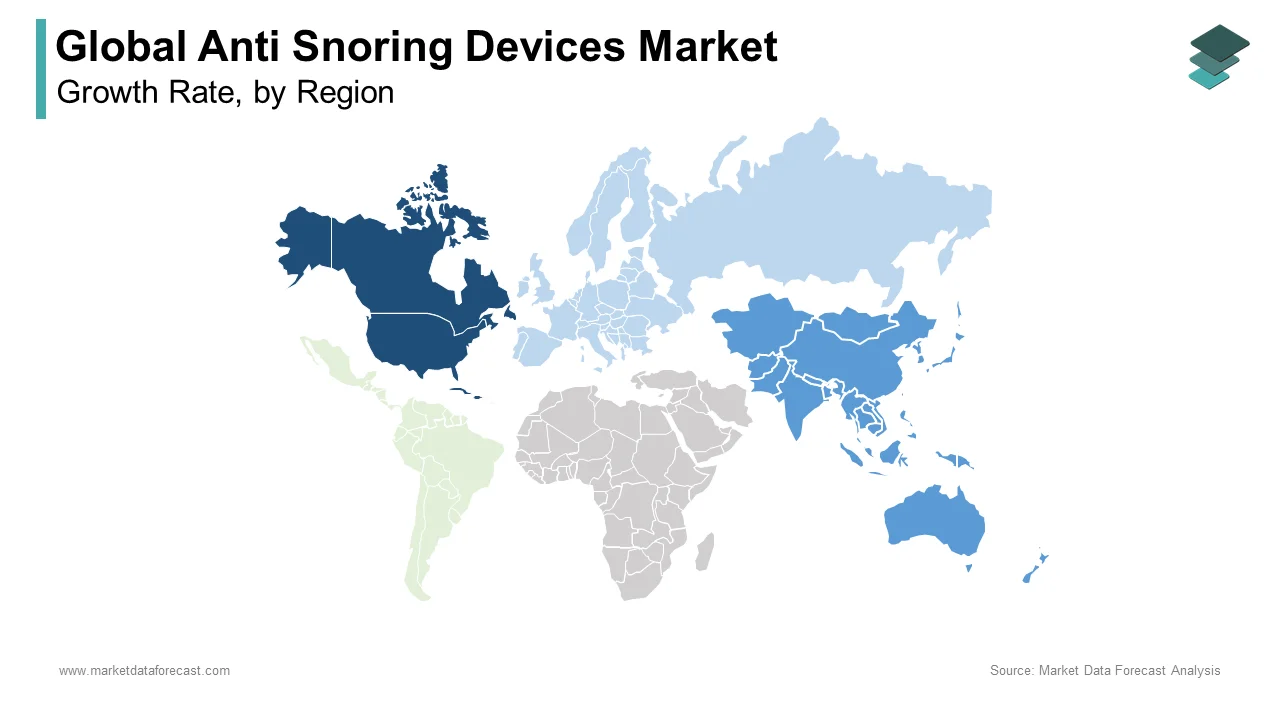

The global anti-snoring devices market is witnessing steady growth across major regions due to rising awareness and increasing diagnosis rates.

- North America led the market in 2025 with 38.2% share, supported by high awareness and advanced healthcare infrastructure.

- Europe followed with 27.2% share in 2025, driven by growing adoption of sleep disorder treatments.

- Asia-Pacific is emerging as the fastest-growing region due to rapid urbanization, lifestyle changes, and increasing awareness of sleep health.

Competitive Landscape

The global anti-snoring devices market is competitive, with several established medical device manufacturers and specialized companies focusing on innovation and product development. Market players are emphasizing user comfort, technological integration, and expanding distribution networks to strengthen their market presence.

Prominent companies operating in the global anti-snoring devices market include Sleeping Well LLC, Apnea Sciences Corporation, Tomed Dr. Toussaint GmbH, AccuMED Corp., Fisher & Paykel Healthcare, ImThera Medical Inc., ResMed Inc., SomnoMed, Philips Respironics, Sleep Well Enjoy Life, Ltd., MEDiTAS Ltd., and Nasal Devices.

Global Anti-Snoring Devices Market Size

The size of the global anti-snoring devices market was worth USD 1.65 billion in 2025. The global market is anticipated to grow at a CAGR of 10.71% from 2026 to 2034 and be worth USD 4.12 billion by 2034 from USD 1.83 billion in 2026.

Anti-snoring devices are specialized tools or appliances designed to reduce or eliminate snoring by keeping the upper airway open during sleep. These solutions range from mandibular advancement devices and tongue stabilizers to continuous positive airway pressure machines and positional therapy aids, serving as critical interventions for respiratory health. The urgency of this sector is underscored by the pervasive nature of sleep-disordered breathing and its severe systemic consequences. A landmark study published in The Lancet Respiratory Medicine estimates that obstructive sleep apnea affects approximately 936 million adults globally between the ages of 30 and 69, with a significant majority remaining undiagnosed and untreated. Furthermore, data from the Centers for Disease Control and Prevention (CDC) confirms that short sleep duration is significantly associated with an increased risk of hypertension, heart disease, and stroke, creating a compelling public health imperative for effective management tools. Research highlighted by the European Respiratory Society suggests that while "dangerous snoring" affects about 20 percent of the population, habitual snoring is even more common, particularly among men (approximately 40 percent), often serving as a primary indicator of underlying airway obstruction. As awareness of the link between poor sleep quality and cognitive decline grows, with the National Sleep Foundation reporting that 45 percent of adults say insufficient sleep affects their daily activities, the demand for non-invasive, home-based solutions has surged. This market functions not merely as a comfort niche but as an essential component of preventive healthcare, offering accessible alternatives to invasive surgery for millions seeking restorative rest.

MARKET DRIVERS

Rising Global Prevalence of Obesity and Sedentary Lifestyles

The escalating global epidemic of obesity is driving the surging demand for these devices and the growth of the anti-snoring devices. This is because excess body weight is the single most significant risk factor for airway collapse during sleep. Adipose tissue accumulation around the neck narrows the upper airway, increasing resistance and causing the soft tissues to vibrate or obstruct breathing entirely. According to the World Health Organization and recent data from The Lancet, worldwide obesity has more than doubled since 1990, surpassing 1 billion people globally in 2022, thereby creating an immediate, massive addressable population for sleep therapies. The Centers for Disease Control and Prevention reports that the prevalence of obstructive sleep apnea is directly correlated with body mass index, affecting up to 70 percent of individuals with severe obesity. Furthermore, sedentary behaviors exacerbate muscle tone loss in the throat, worsening snoring severity. Data from The Lancet confirms that obesity rates already exceeded 1 billion people in 2022, years ahead of the 2030 projection, inevitably driving a proportional and immediate increase in sleep-disordered breathing cases. As traditional weight loss methods often yield slow results, patients increasingly turn to mechanical devices like mandibular advancement splints for immediate relief. This demographic reality ensures a consistent and expanding user base, transforming anti-snoring products from optional accessories into necessary medical interventions for a growing segment of the global population struggling with weight-related respiratory issues.

Increasing Awareness of Sleep Apnea Health Risks and Cardiovascular Links

Heightened public and medical awareness regarding the severe long-term health consequences of untreated snoring and sleep apnea accelerates the expansion of the global anti-snoring devices market. Historically viewed as a mere nuisance, snoring is now widely recognized as a potential symptom of obstructive sleep apnea, a condition linked to life-threatening cardiovascular events. According to the American Heart Association, individuals with untreated sleep apnea are two to three times more likely to develop high blood pressure, heart failure, and irregular heartbeats compared to those without the condition. The National Institutes of Health highlights that chronic hypoxia caused by repeated breathing interruptions during sleep significantly increases the risk of stroke and type 2 diabetes. Educational campaigns by organizations like the Sleep Foundation have successfully shifted consumer perception. This paradigm shift motivates individuals to seek diagnostic testing and proactive treatment options earlier. Data from medical literature shows that early intervention with continuous positive airway pressure (CPAP) and oral appliance therapies can reduce cardiovascular strain and improve overall mortality rates. The correlation between sleep quality and longevity is becoming common knowledge. Consequently, consumers are increasingly willing to invest in effective devices to protect their long-term health, fueling robust market growth.

MARKET RESTRAINTS

Low Diagnosis Rates and High Prevalence of Undetected Cases

A staggering number of individuals with snoring and sleep apnea remain undiagnosed, which creates a critical barrier to the global anti-snoring devices market growth. As a result, this population never enters the treatment pipeline for anti-snoring devices. Many sufferers perceive their condition as normal or are unaware of their symptoms since they occur during sleep, leading to a vast "silent" population that does not seek solutions. According to major studies referenced by the World Sleep Society, a vast majority of moderate to severe obstructive sleep apnea cases remain undiagnosed worldwide, representing a significant disparity between the potential patient population and actual treatment adoption. Health economic analyses and market reports emphasize that logistical hurdles, such as limited access to specialized clinics and the significant expense of in-lab diagnostic tests, prevent many individuals from seeking the professional evaluation often required for prescription-grade devices. Furthermore, primary care physicians frequently fail to screen for sleep disorders during routine visits due to time constraints or lack of training. Research in the field of sleep medicine reveals that the delay between the onset of symptoms and a formal diagnosis often spans several years, leaving patients vulnerable to associated health risks without intervention. This diagnostic bottleneck severely restricts the addressable market, as consumers cannot purchase effective therapeutic devices if they do not recognize they have a medical condition requiring treatment, thus stifling overall market penetration.

Patient Non-Compliance and Comfort Issues with Traditional Devices

Significant obstacles related to patient adherence and physical discomfort associated with traditional anti-snoring devices, particularly Continuous Positive Airway Pressure machines, hamper the sustainability and expansion of the global anti-snoring devices market. CPAP is the gold standard for severe apnea. However, its bulky design, noise, and the sensation of forced air often lead to high abandonment rates among users. According to the Journal of Clinical Sleep Medicine, studies indicate that between 30 percent and 50 percent of patients prescribed CPAP therapy discontinue use within the first year due to intolerance of the mask, skin irritation, or claustrophobia. Similarly, oral appliances like mandibular advancement devices can cause jaw pain, tooth movement, and excessive salivation, leading to discontinuation. The National Sleep Foundation reports that discomfort is the primary reason cited by patients for rejecting therapy, leaving them to revert to untreated snoring. This non-compliance not only negates health benefits but also generates negative word-of-mouth that discourages new users from trying available solutions. Data from industry surveys suggests that nearly 40 percent of device owners leave their equipment unused in drawers. A large portion of users cannot tolerate existing technologies long-term, limiting their comfort and ergonomic well-being. As a result, the effective market size remains restricted until manufacturers can universally solve these issues.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Smart Monitoring Technologies

The incorporation of artificial intelligence, Internet of Things connectivity, and advanced sensors into anti-snoring devices paves the way to enhance efficacy, personalization, and user engagement, which is predicted to propel the growth of the global anti-snoring devices market. Next-generation devices can automatically adjust pressure levels or jaw positioning in real-time based on detected breathing patterns, sleep stages, and body position, optimizing therapy without manual intervention. Research indicates that the adoption of AI-driven sleep solutions is projected to grow significantly as consumers increasingly demand data-backed health insights. Smart apps paired with these devices can provide detailed sleep reports, track progress over time, and offer behavioral coaching, fostering better adherence. Major medical institutions suggest that remote monitoring capabilities allow clinicians to adjust treatment protocols virtually, improving patient outcomes. Consumer electronics trends show that a majority of health-conscious consumers prefer devices that offer interoperability with their existing digital ecosystems. By transitioning from static mechanical tools to dynamic, intelligent health companions, manufacturers can command premium pricing and attract tech-savvy demographics. This technological evolution addresses compliance issues by making therapy seamless and interactive, opening new revenue streams through subscription-based software services, and creating a differentiated market segment poised for rapid scalability.

Development of Customized 3D Printed Oral Appliances

The advent of affordable 3D printing technology offers a substantial opportunity to revolutionize the production of oral anti-snoring devices, which is anticipated to boost the expansion of the global anti-snoring devices market. It enables fully customized, comfortable, and rapidly manufactured solutions tailored to individual anatomy. Traditional boil-and-bite devices often fit poorly, while custom lab-made appliances are expensive and slow to produce. 3D printing allows for the creation of precise digital models from intraoral scans, resulting in devices that fit perfectly, reduce side effects, and improve retention. Studies in restorative dentistry indicate that 3D-printed mandibular advancement devices offer significantly faster production times, with fit and patient satisfaction increasingly comparable to conventional methods. Various sources emphasize that digital workflows can lower laboratory production costs and turnaround times, improving the long-term accessibility of custom therapy, and data from additive manufacturing reports indicate that the cost of producing dental appliances via 3D printing has decreased notably in recent years. Furthermore, the ability to easily iterate on designs based on patient feedback allows for continuous improvement in comfort and efficacy. As tele-dentistry expands, patients can receive scans remotely and have devices mailed directly to them, bypassing geographical barriers. This convergence of digital dentistry and additive manufacturing positions customized 3D printed devices as a high-growth avenue capable of capturing significant market share from both generic and traditional custom segments.

MARKET CHALLENGES

Regulatory Hurdles and Stringent Classification Requirements

Navigating the complex and varied regulatory landscapes governing medical devices is a formidable challenge to the anti-snoring devices market. Manufacturers face this when trying to bring anti-snoring products to global markets. Depending on the jurisdiction and the specific claims made, these devices may be classified as general wellness products, Class I, or Class II medical devices, each requiring different levels of clinical evidence, quality management systems, and pre-market approvals. According to the Food and Drug Administration, obtaining 510(k) clearance for a Class II anti-snoring device can take several months and cost hundreds of thousands of dollars in testing and documentation, creating a high barrier to entry for smaller innovators. The European Union's Medical Device Regulation has further tightened requirements, demanding more rigorous clinical data and post-market surveillance, which delays product launches and increases compliance costs. A study indicates that inconsistent classification standards across countries force companies to maintain multiple product versions and submission dossiers, straining resources. The risk of regulatory rejection or recalls due to insufficient evidence of efficacy creates uncertainty and inhibits investment in research and development. This fragmented regulatory environment slows the pace of innovation and limits the availability of advanced solutions in certain regions, challenging the industry's ability to scale efficiently.

Reimbursement Limitations and High Out-of-Pocket Costs

The lack of comprehensive insurance coverage and reimbursement policies for many anti-snoring devices, particularly over-the-counter options and certain oral appliances, acts as a significant financial constraint limiting the expansion of anti snoring devices market. Some insurance plans cover CPAP machines for diagnosed sleep apnea. However, they often exclude snoring devices or impose high deductibles and co-pays that deter patients. In developing nations, the absence of any reimbursement mechanism makes even basic devices inaccessible to the majority. This financial disconnect between clinical need and affordability restricts market penetration to wealthier demographics, preventing the industry from achieving mass market status and leaving millions of untreated individuals without access to potentially life-improving therapies.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Surgical Procedure, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | Sleeping Well LLC, Apnea Sciences Corporation, Tomed Dr. Toussaint Gmbh, AccuMED Corp., Fisher & Paykel Healthcare, Apnea Sciences Corporation, ImThera Medical Inc., ResMed Inc., SomnoMed, Sleep Well Enjoy Life, Ltd., MEDiTAS Ltd., and Nasal Devices. |

SEGMENTAL ANALYSIS

By Product Type Insights

The Mandibular Advancement Devices (MADs) segment held the majority share of 42.1% of the global anti-snoring market in 2025. This supremacy of the segment is driven by their status as the primary non-invasive alternative to Continuous Positive Airway Pressure therapy, their high efficacy rates for mild to moderate sleep apnea, and increasing insurance coverage for custom-fitted oral appliances. Apart from these, one of the major factors sustaining the leadership of MADs is their proven clinical effectiveness in treating obstructive sleep apnea and snoring, coupled with significantly higher patient tolerance compared to mask-based systems. Unlike CPAP machines, which force air into the airway, MADs mechanically reposition the lower jaw to prevent tissue collapse, a mechanism that many patients find less intrusive and more comfortable for long-term use. According to studies, MADs are recommended as a first-line treatment for patients with mild to moderate obstructive sleep apnea who prefer them over CPAP or who fail CPAP therapy, covering a vast demographic of sufferers. Furthermore, studies indicate that MADs can reduce the Apnea-Hypopnea Index in suitable candidates, providing tangible health benefits that drive physician recommendations. This combination of clinical validation and superior user experience ensures that MADs remain the preferred choice for both clinicians and patients, securing their dominant market position. The growing availability of insurance reimbursement for custom-fitted mandibular advancement devices acts as a powerful driver for market dominance, which makes these premium products accessible to a broader population beyond those who can pay out-of-pocket. Historically, many oral appliances were considered dental cosmetics, but major insurers and government health programs increasingly recognize them as medically necessary, durable medical equipment for sleep apnea management. According to sources, coverage policies have expanded to include custom oral appliances for beneficiaries diagnosed with obstructive sleep apnea, provided they are fitted by qualified dentists, reducing the financial barrier for millions of elderly patients. The financial support encourages patients to opt for high-quality, custom-made devices over cheaper, less effective over-the-counter alternatives. The professional fitting process also ensures better outcomes and fewer side effects, reinforcing the reputation of MADs as a reliable therapeutic standard and driving consistent demand across healthcare systems globally.

The Nasal Dilators segment is projected to register the highest Compound Annual Growth Rate of 9.8 percent during the forecast period. This accelerated growth is fueled by the rising prevalence of nasal obstruction issues, the non-invasive and low-cost nature of the devices, and increasing consumer awareness of nasal breathing's role in sleep quality. The rapid expansion of the nasal dilators segment is largely supported by the escalating global incidence of nasal congestion caused by allergic rhinitis, deviated septa, and chronic sinusitis, which are direct contributors to snoring and mouth breathing. Increasing environmental pollutants and allergens are causing more individuals to suffer from narrowed nasal passages and disrupted sleep. Consequently, a massive addressable market exists for simple mechanical solutions. According to the World Allergy Organization, allergic rhinitis affects a portion of the global population, with numbers rising steadily in urban areas due to pollution and lifestyle changes. A study reports that hay fever and nasal congestion are among the top reasons for sleep disturbances in adults, prompting sufferers to seek immediate relief tools. Nasal dilators, whether internal strips or external adhesives, physically widen the nasal valve, reducing resistance and encouraging nasal breathing, which naturally suppresses snoring. Unlike complex oral appliances, dilators offer an instant, drug-free solution for this specific anatomical issue, appealing to a wide demographic, including athletes and children. This surge in underlying respiratory conditions ensures that the demand for nasal dilators will continue to outpace other segments. The exceptional affordability and over-the-counter availability of nasal dilators is a major growth enablers for their rapid market growth, removing the financial and logistical barriers associated with prescription-only treatments. These devices are typically inexpensive, often costing a lesser amount for a multi-pack, and can be purchased at pharmacies, supermarkets, and online retailers without a doctor's visit or fitting appointment. According to research, the low entry price point makes nasal dilators an attractive first-line trial for individuals experiencing occasional snoring who are hesitant to invest hundreds of dollars in custom oral appliances or CPAP machines. The ease of access is further amplified by the proliferation of e-commerce platforms where consumers can discreetly purchase a wide variety of designs and sizes. Furthermore, the lack of need for professional adjustment or follow-up visits reduces the total cost of ownership to nearly zero, making them highly appealing to price-sensitive consumers and those in regions with limited healthcare access. This combination of low cost, convenience, and immediate availability drives mass adoption, propelling the nasal dilators segment to become the fastest-growing category in the anti-snoring market.

By Surgical Procedure Insights

The RFA segment is estimated to capture the leading share of the global anti-snoring devices market during the forecast period. The growing preference for minimally invasive procedures with shorter recovery times and reduced post-operative discomfort is one of the major factors propelling the growth of the RFA segment in the worldwide market. Radiofrequency ablation offers a targeted approach to shrink and stiffen the tissues in the throat, reducing airway obstruction and improving breathing during sleep. Technological advancements in RFA devices, such as temperature-controlled and impedance-controlled systems, and rising awareness about the effectiveness of RFA in reducing snoring and improving sleep quality, further boost the growth rate of the RFA segment in the global market.

The Uvulopalatopharyngoplasty (UP3) segment is expected to hold a considerable share of the global market during the forecast period, owing to the growing prevalence of snoring and sleep-related breathing disorders. The growing number of advancements in surgical techniques, such as laser-assisted uvulopalatopharyngoplasty (LAUP) and modified procedures, and rising awareness about the potential health risks associated with untreated snoring and sleep apnea further promote segmental growth.

REGIONAL ANALYSIS

North America Anti-Snoring Devices Market Analysis

North America was the top performer in the global anti-snoring devices market and occupied a 38.2% share in 2025. The demand for these devices in North America is credited to high obesity rates, robust healthcare infrastructure, and favorable reimbursement policies for sleep therapies. The market status shows high diagnostic rates and a mature ecosystem of sleep clinics and dental sleep specialists who actively prescribe advanced devices. A primary driving factor is the severe prevalence of obstructive sleep apnea linked to the obesity epidemic. Furthermore, the presence of major medical device manufacturers and continuous innovation in smart sleep technologies fuels market growth. A study indicates that awareness campaigns have successfully increased diagnosis rates, with millions of Americans now seeking treatment annually. The Medicare and private insurance coverage for custom mandibular advancement devices significantly lowers the financial barrier for patients, encouraging uptake of premium solutions. Additionally, the cultural emphasis on productivity and sleep hygiene drives consumers to proactively manage sleep disorders. The region's advanced telehealth capabilities also facilitate remote consultations and device fittings, expanding access to rural populations. These converging factors solidify North America's position as the largest and most sophisticated market for anti-snoring interventions globally.

Europe Anti-Snoring Devices Market Analysis

Europe followed closely behind in the global anti-snoring devices market and captured a 27.2% share in 2025. This expansion of the European market is supported by its aging population, stringent medical device regulations, and growing integration of dental sleep medicine into national health systems. The market status reveals a strong preference for custom-fitted oral appliances and a rising adoption of home sleep testing to diagnose conditions. A key driver is the demographic shift toward an older population, as data reveal that a portion of Europeans are aged 65 or older, a demographic highly susceptible to sleep-disordered breathing due to muscle tone loss. Research highlights that snoring affects nearly half of the adult population in Europe, creating immense latent demand. Governments in countries like Germany and the UK are increasingly recognizing the economic burden of untreated sleep apnea on healthcare systems, leading to expanded reimbursement schemes for oral appliances. Furthermore, the implementation of the EU Medical Device Regulation has raised quality standards, boosting consumer confidence in certified products. The region's strong public health initiatives promoting sleep health and the availability of universal healthcare in many nations ensure steady market growth and high adoption rates of therapeutic devices.

Asia Pacific Anti-Snoring Devices Market Analysis

The Asia Pacific region emerges as the fastest-growing market globally due to rapid urbanization, changing lifestyle patterns, and increasing awareness of sleep health in emerging economies. The market status is dynamic and heterogeneous, ranging from highly developed markets in Japan and Australia to rapidly awakening sectors in China, India, and Southeast Asia. The dominant driving factor is the dramatic rise in obesity and stress-related sleep disorders accompanying economic development, with the World Health Organization noting a sharp increase in non-communicable diseases across the region. In Japan, an aging society similar to Europe's drives significant demand for sleep apnea solutions, while in India and China, the burgeoning middle class is increasingly willing to spend on health and wellness products. Various sources indicate that sleep apnea prevalence in Asia is comparable to the West but remains vastly underdiagnosed, representing a huge opportunity for market education and penetration. The proliferation of e-commerce platforms has made over-the-counter devices like nasal dilators and anti-snoring pillows widely accessible even in remote areas. Furthermore, governments are beginning to incorporate sleep health into national wellness strategies, fostering a conducive environment for market growth. These trends position the Asia Pacific as the most vibrant frontier for the anti-snoring devices industry.

Latin America Anti-Snoring Devices Market Analysis

Latin America expanded gradually in the global market owing to rising urbanization, increasing prevalence of obesity, and gradual improvements in healthcare access and sleep medicine awareness. The shift toward modern healthcare in Brazil, Mexico, and Argentina is accelerating, driven by a growing middle class concentrated in major urban areas. The rising prevalence of obesity acts as a primary catalyst. Economic stabilization in key nations has allowed for greater importation of medical devices and the establishment of local distributors, reducing costs. A study emphasizes a growing number of sleep clinics and trained professionals, although coverage remains uneven compared to North America. The cultural stigma around snoring is slowly diminishing as public health campaigns educate the population on its cardiovascular risks. Additionally, the expansion of private health insurance in the region is beginning to cover sleep diagnostics and treatments, making devices more affordable for insured populations. While economic volatility poses challenges, the fundamental drivers of demographic change and health awareness ensure steady growth potential for the anti-snoring market in this region.

Middle East and Africa Anti-Snoring Devices Market Analysis

The Middle East and Africa region is predicted to grow significantly in the global market during the forecast period. It shows unique growth dynamics fueled by exceptionally high obesity rates in the Gulf, increasing healthcare investments, and a nascent but growing awareness of sleep disorders. The market status is heavily concentrated in Gulf Cooperation Council countries, where high per capita income enables the adoption of premium anti-snoring technologies, while the African market is largely informal but evolving. A significant driving factor is the alarming prevalence of obesity and diabetes in the Middle East. Governments in Saudi Arabia and the UAE are investing heavily in healthcare infrastructure and preventive medicine as part of their national vision plans, including sleep health initiatives. Data from regional medical associations indicates a rising number of sleep conferences and training programs aimed at building local expertise. The expatriate population in the Gulf also drives demand for international standard care. Although infrastructure gaps and cost remain hurdles, the intense health challenges and strategic government focus are laying the groundwork for future market expansion in this diverse region.

COMPETITIVE LANDSCAPE

The competition in the global anti-snoring devices market is characterized by intense rivalry among established medical device giants and agile niche players specializing in oral appliances or over-the-counter solutions. The landscape is moderately consolidated with key players dominating through extensive distribution networks and strong brand recognition, yet fragmented by numerous small manufacturers offering low-cost alternatives. Competitive dynamics are driven by the constant race to enhance user comfort, reduce noise levels, and integrate digital health features that facilitate remote monitoring and adherence tracking. Price competition exists particularly in the over-the-counter segment, but the primary battleground has shifted toward value propositions centered on clinical efficacy and long-term patient support. Regulatory compliance acts as a significant barrier to entry, ensuring that only firms with robust quality management systems can sustain operations in the prescription device sector. Mergers and acquisitions are frequent as larger entities seek to absorb innovative startups and integrate complementary software technologies. This dynamic environment fosters continuous improvement in device design and encourages the adoption of connected health ecosystems that transform traditional sleep therapy into a data-driven clinical practice.

KEY MARKET PLAYERS

The list of top companies leading the global anti-snoring devices market profiled in this report is

- Sleeping Well LLC

- Apnea Sciences Corporation

- Tomed Dr. Toussaint GmbH

- AccuMED Corp.

- Fisher & Paykel Healthcare

- Apnea Sciences Corporation

- ImThera Medical Inc.

- ResMed Inc.

- SomnoMed

- Philips Respironics

- Sleep Well Enjoy Life, Ltd.

- MEDiTAS Ltd.

- Nasal Devices

TOP PLAYERS IN THE MARKET

- ResMed stands as a global leader in the anti-snoring and sleep apnea sector by providing a comprehensive portfolio of connected health devices, including continuous positive airway pressure machines and oral appliances. The company significantly contributes to the global market through its innovative digital health ecosystem that enables remote patient monitoring and data-driven therapy adjustments. Recent actions to strengthen its market position include the acquisition of software companies specializing in sleep diagnostics to create a seamless end-to-end care pathway for users. ResMed has also launched next-generation mask technologies designed to minimize leaks and enhance comfort, directly addressing compliance issues. Their commitment to artificial intelligence integration allows for automatic pressure titration, improving user experience. ResMed maintains a competitive edge and reinforces its reputation as a trusted partner for managing sleep-disordered breathing worldwide. They achieve this by focusing on cloud-based platforms and expanding direct-to-consumer channels.

- SomnoMed operates as a premier provider of oral appliance therapy with a strong emphasis on custom-fitted mandibular advancement devices for treating snoring and obstructive sleep apnea. The company plays a vital role in the global market by offering the SomnoDent product line, which utilizes biocompatible materials and precise digital fabrication techniques to ensure patient comfort and efficacy. Recent strategic moves involve the expansion of their digital workflow capabilities, allowing dentists to design and manufacture devices faster with higher accuracy. SomnoMed has strengthened its market presence by investing in extensive clinical research to validate the long-term cardiovascular benefits of its devices compared to other treatments. Their focus on education and training programs for dental professionals ensures high-quality delivery of care globally. SomnoMed continues to set industry benchmarks for oral appliance therapy through continuous innovation in material science and digital dentistry. By doing so, it solidifies its status as a key driver of non-invasive sleep solutions.

- Philips Respironics remains a dominant force in the anti-snoring market, known for its extensive range of sleep therapy devices, including auto-adjusting positive airway pressure systems and smart masks. The company contributes extensively to the global sector by leveraging its broad healthcare technology infrastructure to deliver integrated sleep and respiratory care solutions. Recent efforts to strengthen its position include the rollout of advanced cloud-connected platforms that provide real-time adherence data to clinicians and patients for better therapy management. Philips has also focused on developing quieter and more compact devices to improve portability and reduce noise disturbance for bed partners. Their investment in user-centric design aims to alleviate common barriers to treatment, such as claustrophobia and skin irritation. Philips is driving accessibility and adherence in sleep therapy by prioritizing interoperability with electronic health records and fostering partnerships with sleep clinics. In doing so, they are reinforcing their leadership role in the global market.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the anti-snoring devices market primarily focus on product innovation to develop smart connected devices that integrate artificial intelligence and remote monitoring capabilities for personalized therapy. Companies heavily invest in research and development to create lighter, quieter, and more comfortable masks and oral appliances that improve patient adherence rates. Strategic acquisitions of digital health startups represent another major approach to expand service offerings and build comprehensive ecosystems for sleep management. Market participants are increasingly adopting direct-to-consumer models and telehealth platforms to reach undiagnosed patients and simplify the prescription process. Partnerships with dental professionals and sleep clinics help firms ensure proper fitting and follow-up care, which are critical for treatment success. Additionally, companies are expanding their global footprint by entering emerging markets where awareness of sleep disorders is rising. These combined strategies allow leading firms to maintain competitive advantages and drive growth in a highly regulated and technology-driven landscape.

KEY MARKET PLAYERS

The list of top companies leading the global anti-snoring devices market profiled in this report is

- Sleeping Well LLC

- Apnea Sciences Corporation

- Tomed Dr. Toussaint GmbH

- AccuMED Corp.

- Fisher & Paykel Healthcare

- Apnea Sciences Corporation

- ImThera Medical Inc.

- ResMed Inc.

- SomnoMed

- Sleep Well Enjoy Life, Ltd.

- MEDiTAS Ltd.

- Nasal Devices

GLOBAL ANTI-SNORING DEVICES MARKET NEWS

- Tomed introduced SomnoBelt, an anti-snoring belt in the chest that prevents supine sleep and disables snoring by providing the right night sleep position.

- In early 2015, Meditas Limited introduced nasal dilators for the continuous flow of air. An unobtrusive nasal system that adds into the nostril where, by opening the air passage, it facilitates ventilation by increasing resistance to incoming air. The extra oxygen received with Nasal Dilators enables people to breathe deeply and much less often.

- In mid-2015, Zimmer Holdings Inc. acquired Biomet and announced they would combine to dominate the markets to counter disruptive small and medium-sized producers. A broad and diverse portfolio of musculoskeletal solutions will be available to the company. Zimmer Biomet's size would ensure greater competition in core franchises and a more substantial presence in emerging markets.

MARKET SEGMENTATION

This research report on the global anti-snoring devices market has been segmented and sub-segmented based on product type, surgical procedure, and Region.

By Product Type

- Oral Appliances

- Mandibular Advancement Devices (MADs)

- Tongue Retaining Devices (TRD)

- Nasal Dilator

- Chin Strap

- Position Control

- Pillow

- Tongue Stabilizing Device (TSD)

- EPAP

By Surgical Procedure

- Uvulopalatopharyngoplasty (UP3)

- Laser-Assisted Uvula Palatoplasty (LAUP)

- Radiofrequency Ablation (RFA)

- Sclerotherapy

- Pillar

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What is the global anti snoring devices market?

The global anti snoring devices market comprises products designed to reduce or eliminate snoring through oral appliances, nasal dilators, CPAPs, and other therapeutic devices worldwide

2. What drives growth in the global anti snoring devices market?

Growth is driven by increasing sleep apnea prevalence, rising awareness, technological advancements, aging populations, and demand for non-invasive treatments globally

3. Which types of devices lead the global anti snoring devices market?

Mandibular advancement devices dominate, followed by nasal dilators and CPAP machines, favored for efficacy, ease of use, and cost-effectiveness

4. How does sleep apnea influence the global anti snoring devices market?

Obstructive sleep apnea, linked to snoring, raises demand for therapeutic devices within the global anti snoring devices market for better treatment outcomes

5. What regions dominate the global anti snoring devices market?

North America leads due to healthcare infrastructure, followed by Europe and Asia-Pacific, driven by growing awareness and technological adoption

6. What technological advancements impact the global anti snoring devices market?

Bluetooth connectivity, smart sensors, enhanced comfort designs, and AI-based monitoring increase device functionality and user adherence

7. How important is patient compliance in the global anti snoring devices market?

High compliance improves treatment efficacy; thus, manufacturers focus on comfort and ease-of-use within the global anti snoring devices market

8. What role do oral appliances play in the global anti snoring devices market?

Oral appliances reposition the jaw to open airways, widely adopted for mild to moderate snoring in the global anti snoring devices market

9. How do nasal dilators work in the global anti snoring devices market?

Nasal dilators keep nasal passages open to enhance airflow, offering a non-invasive snoring solution in the global anti snoring devices market

10. How does lifestyle affect snoring and the global anti snoring devices market?

Lifestyle factors like obesity, smoking, and alcohol increase snoring risk, driving interest in solutions within the global anti snoring devices market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com