Global Accountable Care Solutions Market Size, Share, Trends & Growth Forecast Report By Product & Service (Healthcare Provider, Healthcare Payer and Services), Delivery Mode (Web & Cloud and On-premises), End-User and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2025 To 2033.

Global Accountable Care Solutions Market Size

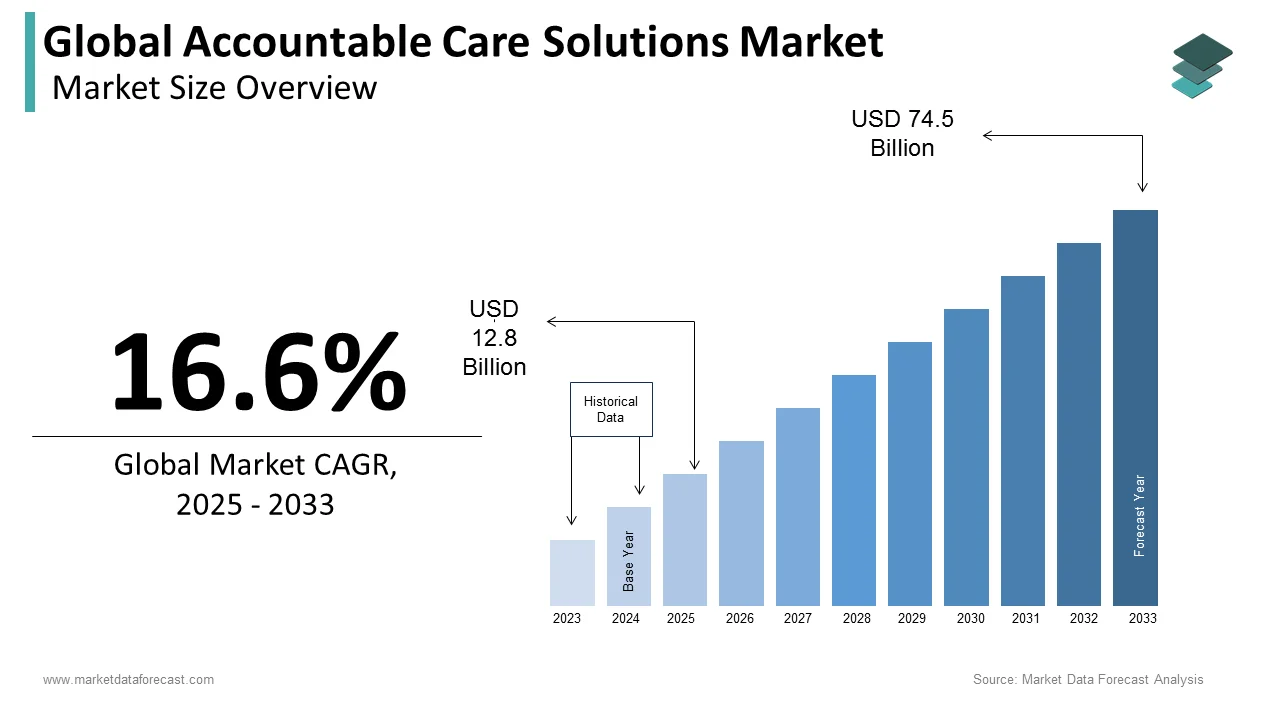

The global accountable care solutions market was worth US$ 18.7 billion in 2024 and is anticipated to reach a valuation of US$ 74.5 billion by 2033 from US$ 12.8 billion in 2025, and it is predicted to register a CAGR of 16.6% during the forecast period 2025-2033.

MARKET DRIVERS

The shift from fee-for-service to value-based care models is one of the key factors propelling the growth of the accountable care solutions market growth. The adoption of a value-based care model is on the rise owing to the benefits associated such as improved patient outcomes and lower healthcare costs enabling care coordination, data analytics, and financial accountability. The transition from fee-for-service to value-based care models is anticipated to accelerate in the coming years and contribute to the accountable care solutions market growth. The rising need for cost containment is another major factor fuelling the market’s growth rate. Healthcare costs are growing significantly worldwide. Accountable care solutions enable better care coordination, population health management and utilization management, which helps limit costs and improve efficiency in healthcare delivery.

The growing number of policies and regulations to promote accountable care models by the governments of several countries and technological advancements such as electronic health records (EHRs), health information exchange (HIE), and telehealth contribute to the market growth. The growing usage of accountable care solutions in population health management, rising demand for interoperability and data analytics across various healthcare settings, and increasing number of collaborations and partnerships between accountable care solution providers, technology vendors, and payers to implement comprehensive accountable care models drive the market growth.

The growing prevalence of chronic diseases and an increasingly aging population fuels the adoption of accountable care solutions and supports market growth. The rising need to comply with regulatory guidelines and government eHealth initiatives favors the global accountable care solutions market. The ability of responsible health care to contain costs while providing affordable and patient-centered care is becoming increasingly important. The growing focus on custom-based medicine and analytics in quality and personalized medicine will likely offer tremendous opportunities for the global accountable care solutions market during the forecast period. Factors such as existing markets and increased take-up of cloud-based models further promote this market. The activities such as acquisitions, partnerships, and collaborations pave the way for market expansion and the client base of market players. These market players are expected to have lucrative opportunities with increasing global accountable care solutions market growth.

MARKET RESTRAINTS

The reluctance of end-users to introduce new procedures and the lack of internal IT skills may hinder the global accountable care solutions market growth. Besides the unwillingness of providers to provide these solutions, the need for infrastructure investment, the lack of patient involvement, and the low usage of Internet solutions impede the market's growth rate. Furthermore, the lack of interoperability and the data security issues associated with cloud solutions are other factors that hold back the global accountable care solutions market.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

Segments Covered |

Products and Services, Delivery Mode, End-User, and Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

|

Market Leaders Profiled |

Cerner Corporation (United States), IBM Corporation (United States), UnitedHealth Group (United States), Aetna, Inc. (United States), Allscripts Healthcare Solutions, Inc. (United States) and Epic Systems Corporation (United States), McKesson Corporation (United States). |

SEGMENTAL ANALYSIS

By Product & Services Insights

Based on product and service, the healthcare providers segment held the most considerable share in the global accountable care solutions market in 2024 and is predicted to continue the domination throughout the forecast period. The growing adoption of value-based care models and accountable care organizations (ACOs) by healthcare providers to improve care coordination, quality, and cost-efficiency and increasing demand for integrated healthcare IT solutions that enable population health management, care coordination, electronic health records (EHR) integration, and data analytics to drive better patient outcomes majorly drive the growth of the healthcare providers segment in the global market. The rising emphasis on patient engagement and care management tools that enhance patient-provider communication, remote monitoring, and self-management of chronic conditions and technological advancements in healthcare provider solutions, such as interoperability, telehealth, and artificial intelligence (AI) applications further propel the segmental growth. Under the sub-segments, the healthcare analytics segment is another segment that held a substantial share of the global market in 2024 and is likely to register a healthy CAGR during the forecast period. The need to improve the gain of healthcare operations and government initiatives to improve the quality of care delivered to patients and reduce the high cost of healthcare are the factors leading to healthcare providers' development.

The healthcare payer solutions segment is anticipated to account for a substantial share of the global market during the forecast period owing to the growing healthcare expenditure and increasing need for payers, such as insurance companies and government agencies, to improve cost control, operational efficiency, and member satisfaction. The growing demand for advanced claims processing systems, payment integrity solutions, fraud detection and prevention tools, and care management platforms to streamline payer operations and enhance decision-making and rising emphasis on population health management and value-based payment models that require payers to implement data analytics, risk stratification, and care coordination solutions for better outcomes and cost management further boost the growth rate of the healthcare payers solutions segment in the worldwide market.

By Delivery Mode Insights

Based on delivery mode, the web and cloud segment is anticipated to account for the leading share of the global market during the forecast period owing to the rapid adoption of cloud-based solutions in the healthcare industry that offer scalability, flexibility, and cost-effectiveness. The easy accessibility and availability of data and applications from any location with an internet connection, rapid technological advancements in web-based platforms, including user-friendly interfaces, real-time data analytics, and interoperability and rising emphasis on population health management and value-based care models further fuel the growth rate of the web and cloud segment in the global market.

The on-premises segment is expected to grow at a moderate CAGR during the forecast period.

By End User Insights

Based on end-user, the healthcare provider holds the most substantial share value of the worldwide accountable care solutions market based on the end-user segment. The growing emphasis on value-based care models, increasing need for care coordination, population health management, and patient engagement to improve the quality of care and achieve better health outcomes drive the growth of the healthcare providers segment in the global market. The rapid adoption of accountable care solutions by healthcare providers to enhance care delivery processes, optimize resource utilization, streamline workflows, and improve communication and collaboration among care teams and integration of electronic health records (EHRs) and other health information systems with accountable care solutions boost the growth rate of the healthcare providers segment in the worldwide market.

REGIONAL ANALYSIS

Geographically, the North American market accounted for the largest share of the global market in 2024, and the domination of the North American region in the global market is most likely to continue throughout the forecast period.

The presence of well-established healthcare infrastructure and high healthcare spending drives the adoption of accountable care solutions to improve care coordination, quality, and cost-effectiveness and propel the North American market growth. The rising emphasis on value-based care models and healthcare reforms incentivizes the implementation of accountable care solutions to improve patient outcomes and reduce healthcare costs and technological advancements and a mature digital health ecosystem supports the adoption of accountable care solutions in the region and boosts the growth rate of the North American market. The U.S. and Canada are the major contributors to the North American regional market.

Europe is a noteworthy regional market for accountable care solutions and is expected to capture a substantial share of the worldwide market during the forecast period. The growing number of initiatives by the governments of European countries to promote integrated care and population health management drive the adoption of accountable care solutions to enhance care coordination and patient outcomes and promote the European market growth. The growing aging population and increasing burden of chronic diseases fuels the demand for accountable care solutions that can improve efficiency, prevent hospital readmissions, ensure continuity of care, and contribute to the European market growth. Interoperability and data exchange initiatives at the regional level facilitate the implementation of accountable care solutions across different healthcare settings favoring the European market growth.

APAC is a potential regional market for accountable care solutions and is predicted to register the fastest CAGR among all the regions worldwide during the forecast period. The growing healthcare expenditure, rising healthcare awareness, and increasing need for healthcare system reforms drive the adoption of accountable care solutions in the Asia-Pacific region, driving the growth of the APAC market. Advancements in healthcare IT infrastructure and increasing digitization of healthcare records support the implementation of accountable care solutions in the APAC region and propel the APAC market growth. India, China, Japan and South Korea are estimated to capture the major share of the APAC market during the forecast period.

Latin America is expected to witness a healthy CAGR during the forecast period. The growing efforts from the governments of Latin American countries to strengthen healthcare systems, improve care quality, and enhance patient outcomes drive the adoption of accountable care solutions in Latin American countries and contribute to the Latin American market growth. The growing private sector investments in healthcare infrastructure and technology fuel the adoption of accountable care solutions to streamline care delivery and improve care coordination and rising emphasis on value-based care models and population health management encourages the implementation of accountable care solutions in the region to promote regional market growth.

MEA accounted for a moderate share of the global market in 2024 and is predicted to showcase a steady CAGR in the coming years owing to the increasing investments to develop the healthcare infrastructure in the countries of MEA and the growing number of digital health initiatives and advancements in telemedicine and health information exchange.

KEY MARKET PARTICIPANTS

Cerner Corporation (United States), IBM Corporation (United States), UnitedHealth Group (United States), Aetna, Inc. (United States), Allscripts Healthcare Solutions, Inc. (United States) and Epic Systems Corporation (United States), McKesson Corporation (United States), Verisk Health (United States), ZeOmega, Inc. (United States), EClinicalWorks, Inc. (United States) and NextGen Healthcare (United States) are some of the major players in the global accountable care solutions market.

RECENT MARKET DEVELOPMENTS

- In November 2019, NextGen Healthcare announced the acquisition of Medfusion. With this acquisition, the company aimed to provide a better experience for healthcare consumers, especially in the ambulatory platform, strengthening its portfolio.

- In July 2019, the partnership between Epic and Connected Care health services brought many changes in healthcare organizations. These companies are engaged in integrating genomic data and AI-based predictive models to improve the quality of services in hospitals and clinics.

MARKET SEGMENTATION

This research report on the global accountable care solutions market has been segmented and sub-segmented based on the products and services, delivery mode, end-user, and region.

By Product & Service

- Healthcare Provider Solutions

- EHR

- Healthcare Analytics

- RCM

- Patient Engagement Solutions

- Population Health Management (PHM) Solutions

- Care Management Solutions

- HCIT Integration Systems

- HIE

- CDSS

- Healthcare Payer Solutions

- Claims Management Solutions

- Payment Management Solutions

- Provider Network Management Solutions

- Other Payer Solutions

- Services

- Support and Maintenance Services

- Implementation Services

- Consulting Services

- Training & Education Services

By Delivery Mode

- Web & Cloud

- On-Premises

By End User

- Healthcare Providers

- Healthcare Payers

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What was the size of the accountable care solutions market worldwide in 2024?

The global accountable care solutions market size was worth USD 18.7 billion in 2024.

Does this report include the impact of COVID-19 on the accountable care solutions market?

Yes, we have studied and included the COVID-19 impact on the global accountable care solutions market in this report.

Which segment by end-user held the leading share in the accountable care solutions market in 2024?

Based on the end-user, the healthcare providers segment had the largest share of the global accountable care solutions market in 2024.

Which are the companies leading the accountable care solutions market?

Cerner Corporation, IBM Corporation, UnitedHealth Group, Aetna, Inc., Allscripts Healthcare Solutions, Inc., Epic Systems Corporation, McKesson Corporation, Verisk Health, ZeOmega, Inc., EClinicalWorks, Inc., and NextGen Healthcare are some of the notable players in the accountable care solutions market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from $ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: [email protected]