- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

Market Size, 2025

$262.23 BnMarket Estimate, 2026

$287.67 BnMarket Forecast, 2034

$603.31 BnCAGR, 2026–2034

9.7%Executive Summary: Global Cybersecurity Market

- Market Scope: Comprehensive global cybersecurity market analysis covering component segments, software solutions, regional country frameworks, zero-trust architectures, and AI-driven threat landscapes.

- Market Valuation: Valued at USD 262.23 billion (2025), estimated at USD 287.67 billion (2026), and projected to reach USD 603.31 billion by 2034, registering a robust CAGR of 9.7% (2026–2034).

- Primary Growth Drivers: Escalating sophistication of AI-powered cyberattacks, rapid digital transformation across critical industries, stringent regulatory mandates (e.g., NIS2, SEC rules), and a global workforce gap of 4 million professionals.

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (2025 Position) | Fastest-Growing Segment |

|---|---|---|

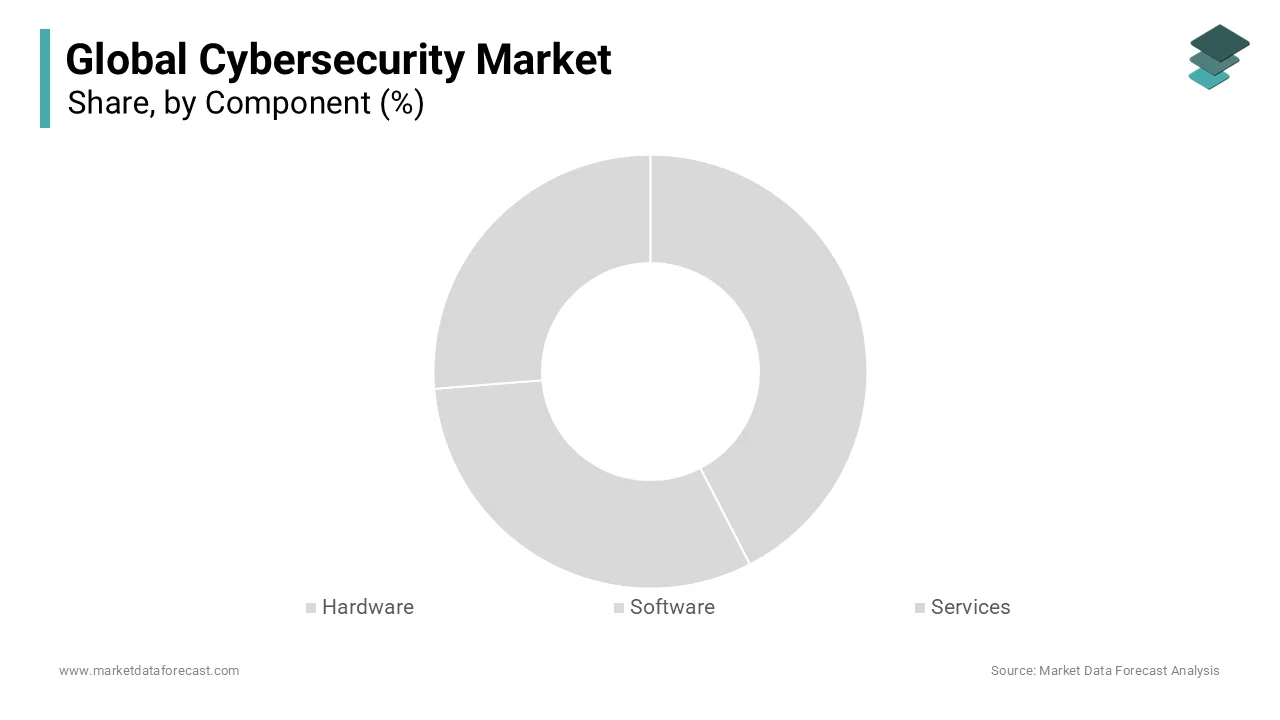

| By Component Type | Services Segment (dominated the market by capturing 42.3% of share) | Software Segment (projected to expand at a CAGR of 14.8%) |

| By Software Category | Firewall Solutions (held the largest software share at 28.3%) | Threat Intelligence Platforms (anticipated to grow at a CAGR of 19.4%) |

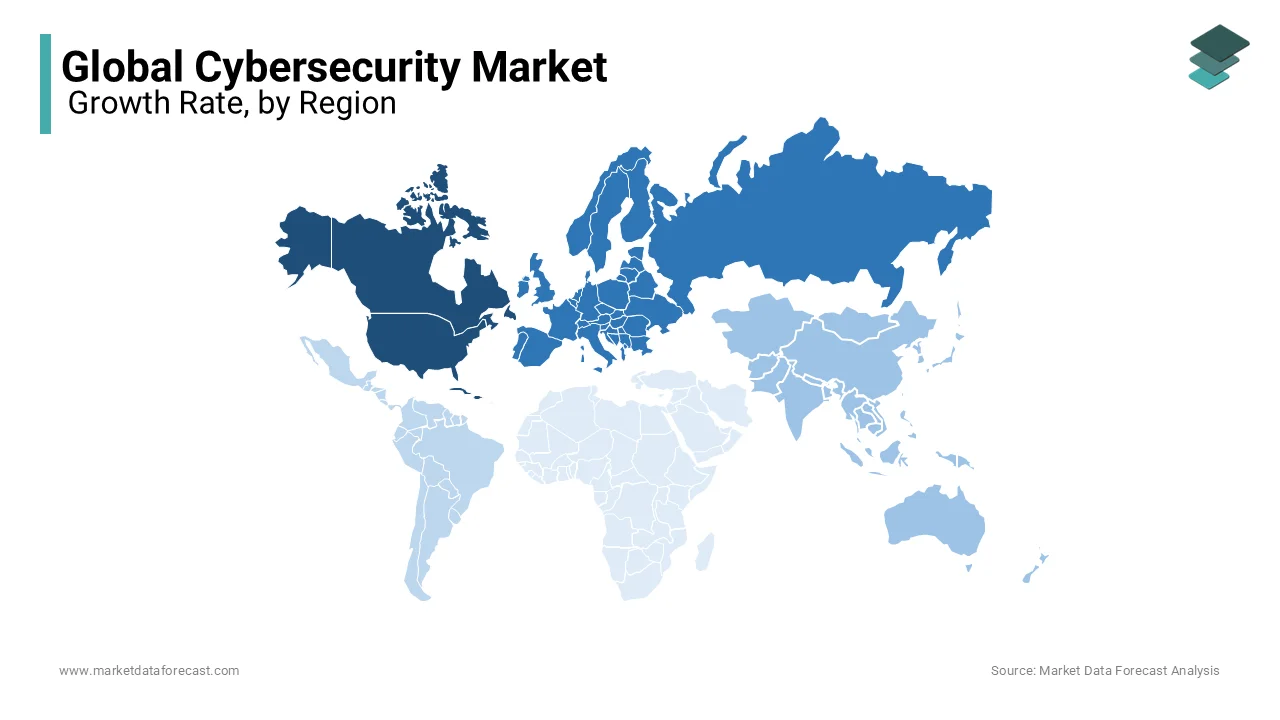

| By Region | North America (led regionally with 38.3% of global share), followed by Europe (26.4%) | Asia-Pacific (positioned as a high-growth market with surging incident rates) |

Major Market Players & Market Structure

Market Structure: Highly competitive global cybersecurity and network protection landscape characterized by strategic acquisitions, identity-centric zero-trust policy rollouts, AI-driven SOC expansions, and third-party vendor integrations.

Key Companies: Broadcom (Symantec Corporation), Cisco Systems Inc., Check Point Software Technology Ltd., CrowdStrike, IBM, McAfee LLC, Palo Alto Networks Inc., Trend Micro Incorporated, Norton LifeLock, Rapid7, and Micro Focus.

Global Cybersecurity Market Size

The global cybersecurity market was worth USD 262.23 billion in 2025. The global market is expected to reach USD 603.31 billion by 2034 from USD 287.67 billion in 2026, growing at a CAGR of 9.7% between 2026 and 2034.

Cybersecurity extends beyond traditional perimeter defenses to include advanced threat intelligence, zero-trust architectures, endpoint detection and response (EDR), cloud security, and identity and access management (IAM). According to the International Telecommunication Union, over 5.4 billion people globally used the internet in 2023, a figure that has intensified exposure to cyber risks. Moreover, as per the International Data Corporation, global spending on cybersecurity solutions surpassed $200 billion in 2023, reflecting institutional recognition of cyber resilience as a strategic imperative. Regulatory frameworks such as the EU’s NIS2 Directive and Singapore’s Cybersecurity Act exemplify governmental efforts to enforce robust digital safeguards.

MARKET DRIVERS

Increasing Digital Transformation Across Sectors Driving Cybersecurity Demand

The relentless pace of digital transformation across finance, healthcare, manufacturing, and government sectors is driving the growth of the cybersecurity market. Enterprises are rapidly adopting cloud computing, artificial intelligence, and data analytics to enhance operational efficiency, but these advancements inherently expand the attack surface. According to the International Data Corporation, global data creation is projected to reach 181 zettabytes by 2025, much of which is sensitive and requires stringent protection. Financial institutions, for instance, process over 1.3 billion digital transactions daily, as reported by the Bank for International Settlements in 2023, making them prime targets for cybercriminals. Additionally, the shift to remote and hybrid work models has led to a 300% surge in phishing attempts targeting corporate credentials, as noted by Verizon’s 2023 Data Breach Investigations Report. These evolving digital ecosystems necessitate advanced security frameworks such as zero-trust models and secure access service edge (SASE), which integrate identity verification and real-time threat monitoring.

Escalating Sophistication and Frequency of Cyberattacks as a Market Driver

The rising complexity and frequency of cyber threats are also expected to propel the growth of the cybersecurity market. Cybercriminals are increasingly leveraging artificial intelligence, machine learning, and automated attack tools to bypass traditional defenses. As per the 2024 Global Threat Report by CrowdStrike, there was a 77% year-over-year increase in ransomware attacks during 2023, with adversaries deploying double and triple extortion tactics to maximize impact. State-sponsored attacks have also intensified, with Microsoft detecting over 1,000 discrete nation-state threat groups actively operating across 140 countries in 2023. Notably, the energy and infrastructure sectors experienced a 45% increase in targeted intrusions, as reported by the Industrial Control Systems Cyber Emergency Response Team (ICS-CERT). These trends have compelled enterprises to invest in proactive defense mechanisms such as extended detection and response (XDR), AI-driven anomaly detection, and cyber threat intelligence platforms.

MARKET RESTRAINTS

Cybersecurity Skills Shortage Impeding Market Effectiveness

The persistent global shortage of skilled professionals capable of managing and responding to complex cyber threats is a significant factor inhibiting the growth of the cybersecurity market. Despite increasing investment in security technologies, organizations struggle to deploy and maintain these systems due to a lack of qualified personnel. As per the 2023 (ISC)² Cybersecurity Workforce Study, the global cybersecurity workforce gap stands at 4 million professionals, with Asia-Pacific alone accounting for 2.4 million unfilled positions. The European Union Agency for Cybersecurity reported that 65% of EU-based organizations face difficulties in recruiting cybersecurity experts, leading to delayed incident response and suboptimal configuration of security tools. The skills gap is further exacerbated by the rapid evolution of attack techniques, which requires continuous upskilling in areas such as cloud security, digital forensics, and adversarial AI. Consequently, many organizations rely on overburdened teams, increasing the risk of human error and prolonged vulnerability exposure. Automation and AI are being leveraged to compensate, but they cannot fully replace human judgment in threat analysis and strategic decision-making.

Regulatory Fragmentation and Compliance Complexity as a Market Restraint

The absence of harmonized global cybersecurity regulations presents a significant impediment to the cohesive development and implementation of security strategies across multinational enterprises. Organizations operating across multiple jurisdictions must navigate a labyrinth of data protection and cybersecurity mandates, including the EU’s GDPR, the U.S. SEC’s cyber disclosure rules, India’s Digital Personal Data Protection Act, and Australia’s Privacy Act. As per the Global Privacy Assembly, over 130 countries have enacted data protection laws, yet enforcement mechanisms and compliance requirements vary widely, creating operational inefficiencies.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence in Threat Detection as a Strategic Opportunity

The integration of artificial intelligence (AI) into cybersecurity frameworks to enhance threat detection, reduce response times, and improve predictive defense capabilities is expected to bolster the growth of the cybersecurity market. Modern cyber threats are increasingly automated and polymorphic, rendering signature-based detection methods obsolete. AI-powered systems, however, can analyze vast datasets in real time to identify anomalous behaviors indicative of breaches. As per McKinsey & Company’s 2023 analysis on AI in cybersecurity, organizations leveraging machine learning models experienced a 60% reduction in false positives and a 40% improvement in mean time to detect (MTTD) threats. Google’s Chronicle platform, for instance, processes over 800 trillion security events annually using AI-driven analytics, enabling rapid identification of sophisticated intrusion patterns. Furthermore, AI enhances proactive defense through predictive modeling; Darktrace’s Antigena system autonomously responds to novel threats by learning normal network behavior, having mitigated over 1.5 million cyber incidents in 2023 alone.

Expansion of Zero Trust Architectures in Enterprise Security

The widespread adoption of Zero Trust security models is another opportunity for the growth of the cybersecurity market. As per Gartner, by 2025, 60% of enterprises will phase out most of their remote access virtual private networks (VPNs) in favor of Zero Trust Network Access (ZTNA) solutions, up from less than 10% in 2021. In the private sector, Microsoft reported that organizations adopting its Zero Trust framework experienced a 90% reduction in identity-related breaches. The healthcare industry, where 83% of organizations now use cloud-hosted electronic health records, has seen a 50% increase in ZTNA deployments since 2022, as noted by the Healthcare Information and Management Systems Society. Additionally, the manufacturing sector, increasingly reliant on industrial IoT, is integrating Zero Trust principles to secure operational technology networks. According to the Industrial Internet Consortium, over 70% of smart factories are piloting Zero Trust policies to prevent lateral movement by attackers.

MARKET CHALLENGES

Rapid Evolution of Adversarial Tactics Outpacing Defensive Capabilities

The accelerating pace at which cyber adversaries refine their tactics, techniques, and procedures (TTPs), often outpacing the development and deployment of defensive technologies, is also hindering the growth of the cybersecurity market. Cybercriminals are increasingly employing AI-driven tools to automate reconnaissance, generate polymorphic malware, and conduct highly personalized phishing campaigns. Additionally, fileless malware, which operates in memory without leaving disk traces, accounted for 45% of all malware attacks in 2023, as reported by Kaspersky’s Global IT Security Risks Survey. These stealthy methods evade traditional signature-based detection systems, necessitating advanced behavioral analytics and endpoint detection tools. However, the average time to patch vulnerabilities remains at 21 days, as disclosed by Palo Alto Networks’ Unit 42 in 2023, creating exploitable windows. The integration of AI by threat actors further complicates defense; IBM Security observed that AI-powered attacks can reduce the time to compromise a system from hours to minutes.

Supply Chain Vulnerabilities as a Systemic Cybersecurity Challenge

The increasing reliance on third-party vendors and software suppliers has introduced systemic vulnerabilities that undermine even the most robust internal security frameworks, which also impedes the growth of the cybersecurity market. Cyber adversaries are increasingly targeting supply chains to gain indirect access to high-value organizations through less secure partners. As per the 2023 Sonatype State of the Software Supply Chain Report, 95% of applications contain open-source components, with an average of 713 such components per application, many of which include unpatched vulnerabilities. The healthcare sector is particularly exposed; a 2023 study by the Healthcare Supply Chain Association revealed that 62% of hospitals use medical devices with outdated firmware, often supplied through opaque vendor networks.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 9.7% |

| Segments Covered | By Component, Software, Security Type, Deployment Mode, Organization Size, End-User Industry, and Region |

|

Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled | Broadcom (Symantec Corporation), Cisco Systems, Inc., Check Point Software Technology Ltd., IBM, McAfee LLC, Palo Alto Networks, Inc., Trend Micro Incorporated, Norton LifeLock, Rapid7, Micro Focus, among others |

SEGMENTAL ANALYSIS

By Component Insights

The services segment held 42.3% of the cybersecurity market share in 2025, with the growing complexity of cyber threats and the increasing need for specialized expertise to design, implement, and manage security frameworks. Unlike off-the-shelf hardware or software, cybersecurity services by encompass managed security services (MSS), consulting, integration, and incident response offer tailored, adaptive solutions that align with dynamic threat landscapes and regulatory environments. The escalating demand for managed detection and response (MDR) services is also prompting the growth of the cybersecurity market. Furthermore, the U.S. Department of Homeland Security disclosed that 82% of infrastructure operators now outsource at least one cybersecurity function, reflecting institutional dependence on external expertise. Another pivotal factor is the regulatory burden across jurisdictions. As per the International Association of Privacy Professionals, organizations spend an average of $3.2 million annually on compliance-related consulting and audit services.

The software segment is projected to expand at a CAGR of 14.8% from 2025 to 2033 with the rapid adoption of cloud security software, particularly cloud access security brokers (CASBs) and secure web gateways (SWGs). This has led to a 60% year-over-year increase in CASB deployments, as noted by the Cloud Security Alliance in 2023. Additionally, the proliferation of remote work has intensified reliance on endpoint protection platforms (EPP) and extended detection and response (XDR) solutions. As per the Ponemon Institute’s 2023 State of Endpoint Security Report, organizations using AI-powered endpoint software reduced breach incidents by 48% compared to those relying on traditional antivirus tools. Microsoft’s 2023 Digital Defense Report revealed that AI-driven threat detection tools blocked 32 billion phishing attempts and 1.8 billion malware downloads monthly across its ecosystem. These capabilities enable real-time anomaly identification and automated response, reducing reliance on manual intervention.

By Software Insights

The firewall solutions segment was the largest by occupying 28.3% of the cybersecurity market share in 2025 with the persistent reliance on network perimeter defense, particularly in hybrid and multi-cloud environments. According to the Enterprise Strategy Group, 74% of enterprises still consider the network layer the most point for threat interception. Palo Alto Networks’ 2023 Unit 42 report indicated that NGFWs blocked an average of 1.2 million threats per enterprise monthly, including ransomware and command-and-control communications. The U.S. Cybersecurity and Infrastructure Security Agency (CISA) requires federal agencies to deploy NGFWs at all network boundaries, a directive mirrored in sectors like energy and finance. In the banking industry, the Financial Conduct Authority found that 89% of institutions upgraded to NGFWs between 2021 and 2023 to comply with enhanced cyber resilience standards.

The threat intelligence platform (TIP) segment is anticipated to grow with an estimated CAGR of 19.4% from 2025 to 2033, with the growing sophistication of cyber adversaries utilizing stealthy, targeted campaigns. As per the 2025 Mandiant M-Trends Report, the median dwell time of attackers in enterprise networks was 79 days in 202,3 with the need for early detection through predictive intelligence. TIPs aggregate and correlate data from global threat feeds, dark web monitoring, and internal logs, enabling organizations to identify indicators of compromise (IOCs) before breaches occur. According to IBM Security, enterprises using integrated threat intelligence reduced incident response time by 52%. Additionally, the U.S. Department of Defense’s Cyber Threat Intelligence Integration Center (CTIIC) has mandated TIP deployment across all defense contractors handling classified data, accelerating adoption in the public sector. CrowdStrike’s 2023 Global Threat Landscape Report revealed that organizations leveraging TIPs detected 70% more zero-day exploits than those relying on standalone tools.

REGIONAL ANALYSIS

North America Cybersecurity Market Insights

North America was the largest contributor to the global cybersecurity market with 38.3% of the share in 2025. The U.S. federal government allocated $11.2 billion for cybersecurity in fiscal year 2024, a 14% increase from the previous year, as disclosed by the Office of Management and Budget. This investment fuels initiatives like the Cybersecurity and Infrastructure Security Agency’s (CISA) Joint Cyber Defense Collaborative, which coordinates threat response across 1,200 public and private entities. The proliferation of ransomware attacks, rising by 47% in 2023, as per the FBI’s Internet Crime Complaint Cente,r has further intensified defensive spending. Additionally, the Securities and Exchange Commission’s new rules requiring public companies to disclose cyber incidents within four business days have elevated boardroom accountability.

Europe Cybersecurity Market Insights

Europe cybersecurity market held 26.4% of the share in 2025. The European Union has emerged as a global standard-setter in digital security, with directives like NIS2 mandating minimum security requirements for over 30,000 essential and digital service providers. According to the European Union Agency for Cybersecurity (ENISA), EU member states collectively invested €18.7 billion in cybersecurity in 2023, a 22% year-on-year increase. The UK, despite Brexit, remains a cybersecurity powerhouse, home to over 1,200 security firms and contributing £10.4 billion to the national economy in 2023, according to the UK Cyber Security Council. The European Central Bank’s 2023 cyber resilience stress test revealed that 92% of major EU banks had upgraded their incident response protocols, reflecting institutional preparedness.

Asia-Pacific Cybersecurity Market Insights

Asia-Pacific cybersecurity market is anticipated to grow with prominent opportunities during the forecast period. According to the Indian Computer Emergency Response Team (CERT-In), cyber incidents in India surged to 1.6 million in 2023, a 37% increase from 2022. Japan, meanwhile, has strengthened its Cybersecurity Strategy Headquarters, mandating all infrastructure operators to conduct annual cyber drills, as disclosed by the National Center of Incident Readiness and Strategy for Cybersecurity (NISC). China’s cybersecurity expenditures exceeded $12 billion in 2023, driven by the Cybersecurity Law and the expansion of its Great Firewall, according to the China Internet Network Information Center. Australia has also intensified efforts, with the Australian Cyber Security Centre reporting a 26% rise in ransomware attacks targeting small and medium enterprises.

Latin America Cybersecurity Market Insights

Latin America cybersecurity market growth is anticipated to grow steadily in the coming years owing to the rising digital banking adoption, increasing cybercrime rates, and nascent regulatory frameworks. According to the Brazilian Internet Steering Committee (CGI.br), phishing attacks increased by 58% in 2023, with 67% of businesses experiencing at least one breach.

Middle East and Africa Cybersecurity Market Insights

The Middle East and Africa cybersecurity market is likely to grow in the coming years. The UAE and Saudi Arabia are at the forefront, integrating cybersecurity into their national digital transformation agendas. Saudi Arabia’s Vision 2030 includes a $1.5 billion fund for cybersecurity startups and talent development, as disclosed by the National Cybersecurity Authority (NCA). Israel, though geographically small, exerts outsized influence, with its cybersecurity sector generating $12 billion in revenue in 2023 and hosting over 500 active startups, according to the Israel National Cyber Directorate.

COMPETITIVE LANDSCAPE

The competition in the cybersecurity market is marked by rapid innovation, strategic consolidation, and a constant race to anticipate evolving threat vectors. Market leaders differentiate themselves not merely through product functionality but through ecosystem integration, scalability, and intelligence depth. The shift from reactive to proactive security models has intensified rivalry, with companies striving to embed artificial intelligence and automation into every layer of defense. Smaller, agile firms often pioneer novel approaches in areas like zero-trust architecture and identity governance, prompting larger vendors to acquire or emulate their technologies. Geopolitical tensions and rising cyber warfare incidents have elevated national security concerns, increasing public-sector contracts and influencing private-sector priorities. Cloud security, endpoint resilience, and identity management have become battlegrounds for dominance, with vendors competing on interoperability, ease of deployment, and operational efficiency. The absence of standardized frameworks across regions further complicates the landscape, requiring companies to tailor solutions to diverse regulatory environments. Customer trust, built through transparency, incident response efficacy, and thought leadership, plays a decisive role in market positioning.

KEY MARKET PLAYERS

A few of the companies playing a notable role in the global cybersecurity market include

- Broadcom (Symantec Corporation)

- Cisco Systems, Inc.

- Check Point Software Technology Ltd.

- CrowdStrike

- IBM

- McAfee LLC

- Palo Alto Networks, Inc.

- Trend Micro Incorporated

- Norton LifeLock

- Rapid7

- Micro Focus

TOP LEADING PLAYERS IN THE MARKET

- Palo Alto Networks has established itself as a global leader in cybersecurity by pioneering a platform-centric approach that integrates network, cloud, endpoint, and identity security under a unified architecture. The company’s commitment to innovation is evident in its continuous expansion of AI-driven threat detection and automated response capabilities. By emphasizing zero-trust frameworks and delivering proactive defense mechanisms, Palo Alto Networks enables organizations to anticipate and neutralize sophisticated threats before they escalate. Its global threat intelligence network, leveraging real-time data from millions of endpoints, enhances the efficacy of its security offerings. The company’s strategic acquisitions have further strengthened its portfolio, allowing seamless integration across hybrid environments.

- CrowdStrike has redefined endpoint protection through its cloud-native Falcon platform, which delivers real-time visibility and response across distributed enterprise environments. The company’s lightweight agent architecture enables rapid deployment and continuous monitoring without degrading system performance. CrowdStrike’s strength lies in its ability to correlate global threat intelligence with behavioral analytics, allowing for immediate identification of adversarial activities. Its focus on identity protection and XDR (Extended Detection and Response) has positioned it as a leader in next-generation security. The company’s proactive threat hunting and adversary disruption initiatives have set new benchmarks in incident response. Its influence extends beyond technology, as it regularly publishes authoritative threat intelligence reports that inform global cybersecurity strategies and policy decisions.

- Microsoft leverages its vast digital ecosystem to embed security deeply within its cloud, productivity, and identity platforms. The company provides organizations with inherently secure environments rather than bolt-on solutions by integrating cybersecurity into core services such as Azure, Microsoft 365, and Active Directory. Microsoft’s approach emphasizes identity as the new perimeter, with advanced conditional access and multi-factor authentication capabilities forming the backbone of its zero-trust model. The company’s unparalleled telemetry from billions of devices and user interactions enables highly accurate threat prediction and response. Its collaboration with governments, enterprises, and cybersecurity alliances enhances global defense coordination. Microsoft’s commitment to transparency, threat intelligence sharing, and responsible disclosure has solidified its role as a trusted steward of digital safety, which is making it a dominant force in shaping the future of secure computing.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

- One of the most prominent strategies employed by leading cybersecurity firms is the development of integrated security platforms that unify disparate tools under a single operational umbrella. This approach eliminates silos between endpoint, network, cloud, and identity protection, enabling streamlined threat detection and response.

- Another key strategy is the strategic acquisition of niche innovators specializing in emerging domains such as identity protection, AI-driven analytics, and attack surface management. These acquisitions allow established players to rapidly incorporate cutting-edge capabilities without internal development delays.

Global Cybersecurity Market News

- In March 2024, Palo Alto Networks acquired Checkmarx, a leader in software security testing, to enhance its application security portfolio and strengthen DevSecOps integration across enterprise environments.

- In January 2024, CrowdStrike announced the launch of its Identity Threat Protection module, expanding its Falcon platform to include real-time monitoring and response for identity-based attacks.

- In February 2024, Microsoft integrated its Microsoft Defender suite with third-party security vendors through the Microsoft Intelligent Security Association by enabling broader ecosystem collaboration and threat intelligence sharing.

- In May 2024, Fortinet expanded its Security Fabric architecture with new AI-driven SOC capabilities, which is improving automated threat detection and response for global enterprise clients.

- In June 2024, Cisco is introducing its zero-trust offerings by introducing identity-centric policy enforcement across its SecureX platform by enhancing access control for hybrid workforce environments.

MARKET SEGMENTATION

This research report on the global cybersecurity market is segmented and sub-segmented into the following categories.

By Component

- Hardware

- Software

- Services

By Software

- IAM

- Encryption

- Firewall

- APT

- Threat Intelligence Platform

- Network Access Control

- IDS/IPS

- Others

By Security Type

- Network Security

- Endpoint Security

- Application Security

- Cloud Security

- Others

By Deployment Mode

- Cloud

- On-Premises

By Organization Size

- Large Enterprises

- Small & Medium Size Enterprises

By End-User

- Aerospace & Defense

- Government

- BFSI

- IT & Telecommunication

- Healthcare

- Retail

- Manufacturing

- Energy & Utilities

- Telecommunications

- Media and Entertainment

- Others

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa